|

시장보고서

상품코드

1683760

북미의 건축용 코팅 : 시장 점유율 분석, 산업 동향, 성장 예측(2025-2030년)North America Architectural Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

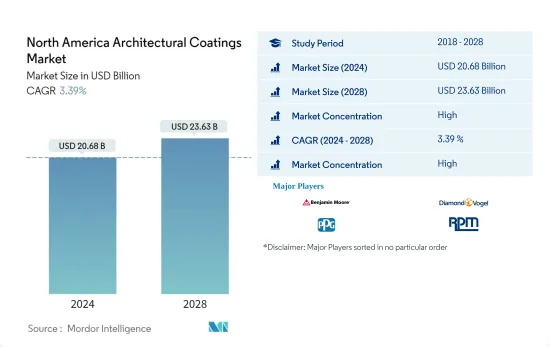

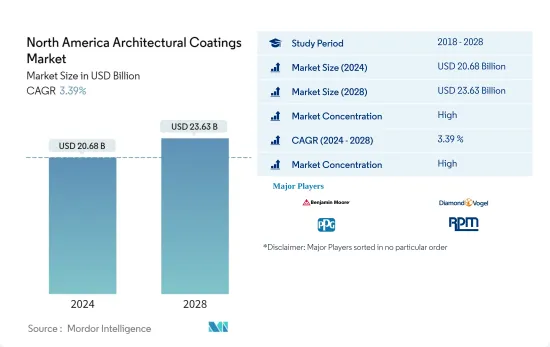

북미의 건축용 코팅 시장 규모는 2024년에 206억 8,000만 달러에 달했고, 2028년에는 236억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2024년-2028년)의 CAGR은 3.39%를 나타낼 것으로 전망됩니다.

주요 하이라이트

- 중기적으로 이 지역의 건설 활동 증가는 예측 기간 동안 북미 건축용 코팅 시장 성장을 이끄는 주요 요인입니다.

- 한편 원자재 가격 및 공급망 중단과 함께 이 지역의 환경 문제 증가는 예측 기간 동안 대상 산업의 성장을 제한 할 것으로 예상되는 주요 요인입니다.

- 그럼에도 불구하고 건축용 페인트 및 코팅의 지속 가능성 증가는 곧 글로벌 시장에 수익성 높은 성장 기회를 창출할 것으로 보입니다.

- 미국은 이 지역의 다른 국가에 비해 주택 재고와 리모델링 지수가 높아 건축용 코팅제 소비를 선도하는 국가입니다.

북미의 건축용 코팅 시장 동향

주거 부문이 시장을 독점할 전망

- 건축용 페인트 및 코팅에는 주택 내부 및 외부 페인트, 프라이머, 바니시, 실러 및 얼룩이 포함됩니다.

- 이 페인트와 코팅은 에너지 효율적인 건물 인클로저에 필수적인 공기 차단막을 제공하는 데 매우 중요합니다. 주거용 건물에서 건축용 코팅이 제공하는 공기 차단막은 건물을 통과하는 공기의 흐름을 차단하고 구조를 보호하며 냉난방 시스템의 효율을 높입니다.

- 이러한 에어 배리어는 모든 친환경 건물 표준에서 요구하는 에너지 효율 성능 요건에도 기여합니다.

- 북미 지역에서는 주택 건설을 위한 부동산 시장의 정부 지출 증가와 고급 주거용 주택에 대한 수요 증가가 시장 성장에 도움이 될 것으로 보입니다. 또한 부동산 비용 상승, 특히 이 지역의 단독 주택 및 다층 아파트 개발로 인해 건축용 페인트 및 코팅 시장이 더욱 활성화될 것으로 예상됩니다.

- 게다가 가계 소득 수준의 증가와 농촌에서 도시로 이주하는 인구가 결합되어 북미 지역의 주택 건설 부문에 대한 수요를 계속 견인할 것으로 예상됩니다. 공공 및 민간 부문 모두에서 저렴한 주택에 대한 관심이 높아지면서 이 지역의 주택 건설 부문이 성장하고 있습니다.

- 캐나다 건설 협회에 따르면, 건설 부문은 캐나다 최대의 고용주 중 하나이며 캐나다 경제의 성공에 크게 기여하고 있습니다. 이 산업은 연간 약 1,410억 달러를 창출해 국내총생산(GDP)의 7.5%를 차지합니다.

- 또한 StatCan에 따르면 2023년 2분기에 약 64,042채의 신규 주택이 착공되는 등 신규 주택 건설이 증가하는 추세를 보이고 있습니다.

- 코로나19로 인한 캐나다의 경제 회복이 계속되면서 공급망 차질과 인력 부족으로 인해 대부분의 산업에서 어려움을 겪고 있으며 건설 부문도 예외는 아닙니다. 하지만 주거용 및 비주거용 투자는 팬데믹 초기 침체에서 점점 회복되고 있습니다.

- 2022년 투자 증가로 인해 2023년에는 페인트 소비가 높을 것으로 예상됩니다. 이러한 성장 시나리오는 2024년 정부의 이민 목표 상향 조정으로 인해 2024년까지 지속될 것으로 예상했습니다.

- 위의 점에서 주거 부문이 예측 기간 동안 북미의 건축용 코팅 시장에서 지배적인 역할을 할 것으로 추론 할 수 있습니다.

국가별로는 미국이 최대

- 미국은 세계에서 가장 크고 강력한 경제대국 중 하나입니다. 그러나 2020년 미국의 GDP는 팬데믹의 심각한 영향을 받아 -2.8%로 감소했습니다. 또한 2021년에는 5.9%의 성장률을 기록했으며, 2022년에는 약 2.1%를 기록했습니다. 2023년에는 GDP가 약 1.6% 성장할 것으로 IMF는 예상했습니다.

- 미국은 760만명 이상의 직원을 보유한 거대한 건설 부문을 자랑합니다. 상업용 및 주거용 건설 분야에서 두드러진 역할을 하는 미국 건설 부문은 미국 경제에 크게 기여하고 있습니다. 미국의 건설 활동이 증가함에 따라 미국 내 건축용 페인트 및 코팅제 소비가 증가할 것으로 예상됩니다.

- 미국에서는 2020년에 주거용 페인트 소비가 크게 증가했습니다. 이는 사람들이 새로운 재택근무 환경을 구축하기 위해 집을 리모델링하면서 특히 DIY 페인트 시장에서 가장 높은 소비 증가율을 보인 주거용 페인트 부문 덕분입니다.

- 미국은 세계 최대 건설 산업 중 하나이며 2021년에는 16억 3,000만 달러, 2022년에는 17억 9,000만 달러로 평가됩니다. 이 나라는 세계 건설 지출의 약 10%를 차지합니다. 게다가 미국의 상업건설액은 2021년 949억 5,000만 달러에 비해 2022년에는 1,147억 9,000만 달러에 이릅니다.

- 미국 인구조사국에 따르면 2022년 민간건설액은 1조 4,292억달러로 2021년 1조 2,795억달러를 11.7%(-1.0%) 웃돌았습니다. 2022년 주택 건설 지출은 8,991억달러로, 2021년 7,937억달러에서 13.3%(-2.1%) 증가했으며, 비주택 건설 지출은 5,301억달러로, 2021년 4,858억달러에서 9.1%(-2.1%) 감소했습니다.

- 또한 이 나라는 또한 기존 공항을 업그레이드하고 있습니다. 예정된 주요 공항 확장 프로젝트에는 시카고 오헤어 국제공항의 활주로 시스템 재구성, 덴버 국제공항의 신규 발권 구역 건설 및 신규 보안 검색대 추가, 휴스턴 조지 부시 인터콘티넨탈 공항의 신규 국제선 터미널 건설, 2. 25마일 자동화 피플 무버 및 로스앤젤레스 국제공항의 새로운 주차 시설, 올랜도 국제공항의 철도 시스템과 연계하기 위한 15개의 게이트 및 복합 터미널 시설 추가, 뉴욕 라과디아 공항의 새로운 터미널 건설, 샌프란시스코 국제공항의 국제선 터미널 용량 2배 확대 등 다양한 프로젝트가 진행 중입니다.

- 따라서 앞서 언급한 모든 요인이 향후 몇 년 동안 미국의 건축용 페인트 및 코팅 수요에 영향을 미칠 것으로 보입니다.

북미의 건축용 코팅 산업 개요

북미의 건축용 코팅 시장은 통합된 특성을 가지고 있습니다. 이 시장의 주요 기업(특정한 순서 없음)에는 벤자민 무어사, 다이아몬드 포겔사, PPG 인더스트리즈사, RPM 인터내셔널사, 샤윈 윌리엄스사 등이 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 북미의 건설 활동 증가

- 억제요인

- 이 지역의 환경 문제 증가

- 원자재 가격 및 공급망 중단란

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 최종 사용자 산업

- 상업

- 주거

- 기술

- 수성

- 용매 기반

- 수지

- 아크릴

- 알키드

- 폴리우레탄

- 에폭시

- 폴리에스테르

- 기타 수지 유형

- 지역

- 미국

- 캐나다

- 멕시코

- 기타 북미

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 분석

- 주요 기업의 전략

- 기업 프로파일

- Beckers Group

- Benjamin Moore & Co.

- Champion Coat Pinturas Y Recubrimientos

- Cloverdale Paint Inc.

- COREV DE MEXICO

- Diamond Vogel

- DUNN-EDWARDS Corporation

- JOTUN

- Kelly-moore Paints

- Masco Corporation

- Micca Paint Inc.

- Pinturas Acuario

- Pinturas Berel SA De Cv

- PPG Industries Inc.

- Pinturas PRISA

- RPM International Inc.

- Selectone Paints Inc.

- Societe Laurentide

- The Sherwin-williams Company

- Farrow & Ball Ltd

- Fine Paints of Europe

제7장 시장 기회와 앞으로의 동향

- 건축용 코팅 및 코팅에서의 지속가능성 증가

The North America Architectural Coatings Market size is estimated at USD 20.68 billion in 2024, and is expected to reach USD 23.63 billion by 2028, growing at a CAGR of 3.39% during the forecast period (2024-2028).

Key Highlights

- Over the medium term, the rising construction activities in the region are the major factors driving the North American architectural coatings market growth during the forecast period.

- On the other hand, the growing environmental concerns in the region, coupled with raw material prices and supply chain disruptions, are key factors anticipated to restrain the growth of the target industry over the forecast period.

- Nevertheless, the growing sustainability in architectural paints and coatings is likely to create lucrative growth opportunities for the global market soon.

- The United States is the leading country in architectural coatings consumption due to its higher housing stocks and remodeling index compared to other countries in the region.

North America Architectural Coatings Market Trends

Residential Segment is Expected Dominate the Market

- Architectural paints and coatings include interior and exterior house paints, primers, varnishes, sealers, and stains.

- These paints and coatings are critical in providing air barriers essential for energy-efficient building enclosures. In residential buildings, air barriers provided by architectural coatings stop the flow of air through the building, protect the structure, and increase the efficiency of heating and cooling systems.

- These air barriers also contribute to the energy efficiency performance requirements found in all green building standards.

- In the North American region, the increased government spending in the real estate market for residential construction and the growing demand for high-class residential homes are likely to benefit the market's growth. In addition, rising real estate costs, particularly the development of single-family homes and multistory apartments in the region, are anticipated to boost the architectural paints and coatings market further.

- Moreover, the rising household income levels, combined with the population migrating from rural to urban areas, are expected to continue to drive the demand for the residential construction sector in North America. The increased focus on affordable housing by both the public and private sectors is driving the growth in the residential construction sector in the region.

- According to the Canadian Construction Association, the construction sector is one of Canada's largest employers and a major contributor to the country's economic success. The industry generates about USD 141 billion annually and contributes 7.5% of the country's gross domestic product (GDP).

- Further, according to StatCan, there was an increasing trend in new housing constructions in Q2 2023, where around 64,042 units of new housing were started.

- As Canada's economic recovery from COVID-19 continues, supply chain disruptions and labor shortages contribute to the challenges felt across most industries, and the construction sector is no exception. However, residential and non-residential investments are increasingly recovering from the early pandemic slowdown.

- Due to increased investments in 2022, the consumption of paints is expected to be high in 2023. This growth scenario is further expected to continue till 2024 due to the government's upgradation of immigration targets in 2024.

- From the above points, it can be inferred that the residential segment is set to play the dominant role in the North American architectural coatings market during the forecast period.

United States is the largest segment by Country.

- The United States is one of the world's largest and most powerful economies. However, the country's GDP declined to -2.8% in 2020, severely impacted by the pandemic. Furthermore, the country recorded a growth of 5.9% in 2021, and it reached about 2.1% in 2022. In 2023, the IMF has estimated that the GDP would grow by about 1.6%.

- The United States boasts a colossal construction sector with over 7.6 million employees. Playing a prominent role in commercial and residential construction, the US construction sector significantly contributes to the country's economy. Due to increasing construction activities in the United States, the consumption of architectural paints and coatings in the country is expected to increase.

- In the United States, residential paint consumption grew substantially in 2020. This was due to the residential repaint segment, which saw the highest jump in consumption, especially in the DIY paint market, as people remodeled their homes to build new work-from-home environments.

- The United States has one of the world's largest construction industries, valued at USD 1,630 million in 2021 and USD 1,790 million in 2022. The country accounts for around 10% of global construction spending. Furthermore, the commercial construction value in the United States was registered at USD 114.79 billion in 2022, compared to USD 94.95 billion in 2021.

- According to the US Census Bureau, the value of private construction in 2022 was USD 1,429.2 billion, 11.7% (+- 1.0%) higher than the USD 1,279.5 billion in 2021. Residential construction spending in 2022 was USD 899.1 billion, up by 13.3% (+-2.1%) from USD 793.7 billion in 2021, while non-residential construction spending amounted to USD 530.1 billion, down by 9.1% (+-2.1%) from USD 485.8 billion in 2021. 1.0%).

- Additionally, the country is upgrading its existing airports. Some of the upcoming major airport expansion projects include the reconfiguration of the runway system at Chicago O'Hare International Airport, the construction of new ticketing areas and the addition of new security checkpoints at the Denver International Airport, the construction of a new international terminal at Houston George Bush Intercontinental Airport, the construction of a 2.25-mile automated people mover and new parking facilities at Los Angeles International Airport, the addition of 15 gates and an Intermodal Terminal Facility to link with rail systems at Orlando International Airport, building a new terminal at New York LaGuardia Airport, doubling the capacity of San Francisco International Airport's international terminal, and many more.

- Therefore, all the aforementioned factors are likely to affect the demand for architectural paints and coatings in the country in the coming years.

North America Architectural Coatings Industry Overview

The North American architectural coatings market is consolidated in nature. Some of the major players in the market (in no particular order) include Benjamin Moore & Co., Diamond Vogel, PPG Industries Inc., RPM International Inc., and The Sherwin-Williams Company, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET Dynamics

- 4.1 Drivers

- 4.1.1 Growing Construction Activities In North America

- 4.2 Restraints

- 4.2.1 Growing Environmental Concerns In the Region

- 4.2.2 Raw Material Prices and Supply Chain Disruptions

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products And Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 End-user Industry

- 5.1.1 Commercial

- 5.1.2 Residential

- 5.2 Technology

- 5.2.1 Water Borne

- 5.2.2 Solvent Borne

- 5.3 Resin

- 5.3.1 Acrylic

- 5.3.2 Alkyd

- 5.3.3 Polyurethane

- 5.3.4 Epoxy

- 5.3.5 Polyester

- 5.3.6 Other Resin Types

- 5.4 Geography

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

- 5.4.4 Rest of North America

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%) Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 Beckers Group

- 6.4.2 Benjamin Moore & Co.

- 6.4.3 Champion Coat Pinturas Y Recubrimientos

- 6.4.4 Cloverdale Paint Inc.

- 6.4.5 COREV DE MEXICO

- 6.4.6 Diamond Vogel

- 6.4.7 DUNN-EDWARDS Corporation

- 6.4.8 JOTUN

- 6.4.9 Kelly-moore Paints

- 6.4.10 Masco Corporation

- 6.4.11 Micca Paint Inc.

- 6.4.12 Pinturas Acuario

- 6.4.13 Pinturas Berel SA De Cv

- 6.4.14 PPG Industries Inc.

- 6.4.15 Pinturas PRISA

- 6.4.16 RPM International Inc.

- 6.4.17 Selectone Paints Inc.

- 6.4.18 Societe Laurentide

- 6.4.19 The Sherwin-williams Company

- 6.4.20 Farrow & Ball Ltd

- 6.4.21 Fine Paints of Europe

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Sustainability In Architectural Paints and Coatings

샘플 요청 목록