|

시장보고서

상품코드

1684066

방수제 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Waterproofing Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

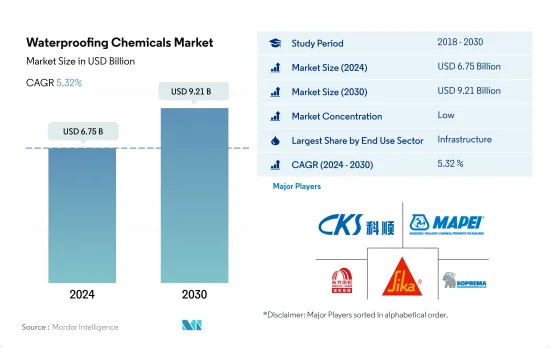

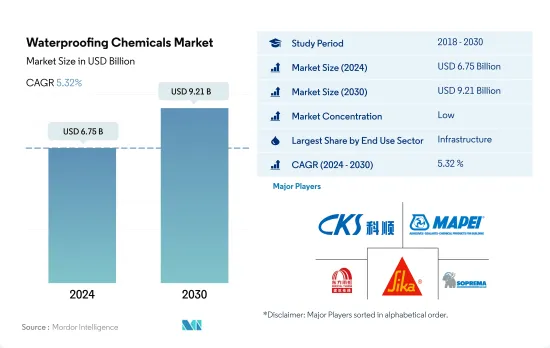

방수제 시장 규모는 2024년에 67억 5,000만 달러로 평가되었고, 2030년에는 92억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2024-2030년) 중 CAGR 5.32%로 성장할 전망입니다.

인프라 건설 프로젝트 투자 증가로 방수제 수요를 끌어올릴 가능성이 높습니다.

- 2022년 세계 방수제 소비량은 인프라 및 상업 건설 부문 수요 증가에 견인되어 금액 기준으로 4.65% 성장했습니다. 2023년에는 세계 방수 솔루션 시장의 약 26.43%를 차지한 것으로 평가됩니다.

- 인프라 부문이 최대 소비자이며 2023년에는 약 31.05%를 차지했습니다. 세계 인프라 지출은 건설 프로젝트 투자 증가로 2023년부터 2030년까지 3,670억 달러 증가할 것으로 보입니다. 예를 들어 영국 정부는 2030년까지 5G 통신 인프라 강화를 목표로 무선 인프라 전략에 1억 9,100만 달러를 할당했습니다. 또한 인도는 2030년까지 인프라 정비에 약 4조 5,000억 달러를 투자할 계획입니다. 그 결과 세계 인프라 분야를 위한 방수제 시장은 2030년까지 6억 6,200만 달러에 이를 것으로 예측됩니다.

- 상업 분야는 예측 기간 중 CAGR이 6.13%로 예측되어 조사 대상 시장에서 가장 급성장하고 있는 소비자가 될 전망입니다. 경제 확대로 사무실, 호텔, 소매몰 등 상업 공간에 대한 수요가 높아지고 있습니다. 게다가 미국에서만 예측 기간 말까지 46억 1,000만 평방피트의 사무실 공간이 필요할 것으로 예상됩니다. 그 결과 세계의 상업 부문 방수제 시장은 2023년 17억 달러에서 2030년 26억 달러로 급증할 것으로 예상됩니다.

아시아태평양과 북미에서 건설 활동이 빠르게 진행되어 방수제 수요가 세계적으로 높아질 것으로 예측됩니다.

- 방수제는 건축물의 설계 및 건설의 모든 측면에서 필수적이며 물의 침입을 방지해야 하는 경우에 사용됩니다. 2022년 세계 방수제 시장은 2021년에 비해 금액으로 4.65%의 성장을 보였습니다. 중동 및 아프리카의 방수제 시장은 2021년부터 2022년까지 금액으로 5.91%의 가장 높은 성장을 기록했고, 같은 기간 금액으로 5.83% 성장한 북미가 뒤를 이었습니다. 게다가 2023년 세계의 방수제 시장은 2022년에 비해 수량으로 5.13%의 성장이 평가되었습니다.

- 2022년에는 아시아태평양이 시장을 크게 지배했으며 금액 기준으로 시장 점유율의 45%를 차지했습니다. 중국, 일본, 인도 등의 국가들이 이 지역의 방수제 수요에 강한 영향력을 전개했습니다. 중국의 교통 인프라에 대한 공공 지출은 2021년 1,576억 달러에 비해 2022년에는 1,656억 달러에 달했습니다. 마찬가지로, 일본에서는 제조 시설의 건설이 증가하고, 인도에서는 도로, 철도, 고속도로를 통해 연결성을 높인다는 구상이 있어, 이 지역 건설 분야 성장을 뒷받침하고 있습니다. 이러한 개발은 건축 및 건설용 방수제의 소비를 뒷받침하고 있습니다.

- 북미의 방수제 시장은 예측 기간 동안 금액 기준으로 가장 빠른 CAGR 5.96%를 기록한 다음 아시아태평양의 CAGR 5.47%가 계속될 것으로 예상됩니다. 정부 자금 및 외국 직접 투자에 지지된 고투자 프로젝트가 이 지역의 주택, 인프라, 상업 건설 활동을 활발하게 할 것으로 예상됩니다. 그 결과, 방수제 수요가 증가할 것으로 예측됩니다.

세계의 방수제 시장 동향

아시아태평양의 대규모 오피스 빌딩 건설 프로젝트의 급증으로 세계 상업 건축용 바닥 면적이 증가할 전망

- 2022년 세계 상업 건축용 신규 바닥 면적은 전년대비 0.15%의 소폭 성장을 이뤘습니다. 유럽은 2030년 이산화탄소 배출 목표에 맞추어 에너지 효율적인 오피스 빌딩을 추진하는 움직임이 원동력이 되고 있습니다. 직원의 사무실 복귀에 따라 유럽 기업은 임대 계약을 재개하고 2022년에는 450만 평방피트의 신규 오피스 건설에 박차를 가했습니다. 이 기세는 2023년에도 계속되어 세계 성장률은 4.26%로 평가되었습니다.

- COVID-19의 유행은 노동력과 자재 부족을 일으켜 상업 시설 건설 프로젝트의 취소와 지연을 초래했습니다. 그러나 폐쇄가 완화되고 건설 활동이 재개됨에 따라 2021년 세계 상업 시설의 신규 바닥 면적은 11.11% 급증하였고 아시아태평양이 20.98%의 성장률로 선도했습니다.

- 향후 세계 상업 시설의 신규 바닥 면적 CAGR은 4.56%로 전망됩니다. 아시아태평양의 CAGR은 5.16%로 예측되며 다른 지역을 능가할 것으로 예상됩니다. 이 성장의 원동력이 되고 있는 것은 중국, 인도, 한국, 일본에서 상업 시설 건설 프로젝트의 활성화입니다. 특히 베이징, 상하이, 홍콩, 타이베이 등 중국의 주요 도시에서는 A급 사무실 공간 건설이 가속화되고 있습니다. 또한 인도에서는 2023년부터 2025년까지 상위 7개 도시에서 약 2,325만 평방피트에 이르는 약 60개의 쇼핑몰이 오픈할 예정입니다. 아시아태평양 전역의 이러한 노력을 합산하면 2030년까지 상업 시설의신규 바닥 면적은 2022년 대비 15억 6,000만 평방피트 증가한 것으로 평가되었습니다.

세계의 주택 부문을 뒷받침하는 저렴한 주택 계획에 대한 정부 투자 증가로 남미 주택 건설이 가장 빠르게 성장할 것으로 추정됩니다.

- 2022년 세계 주택 건축의 신규 바닥 면적은 2021년 대비 약 2억 8,900만 평방피트 감소했습니다. 이는 토지 부족, 노동력 부족, 건축 자재 가격의 지속 불가능한 급등으로 인한 주택 위기 때문입니다. 이 위기는 아시아태평양에 심각한 영향을 미쳤으며, 2022년 신규 바닥 면적은 2021년 대비 5.39% 감소했습니다. 그러나 2023년에는 2030년까지 30억 명을 수용할 수 있는 저렴한 주택을 새로 건설하기 위한 자금을 조달할 수 있는 정부 투자로, 세계 신규 바닥 면적은 2022년 대비 3.31% 증가한 것으로 평가되어 보다 밝은 전망이 기대됩니다.

- COVID-19의 유행은 경기 감속을 일으켜, 그 때문에 많은 주택 건설 프로젝트가 중지 또는 연기되어 2020년 세계의 신규 바닥 면적은 2019년에 비해 4.79% 감소했습니다. 2021년에 규제가 해제되어 주택 프로젝트에 대한 침체된 수요가 해방되면 신규 바닥 면적은 2020년 대비 11.22% 증가했으며, 유럽이 18.28%로 가장 높은 성장세를 보였으며, 남미가 2021년에 2020년 대비 17.36% 증가했습니다.

- 세계의 주택용 신규 바닥 면적은 예측 기간 동안 CAGR 3.81%로 성장을 지속하고, 남미가 가장 빠른 CAGR 4.05%로 발전할 것으로 예측됩니다. 브라질의 Minha Casa Minha Vida는 2023년에 발표되었으며, 정부는 저소득 가구에 저렴한 주택을 제공하기 위해 19억 8,000만 달러의 투자를 계획하고 있습니다.

방수제 산업 개요

방수제 시장은 세분화되어 상위 5개사에서 38.48%를 차지하고 있습니다. 이 시장 주요 기업은 다음과 같습니다. Keshun Waterproof Technology, MAPEI SpA, Oriental Yuhong, Sika AG 및 Soprema.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 용도 분야의 동향

- 상업

- 산업 및 시설

- 인프라

- 주택

- 주요 인프라 프로젝트(현재 및 발표됨)

- 규제 프레임워크

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 최종 용도 분야별

- 상업

- 산업 및 시설

- 인프라

- 주택

- 기술 분야별

- 에폭시계

- 폴리우레탄계

- 수성

- 기타 기술

- 지역별

- 아시아태평양

- 국가별

- 호주

- 중국

- 인도

- 인도네시아

- 일본

- 말레이시아

- 한국

- 태국

- 베트남

- 기타 아시아태평양

- 유럽

- 국가별

- 프랑스

- 독일

- 이탈리아

- 러시아

- 스페인

- 영국

- 기타 유럽

- 중동 및 아프리카

- 국가별

- 사우디아라비아

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

- 북미

- 국가별

- 캐나다

- 멕시코

- 미국

- 남미

- 국가별

- 아르헨티나

- 브라질

- 기타 남미

- 아시아태평양

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Ardex Group

- Fosroc, Inc.

- Hongyuan Waterproof Technology Group Co., Ltd.

- Keshun Waterproof Technology Co., ltd.

- MAPEI SpA

- Oriental Yuhong

- Saint-Gobain

- Sika AG

- Soprema

- Standard Industries Inc.

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Waterproofing Chemicals Market size is estimated at 6.75 billion USD in 2024, and is expected to reach 9.21 billion USD by 2030, growing at a CAGR of 5.32% during the forecast period (2024-2030).

Rising investment in infrastructure construction projects is likely to boost the demand for waterproofing chemicals

- The global consumption of waterproofing chemicals grew by 4.65% in value in 2022, driven by rising demand from the infrastructure and commercial construction sectors. The market studied was projected to make up approximately 26.43% of the global waterproofing solutions market in 2023.

- The infrastructure sector stands as the largest consumer, accounting for about 31.05% in 2023. Global infrastructure spending is set to rise by USD 367 billion from 2023 to 2030, fueled by increased investments in construction projects. For instance, the Government of the United Kingdom has allocated USD 191 million to its Wireless Infrastructure Strategy, targeting enhanced 5G telecommunication infrastructure by 2030. In addition, India plans to invest around USD 4.5 trillion in infrastructure development by 2030. Consequently, the global waterproofing chemicals market for the infrastructure sector is forecasted to reach USD 662 million by 2030.

- The commercial sector is poised to be the fastest-growing consumer in the market studied, with a projected CAGR of 6.13% during the forecast period. The expanding economy has heightened the demand for commercial spaces, including offices, hotels, and retail malls. Moreover, the United States alone is expected to require 4.61 billion square feet of office space by the end of the forecast period. As a result, the global market for waterproofing chemicals in the commercial sector is anticipated to surge from USD 1.7 billion in 2023 to USD 2.6 billion in 2030.

Fast-paced construction activities in the Asia-Pacific and North America predicted to bolster the demand for waterproofing chemicals, globally

- Waterproofing chemicals are essential to all aspects of building design and construction and find applications where a need to prevent water ingress is required. In 2022, the global waterproofing chemicals market witnessed a growth of 4.65% in value compared to 2021. The Middle East & African market for waterproofing chemicals recorded the highest growth of 5.91% in value from 2021 to 2022, followed by North America, which grew by 5.83% in value during the same period. Furthermore, in 2023, the global waterproofing chemicals market was expected to grow by 5.13% in volume compared to 2022.

- In 2022, the Asia-Pacific region significantly dominated the market, accounting for 45% of the market share by value. Countries like China, Japan, and India had an assertive influence over the demand for waterproofing chemicals in the region. China's public expenditure on transport infrastructure reached USD 165.6 billion in 2022 compared to USD 157.6 billion in 2021. Similarly, the rising construction of manufacturing facilities in Japan, along with India's vision to increase its connectivity through roads, railways, and highways, propelled the growth of the construction sector in the region. Such developments are boosting the consumption of waterproofing chemicals for building and construction.

- The waterproofing chemicals market in North America is expected to register the fastest CAGR of 5.96% in value, followed by Asia-Pacific, with a CAGR of 5.47% in value, during the forecast period. High-investment projects supported by government funds and foreign direct investments are expected to raise residential, infrastructure, and commercial construction activities in the regions. As a result, the demand for waterproofing chemicals is projected to rise.

Global Waterproofing Chemicals Market Trends

Asia-Pacific's surge in large-scale office building projects is set to elevate the global floor area dedicated to commercial construction

- In 2022, the global new floor area for commercial construction witnessed a modest growth of 0.15% from the previous year. Europe stood out with a significant surge of 12.70%, driven by a push for high-energy-efficient office buildings to align with its 2030 carbon emission targets. As employees returned to offices, European companies, resuming lease decisions, spurred the construction of 4.5 million square feet of new office space in 2022. This momentum is poised to persist in 2023, with a projected global growth rate of 4.26%.

- The COVID-19 pandemic caused labor and material shortages, leading to cancellations and delays in commercial construction projects. However, as lockdowns eased and construction activities resumed, the global new floor area for commercial construction surged by 11.11% in 2021, with Asia-Pacific taking the lead with a growth rate of 20.98%.

- Looking ahead, the global new floor area for commercial construction is set to achieve a CAGR of 4.56%. Asia-Pacific is anticipated to outpace other regions, with a projected CAGR of 5.16%. This growth is fueled by a flurry of commercial construction projects in China, India, South Korea, and Japan. Notably, major Chinese cities like Beijing, Shanghai, Hong Kong, and Taipei are gearing up for an uptick in Grade A office space construction. Additionally, India is set to witness the opening of approximately 60 shopping malls, spanning 23.25 million square feet, in its top seven cities between 2023 and 2025. Collectively, these endeavors across Asia-Pacific are expected to add a staggering 1.56 billion square feet to the new floor area for commercial construction by 2030, compared to 2022.

South America's estimated fastest growth in residential constructions due to increasing government investments in schemes for affordable housing to boost the global residential sector

- In 2022, the global new floor area for residential construction declined by around 289 million square feet compared to 2021. This can be attributed to the housing crisis generated due to the shortage of land, labor, and unsustainably high construction materials prices. This crisis severely impacted Asia-Pacific, where the new floor area declined 5.39% in 2022 compared to 2021. However, a more positive outlook is expected in 2023 as the global new floor area is predicted to grow by 3.31% compared to 2022, owing to government investments that can finance the construction of new affordable homes capable of accommodating 3 billion people by 2030.

- The COVID-19 pandemic caused an economic slowdown, due to which many residential construction projects got canceled or delayed, and the global new floor area declined by 4.79% in 2020 compared to 2019. As the restrictions were lifted in 2021 and pent-up demand for housing projects was released, new floor area grew 11.22% compared to 2020, with Europe having the highest growth of 18.28%, followed by South America, which rose 17.36% in 2021 compared to 2020.

- The global new floor area for residential construction is expected to register a CAGR of 3.81% during the forecast period, with South America predicted to develop at the fastest CAGR of 4.05%. Schemes and initiatives like the Minha Casa Minha Vida in Brazil announced in 2023 with a few regulatory changes, for which the government plans an investment of USD 1.98 billion to provide affordable housing units for low-income families, and the FOGAES in Chile also publicized in 2023, with an initial investment of USD 50 million, are aimed at providing mortgage loans to families for affordable housing and will encourage the construction of new residential units.

Waterproofing Chemicals Industry Overview

The Waterproofing Chemicals Market is fragmented, with the top five companies occupying 38.48%. The major players in this market are Keshun Waterproof Technology Co., ltd., MAPEI S.p.A., Oriental Yuhong, Sika AG and Soprema (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Technology

- 5.2.1 Epoxy-based

- 5.2.2 Polyurethane-based

- 5.2.3 Water-based

- 5.2.4 Other Technologies

- 5.3 Region

- 5.3.1 Asia-Pacific

- 5.3.1.1 By Country

- 5.3.1.1.1 Australia

- 5.3.1.1.2 China

- 5.3.1.1.3 India

- 5.3.1.1.4 Indonesia

- 5.3.1.1.5 Japan

- 5.3.1.1.6 Malaysia

- 5.3.1.1.7 South Korea

- 5.3.1.1.8 Thailand

- 5.3.1.1.9 Vietnam

- 5.3.1.1.10 Rest of Asia-Pacific

- 5.3.2 Europe

- 5.3.2.1 By Country

- 5.3.2.1.1 France

- 5.3.2.1.2 Germany

- 5.3.2.1.3 Italy

- 5.3.2.1.4 Russia

- 5.3.2.1.5 Spain

- 5.3.2.1.6 United Kingdom

- 5.3.2.1.7 Rest of Europe

- 5.3.3 Middle East and Africa

- 5.3.3.1 By Country

- 5.3.3.1.1 Saudi Arabia

- 5.3.3.1.2 United Arab Emirates

- 5.3.3.1.3 Rest of Middle East and Africa

- 5.3.4 North America

- 5.3.4.1 By Country

- 5.3.4.1.1 Canada

- 5.3.4.1.2 Mexico

- 5.3.4.1.3 United States

- 5.3.5 South America

- 5.3.5.1 By Country

- 5.3.5.1.1 Argentina

- 5.3.5.1.2 Brazil

- 5.3.5.1.3 Rest of South America

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Fosroc, Inc.

- 6.4.3 Hongyuan Waterproof Technology Group Co., Ltd.

- 6.4.4 Keshun Waterproof Technology Co., ltd.

- 6.4.5 MAPEI S.p.A.

- 6.4.6 Oriental Yuhong

- 6.4.7 Saint-Gobain

- 6.4.8 Sika AG

- 6.4.9 Soprema

- 6.4.10 Standard Industries Inc.

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms