|

시장보고서

상품코드

1685765

미국의 건설용 화학제품 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)United States Construction Chemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

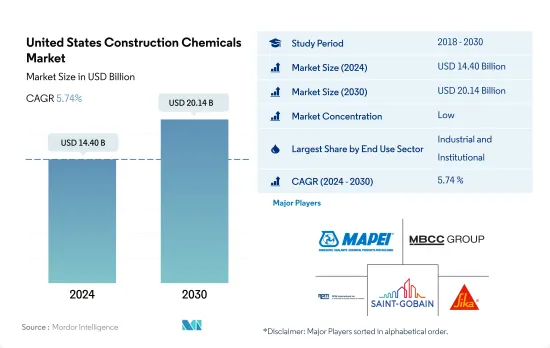

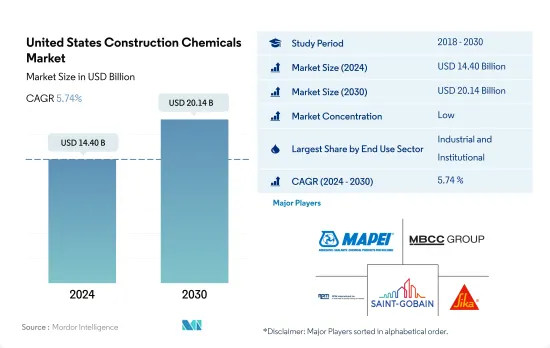

미국의 건설용 화학제품 시장 규모는 2024년 144억 달러로, 2030년에는 201억 4,000만 달러에 이를 것으로 예측되고, 예측 기간 중(2024-2030년) CAGR 5.74%로 성장할 전망입니다.

2026년까지 새로운 공업용 건물에 475억 9,000만 달러가 지출되는 등 공업용 건설에 대한 투자가 증가하고 있어 시장을 밀어올릴 가능성이 높습니다.

- 2022년 미국의 건축용 화학제품 시장은 상업 및 산업용 시설 부문 수요 증가에 견인되어 금액 기준으로 5.15%의 성장을 이루었습니다.

- 미국에서는 산업용 및 시설용 최종 용도 부문이 건설용 화학제품의 최대 소비자입니다. 미국의 새로운 산업용 건물 건설 지출은 2026년까지 475억 9,000만 달러에 이를 것으로 예상됩니다.

- 주택건설 섹터는 미국에서 가장 급성장하고 있는 건설용 화학제품의 소비자가 될 것으로 예측되고 있습니다. 이 동향은 국내 주택 건설 활동을 촉진할 것으로 예상됩니다. 2023년까지 미국은 29억 4,400만 평방피트의 신규 주거 면적을 확보할 것으로 예상되며, 2030년까지 3.68%의 연평균 성장률로 37억 9,900만 평방피트로 증가할 것으로 예상됩니다.

미국 건설용 화학제품 시장 동향

전자상거래와 디지털화의 진전으로 상업공간 수요가 앞으로 크게 늘어날 것으로 예상됩니다.

- 미국 상업 부문에서는 2022년 신규 바닥 면적이 전년 대비 700만 평방 피트 증가와 소폭 증가에 머물렀습니다. 103rd Street와 Antioch Road의 복합 재개발, Elliot와 Sossaman Road의 데이터센터, Monroe Block의 복합 시설 등 주목할만한 프로젝트가 이 급증을 견인할 것으로 예상되고 있습니다.

- COVID-19가 대유행하는 가운데, 상업 부문은 2년 연속으로 신설 바닥 면적이 감소했습니다. 팬데믹에 의한 봉쇄, 경제의 불확실성, 진화하는 워크 다이내믹스에 의해 오피스 스페이스, 소매점, 호텔, 기타 상업시설의 신규 수요가 대폭 감소했습니다.

- 향후를 전망하면, 상업 섹터의 신규 바닥 면적은 2023-2030년간, 수량 베이스로 CAGR 3.96%를 나타낼 것으로 예상됩니다. 또한, 온라인 쇼핑으로의 전환과 소비자 기호 변화에 의해 추진되어 E-Commerce 창고나 배송 센터 수요가 급증할 전망입니다.

미국 주택 부문은 주택 시장에서 수요가 증가하고 공급이 적기 때문에 향후 수년간 높은 성장이 예상됩니다.

- 2022년 미국 주택 부문은 다가구 주택과 단독주택 모두 수요 급증에 견인되어 신규 바닥 면적이 8,600만 평방 피트 증가했습니다. 2023년 동부문의 신설 바닥 면적은 지속적인 주택 수요와 가격 하락 전망에 힘입어 1억 800만 평방 피트 증가할 것으로 예측됐습니다.

- 2020년 미국 주택건설 부문은 후퇴에 직면해 신설 바닥면적은 2019년 대비 2,100만 평방피트 감소했습니다. 그러나 2021년에는 힘차게 회복해, 단독주택과 집합 주택 두 부문에서 14.5%의 견조한 성장을 나타내, 1억 2,200만 평방 피트로 현저한 상승을 나타냈습니다.

- 미국에서는 대폭적인 주택 부족이 계속되고 있지만, 주택 수요는 해마다 증가하고 있어, 신축 주택 호수의 급증을 견인하고 있습니다. 신규 주택 건설 프로젝트에 대한 소비자의 지출이 둔화될 가능성에 기인하고 있습니다.

미국 건설용 화학제품 산업 개요

미국의 건설용 화학제품 시장은 세분화되어 있으며 상위 5개사에서 39.98%를 차지하고 있습니다. 주요 시장 기업은 MAPEI S.p.A., MBCC Group, RPM International Inc., Saint-Gobain Sika AG가 있습니다(알파벳순 정렬)

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 용도 분야의 동향

- 상업

- 산업 및 시설

- 인프라

- 주택

- 주요 인프라 프로젝트(현재 및 발표됨)

- 규제 프레임워크

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 최종 용도 분야

- 상업

- 산업 및 시설

- 인프라

- 주택

- 제품

- 접착제

- 서브 제품별

- 핫멜트

- 반응성

- 용제계

- 수용계

- 앵커와 그라우트

- 서브 제품별

- 시멘트계 고정재

- 수지 고정

- 기타 유형

- 콘크리트 혼화제

- 서브 제품별

- 촉진제

- 공기혼입혼화제

- 고범위 감수제(초가소제)

- 지연제

- 수축 저감 혼화제

- 점도 조정제

- 감수제(가소제)

- 기타 유형

- 콘크리트 보호 페인트

- 서브 제품별

- 아크릴계

- 알키드

- 에폭시

- 폴리우레탄

- 기타 수지

- 바닥재용 수지

- 서브 제품별

- 아크릴

- 에폭시

- 폴리아스파라긴

- 폴리우레탄

- 기타 수지 유형

- 보수 및 재생 화학제품

- 서브 제품별

- 섬유 보호 시스템

- 주입 그라우트재

- 마이크로 콘크리트 모르타르

- 개질 모르타르

- 철근 보호재

- 실링재

- 서브 제품별

- 아크릴

- 에폭시

- 폴리우레탄

- 실리콘

- 기타 수지

- 표면 처리 약품

- 서브 제품별

- 경화 컴파운드

- 이형제

- 기타 제품 유형

- 방수 솔루션

- 서브 제품별

- 화학제품

- 멤브레인

- 접착제

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Ardex Group

- Arkema

- Dow

- HB Fuller Company

- Henkel AG & Co. KGaA

- MAPEI SpA

- MBCC Group

- RPM International Inc.

- Saint-Gobain

- Sika AG

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The United States Construction Chemicals Market size is estimated at 14.40 billion USD in 2024, and is expected to reach 20.14 billion USD by 2030, growing at a CAGR of 5.74% during the forecast period (2024-2030).

Rising investments in industrial construction, such as the USD 47.59 billion spending on new industrial buildings by 2026, are likely to boost the market

- In 2022, the US construction chemicals market saw a 5.15% growth in value, driven by rising demand from the commercial and industrial & institutional sectors. In 2023, the US market accounted account for approximately 79.46% of the North American construction chemicals market.

- The industrial and institutional end-use sector of the market is the largest consumer of construction chemicals in the United States. The end-use sector witnessed a notable growth of 5.67% by value in 2022 compared to the previous year. This surge can be attributed to increased investments in sectors like healthcare and industrial. Notably, the construction spending on new industrial buildings in the United States is expected to reach USD 47.59 billion by 2026. Consequently, the demand for construction chemicals in this sector is projected to rise from USD 5.2 billion in 2023 to USD 7.9 billion in 2030.

- The residential construction sector is anticipated to be the fastest-growing consumer of construction chemicals in the United States. It is projected to register a CAGR of 6.11% during the forecast period (2023-2030). Factors such as urbanization, government initiatives, and foreign and domestic investments are bolstering the nation's housing needs. This trend, in turn, is expected to drive residential building construction activities in the country. By 2023, the United States was projected to reach a new residential floor area of 2.94 billion sq. ft, which is estimated to grow to 3.79 billion sq. ft by 2030, with a CAGR of 3.68%.

United States Construction Chemicals Market Trends

Growing e-commerce and digitalization are expected to propel the demand for commercial spaces in the future significantly

- The commercial sector in the United States saw a modest increase of 7 million sq. ft. in new floor area in 2022 compared to the previous year. This growth was dampened by the rising trend of remote work, leading to reduced demand for new office spaces. However, 2023 was projected to witness a significant uptick, with an estimated 58 million sq. ft. of new floor area. Notable projects like the 103rd Street and Antioch Road mixed-use redevelopment, Elliot and Sossaman Road data center, and Monroe Block mixed-use complex are expected to drive this surge.

- Amidst the COVID-19 pandemic, the commercial sector experienced a decline in new floor area construction for two consecutive years. The drop was 10.85% in 2020 compared to 2019 and further deepened to 12.99% in 2021 compared to the previous year. The pandemic-induced lockdowns, economic uncertainties, and evolving work dynamics led to a significant decrease in demand for new office spaces, retail outlets, hotels, and other commercial properties.

- Looking ahead, the commercial sector's new floor area is projected to witness a CAGR of 3.96% in volume from 2023 to 2030. Noteworthy projects like the Eleven Park Mixed-Use Complex, Queensbridge Collective Mixed-Use Complex, Sacramento Convention Center Expansion, and Church Street Plaza Tower 2 are poised to drive this growth. Furthermore, there is a notable surge in demand anticipated for e-commerce warehouses and distribution centers, fueled by the increasing shift toward online shopping and consumer preferences.

The US residential sector looks at high growth in the coming years due to the rising demand and low supply situation in the housing market

- In 2022, the US residential sector witnessed an 86 million sq. ft. increase in new floor area construction, driven by surging demand for both multifamily and single housing units. Notably, approximately 2 million more housing units were built in 2022 compared to the previous year. The sector's new floor area construction was projected to rise by 108 million sq. ft. in 2023, buoyed by sustained housing demand and the prospect of reduced pricing. Home prices were anticipated to dip by 4.5% in 2023, fueling this growth.

- In 2020, the residential construction sector in the United States faced a setback, with new floor area construction declining by 21 million sq. ft. compared to 2019, largely due to a 2.1% drop in new apartment and condo constructions. However, the sector rebounded strongly in 2021, witnessing a notable uptick of 122 million sq. ft., driven by a robust 14.5% growth in both single-family and multifamily segments.

- Despite a significant housing shortage in the United States, the demand for housing is poised to climb year after year, driving a surge in new housing unit constructions. While spending on new single-family residential construction is on the rise, experts anticipate a slowdown in the coming years. This projection is primarily attributed to the anticipated rise in mortgage rates, which could dampen consumer spending on new residential projects. In light of this demand-supply dynamic, the residential sector's new floor area construction is projected to witness a CAGR of approximately 3.68% during the study period (2023-2030).

United States Construction Chemicals Industry Overview

The United States Construction Chemicals Market is fragmented, with the top five companies occupying 39.98%. The major players in this market are MAPEI S.p.A., MBCC Group, RPM International Inc., Saint-Gobain and Sika AG (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End Use Sector Trends

- 4.1.1 Commercial

- 4.1.2 Industrial and Institutional

- 4.1.3 Infrastructure

- 4.1.4 Residential

- 4.2 Major Infrastructure Projects (current And Announced)

- 4.3 Regulatory Framework

- 4.4 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size, forecasts up to 2030 and analysis of growth prospects.)

- 5.1 End Use Sector

- 5.1.1 Commercial

- 5.1.2 Industrial and Institutional

- 5.1.3 Infrastructure

- 5.1.4 Residential

- 5.2 Product

- 5.2.1 Adhesives

- 5.2.1.1 By Sub Product

- 5.2.1.1.1 Hot Melt

- 5.2.1.1.2 Reactive

- 5.2.1.1.3 Solvent-borne

- 5.2.1.1.4 Water-borne

- 5.2.2 Anchors and Grouts

- 5.2.2.1 By Sub Product

- 5.2.2.1.1 Cementitious Fixing

- 5.2.2.1.2 Resin Fixing

- 5.2.2.1.3 Other Types

- 5.2.3 Concrete Admixtures

- 5.2.3.1 By Sub Product

- 5.2.3.1.1 Accelerator

- 5.2.3.1.2 Air Entraining Admixture

- 5.2.3.1.3 High Range Water Reducer (Super Plasticizer)

- 5.2.3.1.4 Retarder

- 5.2.3.1.5 Shrinkage Reducing Admixture

- 5.2.3.1.6 Viscosity Modifier

- 5.2.3.1.7 Water Reducer (Plasticizer)

- 5.2.3.1.8 Other Types

- 5.2.4 Concrete Protective Coatings

- 5.2.4.1 By Sub Product

- 5.2.4.1.1 Acrylic

- 5.2.4.1.2 Alkyd

- 5.2.4.1.3 Epoxy

- 5.2.4.1.4 Polyurethane

- 5.2.4.1.5 Other Resin Types

- 5.2.5 Flooring Resins

- 5.2.5.1 By Sub Product

- 5.2.5.1.1 Acrylic

- 5.2.5.1.2 Epoxy

- 5.2.5.1.3 Polyaspartic

- 5.2.5.1.4 Polyurethane

- 5.2.5.1.5 Other Resin Types

- 5.2.6 Repair and Rehabilitation Chemicals

- 5.2.6.1 By Sub Product

- 5.2.6.1.1 Fiber Wrapping Systems

- 5.2.6.1.2 Injection Grouting Materials

- 5.2.6.1.3 Micro-concrete Mortars

- 5.2.6.1.4 Modified Mortars

- 5.2.6.1.5 Rebar Protectors

- 5.2.7 Sealants

- 5.2.7.1 By Sub Product

- 5.2.7.1.1 Acrylic

- 5.2.7.1.2 Epoxy

- 5.2.7.1.3 Polyurethane

- 5.2.7.1.4 Silicone

- 5.2.7.1.5 Other Resin Types

- 5.2.8 Surface Treatment Chemicals

- 5.2.8.1 By Sub Product

- 5.2.8.1.1 Curing Compounds

- 5.2.8.1.2 Mold Release Agents

- 5.2.8.1.3 Other Product Types

- 5.2.9 Waterproofing Solutions

- 5.2.9.1 By Sub Product

- 5.2.9.1.1 Chemicals

- 5.2.9.1.2 Membranes

- 5.2.1 Adhesives

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles

- 6.4.1 Ardex Group

- 6.4.2 Arkema

- 6.4.3 Dow

- 6.4.4 H.B. Fuller Company

- 6.4.5 Henkel AG & Co. KGaA

- 6.4.6 MAPEI S.p.A.

- 6.4.7 MBCC Group

- 6.4.8 RPM International Inc.

- 6.4.9 Saint-Gobain

- 6.4.10 Sika AG

7 KEY STRATEGIC QUESTIONS FOR CONCRETE, MORTARS AND CONSTRUCTION CHEMICALS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms

샘플 요청 목록