|

시장보고서

상품코드

1686561

고성능 단열재 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)High-Performance Insulation Materials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

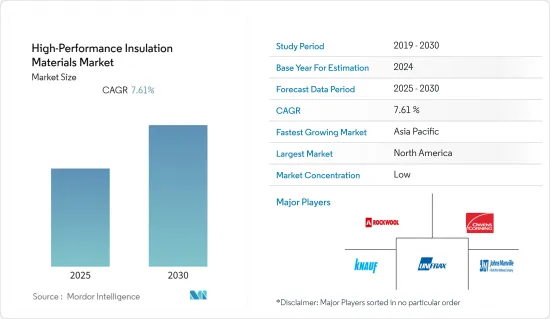

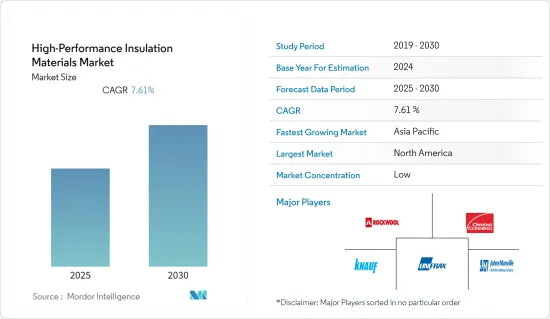

고성능 단열재 시장은 예측 기간 동안 CAGR 7.61%로 성장할 전망입니다.

주요 하이라이트

- 석유 및 가스 산업에서의 사용 증가와 온실가스 배출 및 에너지 절감에 대한 인식이 높아지면서 고성능 단열재 시장의 성장을 견인할 것으로 보입니다.

- 반면, 높은 설치 및 유지보수 비용, 상대적으로 낮은 서비스 수명, CFC가 포함된 단열재 및 폼 제품의 높은 가연성 등은 시장 성장을 저해할 것으로 예상됩니다.

- 아시아태평양의 인프라 활동에 대한 투자가 증가하면서 연구 대상 시장에 새로운 기회가 열릴 것으로 예상됩니다.

고성능 단열재 시장 동향

석유 및 가스 산업에서의 수요 증가

- 고온의 석유 및 가스 조성물은 유정에서 흘러 올라와 라이저가 오일을 표면으로 가져 오기 전에 XMT, 매니폴드, 다양한 중요 기기, 스풀 및 흐름 라인을 통해 이송됩니다.

- 고성능 단열재는 주로 해저 파이프라인 용도에 대한 수요 증가로 인해 석유 및 가스 부문에서 큰 수요를 보이고 있습니다.

- 또한 이러한 소재는 내화성 및 내수성, 우수한 내열성, 향상된 차음성, 경량화 및 두께 감소와 같은 석유 및 가스 부문에서 요구되는 특성을 제공합니다.

- 일본 경제산업성(METI)에 따르면 2021년의 일본의 원유 생산량은 약 49만킬로리터로, 전년의 약 51만 2,000킬로리터로부터 감소했습니다.

- StatCan에 따르면, 미국에서 2021년 10월의 원유 및 동등 제품의 생산량은 10.8% 증가한 2,440만 입방미터가 되어, 2019년 12월 이후의 원유 생산량이 되었습니다.

- 앞서 언급한 요인으로 인해 예측 기간 동안 고성능 단열재의 사용량이 증가할 것으로 보입니다.

시장을 독점하는 아시아태평양

- 아시아태평양 지역은 예측 기간 동안 고성능 단열재 시장을 지배 할 것으로 예상됩니다.

- 이 지역의 석유 및 가스 산업은 에너지 및 석유 화학에 대한 수요 증가로 인해 성장하고 있습니다.

- 아시아태평양의 석유 및 가스 산업은 에너지와 석유화학제품 수요 증가에 따라 성장하고 있습니다.

- 중국의 2022년 1-2월의 원유 생산량은 3,347만톤으로 전년 동기 대비 약 4.6% 증가했습니다.

- OICA에 따르면 2021년 자동차 생산 대수는 784만 6,955대로 2020년 806만 7,557대에 비해 3% 감소했습니다.

- 항공우주 부문에서는 인도 브랜드 자산 재단(IBEF)에 따르면, 이 나라의 항공산업은 향후 4년간 35,000캐롤 루피(49억 9,000만 달러)의 투자가 전망되고 있습니다.

- 앞서 언급한 요인으로 인해 예측 기간 동안 고성능 단열재에 대한 수요가 증가할 것으로 보입니다.

고성능 단열재 산업 개요

세계의 고성능 단열재 시장은 고도로 세분화되어 있으며 상위 10개 업체가 연구 대상 시장에서 눈에 띄는 점유율을 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 석유 및 가스 산업에서의 사용량 증가

- 온실가스 배출 및 에너지 절약에 대한 인식 증가

- 억제요인

- 높은 설치 및 유지보수 비용과 상대적으로 낮은 서비스 수명

- CFC가 포함 된 단열재 및 폼 제품의 높은 가연성

- 업계 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 소재 유형별

- 에어로겔

- 진공 단열 패널(VIP)

- 유리 섬유

- 세라믹 섬유

- 고성능 폼

- 기타

- 최종 사용자 산업별

- 석유 및 가스

- 산업

- 건축 및 건설

- 운송

- 발전

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 기타 북미

- 유럽

- 독일

- 영국

- 이탈리아

- 프랑스

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%) 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- 3M

- Aerogel Technologies LLC

- Armacell

- Aspen Aerogels Inc.

- BASF SE

- Cabot Corporation

- IBIDEN

- Isolite Insulating Products Co. Ltd

- Johns Manville

- Knauf Gips KG

- Luyang Energy-Saving Materials Co. Ltd

- Morgan Advanced Materials

- Owens Corning

- Panasonic Corporation

- PAR Group

- Rath Group

- ROCKWOOL Group

- Saint-Gobain

- Unifrax

제7장 시장 기회와 앞으로의 동향

- 아시아태평양의 인프라 투자 증가

The High-Performance Insulation Materials Market is expected to register a CAGR of 7.61% during the forecast period.

Key Highlights

- The growing usage in the oil and gas industry and rising awareness regarding greenhouse emissions and energy savings are likely to drive the growth of the high-performance insulation materials market.

- On the flip side, high set-up and maintenance costs, relatively low service life, and high flammability with insulated materials and foam products that contain CFC are expected to hinder the market's growth.

- Increasing investments in infrastructural activities in Asia-Pacific are expected to unveil new opportunities for the market studied.

High Performance Insulation Materials Market Trends

Increasing Demand from the Oil and Gas Industry

- The hot oil and gas composition flows up at the wellhead and is transported through XMTs, manifolds, various critical instruments, spools, and flow lines before the riser brings the oil to the surface.

- High-performance insulation materials are witnessing a huge demand from the oil and gas sector, primarily owing to the increasing demand for subsea pipeline applications.

- Additionally, these materials offer properties, such as fire and water resistance, excellent thermal resistance, enhanced acoustic insulation, lightweight, and reduced thickness, that are required in the oil and gas sector.

- According to the Ministry of Economy, Trade, and Industry (METI), in 2021, approximately 490 thousand kiloliters of crude oil were produced in Japan, down from about 512 thousand kiloliters in the previous year.

- According to StatCan, the production of crude oil and equivalent products in the United States rose 10.8% in October 2021 to 24.4 million cubic meters, the highest crude production level since December 2019.

- The aforementioned factors are likely to result in an increase in the usage of high-performance insulation materials during the forecast period.

Asia-Pacific Region to Dominate the Market

- Asia-Pacific is expected to dominate the market for high-performance insulation materials during the forecast period.

- The growth in the oil and gas and the construction sector in the region has significantly boosted the demand for such insulation panels.

- The oil and gas industry in the Asia-Pacific region is growing due to the increasing demand for energy and petrochemicals. Countries such as India, Malaysia, Indonesia, China, South Korea, and Japan are experiencing increased offshore drilling activities.

- The crude oil output of China has registered at 33.47 million tons in the first two months of 2022, which is about 4.6% up from the same period of the previous year. According to the National Bureau of Statistics China, the daily output of crude oil is nearly 576,000 tons.

- According to OICA, the production of vehicles in 2021 accounted for 78,46,955 units, a fall of 3% compared to 80,67,557 units produced in 2020. However, the demand for electric vehicles in Japan is projected to grow over the forecast period.

- In the aerospace sector, according to the India Brand Equity Foundation (IBEF), the country's aviation industry is expected to witness INR 35,000 crore (USD 4.99 billion) investment in the next four years.

- The aforementioned factors will likely increase the demand for high-performance insulation materials during the forecast period.

High Performance Insulation Materials Industry Overview

The global High-Performance Insulation Materials Market is highly fragmented, with the top 10 players capturing a noticeable share in the market studied. Some of the major players in the market include (not in any particular order) Owens Corning, Knauf Gips KG, Rockwool, Johns Manville, and Unifrax, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Growing Usage in the Oil and Gas Industry

- 4.1.2 Rising Awareness Regarding Greenhouse Emissions and Energy Savings

- 4.2 Restraints

- 4.2.1 High Set-up and Maintenance Costs and Relatively Low Service Life

- 4.2.2 High Flammability with Insulated Materials and Foam Products that Contain CFC

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION

- 5.1 Material Type

- 5.1.1 Aerogel

- 5.1.2 Vacuum Insulation Panel (VIP)

- 5.1.3 Fiberglass

- 5.1.4 Ceramic Fiber

- 5.1.5 High-performance Foam

- 5.1.6 Other Material Types

- 5.2 End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Industrial

- 5.2.3 Building and Construction

- 5.2.4 Transportation

- 5.2.5 Power Generation

- 5.2.6 Other End-user Industries

- 5.3 Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.2.4 Rest of North America

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share(%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 3M

- 6.4.2 Aerogel Technologies LLC

- 6.4.3 Armacell

- 6.4.4 Aspen Aerogels Inc.

- 6.4.5 BASF SE

- 6.4.6 Cabot Corporation

- 6.4.7 IBIDEN

- 6.4.8 Isolite Insulating Products Co. Ltd

- 6.4.9 Johns Manville

- 6.4.10 Knauf Gips KG

- 6.4.11 Luyang Energy-Saving Materials Co. Ltd

- 6.4.12 Morgan Advanced Materials

- 6.4.13 Owens Corning

- 6.4.14 Panasonic Corporation

- 6.4.15 PAR Group

- 6.4.16 Rath Group

- 6.4.17 ROCKWOOL Group

- 6.4.18 Saint-Gobain

- 6.4.19 Unifrax

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Increasing Investments in Infrastructural Activities in Asia-Pacific