|

시장보고서

상품코드

1851522

조직 진단 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Tissue Diagnostics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

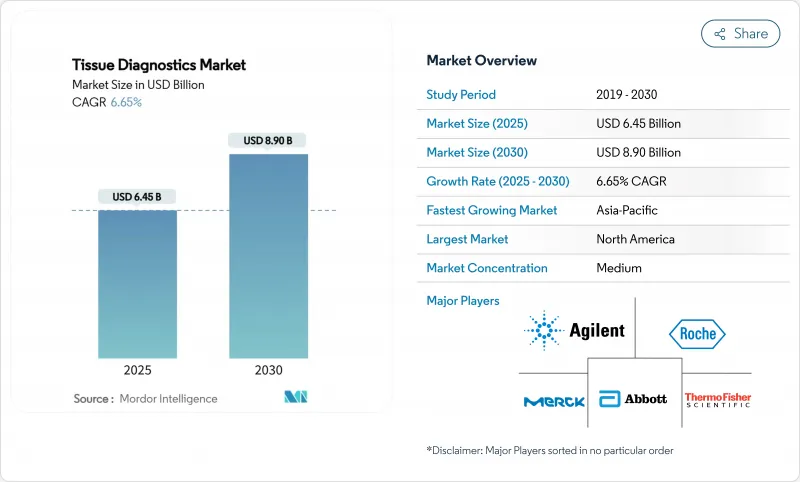

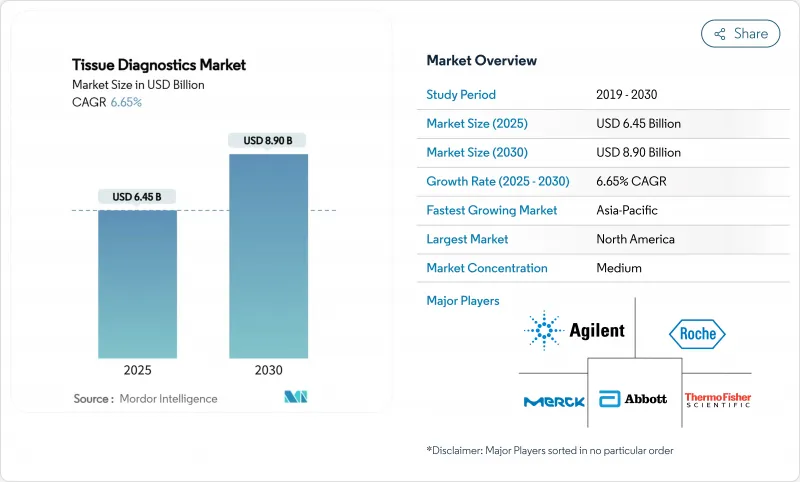

조직 진단 시장 규모는 2025년에 64억 5,000만 달러로, CAGR 6.65%를 나타내 2030년에는 89억 달러에 달할 것으로 예상됩니다.

이 확대는 세계적인 암 이환율의 상승과 검사실의 급속한 자동화, 특히 독영시간을 단축하고 결과를 표준화하는 AI 대응 홀 슬라이드 이미징이라는 두 가지 기세로 뒷받침되고 있습니다. 시약 및 소모품은 모든 병리 조직 검사가 단일 사용 항체를 소비하기 때문에 예측 가능한 수요를 유지하는 반면, 검사실이 슬라이드 취급을 디지털화하고 오류 없는 처리량을 위해 로봇 공학을 통합함에 따라 장비가 상승하고 있습니다. 미국과 유럽에서는 디지털 진료 보상이 명확해지고 경제적 장벽이 낮아졌기 때문에 소규모 병원과 레퍼런스 실험실은 병리학의 부족을 완화하는 원격 진찰 워크플로를 채택하게 되었습니다. 아시아태평양에서는 각국 정부가 조기 발견 목표를 국가의 의료 예산에 통합하고 있기 때문에 기록적인 자본이 모여 세계 벤더와 로컬 벤더 모두 새로운 거래량을 획득하고 있습니다. 동시에 AI 네이티브 신흥 기업은 소프트웨어, 하드웨어 및 시약을 완벽한 플랫폼에 번들링하기 위해 기존 기업에 압력을 가하여 10년 동안 활발한 합병과 파트너십의 무대를 마련합니다.

세계의 조직 진단 시장 동향과 인사이트

암 이환율 상승

세계의 암 이환수는 매년 2.1%씩 증가하고, 2050년에는 3,500만명에 달할 것으로 예상되고 있기 때문에 확정 조직 분석은 계속 불가결합니다. 유방암은 계속 진단 건수의 대부분을 차지하고 있지만, 비소세포 폐암은 국가의 스크리닝 프로그램이 상세한 종양 프로파일링을 요구하고 있기 때문에 이용 사례가 가장 급속히 확대되고 있습니다. 위험은 65세를 넘으면 급증하고, 이미 좁은 병리실의 처리 능력에 대한 압력이 강해지고 있습니다. 지속적인 시료 유입으로 공급업체는 안정적인 수익을 보장하고 자동화, 다중 면역조직화학, 정밀도를 유지하면서 소요시간을 단축하는 AI 알고리즘 등 현재 진행중인 연구개발을 검증할 수 있습니다.

병리 조직 검사실에서 자동화와 AI의 가속

AI를 탑재한 홀 슬라이드 스캐너는 슬라이드 검토 시간을 40% 단축하고 검사실 간의 콘코 댄스를 향상시켜 부족한 병리의가 복잡한 사례에 집중할 수 있습니다. 2024년에 로슈의 계산 동반진단제가 FDA로부터 획기적인 지정을 받은 것은 알고리즘 지원에 의한 판독이 규제 당국에 받아들여져 고객층이 확대되었음을 나타냅니다. 미국에서는 현재 퇴직률이 후임자를 2대 1로 웃돌고 있으며, 자동화가 서비스 계속의 중심이 되고 있습니다. AI를 도입한 검사 시설은 보다 신속한 보고, 보다 엄격한 품질 지표, 보다 높은 확장성을 실현하고, 조직 진단 시장을 소프트웨어에 의한 표준 치료로 밀어 올리고 있습니다.

자본 비용과 소모품 비용이 높고, 불규칙한 보상 체계

홀 슬라이드 스캐너의 가격은 20만 달러에서 50만 달러로, 소모품은 검사실 운영 예산의 약 65%를 차지합니다. 소규모 병원은 민간지급기관에 의해 환불에 편차가 있기 때문에 이러한 지출을 회수하는 데 어려움을 겪고 있으며, 현금이 풍부한 공급자가 능력 격차를 넓히는 2층 생태계를 만들고 있습니다. COVID-19는 지출을 급성기 의료에 돌려 보내고, 하드웨어 업데이트 사이클을 지연시키고, 교체 백로그를 확대하고 있습니다. 리스 모델과 지역 공유 서비스 허브는 새로운 톱니바퀴가 되어 있지만, 저렴한 가격의 완전한 해결은 되어 있지 않습니다.

부문 분석

장비 부문은 2030년까지 연평균 복합 성장률(CAGR) 7.23%를 나타낼 것으로 예측되며, 실험실이 수작업 워크플로를 검토함에 따라 전체 시장 성장을 능가합니다. 홀 슬라이드 스캐너는 미국과 EU에서 상환의 확실성에 힘입어 가장 급성장합니다. 로봇화된 조직 프로세서는 처리 오류를 줄이고 AI화된 염색 시스템은 시약 사용을 절약합니다. 바코드에 의한 샘플 추적과 클라우드 네이티브 대시보드 등의 진보는 검사실의 효율을 더욱 향상시킵니다. 반대로 시약 및 소모품의 경상 수익은 공급업체의 여백을 지원합니다. 이 카테고리는 2024년에 68.23%의 점유율을 유지했습니다. 멀티플렉스 분석 키트는 여러 바이오마커를 한 번의 측정으로 응축하므로 한 번에 측정 비용을 줄이고 조직을 저장할 수 있습니다. 루틴 시약의 안정적인 수요는 공급업체에게 예측 가능한 현금 흐름을 가져오고 이익률이 높은 장비의 R&D 자금원이 됩니다.

2세대 마이크로톰과 크라이오스탯은 디지털 온도 제어와 블레이드 각도 제어를 통합하여 절편 두께의 편차를 최소화합니다. 이 장비는 성숙하지만 마모 및 CAP 인증 요구 사항을 준수하여 교체 사이클이 안정적입니다. 일회용 플라스틱 카세트, 슬라이드 유리, 커버 슬립이 소모품으로 사용되어 소규모 지역의 병리 검사실에서도 안정적인 수입원이 되고 있습니다. 장비와 소모품의 공생 관계는 처리량에 대한 기대 증가와 함께 조직 진단 시장의 장기적인 확장을 지원합니다.

디지털 퍼솔로지의 CAGR은 7.31%로 모든 모달리티 중에서 가장 높습니다. 알고리즘 기반 패턴 인식은 픽셀 데이터를 정량적 인 지표로 변환하여 종양 침윤 림프구 및 유사 분열 이미지의 객관적인 등급을 부여합니다. 현지 시설에서는 클라우드 연결을 이용하여 도시의 하위 전문가를 활용하여 환자의 이동 시간과 대기 시간을 단축합니다. FDA가 2025년 AI 대응 유방암 전이 검출기를 인가하는 등 규제상의 이정표는 병원 조달위원회를 활기차게 합니다. 한편, 면역조직화학은 임상적 친숙함과 표적 치료 지침이 되는 바이오마커 카탈로그의 확대로 43.44% 시장 점유율을 유지하고 있습니다. 자동화를 통해 염색 사이클 시간이 60분 미만으로 단축되어 인력을 늘리지 않고 매일 슬라이드 처리 능력을 높입니다.

In-situ hybridization은 특히 혈액 악성 종양에서 유전자 재배열과 바이러스 유전체을 검출하는 관련성을 유지합니다. 일부 실험실에서는 ISH와 multiplex IHC를 조합하여 RNA와 단백질의 공발현을 삼각측량하여 부족한 조직으로부터의 진단 수율을 높이고 있습니다. 새로운 질량 분석 이미징과 라만 기반 방법은 여전히 틈새 시장이지만 약물 분포 연구와 리피도믹스에 유망합니다. 이러한 기술 아크를 종합하면 조직 진단 시장의 지속적인 다양화가 보장됩니다.

지역 분석

북미는 2024년 세계 매출의 41.34%를 차지하며, CLIA 인증 실험실의 풍부한 설치 베이스, 폭넓은 지불자 커버리지, 많은 기기·시약 본사에의 근접성 등에 지지되었습니다. FDA의 지속적인 모니터링은 세계 모범 사례 기준을 형성하고 벤처 자본의 흐름은 AI 신흥 기업의 형성을 지원합니다. 캐나다에서는 인구가 적은 지역과 도시 지역의 암 센터를 연결하는 전국적인 원격 병리학 네트워크가 진전되어 시장 범위가 넓어지고 있습니다.

유럽은 국경을 넘은 데이터 교환과 조달을 합리화하는 EU 디지털 단일 시장 전략의 혜택을 받습니다. 독일과 영국은 AI 검증 연구를 이끌고 있으며, 북유럽 국가들은 알고리즘 훈련에 중앙 병리학 등록을 활용하고 있습니다. 일부 남부 및 동부 회원국에서는 긴축 재정이 성장을 억제하고 있는 것, 결속력 있는 규제 프레임워크과 안정적인 상환으로 유럽은 2세대 디지털 시스템의 확실한 도입국이 되고 있습니다.

아시아태평양은 가장 급성장하는 지역으로 중국과 인도가 총 2,000억 달러를 진단 인프라 업그레이드에 투입하기 때문에 CAGR은 7.62%를 나타낼 전망입니다. 일본과 한국의 검사 시설은 이미 기술적으로 진행되고 있으며, 공간 생물학에 신속하게 축족을 옮기는 한편, 동남아시아 국가들은 기초적인 병리 조직 검사 능력에 투자합니다. 쑤저우, 심천, 하이데라바드에서는 항체와 슬라이드의 현지 제조 클러스터가 상승하고 공급의 탄력성을 높이고 육양 비용을 낮추고 있습니다. 이와 병행하여 싱가포르와 태국과 같은 의료 투어리즘의 중심지는 국제적으로 인정된 실험실을 요구하고 품질 기준을 높이고 있습니다.

라틴아메리카와 중동 및 아프리카는 새로운 프론티어입니다. 브라질, 사우디아라비아, 아랍에미리트(UAE)은 민간 병원의 확대와 정부의 현대화 추진에 힘입어 각 지역에서 지출을 이끌고 있습니다. 하지만 불충분한 진료 보상과 숙련 노동력 부족으로 인해 전체 성장은 세계 평균보다 낮습니다. 저소득국가의 진단 갭을 메우기 위해, 타겟을 좁힌 원조 프로그램이나 POC(Point-of-Care)의 마이크로플루이딕스 공학이 도입되어 조직 진단 시장의 대응 가능 베이스가 서서히 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암 이환 부담 증가

- 병리 조직 검사실에서 자동화와 AI의 가속

- 미국·EU에 있어서 디지털 파솔로지 상환의 확대

- 인구가 많은 아시아에서 헬스케어 CAPEX가 급증

- 공간 생물학적 방법에 의한 멀티플렉스 IHC의 채용

- LMICs용 POC(Point-of-Care) 마이크로플루이딕스 조직 프리퍼레이션

- 시장 성장 억제요인

- 높은 자본 비용과 소모품 비용

- 훈련을 받은 병리전문의의 세계적 부족

- 플랫폼간의 데이터 포맷 상호 운용성의 갭

- 시약·항체 공급망의 변동성

- 가치/공급망 분석

- 규제 상황

- 기술의 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 제품별

- 기기

- 슬라이드 염색 시스템

- 조직 처리 시스템

- 전체 슬라이드 스캐너

- 마이크로톰 및 크라이오스탯

- 기타 기기

- 시약 및 소모품

- 항체

- 키트 및 분석

- 시약 및 프로브

- 기타 소모품

- 기기

- 기술별

- 면역조직화학

- In-situ Hybridization

- 디지털 병리학

- 기타 기술

- 용도별

- 유방암

- 전립선암

- 비소세포폐암

- 위암

- 림프종

- 기타

- 최종 사용자별

- 병원 및 진단 실험실

- 제약 및 바이오테크놀러지 기업

- 연구 및 학술 기관

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- F. Hoffmann-La Roche

- Danaher(Leica Biosystems)

- Agilent Technologies(Dako)

- Thermo Fisher Scientific

- Abbott Laboratories

- Merck KGaA

- Illumina

- QIAGEN

- PerkinElmer(Revvity)

- Sakura Finetek

- Epredia(PHC)

- 3DHISTECH

- Philips Digital & Computational Pathology

- PathAI

- OptraSCAN

- Indica Labs

- Biocare Medical

- Lunaphore Technologies

- Qritive

- Bio-Genex Laboratories

- Ventana Medical Systems(Roche)

제7장 시장 기회와 향후 전망

KTH 25.11.13The tissue diagnostics market size is USD 6.45 billion in 2025 and is forecast to reach USD 8.90 billion by 2030, reflecting a 6.65% CAGR.

This expansion rests on the dual momentum of a rising global cancer burden and rapid laboratory automation, especially AI-enabled whole-slide imaging that compresses reading times and standardizes results. Reagents and consumables sustain predictable demand because every histopathology test consumes single-use antibodies, while instruments gain ground as laboratories digitize slide handling and integrate robotics for error-free throughput. Digital reimbursement clarity in the United States and Europe lowers economic barriers, prompting small hospitals and reference labs to adopt remote-consultation workflows that ease persistent pathologist shortages. Asia-Pacific draws record capital as governments embed early detection targets into national health budgets, unlocking fresh volume for global and local vendors alike. Simultaneously, AI-native startups press incumbents to bundle software, hardware and reagents into seamless platforms, setting the stage for vigorous mergers and partnerships through the decade.

Global Tissue Diagnostics Market Trends and Insights

Rising Cancer Incidence Burden

Confirmatory tissue analysis remains indispensable as global cancer cases grow 2.1% each year and are projected to hit 35 million by 2050. Breast cancer continues to dominate diagnostic volumes, yet non-small cell lung cancer is the fastest-expanding use case because national screening programs demand detailed tumor profiling . Risk escalates sharply beyond age 65, intensifying throughput pressure on already stretched pathology labs. The sustained specimen inflow gives vendors a stable revenue runway and validates ongoing R&D in automation, multiplex immunohistochemistry and AI algorithms that compress turnaround time while preserving accuracy.

Acceleration of Automation & AI in Histopathology Labs

AI-powered whole-slide scanners reduce slide review time by 40% and raise inter-laboratory concordance, allowing scarce pathologists to focus on complex cases. FDA breakthrough designation for Roche's computational companion diagnostic in 2024 signaled regulatory acceptance of algorithm-assisted reads, widening the customer pool. Retirement rates now outstrip replacements two-to-one in the United States, making automation central to service continuity. Laboratories that deploy AI achieve faster reporting, tighter quality metrics and greater scalability, pushing the tissue diagnostics market toward a software-augmented standard of care.

High Capital & Consumable Costs; Patchy Reimbursement

Whole-slide scanners list between USD 200,000 and USD 500,000, and consumables absorb roughly 65% of lab operating budgets. Smaller hospitals struggle to recoup such outlays when reimbursement remains inconsistent across private payors, creating a two-tier ecosystem where cash-rich providers widen capability gaps. COVID-19 diverted spending to acute care, delaying hardware refresh cycles and enlarging the replacement backlog. Leasing models and regional shared-service hubs are emerging stopgaps but do not fully resolve affordability.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Digital Pathology Reimbursement in US-EU

- Healthcare CAPEX Surge in High-Population Asia

- Global Shortage of Trained Pathologists

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The instruments segment is projected to clock a 7.23% CAGR through 2030, outpacing overall tissue diagnostics market growth as labs overhaul manual workflows. Whole-slide scanners post the steepest unit growth, buoyed by reimbursement certainty in the United States and European Union. Robotics-enabled tissue processors reduce handling errors, while AI-oriented staining systems economize reagent use. Advances such as barcode-driven sample tracking and cloud-native dashboards further elevate laboratory efficiency . Conversely, recurring revenue from reagents and consumables sustains vendor margins; this category retained 68.23% share in 2024 because every specimen necessitates antibodies, probes and mounting media. Multiplex assay kits gain traction because they condense several biomarkers into a single run, lowering per-result cost and conserving tissue-an increasingly valuable commodity in small biopsy samples. Stable demand for routine reagents provides vendors with predictable cash flows that finance R&D in high-margin instrumentation.

Second-generation microtomes and cryostats incorporate digital temperature and blade-angle controls, minimizing variance in section thickness. Although these tools are mature, replacement cycles remain steady due to wear and adherence to CAP accreditation requirements. Disposable plastic cassettes, glass slides and cover slips round out the consumables landscape, ensuring that even small community pathology units contribute steady income streams. The symbiotic relationship between instruments and disposables, coupled with rising throughput expectations, anchors long-term expansion of the tissue diagnostics market.

Digital pathology is advancing at a 7.31% CAGR, the highest among all modalities. Algorithm-based pattern recognition converts pixel data into quantitative metrics, allowing objective grading of tumor infiltrating lymphocytes and mitotic figures. Rural facilities exploit cloud connectivity to tap urban subspecialists, cutting patient travel and wait times. Regulatory milestones-such as the FDA's 2025 clearance of an AI-enabled breast cancer metastasis detector-galvanize hospital procurement committees. Meanwhile, immunohistochemistry retains 43.44% market leadership thanks to its clinical familiarity and an ever-expanding biomarker catalog that guides targeted therapies. Automation has reduced staining cycle times to under 60 minutes, boosting daily slide throughput without extra headcount.

In-situ hybridization maintains relevance for detecting gene rearrangements and viral genomes, particularly in hematologic malignancies. Some laboratories combine ISH with multiplex IHC to triangulate RNA-protein co-expression, enhancing diagnostic yield from scarce tissue. Novel mass-spectrometry imaging and Raman-based modalities remain niche but show promise for drug-distribution studies and lipidomics. Collectively, these technology arcs ensure continual diversification within the tissue diagnostics market.

The Tissue Diagnostics Market Report is Segmented by Product (Instruments, Reagents and Consumables), Technology (Immunohistochemistry, In-Situ Hybridization, and More), Application (Breast Cancer, Prostate Cancer, Non-Small Cell Lung Cancer, and More), End User (Hospitals and Diagnostic Laboratories, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.34% of global revenue in 2024, anchored by a deep installed base of CLIA-certified labs, broad payer coverage and proximity to many instrument and reagent headquarters. Continuous FDA oversight shapes worldwide best-practice standards, and venture capital flows sustain AI startup formation. Canada advances national telepathology networks that connect sparsely populated regions to urban cancer centers, broadening market reach.

Europe benefits from the EU Digital Single Market strategy, which streamlines cross-border data exchange and procurement. Germany and the United Kingdom spearhead AI validation studies, while the Nordics leverage centralized pathology registries for algorithm training. Cohesive regulatory frameworks and stable reimbursement make Europe a reliable adopter of second-generation digital systems, although budget austerity in some Southern and Eastern member states tempers growth.

Asia-Pacific is the fastest-growing region, posting a projected 7.62% CAGR as China and India channel a combined USD 200 billion into diagnostics infrastructure upgrades. Japanese and South Korean labs, already technologically advanced, pivot quickly to spatial biology, whereas Southeast Asian nations invest in foundational histopathology capacity. Local manufacturing clusters in Suzhou, Shenzhen and Hyderabad emerge for antibodies and slides, improving supply resilience and lowering landed costs. In parallel, medical-tourism hubs such as Singapore and Thailand demand internationally accredited labs, elevating quality benchmarks.

Latin America and the Middle East & Africa represent emerging frontiers. Brazil, Saudi Arabia and the United Arab Emirates lead spending in their respective regions, buoyed by private hospital expansion and government modernization drives. Nonetheless, inadequate reimbursement and skilled-workforce shortages hold aggregate growth below global averages. Targeted aid programs and point-of-care microfluidics aim to bridge diagnostic gaps in lower-income countries, slowly enlarging the addressable base for the tissue diagnostics market.

- Roche

- Danaher (Leica Biosystems)

- Agilent Technologies (Dako)

- Thermo Fisher Scientific

- Abbott Laboratories

- Merck

- Illumina

- QIAGEN

- PerkinElmer (Revvity)

- Sakura Finetek

- Epredia (PHC)

- 3DHISTECH

- Philips Digital & Computational Pathology

- PathAI

- OptraSCAN

- Indica Labs

- Biocare Medical

- Lunaphore Technologies

- Qritive

- Bio-Genex Laboratories

- Ventana Medical Systems (Roche)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising cancer incidence burden

- 4.2.2 Acceleration of automation & AI in histopathology labs

- 4.2.3 Expanding digital pathology reimbursement in US-EU

- 4.2.4 Healthcare CAPEX surge in high-population Asia

- 4.2.5 Spatial-biology enabled multiplex IHC adoption

- 4.2.6 Point-of-care microfluidic tissue prep for LMICs

- 4.3 Market Restraints

- 4.3.1 High capital & consumable costs; patchy reimbursement

- 4.3.2 Global shortage of trained pathologists

- 4.3.3 Inter-platform data-format interoperability gaps

- 4.3.4 Reagent/antibody supply-chain volatility

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porters Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Instruments

- 5.1.1.1 Slide-staining systems

- 5.1.1.2 Tissue-processing systems

- 5.1.1.3 Whole-slide scanners

- 5.1.1.4 Microtomes & cryostats

- 5.1.1.5 Other Instruments

- 5.1.2 Reagents and Consumables

- 5.1.2.1 Antibodies

- 5.1.2.2 Kits & assays

- 5.1.2.3 Reagents & probes

- 5.1.2.4 Other consumables

- 5.1.1 Instruments

- 5.2 By Technology

- 5.2.1 Immunohistochemistry

- 5.2.2 In-situ Hybridization

- 5.2.3 Digital Pathology

- 5.2.4 Other Technologies

- 5.3 By Application

- 5.3.1 Breast Cancer

- 5.3.2 Prostate Cancer

- 5.3.3 Non-Small Cell Lung Cancer

- 5.3.4 Gastric Cancer

- 5.3.5 Lymphoma

- 5.3.6 Others

- 5.4 By End User

- 5.4.1 Hospitals and Diagnostic Laboratories

- 5.4.2 Pharmaceutical and Biotechnology Companies

- 5.4.3 Research & Academic Institutes

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 F. Hoffmann-La Roche

- 6.3.2 Danaher (Leica Biosystems)

- 6.3.3 Agilent Technologies (Dako)

- 6.3.4 Thermo Fisher Scientific

- 6.3.5 Abbott Laboratories

- 6.3.6 Merck KGaA

- 6.3.7 Illumina

- 6.3.8 QIAGEN

- 6.3.9 PerkinElmer (Revvity)

- 6.3.10 Sakura Finetek

- 6.3.11 Epredia (PHC)

- 6.3.12 3DHISTECH

- 6.3.13 Philips Digital & Computational Pathology

- 6.3.14 PathAI

- 6.3.15 OptraSCAN

- 6.3.16 Indica Labs

- 6.3.17 Biocare Medical

- 6.3.18 Lunaphore Technologies

- 6.3.19 Qritive

- 6.3.20 Bio-Genex Laboratories

- 6.3.21 Ventana Medical Systems (Roche)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment