|

시장보고서

상품코드

1687187

미국의 엔지니어링 플라스틱 시장 : 시장 점유율 분석, 산업 동향, 성장 예측(2024-2029년)United States Engineering Plastics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029) |

||||||

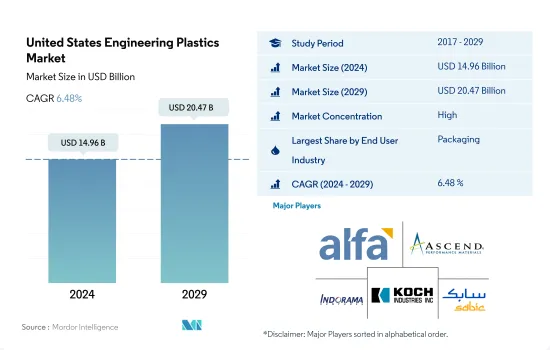

미국의 엔지니어링 플라스틱 시장 규모는 2024년에 149억 6,000만 달러로 평가되었고, 2029년에는 204억 7,000만 달러에 이를 전망이며, 예측 기간(2024-2029년) 중 CAGR 6.48%로 성장할 것으로 예측됩니다.

엔지니어링 플라스틱 수요를 견인하는 첨단 재료 채용 증가

- 엔지니어링 플라스틱의 용도는 항공우주 부문의 내장벽 패널과 도어에서 경질포장 및 연질포장까지 다양합니다. 엔지니어링 플라스틱은 가볍고 강도, 저피로성, 저연소성 등의 점에서 고품질이기 때문에 많은 산업에서 보급되고 있습니다. 미국의 엔지니어링 플라스틱 시장은 포장, 전기 및 전자, 자동차 등의 산업이 견인하고 있습니다.

- 미국에서는 포장 산업이 최대 시장 수익 점유율을 차지하고 있으며 예측 기간 동안 5.93%의 성장이 예상되고 있습니다. 플라스틱 포장 수요는 주로 식음료 산업에서 증가하고 있습니다. 또한 조리된 식품의 수요 증가, 온라인 식품 구입 등이 이 나라의 포장 산업을 활성화시키고 있습니다. 미국의 플라스틱 포장 생산량은 2022년에는 17만 8,000톤이었습니다. 포장 산업의 엔지니어링 플라스틱 수요는 2022년에는 2021년 대비 금액 기준으로 7.71%의 비율로 증가했습니다.

- 미국의 전기 및 전자 산업은 엔지니어링 플라스틱의 두 번째로 유망한 시장으로, 예측 기간(2023-2029년) CAGR은 금액 기준으로 8.41%로 예상됩니다. 이 배경에는 스마트홈 디바이스, 웨어러블 헬스 모니터, 엔터테인먼트 기기 등 원격지와의 교류, 엔터테인먼트, 생산성을 촉진하는 소비자용 전자기기 제품의 이용이 확산되고 있는 것이 있습니다.

- 전기자동차 수요 증가 및 무역 시책의 긍정적인 변화가 미국의 자동차 엔지니어링 플라스틱 시장 성장의 최대 촉진요인이 될 것으로 예상됩니다. 자동차 산업으로부터의 엔지니어링 플라스틱 수요는 예측 기간 동안 금액 기준 5.31%의 CAGR로 추이할 것으로 예상됩니다.

미국의 엔지니어링 플라스틱 시장 동향

소비자용 전자 기기 증가로 전기 및 전자 제품의 생산 수입이 증가

- 기술 혁신의 급속한 속도, 가처분소득 증가, 고급제품에 대한 수요 증가, 생활수준의 향상은 전기 및 전자 시장의 성장을 가속하는 주요 요인의 일부입니다. 2017년 미국은 북미 전기 및 전자 기기 생산 시장의 약 85.9%를 차지했습니다.

- 2020년 이 나라의 전기 및 전자 기기 생산은 정부가 실시한 광범위한 봉쇄 및 이러한 봉쇄로 인한 공급망의 혼란으로 인해 전년 대비 약 3.3%의 감수로 이어졌습니다. 팬데믹 결과 2020년 이 나라의 전자기기 및 소비자용 전자기기 제품 매출은 9.9% 감소했습니다. 그러나 2021년에는 미국의 소비자용 전자기기 산업 매출액은 전년 대비 9% 증가한 약 1,270억 달러에 달했습니다. 그 결과, 2021년 이 나라의 전기 및 전자 기기 생산은, 전년대비 17.1%의 수입 증가가 되었습니다.

- 스마트폰, 노트북, PC, TV 등 기술적으로 선진적 소비자용 전자기기 및 전자기기에 대한 수요의 급증이 예측 기간 중의 소비자용 전자기기 수요를 밀어올릴 것으로 예상됩니다. 이 나라의 소비자용 전자 기기의 시장 규모는, 2023년의 1,551억 달러에서 2027년에는 약 1,613억 달러가 될 것으로 예측됩니다. 기존의 소비자용 전자기기 제품의 조사나 기술 진보의 증가, 신모델의 혁신이, 전자기기 시장의 성장을 촉진하고 있습니다. 그 결과, 이 나라의 전기 및 전자 제품의 생산은 증가할 것으로 예상됩니다.

미국의 엔지니어링 플라스틱 산업 개요

미국의 엔지니어링 플라스틱 시장은 상당히 통합되어 있으며 상위 5개 기업에서 66.72%를 차지하고 있습니다. 이 시장의 주요 기업은 Alfa SAB de CV, Ascend Performance Materials, Indorama Ventures Public Company Limited, Koch Industries, Inc., SABIC 등입니다.

ㅊ기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 주요 요약 및 주요 조사 결과

제2장 보고서 제안

제3장 서문

- 조사의 전제조건 및 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 최종 사용자 동향

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 포장

- 수출입 동향

- 가격 동향

- 재활용 개요

- 폴리아미드(PA)의 재활용 동향

- 폴리카보네이트(PC)의 재활용 동향

- 폴리에틸렌테레프탈레이트(PET)의 재활용 동향

- 스티렌계 공중합체(ABS, SAN)의 재활용 동향

- 규제 프레임워크

- 미국

- 밸류체인 및 유통채널 분석

제5장 시장 세분화

- 최종 사용자 산업별

- 항공우주

- 자동차

- 건축 및 건설

- 전기 및 전자

- 공업 및 기계

- 포장

- 기타

- 수지 유형별

- 불소수지

- 서브 유형별

- 에틸렌테트라플루오로에틸렌(ETFE)

- 불소화 에틸렌 프로파일렌(FEP)

- 폴리테트라플루오로에틸렌(PTFE)

- 폴리불화비닐(PVF)

- 폴리불화비닐리덴(PVDF)

- 기타 서브레진 유형

- 액정 폴리머(LCP)

- 폴리아미드(PA)

- 서브레진 유형별

- 아라미드

- 폴리아미드(PA) 6

- 폴리아미드(PA) 66

- 폴리프탈아미드

- 폴리부틸렌테레프탈레이트(PBT)

- 폴리카보네이트(PC)

- 폴리에테르에테르케톤(PEEK)

- 폴리에틸렌테레프탈레이트(PET)

- 폴리이미드(PI)

- 폴리메틸메타크릴레이트(PMMA)

- 폴리옥시메틸렌(POM)

- 스티렌 공중합체(ABS와 SAN)

- 불소수지

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Alfa SAB de CV

- Arkema

- Ascend Performance Materials

- BASF SE

- Celanese Corporation

- Covestro AG

- DuPont

- Formosa Plastics Group

- Indorama Ventures Public Company Limited

- INEOS

- Koch Industries, Inc.

- RTP Company

- SABIC

- Solvay

- The Chemours Company

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크(산업 매력도 분석)

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원 및 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The United States Engineering Plastics Market size is estimated at 14.96 billion USD in 2024, and is expected to reach 20.47 billion USD by 2029, growing at a CAGR of 6.48% during the forecast period (2024-2029).

Rising adoption of advanced materials to drive the demand for engineering plastics

- Engineering plastics have applications ranging from interior wall panels and doors in aerospace to rigid and flexible packaging. Engineering plastics are popular in many industries due to their lightweight and high quality in terms of strength, low fatigue, and low flammability. The US engineering plastics market is led by industries such as packaging, electrical and electronics, and automotive.

- In the United States, the packaging industry holds the largest market revenue share, which is expected to grow by 5.93% over the forecast period. The demand for plastic packaging is increasing mainly from the food and beverages industry. Moreover, increasing demand for ready-to-eat meals, online food purchasing, etc., has triggered the packaging industry in the country. United States plastic packaging production had a volume of 178 thousand tons in 2022. The demand for engineering plastics in the packaging industry increased at a rate of 7.71% by value in 2022 compared to 2021.

- The electrical and electronics industry in the United States is the second most promising market for engineering plastics, with an expected CAGR of 8.41% by value during the forecast period (2023-2029). This is due to the wider use of consumer electronics products such as smart home devices, wearable health monitors, and entertainment devices to facilitate remote interaction, entertainment, and productivity.

- The rise in demand for electric vehicles and positive changes in trade policies are expected to be the biggest driving factors in the growth of the market for US automotive engineering plastics. The demand for engineering plastic from the automotive industry is expected to record a CAGR of 5.31% by value during the forecast period.

United States Engineering Plastics Market Trends

Rising consumer electronics to augment the electrical & electronics production revenue

- The rapid pace of technological innovation, rising disposable income, increased demand for luxury products, and improving living standards are some of the major factors driving the growth of the electrical and electronics market. In 2017, the United States accounted for around 85.9% of the North American electrical and electronics production market.

- In 2020, the electrical and electronics production in the country decreased by around 3.3% in revenue compared to the previous year, owing to widespread lockdowns implemented by the government and supply chain disruptions caused by these lockdowns. The pandemic resulted in a decline in sales of electronics and appliances in the country by 9.9% in 2020. However, in 2021, consumer electronics industry sales in the United States reached around USD 127 billion, a 9% increase compared to the previous year. Consequently, in 2021, electrical & electronics production in the country grew by a rate of 17.1% in revenue compared to the previous year.

- The surge in demand for technologically advanced consumer electronics and appliances, such as smartphones, laptops, computers, televisions, and others, is expected to boost consumer electronics demand during the forecast period. Consumer electronics in the country are projected to generate a market volume of approximately USD 161.3 billion in 2027, up from USD 155.10 billion in 2023. The increasing research and technological advancements in existing appliances, as well as the innovation of new models, are driving the growth of the electronics market. As a result, the electrical and electronic production in the country is expected to grow.

United States Engineering Plastics Industry Overview

The United States Engineering Plastics Market is fairly consolidated, with the top five companies occupying 66.72%. The major players in this market are Alfa S.A.B. de C.V., Ascend Performance Materials, Indorama Ventures Public Company Limited, Koch Industries, Inc. and SABIC (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 End User Trends

- 4.1.1 Aerospace

- 4.1.2 Automotive

- 4.1.3 Building and Construction

- 4.1.4 Electrical and Electronics

- 4.1.5 Packaging

- 4.2 Import And Export Trends

- 4.3 Price Trends

- 4.4 Recycling Overview

- 4.4.1 Polyamide (PA) Recycling Trends

- 4.4.2 Polycarbonate (PC) Recycling Trends

- 4.4.3 Polyethylene Terephthalate (PET) Recycling Trends

- 4.4.4 Styrene Copolymers (ABS and SAN) Recycling Trends

- 4.5 Regulatory Framework

- 4.5.1 United States

- 4.6 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD and Volume, Forecasts up to 2029 and analysis of growth prospects)

- 5.1 End User Industry

- 5.1.1 Aerospace

- 5.1.2 Automotive

- 5.1.3 Building and Construction

- 5.1.4 Electrical and Electronics

- 5.1.5 Industrial and Machinery

- 5.1.6 Packaging

- 5.1.7 Other End-user Industries

- 5.2 Resin Type

- 5.2.1 Fluoropolymer

- 5.2.1.1 By Sub Resin Type

- 5.2.1.1.1 Ethylenetetrafluoroethylene (ETFE)

- 5.2.1.1.2 Fluorinated Ethylene-propylene (FEP)

- 5.2.1.1.3 Polytetrafluoroethylene (PTFE)

- 5.2.1.1.4 Polyvinylfluoride (PVF)

- 5.2.1.1.5 Polyvinylidene Fluoride (PVDF)

- 5.2.1.1.6 Other Sub Resin Types

- 5.2.2 Liquid Crystal Polymer (LCP)

- 5.2.3 Polyamide (PA)

- 5.2.3.1 By Sub Resin Type

- 5.2.3.1.1 Aramid

- 5.2.3.1.2 Polyamide (PA) 6

- 5.2.3.1.3 Polyamide (PA) 66

- 5.2.3.1.4 Polyphthalamide

- 5.2.4 Polybutylene Terephthalate (PBT)

- 5.2.5 Polycarbonate (PC)

- 5.2.6 Polyether Ether Ketone (PEEK)

- 5.2.7 Polyethylene Terephthalate (PET)

- 5.2.8 Polyimide (PI)

- 5.2.9 Polymethyl Methacrylate (PMMA)

- 5.2.10 Polyoxymethylene (POM)

- 5.2.11 Styrene Copolymers (ABS and SAN)

- 5.2.1 Fluoropolymer

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Alfa S.A.B. de C.V.

- 6.4.2 Arkema

- 6.4.3 Ascend Performance Materials

- 6.4.4 BASF SE

- 6.4.5 Celanese Corporation

- 6.4.6 Covestro AG

- 6.4.7 DuPont

- 6.4.8 Formosa Plastics Group

- 6.4.9 Indorama Ventures Public Company Limited

- 6.4.10 INEOS

- 6.4.11 Koch Industries, Inc.

- 6.4.12 RTP Company

- 6.4.13 SABIC

- 6.4.14 Solvay

- 6.4.15 The Chemours Company

7 KEY STRATEGIC QUESTIONS FOR ENGINEERING PLASTICS CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework (Industry Attractiveness Analysis)

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms