|

시장보고서

상품코드

1687237

유럽의 원격 의료 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측Europe Telemedicine - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

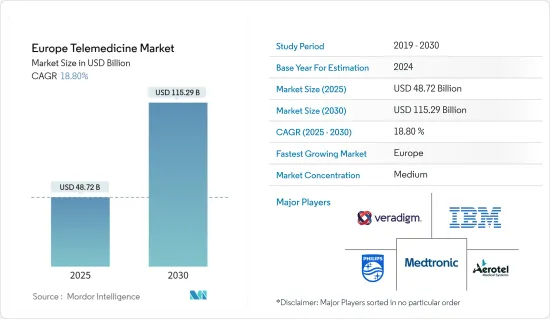

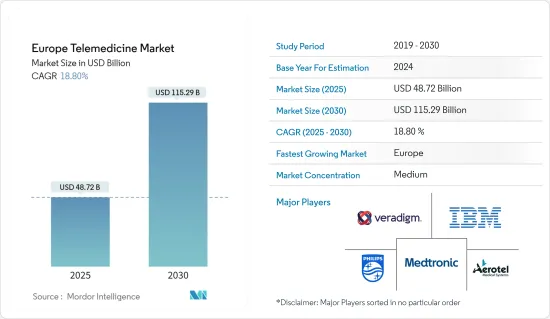

유럽의 원격 의료 시장 규모는 2025년 487억 2,000만 달러에서 예측 기간(2025-2030년) 동안 CAGR 18.8%로 성장하여 2030년에는 1,152억 9,000만 달러에 달할 것으로 예측됩니다.

유럽의 원격 의료 시장은 이 대륙의 건강 관리 부문을 변화시키는 중요한 요소에 힘입어 상당한 성장을 이루고 있습니다. 이러한 동력은 건강 관리 제공 방법을 재구성하고 유럽 건강 관리 시스템에서 매우 중요한 과제를 해결합니다.

메가트렌드와 거시 촉진요인 : 건강 관리의 디지털화, 비용 효율적인 솔루션에 대한 요구, 환자 중심의 케어 모델로의 전환이 유럽의 원격 의료 시장을 견인하고 있습니다. 이러한 추세는 다른 특정 성장 촉진요인과 연관되어 유럽에서 원격 의료의 확대에 박차를 가하고 있습니다.

헬스케어 비용 상승 : 유럽 전역에서 헬스케어 지출이 증가하면서 원격 의료의 보급을 뒷받침하고 있습니다. 정부가 건강 수준을 높이기 위해 지출을 늘리면서 비용 효율적인 솔루션에 대한 수요가 증가하고 있습니다. 예를 들어 프랑스, 덴마크, 오스트리아, 네덜란드, 노르웨이 등 국가에서는 GDP의 8-10%를 건강 관리에 할당하고 있습니다. 원격 의료는 만성 질환 관리와 관련된 비용 절감, 환자 이동 시간 단축, 입원 기간 단축에 도움이 되며 급증하는 건강 관리 비용에 대한 현실적인 솔루션을 제공합니다.

기술 혁신 : COVID-19의 대유행으로 가속화된 급속한 디지털 변혁은 유럽의 건강 관리 제공 상황에 큰 영향을 미칩니다. 유럽 연합(EU)과 회원국은 디지털 건강을 추진하는 이니셔티브의 선두에 서 있습니다. 예를 들어, EU4Health 프로그램은 헬스케어의 디지털화를 지원하기 위해 51억 유로를 할당합니다. 한편, 디지털 헬스 신흥 기업에 대한 투자도 급증하고 있으며, 유럽 전역에서 600개가 넘는 기업이 자금 제공을 받아 활동하고 있습니다. 이러한 혁신의 웨이브는 원격 의료의 접근성, 효율성 및 건강 관리 시스템 내에서의 통합성을 향상시킵니다.

원격 환자 모니터링 증가 : 원격 환자 모니터링(RPM)은 질병 관리를 개선하는 중요한 도구로 부상했습니다. MicroPort CRM의 블루투스 호환 페이스메이커인 Alizea(TM) 및 Borea(TM)와 같은 제품은 RPM 성장에 박차를 가하고 있는 기술적 진보의 한 예입니다. 영국에서는 Smith Nephew와 Huma가 정형외과 수술을 위한 RPM 서비스를 시작하여 수술 전 치료와 예후를 최적화하고 있습니다. 이러한 혁신은 케어의 질을 향상시키고 헬스케어 시스템에 대한 부담을 경감합니다.

만성 질환의 부담 증가 : 만성 질환은 유럽의 건강 관리 시스템에 큰 도전 과제이며 원격 의료는 이러한 부담을 완화하는 솔루션을 제공합니다. 유럽에서는 15세 이상의 인구 중 3분의 1이 만성 질환을 앓고 있습니다. 원격 의료는 특히 유럽에서 5,900만 명의 성인이 앓고 있는 당뇨병과 같은 질병에 대한 지속적인 모니터링과 관리에 대한 접근을 용이하게 합니다. 이 기술은 조기 진단과 개별 케어를 가능하게 하며 유럽 전역의 만성 질환 관리에 기여합니다.

요약하면 유럽의 원격 의료 시장은 경제적 압력 증가, 기술 진보, 의료 수요 변화, 만성 질환 부담이 원동력이 되고 있습니다. 이러한 힘으로 건강 관리 상황이 재구성되면서 원격 의료는 사용이 용이한 고품질 건강 관리 프로그램을 제공하는 데 중요한 역할을 지속할 것입니다.

유럽 원격 의료 시장 동향

소프트웨어 : 유럽 원격 의료 시장의 혁신을 견인

부문 개요 : 소프트웨어 솔루션은 유럽의 원격 의료 시장의 핵심이며 디지털 플랫폼을 통해 원격 진단 및 진료를 가능하게 합니다. 이 분야는 환자와 의사의 의사 소통을 간소화하고 보다 광범위한 건강 관리 시스템과의 통합성으로 인해 시장의 약 45%를 차지합니다.

성장의 원동력 : 소프트웨어 분야는 만성 질환 증가와 인공지능(AI) 및 데이터 분석의 기술 진보와 같은 메가트렌드로부터 혜택을 받습니다. COVID-19의 대유행을 계기로 유럽 전역에서 원격 진찰이 대폭 증가했습니다. 프랑스에서는 주당 원격 상담 건수가 2020년 초에 4만 건에서 유행 피크 때 100만 건 가까이로 급증했습니다. AI를 탑재한 툴과 실시간 분석이 원격 의료 소프트웨어를 변화시켜 개별 케어와 예측 진단을 제공합니다.

경쟁 구도 : 각 회사가 시장 패권을 다투면서 광범위한 기능을 제공하는 종합적인 소프트웨어 플랫폼 개발이 우선 과제가 되었습니다. HealthHero의 Fernarzt.com 인수와 같은 협업 및 인수로 각 회사는 서비스 제공을 확대하고 있습니다. 대기업은 사용자 경험 최적화, 데이터 보안 확보, AI 주도 기능의 통합에 주력하고 있습니다. 이 추세는 유럽 원격 의료 소프트웨어 시장의 미래 성장을 뒷받침하고 있습니다.

독일 : 유럽에서 원격 의료 도입의 선도자 역할

지역 역학 : 독일은 견고한 건강 관리 인프라와 첨단 의료 정책에 힘입어 유럽 내에서 급성장하는 원격 의료 시장으로 부상하고 있습니다. 이 시장은 헬스케어의 디지털화와 지역 의료 격차 대응에 주력하고 있기 때문에 다른 유럽 국가를 웃도는 2자리 성장이 전망되고 있습니다.

시장 촉매 : 독일 내 노화와 만성 질환 증가로 원격 의료 서비스에 대한 수요가 증가하고 있습니다. 2019년 디지털 헬스케어법(DVG)은 디지털 헬스를 주류 케어에 통합하는 길을 열었습니다. COVID-19 위기는 원격 의료의 채택을 더욱 가속화하고 독일 환자와 의료 제공업체는 가상 케어 서비스를 빠르게 받아들였습니다.

경쟁 전략 : 독일의 원격 의료 시장을 목표로 하는 기업은 현지화와 엄격한 건강 관리 규정을 준수하는 데 주력하고 있습니다. 시장 진입에는 현지의 의료 제공자와의 협력이 불가피하며 독일어로 된 플랫폼에 대한 투자가 시장 진입의 열쇠입니다. 시장은 국내 신흥기업과 국제 선도기업 간의 경쟁이 치열해지면서 혁신이 촉진되고 통합이 진행될 것으로 예상됩니다.

유럽 원격 의료 산업 개요

시장 우위 : 세계 기업과 전문 기업이 주도

유럽의 원격 의료 시장은 글로벌 건강 관리 대기업과 전문 원격 의료 공급자가 혼재되어 있습니다. 이 합리적인 통합 시장에서 Koninklijke Philips NV, Medtronic PLC, Teladoc Health Inc.와 같은 대기업은 강력한 기술 전문 지식, 광범위한 건강 관리 포트폴리오 및 풍부한 자원을 배경으로 우위를 차지합니다.

시장 리더 기술 혁신과 종합적 솔루션

주요 기업은 기술 혁신과 종합적인 서비스 제공에 대한 헌신을 통해 타사와의 차별화를 도모하고 있습니다. Koninklijke Philips NV는 통합 원격 의료 플랫폼을 개발하고 Medtronic PLC는 만성 질환의 원격 모니터링을 제공합니다. Teladoc Health Inc.는 InTouch Technologies 인수 후 가상 케어 서비스의 광범위한 제품군을 제공합니다. 이 선도기업들은 원격 심장병학, 원격 방사선학, 원격 병리학 등 여러 전문 분야에 걸쳐 원격 의료 솔루션을 제공하며 유럽의 다양한 의료 요구에 부응하고 있습니다.

미래 성공을 위한 전략 통합 및 규제 준수

앞으로 원격 의료 기업은 AI와 머신러닝 기술을 자사의 플랫폼에 통합하여 진단을 강화하고 개별화된 케어를 제공할 필요가 있습니다. 기존의 건강 관리 인프라와의 원활한 통합을 보장하는 솔루션이 경쟁 우위를 확보할 가능성이 높습니다. GDPR(EU 개인정보보호규정)과 같은 유럽에서 진화하는 규제 프레임워크를 준수하는 것도 신뢰 구축과 컴플라이언스 유지에 필수적입니다. 사이버 보안을 중시하고 환자 예후를 개선하면서 비용 효과성을 높이는 기업은 유럽 전역에서 시장 점유율을 확보하고 정부 지원을 확보하는 데 유리한 입장에 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 원격 환자 모니터링 증가

- 만성 질환의 부담 증가

- 시장 성장 억제요인

- 법률과 상환의 문제

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 유형별

- 원격 병원

- 원격 재택 의료

- mHealth(모바일 건강)

- 컴포넌트별

- 제품별

- 하드웨어

- 소프트웨어

- 기타 제품

- 서비스별

- 원격 병리학

- 원격 심장병학

- 원격 방사선학

- 원격 피부과학

- 원격 정신의학

- 기타 서비스

- 제품별

- 제공 모드별

- 온프레미스

- 클라우드 기반

- 지역별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 기업 프로파일

- Aerotel Medical Systems(1998) Ltd

- Veradigm LLC

- AMD Global Telemedicine

- OTH.IO

- International Business Machinery Corporation(IBM)

- Teladoc Health Inc.

- Resideo Technologies Inc.

- Koninklijke Philips NV

- Medtronic PLC

- SHL Telemedicine

제7장 시장 기회와 앞으로의 동향

CSM 25.04.07The Europe Telemedicine Market size is estimated at USD 48.72 billion in 2025, and is expected to reach USD 115.29 billion by 2030, at a CAGR of 18.8% during the forecast period (2025-2030).

The Europe Telemedicine Market is undergoing substantial growth, driven by critical factors transforming the healthcare sector across the continent. These forces are reshaping how healthcare is delivered and addressing pivotal challenges within European healthcare systems.

Megatrends and Macro Growth Drivers: Digital healthcare transformation, the need for cost-efficient solutions, and the shift towards patient-centered care models are driving the European Telemedicine Market. These trends are intertwined with other specific growth drivers, fueling the expansion of telemedicine in Europe.

Rising Healthcare Costs: Rising healthcare expenditures across Europe are propelling telemedicine adoption. As governments increase spending to enhance healthcare standards, there is a growing demand for cost-effective solutions. For example, countries like France, Denmark, Austria, the Netherlands, and Norway allocate 8-10% of their GDP to healthcare. Telemedicine helps mitigate costs linked to chronic disease management, reduce patient travel, and shorten hospital stays, offering a practical solution to escalating healthcare expenses.

Technological Innovations: The rapid digital transformation, accelerated by the COVID-19 pandemic, is significantly impacting healthcare delivery in Europe. The European Union and member states are spearheading initiatives to promote digital health. For instance, the EU4Health program allocates €5.1 billion to support healthcare's digital evolution. Meanwhile, investments in digital health startups are surging, with over 600 funded companies active across Europe. This innovation wave enhances telemedicine's accessibility, efficiency, and integration within healthcare systems.

Increasing Remote Patient Monitoring: Remote patient monitoring (RPM) has emerged as a valuable tool in improving disease management. Products like MicroPort CRM's Bluetooth-enabled Alizea(TM) and Borea(TM) pacemakers exemplify the technological advancements fueling RPM growth. In the UK, Smith+Nephew and Huma launched an RPM service for orthopedic surgeries, optimizing preoperative care and outcomes. These innovations improve care quality while reducing strain on healthcare systems.

Growing Burden of Chronic Diseases: Chronic diseases represent a significant challenge for healthcare systems in Europe, with telemedicine offering solutions to mitigate this burden. One-third of the European population over 15 lives with a chronic condition. Telemedicine facilitates continuous monitoring and access to care, especially for diseases like diabetes, which affects 59 million adults in Europe. The technology enables early diagnosis and personalized care, making it invaluable for managing chronic conditions across the continent.

In summary, the Europe Telemedicine Market is driven by rising economic pressures, technological advances, changing healthcare demands, and the chronic disease burden. As these forces reshape the healthcare landscape, telemedicine will continue playing a crucial role in delivering high-quality, accessible healthcare.

Europe Telemedicine Market Trends

Software: Driving Innovation in Europe's Telemedicine Market

Segment Overview: Software solutions are at the core of the European telemedicine market, enabling remote consultations and diagnoses via digital platforms. This segment accounts for roughly 45% of the market, driven by its ability to streamline patient-provider communication and integrate into broader healthcare systems.

Growth Drivers: The software segment benefits from megatrends like the rise in chronic diseases and technological advancements in artificial intelligence (AI) and data analytics. The COVID-19 pandemic triggered a significant increase in teleconsultations across Europe. In France, weekly teleconsultations skyrocketed from 40,000 in early 2020 to nearly 1 million at the pandemic's peak. AI-powered tools and real-time analytics are transforming telemedicine software, offering personalized care and predictive diagnostics.

Competitive Landscape: As companies vie for market dominance, developing comprehensive software platforms that offer broad functionality is a priority. Collaborations and acquisitions, like HealthHero's acquisition of Fernarzt.com, are enabling companies to expand their service offerings. Leading players focus on optimizing user experience, ensuring data security, and integrating AI-driven features. This trend is driving the future growth of Europe's telemedicine software market.

Germany: Spearheading Telemedicine Adoption in Europe

Regional Dynamics: Germany has emerged as a fast-growing telemedicine market within Europe, driven by robust healthcare infrastructure and progressive health policies. The market is expected to experience double-digit growth, outpacing other European countries due to Germany's focus on healthcare digitization and addressing care gaps in rural regions.

Market Catalysts: Germany's aging population and rising incidence of chronic diseases contribute to the growing demand for telemedicine services. The Digital Healthcare Act (DVG) of 2019 paved the way for integrating digital health into mainstream care. The COVID-19 crisis further accelerated telemedicine adoption, with German patients and healthcare providers rapidly embracing virtual care services.

Competitive Strategies: Companies eyeing the German telemedicine market are focusing on localization and compliance with stringent healthcare regulations. Collaborations with local healthcare providers are crucial for market entry, and investments in German-language platforms are key for user engagement. The market is expected to see increased competition between domestic startups and international players, fostering innovation and driving consolidation.

Europe Telemedicine Industry Overview

Market Dominance: Global Players and Specialized Companies Lead

The Europe Telemedicine Market is a mix of global healthcare conglomerates and specialized telemedicine providers. This moderately consolidated market sees major players like Koninklijke Philips NV, Medtronic PLC, and Teladoc Health Inc. dominate due to their strong technological expertise, broad healthcare portfolios, and significant resources.

Market Leaders: Technological Innovation and Comprehensive Solutions

Leading companies distinguish themselves through their commitment to innovation and comprehensive service offerings. Koninklijke Philips NV has developed integrated telehealth platforms, while Medtronic PLC offers remote monitoring for chronic diseases. Teladoc Health Inc., following its acquisition of InTouch Technologies, now offers an extensive suite of virtual care services. These leaders provide telemedicine solutions across multiple specialties, including telecardiology, teleradiology, and telepathology, catering to Europe's diverse healthcare needs.

Strategies for Future Success: Integration and Regulatory Compliance

Looking ahead, telemedicine companies must integrate AI and machine learning technologies into their platforms to enhance diagnostics and deliver personalized care. Solutions that ensure seamless integration with existing healthcare infrastructure will likely secure a competitive edge. Adherence to Europe's evolving regulatory frameworks, such as GDPR, is also critical for building trust and maintaining compliance. Firms that prioritize cybersecurity and demonstrate cost-effectiveness while improving patient outcomes are better positioned to capture market share and secure government support across Europe.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Remote Patient Monitoring

- 4.2.2 Growing Burden of Chronic Diseases

- 4.3 Market Restraints

- 4.3.1 Legal and Reimbursement Issues

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value -USD)

- 5.1 By Type

- 5.1.1 Telehospitals

- 5.1.2 Telehomes

- 5.1.3 mHealth (Mobile Health)

- 5.2 By Component

- 5.2.1 By Products

- 5.2.1.1 Hardware

- 5.2.1.2 Software

- 5.2.1.3 Other Products

- 5.2.2 By Services

- 5.2.2.1 Telepathology

- 5.2.2.2 Telecardiology

- 5.2.2.3 Teleradiology

- 5.2.2.4 Teledermatology

- 5.2.2.5 Telepsychiatry

- 5.2.2.6 Other Services

- 5.2.1 By Products

- 5.3 By Mode of Delivery

- 5.3.1 On-premise Delivery

- 5.3.2 Cloud-based Delivery

- 5.4 Geography

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Aerotel Medical Systems (1998) Ltd

- 6.1.2 Veradigm LLC

- 6.1.3 AMD Global Telemedicine

- 6.1.4 OTH.IO

- 6.1.5 International Business Machinery Corporation (IBM)

- 6.1.6 Teladoc Health Inc.

- 6.1.7 Resideo Technologies Inc.

- 6.1.8 Koninklijke Philips NV

- 6.1.9 Medtronic PLC

- 6.1.10 SHL Telemedicine