|

시장보고서

상품코드

1852179

포장용 접착제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Packaging Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

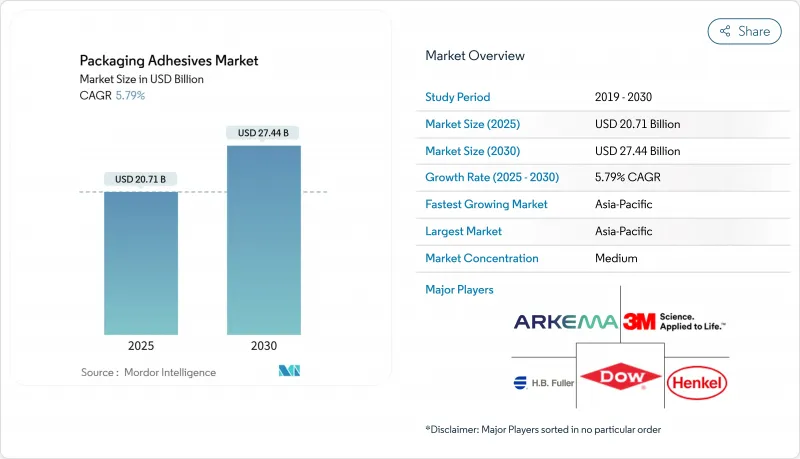

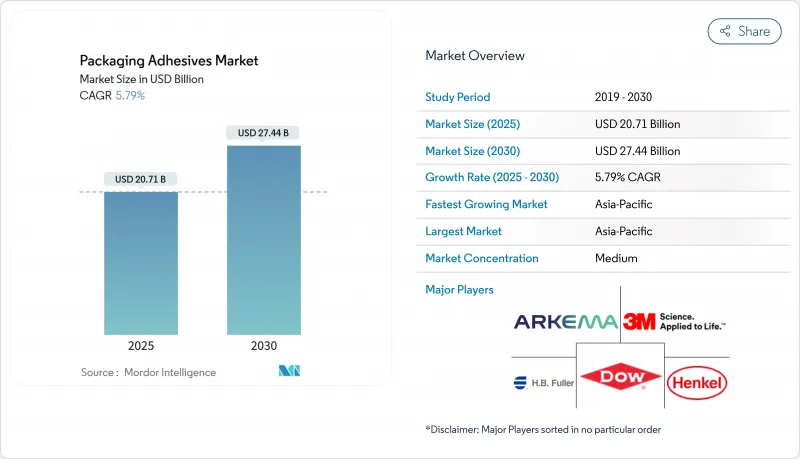

포장용 접착제 시장 규모는 2025년에 207억 1,000만 달러로 평가되었고, 예측기간(2025-2030년)의 CAGR은 5.79%를 나타낼 것으로 예측되며, 2030년에 274억 4,000만 달러에 달할 전망입니다.

성장은 네 가지 기둥에 기반합니다 : 즉석식품(RTE)의 증가하는 물량, 위조방지 밀봉을 우선시하는 전자상거래 붐, 휘발성 유기화합물(VOC) 배출에 대한 규제 압박, 그리고 생물 기반 화학물질의 빠른 채택입니다. 수성 제형은 접착 강도를 저하시키지 않으면서 강화되는 대기질 규정을 충족시키기 때문에 전체 매출의 절반 이상을 차지하며, 핫멜트 라인은 더 빠른 라인 속도를 요구하는 자동화 물류센터에서 점유율을 계속 확대하고 있습니다. 지역별로는 아시아태평양 지역이 제조 규모와 재활용 인프라에 대한 공공 부문 투자로 혜택을 보며, 북미는 공정 혁신을 통해 수익을 창출하고, 유럽은 재펄핑 가능 또는 퇴비화 가능 등급에 대한 수요를 높이는 순환경제 규정을 시행합니다. 대형 화학 기업들이 인수합병, 공동 연구개발, 범위-3 탄소 배출 목표를 통해 가격 민감도가 높은 환경에서 차별화를 꾀함에 따라 경쟁 강도는 중간 수준을 유지합니다.

세계의 포장용 접착제 시장 동향 및 인사이트

식품 및 음료 부문 수요 증가

차단 성능과 유통기한 연장에 대한 수요로 인해 포장용 접착제 시장은 음료, 유제품, 즉석식품 분야의 신제품 출시와 발맞춰 성장하고 있습니다. 제조사들은 이제 에너지 절감을 위해 낮은 라인 온도에서도 가동 가능하며 다지역 규정을 통과한 이민성 테스트 등급을 지정하고 있습니다. 헨켈의 바이오 기반 테크노멜트 수프라 079 에코 쿨(2024년 상용화)은 재생 가능 성분 49%를 함유하며 가동 열을 40°C 낮춰 CO2 배출량을 32% 감소시키고 종이 섬유와의 원활한 재활용성을 제공합니다. 유사한 에너지 절감 특성은 대형 병입업체가 공공 기후 목표를 달성하는 데 기여합니다.

식품안전에 대한 의식 증가

글로벌 규제 기관들은 간접 식품 접촉 승인 규정의 허점을 보완하고 있습니다. 중국의 GB 4806.15-2024는 392종의 접착 물질에 대한 허용 목록, 의무적 표시 규정 및 이주 제한을 도입하며, 이는 2025년 2월 8일부터 적용됩니다. 이와 동시에 미국 식품의약국(FDA)은 2024년 초 PFAS 방유 화학물질을 단계적으로 폐지하여 변환업체들이 비불소 대체재 인증을 받도록 강제하고 있습니다. 이에 따른 규정 준수 부담은 수출 시장 전반에 걸쳐 문서 작업을 간소화하는 다지역 접착제 제형을 촉진하고 있습니다.

엄격한 정부 규제

휘발성 유기화합물(VOC) 상한선은 지속적으로 강화되고 있습니다. 뉴저지주의 2024년 초안은 소비자용 접착제의 허용 VOC 함량을 7%로 낮추는 한편, 캘리포니아 규정은 47종의 유독 대기 오염 물질을 전면 금지합니다. 유럽연합 규정 2024/3190은 식품 포장재에서 비스페놀 A를 제거하여 제형 개발자들이 수성 또는 UV 경화형 대체재로 전환하도록 유도합니다. 규제 준수 비용은 증가하지만, 조기 도입 기업들은 인증된 저배출 라벨을 통해 가격 결정력을 확보합니다.

부문 분석

수성 시스템은 2024년 포장용 접착제 시장에서 매출 기준 57.19%의 점유율을 차지했으며, 이는 제조사들이 무용제 생산 목표를 달성해야 하는 필요성을 반영합니다. 이러한 우위는 6.04%의 연평균 복합 성장률(CAGR)로 확대되어 용제형 유사 제품들을 크게 앞지를 전망입니다. 빠른 건조 아크릴 분산액은 이제 실온에서 다층 필름을 접착하여 오븐 체류 시간을 단축합니다. 동시에, 개선된 유변학 조절제는 고속 슬롯 코터에서 비드 형태를 유지하여 안정제 추가 없이 처리량을 높입니다. 핫멜트 화학 제품군은 창고 자동화가 즉각적인 설정을 선호하기 때문에 근소한 차이로 2위를 차지합니다. 재생 가능 원료 기반 폴리올레핀 골격과 같은 혁신은 수성 제품군과의 탄소 격차를 줄입니다.

유럽과 북미 전역의 엄격한 규정은 수요의 지속성을 보장합니다. 다가올 OECD 지침이 수명주기 배출량을 정량화함에 따라, 브랜드 소유자들은 공장 단위 배출 데이터를 공개하는 공급업체를 확보하고 있습니다. 결과적으로 수성 라인은 대중 시장 골판지 및 프리미엄 유연 라미네이트 모두에 공급할 수 있는 위치에 있어, 2030년까지 기술 선도 기업의 포장용 접착제 시장 규모 우위를 강화할 것입니다. 용제 기반 업체들은 여전히 틈새 고온 응용 분야를 담당하겠지만, 초저 VOC 혼합물로 재구성하지 않는 한 점진적인 시장 침식을 겪을 것입니다.

2024년 포장용 접착제 시장 규모에서 EVA는 30.51%를 차지했으며, 이는 우수한 비용 대비 성능 비율과 다양한 기질과의 호환성에 기반합니다. 골판지 밀봉, 잡지 등 접착, 변조 방지 라벨링에서의 역할로 높은 판매량을 유지하고 있습니다. 열감도 단점을 극복하기 위해 공급업체들은 현재 메탈로센 폴리에틸렌 부문를 혼합하여 핫택(hot-tack) 성능을 강화함으로써 수지 가격 변동 속에서도 마진을 보호하고 있습니다. 바이오 기반 등급은 규모는 작지만 사탕수수 유래 단량체 생산 확대에 힘입어 연평균 6.71% 성장률(CAGR)을 기록할 전망입니다. 보스틱의 바이오 함량 60% 시아노아크릴레이트 라인은 고부가가치 포장재에 즉각적인 접착력을 제공하면서 온실가스 배출량을 줄여, 다른 주요 기업들이 따라 하려는 모델이 되고 있습니다.

범위 3(Scope 3) 배출량 공개에 대한 투자자 감시가 전환을 가속화하고 있습니다. 과학 기반 목표를 가진 다국적 기업들은 현장 재생에너지 및 질량 균형 인증을 기준으로 공급업체를 선별하며, 바이오 기반 혁신 기업으로 물량을 재배분하고 있습니다. 동시에 내화학성이나 유연성이 중요한 분야에서는 아크릴 및 폴리우레탄이 여전히 필수적이며, 중간 단일자리 수 성장률을 유지하고 있습니다. 이러한 화학 혼합은 포장용 접착제 시장이 경쟁적이면서도 혁신이 풍부한 상태를 유지하도록 보장합니다.

지역 분석

아시아태평양 지역은 2024년 포장용 접착제 시장에서 40.19%의 점유율로 매출을 주도했으며, 6.51%라는 가장 높은 연평균 복합 성장률(CAGR)을 기록할 전망입니다. 중국 변환업체들은 1회용 음료 출시 속도를 따라잡기 위해 고속 라미네이션에 투자하고 있으며, 인도 골판지 제조업체들은 지역 물류 허브를 활용하기 위해 수성 코팅 라인을 추가하고 있습니다. 일본 브랜드 소유자들은 즉석 도시락용 차단 필름을 혁신하며 실온 경화형 저이동성 폴리우레탄 분산액 수요를 창출하고 있습니다. 중국의 2023년 과도한 포장 층 제한 의무화 등 국가별 포장 폐기물 규제로 인해 접착제 공급업체들은 박판 기판에서도 박리 없이 견디는 접착 기술을 개발해야 합니다. 아세안(ASEAN) 경제권 내 전자상거래 확산은 핫멜트 스틱과 강화형 접착 테이프 수요를 추가로 촉진할 전망입니다.

북미는 기술 도입의 선도적 역할을 지속하고 있습니다. 미국 환경보호청(EPA)의 구매 가이드라인은 40개 이상의 민간 친환경 인증을 참조하여 연방 기관들이 저휘발성유기화합물(VOC) 및 재생 소재 포장재를 선택하도록 유도합니다. 이로 인해 봉투 밀봉재와 군용 식사 키트 분야에서 수성 및 바이오 기반 등급 제품에 대한 수요가 증가하고 있습니다. 미국 대형 골판지 제조사들은 현재 톨오일 원료에서 추출한 질량 균형 EVA를 시험 중이며, 고객 평가표에서 측정 가능한 탄소 감축 효과를 입증하고자 합니다. 캐나다의 2021-2028 VOC 감축 계획은 다음 목표로 산업용 접착제를 지정하여 현지 제형 개발사들이 용제 대체를 가속화하도록 압박하고 있습니다.

유럽은 여전히 규제 선도자로서, 규정 2024/3190에 따른 식품 접촉 재료 내 비스페놀 A(BPA) 금지가 간접 식품 접촉 접착제의 새로운 기준을 설정했습니다. 독일의 DIN CERTCO는 퇴비화 가능 라미네이트를 인증하는 반면, 프랑스의 AGEC 법은 초박형 접착층이 여전히 필요한 단일 소재 유연 포장재를 촉진합니다. 동유럽 공장들은 서구 브랜드들이 생산 능력을 합리화함에 따라 이 변화를 활용해 계약 제조 경쟁에 나서고 있습니다. 브라질이 주도하는 남미는 식료품 체인점들이 핫멜트 EVA 혼합물로 밀봉된 소포를 사용하는 자체 브랜드 스낵 라인을 확장함에 따라 견실한 한 자릿수 중반 성장률을 보입니다. 규모는 작지만 중동 및 아프리카 지역에서는 사우디아라비아 유제품 부문과 남아프리카 과일 수출 사업의 수요 증가로 냉장 유통을 처리하는 습기 경화형 폴리우레탄 핫멜트 접착제의 시장 기회가 열리고 있습니다.

이러한 지역적 다각화는 포장용 접착제 시장을 지역적 경기 침체로부터 완충하는 역할을 합니다. 글로벌 규제 정보를 지역별 기술 서비스와 결합하는 공급업체들은 걸프 시장용 할랄 인증 원료 개발이나 적도 이남 지역 습도 수준에 맞춘 점착제 조정 등을 통해 높은 부가가치를 창출하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장의 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 식품 및 음료 산업의 수요 증가

- 식품 안전에 대한 인식 제고

- 접착제 제형의 기술 발전

- 전자상거래 업계 수요 증가

- 소매 및 소비재 부문의 확장

- 시장 성장 억제요인

- 엄격한 정부 규제

- 원자재 가격 변동

- VOC 배출 우려

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모와 성장 예측

- 기술별

- 수성

- 용제계

- 핫멜트

- 수지 화학별

- 아크릴

- 폴리우레탄

- 에틸렌-비닐 아세테이트(EVA)

- 스티렌계 블록 공중합체

- 천연/바이오기반

- 용도별

- 연포장

- 접이식 카톤 및 상자

- 라벨 및 테이프

- 씰링

- 기타 용도 (티슈 및 타월 오버랩, 그래픽 및 특수 용도)

- 최종 이용 산업별

- 식품 및 음료

- 의약품 및 헬스케어

- 퍼스널케어 및 화장품

- 산업용 및 소비재

- 전자상거래 및 소매 주문 처리

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Dow

- Dymax

- Franklin International

- HB Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Paramelt

- Sonoco Products Company

- Synthomer plc

- Wacker Chemie AG

제7장 시장 기회와 장래의 전망

HBR 25.11.27The Packaging Adhesives Market size is estimated at USD 20.71 billion in 2025, and is expected to reach USD 27.44 billion by 2030, at a CAGR of 5.79% during the forecast period (2025-2030).

Growth rests on four pillars: rising volumes of ready-to-eat food, an e-commerce boom that prioritizes tamper-evident sealing, regulatory pressure on volatile organic compound (VOC) emissions, and rapid uptake of bio-based chemistries. Water-based formulations command more than half of all revenue because they meet tightening air-quality rules without compromising bond strength, while hot-melt lines keep gaining share in automated fulfillment centers that demand quicker line speeds. Regionally, Asia-Pacific benefits from manufacturing scale and public-sector investment in recycling infrastructure, North America monetizes process innovation, and Europe enforces circular-economy rules that lift demand for repulpable or compostable grades. Competitive intensity stays moderate as large chemical producers use acquisitions, joint R&D, and scope-3 carbon targets to differentiate in an otherwise price-sensitive landscape.

Global Packaging Adhesives Market Trends and Insights

Growing Demand from the Food & Beverage Sector

Demand for barrier integrity and extended shelf life keeps the packaging adhesives market aligned with new product launches in beverages, dairy, and ready meals. Producers now specify migration-tested grades that pass multi-regional rules while running at lower line temperatures to save energy. Henkel's bio-based Technomelt Supra 079 Eco Cool, commercialized in 2024, contains 49% renewable content and cuts operating heat by 40 °C, which translates to 32% lower CO2 emissions and seamless recyclability with paper fibers. Similar energy-saving profiles help large bottlers achieve public climate milestones.

Increasing Awareness of Food Safety

Global regulators are closing loopholes in indirect-food-contact approvals. China's GB 4806.15-2024 introduces positive lists for 392 adhesive substances, mandatory labeling, and migration limits that apply on 8 February 2025. In parallel, the U.S. Food & Drug Administration phased out PFAS grease-proofing chemistries in early 2024, compelling converters to qualify non-fluorinated alternatives. The resulting compliance burden spurs multi-regional adhesive formulations that simplify documentation across export markets.

Stringent Government Regulations

VOC caps continue to tighten. New Jersey's 2024 draft lowers allowable VOCs in consumer adhesives to 7%, while California's rulebook bans 47 toxic air contaminants outright. European Union Regulation 2024/3190 removes Bisphenol A from food packaging, driving formulators to water-based or UV-cured alternatives. Compliance costs rise, yet early adopters gain pricing power through certified low-emission labels.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Adhesive Chemistry

- E-Commerce Packaging Requirements

- Fluctuating Raw Material Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-based systems held a 57.19% share of the packaging adhesives market in 2024 on revenue terms, reflecting converters' need to meet zero-solvent production targets. This dominance will expand at a 6.04% CAGR, far ahead of solvent-borne analogues. Fast-drying acrylic dispersions now bond multilayer films at room temperature, lowering oven dwell times. In parallel, upgraded rheology modifiers preserve bead shape on high-speed slot coaters, elevating throughput without adding stabilizers. Hot-melt chemistries rank a close second because warehouse automation favors instant set-up; innovations such as renewable-sourced polyolefin backbones shrink the carbon gap with water-based peers.

Stringent rules across Europe and North America guarantee demand longevity. As upcoming OECD guidelines quantify life-cycle emissions, brand owners lock in suppliers that disclose plant-level emissions data. Consequently, water-based lines are positioned to supply both mass-market corrugate and premium flexible laminates, reinforcing the packaging adhesives market size advantage of technology leaders through 2030. Solvent-based players will still serve niche high-temperature applications but face gradual erosion unless they reformulate toward ultra-low VOC blends.

EVA accounted for 30.51% of the packaging adhesives market size in 2024, underpinned by favorable cost-to-performance ratios and compatibility with diverse substrates. Its role in carton sealing, magazine spine gluing, and tamper-evident labeling sustains high volumes. To counter thermal sensitivity drawbacks, suppliers now blend metallocene polyethylene segments for stronger hot-tack, safeguarding margins as resin prices swing. Bio-based grades, although smaller in volume, are on track for a 6.71% CAGR as sugar-cane-derived monomers scale. Bostik's 60% bio-content cyanoacrylate line brings instant adhesion to high-value packages while cutting greenhouse-gas footprints, a template other majors aim to replicate.

Investor scrutiny of scope-3 disclosures speeds the transition. Multinationals with science-based targets screen vendors for on-site renewable energy and mass-balance certification, reallocating volume toward bio-based innovators. In parallel, acrylics and polyurethanes remain indispensable where chemical resistance or flexibility is vital, maintaining mid-single-digit growth. Collectively, this chemistry mix ensures the packaging adhesives market remains both competitive and innovation-rich.

The Packaging Adhesives Market Report Segments the Industry by Technology (Water-Based, Solvent-Based, and Hot-Melt), Resin Chemistry (Acrylics, Polyurethanes, and More), Application (Flexible Packaging, Folding Cartons and Boxes, and More), End-Use Industry (Food and Beverage, Pharmaceuticals and Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa).

Geography Analysis

Asia-Pacific dominated 2024 revenue with a 40.19% stake in the packaging adhesives market and is set to advance at the highest 6.51% CAGR. Chinese converters invest in high-speed lamination to keep pace with single-serve beverage launches, while Indian corrugators add water-based coating lines to tap regional fulfilment hubs. Japan's brand owners innovate barrier films for ready-to-eat bento boxes, creating demand for low-migration polyurethane dispersions that cure at room temperature. National packaging waste rules-such as China's 2023 mandate capping excessive wrap layers-force adhesive suppliers to engineer bonds that survive thinner substrates without delamination. Growing adoption of e-commerce across ASEAN economies adds further upside for hot-melt sticks and reinforced gummed tapes.

North America remains a trendsetter in technology adoption. The Environmental Protection Agency's purchasing framework references over 40 private ecolabels, steering federal agencies toward low-VOC and recycled-content packs. This shifts demand toward water-based and bio-based grades across envelope closures and military meal kits. Large-scale carton makers in the United States now trial mass-balance EVA derived from tall-oil feedstocks, aiming to show measurable carbon reductions in customer scorecards. Canada's 2021-2028 VOC reduction agenda targets industrial adhesives next, pushing local formulators to accelerate solvent replacement.

Europe remains the regulatory bellwether, with the ban on Bisphenol A in food contact materials under Regulation 2024/3190 setting a new baseline for indirect-food-contact adhesives. Germany's DIN CERTCO certifies compostable laminates, while France's AGEC law drives mono-material flexible packs that still require ultra-thin tie layers. Eastern European plants leverage this shift to compete for contract manufacturing as Western brands rationalize capacity. South America, led by Brazil, exhibits solid mid-single-digit growth because grocery chains extend private-label snack lines that use sachets sealed with hot-melt EVA blends. Although smaller, the Middle East and Africa witness rising demand in Saudi Arabia's dairy sector and South Africa's fruit export operations, opening space for moisture-cure polyurethane hot melts that handle cold-chain logistics.

Collectively, geographic diversification cushions the packaging adhesives market from localized downturns. Suppliers blending global regulatory intelligence with localized technical service capture outsized value by formulating halal-compliant raw materials for Gulf markets or tuning tackifiers for sub-equatorial humidity levels.

- 3M

- Arkema

- Ashland

- Avery Dennison Corporation

- Dow

- Dymax

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Jowat SE

- Paramelt

- Sonoco Products Company

- Synthomer plc

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand from the Food and Beverage Industry

- 4.2.2 Increasing Awareness for Food Safety

- 4.2.3 Technological Advancements in Adhesive Formulations

- 4.2.4 Growing Demand form the E-commerce industry

- 4.2.5 Expansion of Retail and Consumer Good Sector

- 4.3 Market Restraints

- 4.3.1 Stringent Government Regulations

- 4.3.2 Fluctiations in Raw Material Prices

- 4.3.3 Concerns of VOC Emissions

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 Water-based

- 5.1.2 Solvent-based

- 5.1.3 Hot-Melt

- 5.2 By Resin Chemistry

- 5.2.1 Acrylics

- 5.2.2 Polyurethanes

- 5.2.3 Ethylene-Vinyl Acetate (EVA)

- 5.2.4 Styrenic Block Copolymers

- 5.2.5 Natural/Bio-based

- 5.3 By Application

- 5.3.1 Flexible Packaging

- 5.3.2 Folding Cartons and Boxes

- 5.3.3 Labels and Tapes

- 5.3.4 Sealing

- 5.3.5 Other Applications (Tissue and Towel Over-wrap, Graphics and Specialty)

- 5.4 By End-Use Industry

- 5.4.1 Food and Beverage

- 5.4.2 Pharmaceuticals and Healthcare

- 5.4.3 Personal Care and Cosmetics

- 5.4.4 Industrial and Consumer Goods

- 5.4.5 E-Commerce Retail Fulfilment

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Ashland

- 6.4.4 Avery Dennison Corporation

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 Franklin International

- 6.4.8 H.B. Fuller Company

- 6.4.9 Henkel AG & Co. KGaA

- 6.4.10 Jowat SE

- 6.4.11 Paramelt

- 6.4.12 Sonoco Products Company

- 6.4.13 Synthomer plc

- 6.4.14 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment