|

시장보고서

상품코드

1687714

인도의 콤바인 수확기 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)India Combine Harvester - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

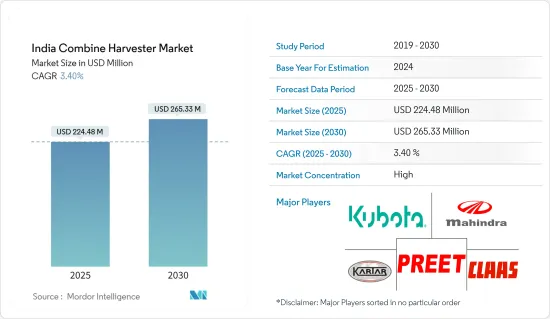

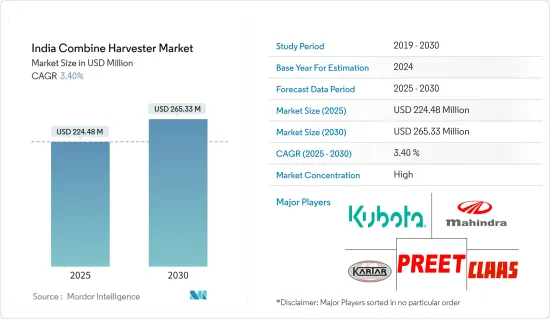

인도의 콤바인 수확기 시장 규모는 2025년에 2억 2,448만 달러로 예측되며, 예측 기간(2025-2030년) 동안 3.4%의 CAGR로 2030년에는 2억 6,533만 달러에 달할 것으로 예상됩니다.

주요 하이라이트

- 인도 농업연구위원회(ICAR)에 따르면, 인도에서 주요 곡물, 콩류, 유지종자, 잡곡, 환금작물(쌀과 밀 제외)의 수확 및 탈곡 작업은 32% 가까이 기계화되어 있습니다. 특히 쌀과 밀의 수확 및 탈곡 작업의 기계화율은 60%를 넘어섰습니다. 이러한 추세는 수확과 탈곡을 간소화하는 콤바인의 채택이 확대되고 있음을 강조하며, 시장 확대를 촉진하고 있습니다.

- 또한, 조사 기간 동안 다양한 작물의 재배 면적이 증가하고 있습니다. 예를 들어, FAOSTAT 통계에 따르면 인도 전역의 조곡 재배 면적은 2019년 9,510만 헥타르에서 2022년 9,960만 헥타르로 증가할 것으로 예상됩니다. 이는 콤바인에 큰 잠재력을 가지고 있는 것으로 보입니다.

- 조사 기간 동안 Preet 987, Mahindra Arjun 605, Kartar 4000, Dasmesh 9100 Self Combine Harvester, New Holland TC5.30, Kubota HARVESTING DC-68G-HK와 같은 유명 브랜드 가 인도에서 큰 존재감을 보이고 있습니다. 인도에서 이러한 콤바인이 채택되기 시작한 것은 농작업의 노동력 부족이 두드러지게 나타났기 때문입니다.

- 인도 정부는 기계를 포함한 다양한 농업 투입물에 보조금을 지급하고 있으며, 2022년에는 아삼 주 정부의 마을 개발을 위한 제도인 CMSGUY(Chief Minister's Samagra Gramya Unnayan Yojana)에 따라 아삼 주 치란 카운티의 농민과 생산자 기업(FPC) 2곳에 콤바인이 90%라는 놀라운 보조금 비율로 지급되었습니다. 보조금을 통해 콤바인 수확기를 보다 쉽게 이용할 수 있도록 하는 이러한 노력은 콤바인 수확기의 채택을 확대하여 시장 성장을 더욱 촉진할 것으로 보입니다.

인도의 콤바인 수확기 시장 동향

높은 농업 인건비

농업은 인구의 대다수에게 주요 생계 수단입니다. 인도 경제 조사 2022-23에 따르면, 농업 부문은 인도 노동 인구의 45.76%에 가까운 인구를 고용하고 있습니다. 인도에서 볼 수 있는 도시화 추세의 상승은 인구 증가의 결과입니다. 세계은행 자료에 따르면 2020년부터 2023년까지 도시화 정도는 34.9%에서 36.4%로 상승했습니다. 그 결과, 농촌 가구가 인근 도시로 이주하여 국내 농업 노동력이 부족하게 되었습니다. 예를 들어, 세계은행 자료에 따르면 2020년에서 2022년까지 농업에 종사하는 노동 인구는 44.3%에서 42.9%로 감소했습니다.

마찬가지로 농업 노동력 부족으로 인해 임금도 상승하여 농가의 전체 생산 비용이 상승했습니다. 인도 정부 통계에 따르면 2022년 인도 전체 여성 현장(농업) 노동자의 연간 평균 일당은 328.51 인도 루피(4달러)로 전년 대비 8.32% 증가한 것으로 보고됐습니다. 마찬가지로, 남성 현장(농업) 노동의 경우, 인도 전체의 일당은 2022년 394.52 인도 루피(USD 4.8)로 전년 대비 8.55% 상승한 것으로 보고되었습니다. 이로 인해 농가의 고용이 억제되고 콤바인의 도입이 진행되고 있습니다.

이 나라의 농업은 수작업에 크게 의존하고 있으며, 농업 종사자의 감소는 수확과 같은 농작업을 수행하는 데 있어 큰 도전이 되고 있습니다. 이 문제의 해결책으로, 이러한 농작업을 효과적이고 효율적으로 수행하기 위한 첨단 수확 기계의 사용이 점점 더 널리 보급되고 있습니다.

인도의 곡물 재배 증가로 자체 추진식 콤바인 수확기 수요 촉진

인도에서 곡물은 식탁에서 매우 중요한 역할을 하고 있으며, 인도는 주요 곡물 생산국이자 소비국으로서 주요 식량 생산국이자 소비국입니다. 곡물 소비가 증가함에 따라 재배 면적을 확대할 필요성이 커지고 있습니다. 이러한 추세는 곡물 및 곡류의 수확 면적이 증가하는 추세에서 알 수 있습니다. 예를 들어, FAOSTAT에 따르면 곡물 수확 면적은 2019년 9,510만 헥타르에서 2022년 9,960만 헥타르로 증가할 것으로 예상됩니다. 콤바인, 특히 자체 추진 콤바인이 주로 곡물에 이용된다는 점을 감안할 때, 이러한 재배의 증가는 이러한 장비에 대한 수요를 직접적으로 증가시켜 시장 성장을 촉진할 것입니다.

강력한 엔진이 장착된 자율주행 콤바인은 밭에서 작업하기에 적합하며, 효율적인 수확과 생산성 향상을 보장합니다. 이러한 생산성 향상은 이 부문 확대의 중요한 원동력입니다. 자율주행 콤바인은 인도 북부, 서부 및 중부 지역에서 주로 쌀, 밀 및 기타 계절 작물에 사용됩니다. 또한, 특히 펀자브(Punjab)와 할리야나(Haryana)와 같은 주요 쌀 및 밀 재배 지역에서 대규모 농부들이 이 콤바인을 사용하는 것이 유리한 관행으로 작용하여 다른 농부들의 채택이 급증하고 있습니다.

곡물 작물 전용 지역 확대에 대응하기 위해 제조업체들은 곡물 작물 전용 콤바인 제품을 출시하고 있습니다. 마힌드라 & 마힌드라의 자회사인 스와라지(Swaraj) 사업부는 2021년 10월 자율주행 콤바인 'Gen2 8100 EX'를 출시했습니다. 이 모델은 논 농가의 생산성과 성능을 향상시키고, 넓은 면적에서 최적의 곡물 수확량을 확보하는 것을 목표로 하고 있습니다.

인도의 콤바인 수확기 산업 개요

인도 콤바인 시장은 통합되어 있으며, Claus India, Preet Group, Kubota Corporation, Mahindra &Mahindra Ltd, Kartar Agro Industries Private Limited가 주요 시장 기업입니다. 이들은 제품의 품질과 판매 촉진으로 경쟁하고, 전략적 노력에 중점을 두어 압도적인 시장 점유율을 차지하고 있습니다. 또한, R&D 활동을 강화하면서 시장 점유율을 확대하기 위해 타사와의 제휴 및 인수를 추진하고, 신제품 개발에 많은 투자를 하고 있습니다.

기타 특전:

- 엑셀 형식의 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

목차

제1장 소개

- 조사 가정과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 작물 생산 강화의 필요성

- 정부 지원 증가

- 농업기계화 수요

- 시장 성장 억제요인

- 콤바인 수확기의 고비용

- 소규모이고 단편적인 토지 보유

- 업계의 매력 - Porter's Five Forces 분석

- 공급 기업의 교섭력

- 구매자의 교섭력

- 신규 참여업체의 위협

- 대체품의 위협

- 경쟁 기업 간의 경쟁 강도

제5장 시장 세분화

- 유형

- 자주식 콤바인 수확기

- 트럭식 콤바인 수확기

- 트랙터식 콤바인 수확기

제6장 경쟁 구도

- 가장 많이 채용되고 있는 전략

- 시장 점유율 분석

- 기업 개요

- PREET Group

- John Deere India Pvt. Ltd

- CLAAS India

- Tractors and Farm Equipment(TAFE) Ltd

- Mahindra Tractors

- Kubota Agricultural Machinery India Pvt. Ltd

- Dasmesh Group

- Balkar Combines

- Kartar Agro Industries Pvt. Ltd

- Sonalika Group

제7장 시장 기회와 향후 동향

ksm 25.05.12The India Combine Harvester Market size is estimated at USD 224.48 million in 2025, and is expected to reach USD 265.33 million by 2030, at a CAGR of 3.4% during the forecast period (2025-2030).

Key Highlights

- Indian Council of Agricultural Research (ICAR), in India, harvesting and threshing operations for major cereals, pulses, oil seeds, millets, and cash crops (excluding rice and wheat) are nearly 32% mechanized. Notably, mechanization levels for harvesting and threshing in rice and wheat exceed 60%. This trend emphasizes the growing adoption of combine harvesters, which streamlines harvesting and threshing, bolstering market expansion.

- Additionally, the area under cultivation of various crops has been rising during the study period. For instance, according to the FAOSTAT Statistics, the total area for cultivating coarse cereals across India increased from 95.1 million hectares in 2019 to 99.6 million hectares in 2022. This seems like a great potential for combine harvesters.

- Throughout the study period, prominent brands such as Preet 987, Mahindra Arjun 605, Kartar 4000, Dasmesh 9100 Self Combine Harvester, New Holland TC5.30, and Kubota HARVESTING DC-68G-HK have established a significant presence in the country. The rising adoption of these combines in India can be largely attributed to a notable shortage of farm labor.

- The Indian government extends subsidies on various agricultural inputs, including machinery. In 2022, under the Chief Minister's Samagra Gramya Unnayan Yojana (CMSGUY) - a scheme by the Assam Government aimed at village development - two farmer-producer companies (FPCs) in Assam's Chirang District were granted combined harvester machinery at a remarkable 90% subsidized rate. Such initiatives, making combined harvester machinery more accessible through subsidies, are poised to amplify their adoption and further fuel market growth.

India Combine Harvester Market Trends

High Cost of Farm Labor

Agriculture is a major source of livelihood for a large group of the population. As per the Indian Economic Survey 2022 -23, the agriculture sector employs nearly 45.76% of the Indian workforce. The rise in urbanization trends observed in the country is a result of the expanding population. According to the World Bank data, the degree of urbanization increased from 34.9% to 36.4% from 2020 to 2023. This resulted in the migration of rural households to the nearby cities, leading to the scarcity of farm labor in the country. For instance, the workforce employed in agriculture dropped from 44.3% to 42.9% from 2020 to 2022, as per the World Bank data.

Likewise, the scarcity of farm labor also increased wage rates, which increased the overall production costs of the farmers. As per the Government of India statistics, the annual average daily wage rate for female field (Agriculture) labor, at all India levels, has reported at ₹ 328.51 (USD 4.0) in 2022, registering an increase of 8.32% over the previous year. Likewise, in the case of male field (agriculture) labor, the daily wage rate at all India levels was reported at ₹ 394.52 (USD 4.8) in 2022, registering an increase of 8.55 percent over the previous year. This resulted in a restrain in employing them in farms, favoring the adoption of combine harvesters by the farmers in the country.

The agricultural industry of the country heavily relies on manual labor, and the decreasing workforce in agriculture has led to major challenges in performing farming operations such as harvesting. As a solution to this problem, the usage of advanced harvesting machinery has become increasingly popular for performing these agricultural operations effectively and efficiently.

Rising Grain Cultivation in India Fuels Demand for Self-Propelled Combine Harvesters

In India, cereals play a pivotal role in the culinary landscape, positioning the nation as a leading producer and consumer of these staples. As the consumption of cereal crops rises, so does the need for expanded cultivation. This trend is evident, with harvested areas for cereals and grains on the upswing. For instance, according to FAOSTAT, the area harvested under cereals increased from 95.1 million hectares in 2019 to 99.6 million hectares in 2022. Given that combines, especially self-propelled ones, are predominantly utilized for cereals, this uptick in cultivation directly boosts the demand for such equipment, propelling the market growth.

Equipped with a robust engine, self-propelled combine harvesters excel in the fields, ensuring efficient harvesting and heightened productivity. This boost in productivity is a key driver for the segment's expansion. Predominantly, these harvesters find their application in Northern, Western, and Central India, catering mainly to rice, wheat, and other seasonal crops. Moreover, the lucrative custom hiring of these harvesters by large farmers, especially in major rice-wheat regions like Punjab and Haryana, has led to a surge in adoption among other farmers.

In response to the expanding areas dedicated to grain crops, manufacturers are rolling out specialized combine harvester products tailored for these crops. A case in point is Swaraj Division, a Mahindra and Mahindra Ltd subsidiary, which unveiled its Gen2 8100 EX self-propelled combine harvester in October 2021. This model aims to enhance productivity and performance for paddy farmers, ensuring optimal grain yield across extensive acreage.

India Combine Harvester Industry Overview

The Indian combined harvester market is consolidated. Claas India, Preet Group, Kubota Corporation, Mahindra & Mahindra Ltd, and Kartar Agro Industries Private Limited are the major market players. Companies compete based on product quality and promotion and focus on strategic initiatives to account for prominent market shares. They are also heavily investing in developing new products while collaborating with and acquiring other companies, which may increase their market shares while strengthening their R&D activities.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need to Enhance Crop Production

- 4.2.2 Increase In Government Support

- 4.2.3 Demand for Farm Mechanization

- 4.3 Market Restraints

- 4.3.1 High Cost of Combine Harvesters

- 4.3.2 Small and Fragmented Land Holdings

- 4.4 Industry Attractiveness - Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Type

- 5.1.1 Self-propelled Combine Harvester

- 5.1.2 Track Combine Harvester

- 5.1.3 Tractor-powered Combine Harvester

6 COMPETITIVE LANDSCAPE

- 6.1 Most Adopted Strategies

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 PREET Group

- 6.3.2 John Deere India Pvt. Ltd

- 6.3.3 CLAAS India

- 6.3.4 Tractors and Farm Equipment (TAFE) Ltd

- 6.3.5 Mahindra Tractors

- 6.3.6 Kubota Agricultural Machinery India Pvt. Ltd

- 6.3.7 Dasmesh Group

- 6.3.8 Balkar Combines

- 6.3.9 Kartar Agro Industries Pvt. Ltd

- 6.3.10 Sonalika Group