|

시장보고서

상품코드

1687854

보안 오케스트레이션 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Security Orchestration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

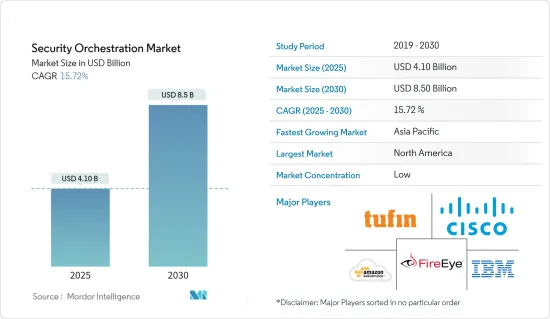

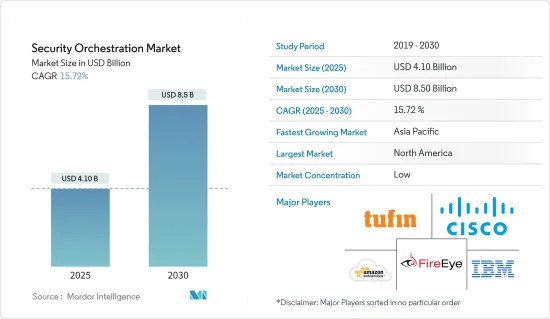

보안 오케스트레이션 시장 규모는 2025년에 41억 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 15.72%로 성장할 전망이며, 2030년에는 85억 달러에 달할 것으로 예측됩니다.

다양한 조직에 보안 오케스트레이션을 도입함으로써 보안 경보를 관리하고 심각한 사이버 공격을 방지할 수 있습니다. 사이버 공격의 고도화에 따라 보안 벤더는 중요한 비즈니스 용도를 처리하기 위한 능동적이고 종합적인 보안 아키텍처를 제공하기 위해 더 나은 오케스트레이션 플랫폼을 개발하려고 합니다.

주요 하이라이트

- 중소기업에 영향을 미치는 BYOD 동향의 극적인 증가와 클라우드 기반 솔루션의 급속한 전개와 개발에 의해 보안 침해나 보안 사건이 증가하고 있어 다양한 조직에서 보안 오케스트레이션 적용에 박차를 가하고 있습니다.

- 컴퓨터 네트워크 트래픽을 모니터링 및 관리하기 위해 보안 오케스트레이션 플랫폼을 채용하는 기업이 늘고 있기 때문에 네트워크 포렌식 용도가 증가하여 시장 수요를 촉진할 것으로 예상됩니다.

- 커넥티드 디바이스의 보급에 따라, 다양한 IT 서비스나 솔루션의 채용이 증가하고 있기 때문에 날마다 생성되는 데이터량이 더욱 증가해, 그 결과, 효과적인 관리와 봉쇄가 필요한 잠재적 취약성의 범위가 방대해지고 있습니다.

- 이러한 솔루션의 도입으로 ITIL, PCI, HIPAA(Health Insurance Portability and Accountability Act: 의료보험 상호 운용성 및 책임 법), SOX법(Sarbanes-Oxley Act : 서벤스 옥슬리법), 그람 리치 브라일리법(Gramm-Leach-Bliley) Act : 그람 리치 브라일리법)과 같은 감사 컴플라이언스 요건에의 준거도 용이하게 되어, 적극적인 시책의 실시나 감사 컴플라이언스 보고서의 작성이 가능하게 되었습니다. 이러한 요인이 시장의 성장을 뒷받침하고 있습니다.

보안 오케스트레이션 시장 동향

IT 및 통신 부문이 대폭적인 성장을 기록할 전망

- IT 및 통신 산업은 수백만의 고객을 연결하는 세계와 국내의 폭넓은 서비스를 제공합니다. 이 다양한 생태계는 모든 업무를 수행하는 데 있어 인프라, 네트워크, 데이터베이스에 크게 의존하기 때문에 사이버 공격을 자주 받습니다.

- 통신 사업자는 일반적으로 성명, 주소, 재무 데이터 등 고객의 개인 정보를 저장합니다. 정보에 민감한 데이터는, 내부 관계자나 사이버 범죄자에게 있어서, 금전을 훔치거나, 고객을 공갈하거나, 새로운 공격을 가하기 위한 형태의 표적이 됩니다. 그 때문에, 이 산업에서는, 최신의 솔루션, 적절한 툴, 선진적 훈련을 받은 인재, 위협에 즉시 대응하는 능력에 보다 중점을 두는 것이 요구되고 있습니다.

- SOAR 도구는 IT 팀이 조직의 사고 대응 활동을 정의, 표준화 및 자동화할 수 있도록 지원합니다. 대부분의 IT 조직은 이러한 도구를 사용하여 보안 운영 및 프로세스 자동화, 사고 대응, 취약성 및 위협 관리를 수행합니다. 또한 보안 오케스트레이션은 엔터프라이즈 보안에 종사하는 IT 전문가의 위협 대응 및 해결에 소요되는 시간을 단축합니다.

- 클라우드 및 IoT를 통한 데이터 연결 증가는 IT 부문의 핵심 과제가 되었으며, 보안은 데이터 침해로부터 자신을 보호하기 위해 산업의 모든 조직에 최우선 과제가 되었습니다. 게다가 COVID-19의 대유행은 정보통신기술 기업이 비즈니스 프로세스를 재검토하고 통신 네트워크 수요가 두배로 되고 있는 경우 특히 대유행을 통해 고객에게 안정적인 서비스를 제공하기 위해 네트워크 성능을 향상시킬 필요가 있습니다. 따라서 기업은 이러한 보안 오케스트레이션 솔루션을 채택하여 시장 성장률을 높이고 있습니다.

북미가 가장 큰 시장 점유율을 차지

- 북미는 IBM Corporation, DXC Technology Company, Cisco System Inc., FireEye Inc. 등 이 지역의 많은 저명한 보안 오케스트레이션 공급업체 덕분에 보안 오케스트레이션 시장을 독점하고 있습니다. 최종 사용자 산업의 성장, 중요 인프라에 대한 정부 지출, 확립된 R&D 센터, 첨단 보안 기술에 대한 수요 등의 요인이 이 지역 시장 성장을 가속할 것으로 예상됩니다.

- 이 지역의 사이버 공격 증가는 시장 성장에 더욱 기여하고 있습니다. 2021년 미국 국가안전보장국(NSA), 사이버보안인프라보안국(CISA), 연방수사국(FBI)은 미국의 16개 주요 인프라 부문 중 국방산업기반, 긴급서비스, 식품 및 농업, 정부 시설, 정보 기술 부문을 포함한 14개 부문에 대해 랜섬웨어가 관여하는 사건을 확인했다고 보고했습니다.

- 또, 다양한 조직이, 네트워크의 복잡성이 과거 몇년간에 증대해, 향후 5년간도 계속 증가할 것을 인정하고 있습니다. 따라서 해킹이나 사이버 공격에 의한 산업 프로세스의 안전 확보를 막기 위한 네트워크 보안의 필요성이 높아지고 있으며, 이에 보안 오케스트레이션이 그 역할을 하고 있습니다.

- 게다가 이 지역에서는 하이브리드와 멀티클라우드 환경에 채용되는 새로운 클라우드 툴이 폭발적으로 증가하고 있으며, 동시에 기존 클라우드 플랫폼은 새로운 하이브리드의 현실에 적합하도록 방향 전환하고 있습니다.

보안 오케스트레이션 산업 개요

보안 오케스트레이션 시장은 경쟁이 치열하여 여러 대기업이 참가하고 있습니다. 시장 점유율에서는 현재 소수의 대기업이 시장을 독점하고 있습니다. 게다가 클라우드 네트워크 부문의 출현으로 대부분의 기업이 SOAR 시장에서의 위상을 높이고 후속 시장 전체의 고객을 획득하고 있습니다. 게다가 각 회사는 협업 및 솔루션의 시작 등, 다양한 전략을 선택해, 시장 성장률에 공헌하고 있습니다. 예를 들면

- 2023년 3월-IBM과 Cohesity는 하이브리드 클라우드 환경에서 데이터 보안과 신뢰성을 향상시키는 조직의 필수적인 요구에 부응하기 위해 새로운 파트너십을 맺었습니다. IBM Storage Defender는 랜섬웨어, 휴먼 에러, 공격 등의 위협으로부터 조직의 데이터 레이어를 보호하기 위해 하나의 창을 통해 다양한 스토리지 플랫폼 전체에서 AI와 이벤트 모니터링을 사용하도록 개발되었습니다.

- 2023년 2월-사이버 위협 인텔리전스 및 보안 운영 최적화에 대한 고객의 요구를 지원하는 위협 인텔리전스 기업인 모라드 인텔리전스와 기업 및 MSSP/MDR용 저 코드 SOAR 및 위협 인텔리전스 자동화 기능을 탑재 한 사이버 퓨전 센터, ISAC 및 ISAO에 대한 위협 인텔리전스 공유 솔루션을 구축하는 기술 플랫폼을 제공하는 사이웨어는 파트너십을 체결했습니다. 이 파트너십의 주요 목적은 사이웨어의 첨단 TIP & SOAR 모듈을 사용하여 위협 데이터의 효과적인 도입, 강화, 분석 및 대응을 통해 Morado의 강력한 고객 포트폴리오를 보다 쉽게 만드는 것입니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 산업의 매력-Porter's Five Forces 분석

- 신규 진입업자의 위협

- 구매자 및 소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

- COVID-19가 시장에 미치는 영향

제5장 시장 역학

- 시장 성장 촉진요인

- 원활한 워크 플로우를 실현하는 보안 운용의 높은 자동화 동향

- 네트워크의 복잡성에 대응하기 위한 개별 사이버 보안 기술의 필요성

- 시장 성장 억제요인

- 전문가의 인식 부족

- 기술 스냅샷

제6장 시장 세분화

- 유형별

- 소프트웨어

- 서비스

- 최종 사용자 산업별

- BFSI

- IT 및 통신

- 정부 및 방위

- 전자상거래

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 프랑스

- 독일

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 호주

- 기타 아시아태평양

- 기타

- 라틴아메리카

- 중동 및 아프리카

- 북미

제7장 경쟁 구도

- 기업 프로파일

- IBM Corporation

- Tufin Software Technologies Ltd

- DXC Technology Company

- Cisco System Inc.

- Swimlane LLC

- RSA Security LLC

- FireEye Inc.

- DFLabs SpA

- Palo Alto Networks Inc.

- Siemplify Ltd

- Accenture PLC

- Amazon Web Services Inc.

- Cyberbit Ltd

- Forescout Technologies Inc.

제8장 투자 분석

제9장 시장 기회 및 향후 동향

AJY 25.05.07The Security Orchestration Market size is estimated at USD 4.10 billion in 2025, and is expected to reach USD 8.50 billion by 2030, at a CAGR of 15.72% during the forecast period (2025-2030).

The implementation of security orchestration across various organizations can help manage security alerts and prevent severe cyber-attacks. As the sophistication level in cyber-attacks is increasing, security vendors are trying to develop better orchestration platforms to provide proactive and holistic security architecture to handle critical business applications.

Key Highlights

- An increase in the security breaches and occurrences due to dramatic growth in the BYOD trend affecting SMEs, along with the rapid deployment and development of cloud-based solutions, is fueling the application of security orchestration among various organizations.

- A rise in the application of network forensics is expected to drive the market demand, as a growing number of companies are adopting the security orchestration platform to monitor and manage their computer network traffic.

- Growing adoption of various IT enabled services and solutions, due to the growing popularity of connected devices, has further boosted the amount of data generated daily, subsequently resulting in a vast scope for potential vulnerabilities that need effective management and containment.

- Implementation of these solutions has also enabled improved adherence to audit and compliance requirements easily, with proactive policy enforcement and audit and compliance reports, such as ITIL, PCI, Health Insurance Portability and Accountability Act (HIPAA), Sarbanes-Oxley Act (SOX), and Gramm-Leach-Bliley Act. These factors have been aiding the growth of the market.

Security Orchestration Market Trends

IT and Telecommunication Sector is Projected to Record Significant Growth

- The IT and telecommunication industry offers a wide range of global and domestic services for connecting millions of customers. This diverse ecosystem is more prone to frequent cyber attacks, as they are highly dependent on their infrastructure, network, and databases to perform any operation.

- Telecom organizations typically store customers' personal information, such as names, addresses, and financial data. Information-sensitive data is a compelling target for insiders or cyber-criminals to steal money, blackmail customers, or launch further attacks. Therefore, the industry demands a greater focus on updated solutions, the right tools, highly trained personnel, and the ability to respond to threats immediately.

- SOAR tools aid IT teams in defining, standardizing, and automating organizations' incident response activities. Most IT organizations use these tools to automate security operations and processes, respond to incidents, and manage vulnerabilities and threats. Moreover, security orchestration reduces the threat response and resolution time for IT professionals working in enterprise security.

- With the increased data connectivity with the cloud as well as IoT taking center stage in the IT sector, security has been a top priority for the all the organizations in the industry to protect themselves from the data breaches. Further, COVID-19 pandemic has led Information and communication technology organizations to rethink their business processes and improve their network performance to provide their customers with reliable services throughout the pandemic, specially when the demand for telecom networks has doubled. Thus, companies are adopting these security orchestration solutions thereby driving the market growth rate.

North America Accounts for the Largest Market Share

- North America dominates the security orchestration market, owing to many prominent security orchestration vendors across the region, such as IBM Corporation, DXC Technology Company, Cisco System Inc., FireEye Inc., etc. Factors such as the growing end-user industries, government expenditure toward critical infrastructure, well-established R&D centers, and the demand for advanced security technology across the region are expected to drive market growth.

- The growing number of cyber attacks in the region further contributes to the market growth. In 2021, The National Security Agency (NSA), the Cybersecurity and Infrastructure Security Agency (CISA), and the Federal Bureau of Investigation (FBI) reportedly witnessed occurrences involving ransomware against 14 of the 16 critical infrastructure sectors in the United States, including the Defense Industrial Base, Emergency Services, Food and Agriculture, Government Facilities, and Information Technology Sectors.

- Also, various organizations have admitted that network complexity has increased over the past few years and will continue to increase over the next five years. Therefore, there is a high need for network security to stop hacking and cyber-attacks from securing industrial processes, and that is where security orchestration plays its part.

- Further, the region is witnessing an explosion of new cloud tools adopted for hybrid and multicloud environments, while at the same time, established cloud platforms are pivoting to fit into the new hybrid reality.

Security Orchestration Industry Overview

The security orchestration market is highly competitive and consists of several major players. In terms of market share, few major players currently dominate the market. Moreover, due to the emergence of the cloud network segment, most companies are increasing their SOAR market presence, tapping customers across the subsequent markets. Further, the players are opting for various strategies, such as collaborations and solution launches, thereby contributing to the market growth rate. For instance:

- March 2023-IBM and Cohesity have formed a new partnership to meet organizations' essential need for better data security and reliability in hybrid cloud settings. IBM Storage Defender is being developed to use AI and event monitoring across various storage platforms through one single window to assist in safeguarding organizations' data layer from threats, including ransomware, human error, and attack.

- February 2023-Morado Intelligence, a threat intelligence company that assists clients with their needs for cyber threat intelligence and security operations optimisation, and Cyware, a provider of the technology platform to build low-code SOAR and threat intel automation powered Cyber Fusion Centres for businesses and MSSPs/MDRs, as well as threat intelligence sharing solutions for ISACs and ISAOs, have formed a partnership. The partnership's primary objective is to make it easier for Morado's robust client portfolio to use Cyware's advanced TIP & SOAR modules to effectively ingest, enhance, analyze, and respond on threat data.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Attractiveness - Porter's Five Forces Analysis

- 4.2.1 Threat of New Entrants

- 4.2.2 Bargaining Power of Buyers/Consumers

- 4.2.3 Bargaining Power of Suppliers

- 4.2.4 Threat of Substitute Products

- 4.2.5 Intensity of Competitive Rivalry

- 4.3 Impact of COVID-19 on the market

5 Market Dynamics

- 5.1 Market Drivers

- 5.1.1 Rising Trend of Automated Security Operation for Seamless Workflow

- 5.1.2 Need of Disparate Cybersecurity Technologies to Handle Network Complexity

- 5.2 Market Restraints

- 5.2.1 Lack of Awareness among Professionals

- 5.3 Technology Snapshot

6 MARKET SEGMENTATION

- 6.1 Type

- 6.1.1 Software

- 6.1.2 Services

- 6.2 End-user Industry

- 6.2.1 BFSI

- 6.2.2 IT and Telecommunication

- 6.2.3 Government and Defence

- 6.2.4 E-commerce

- 6.2.5 Other End-user Industries

- 6.3 Geography

- 6.3.1 North America

- 6.3.1.1 United States

- 6.3.1.2 Canada

- 6.3.2 Europe

- 6.3.2.1 United Kingdom

- 6.3.2.2 France

- 6.3.2.3 Germany

- 6.3.2.4 Rest of Europe

- 6.3.3 Asia-Pacific

- 6.3.3.1 China

- 6.3.3.2 Japan

- 6.3.3.3 Australia

- 6.3.3.4 Rest of Asia-Pacific

- 6.3.4 Rest of the World

- 6.3.4.1 Latin America

- 6.3.4.2 Middle-East & Africa

- 6.3.1 North America

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 IBM Corporation

- 7.1.2 Tufin Software Technologies Ltd

- 7.1.3 DXC Technology Company

- 7.1.4 Cisco System Inc.

- 7.1.5 Swimlane LLC

- 7.1.6 RSA Security LLC

- 7.1.7 FireEye Inc.

- 7.1.8 DFLabs SpA

- 7.1.9 Palo Alto Networks Inc.

- 7.1.10 Siemplify Ltd

- 7.1.11 Accenture PLC

- 7.1.12 Amazon Web Services Inc.

- 7.1.13 Cyberbit Ltd

- 7.1.14 Forescout Technologies Inc.