|

시장보고서

상품코드

1689745

농업용 윤활유 시장 : 점유율 분석, 산업 동향과 통계, 성장 예측(2025-2030년)Agriculture Lubricants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

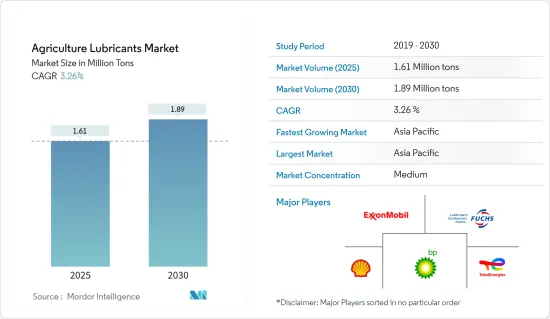

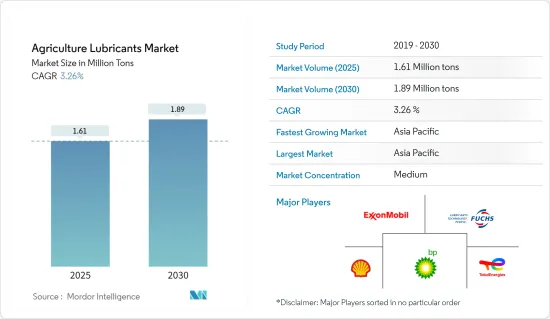

세계의 농업용 윤활유 시장 규모는 2025년 161만톤으로 추정되며 예측 기간 중(2025-2030년) CAGR 3.26%를 나타낼 전망이며, 2030년에는 189만톤에 달할 것으로 예측됩니다.

2020년, 농업용 윤활유 시장은 COVID-19 바이러스의 발생에 의해 악영향을 받았고, 세계적으로 봉쇄나 다양한 정부 규제가 이루어졌습니다. 그러나 2021년과 2022년에는 백신 접종 증가로 각국은 서서히 폐쇄 등의 규제를 해제했습니다.

인도나 중국 정부에 의한 농업기계에의 보조금 지급, 신흥 국가에서의 농업 기계화율의 상승, 농업노동 비용의 상승 등의 요인이 시장의 현저한 촉진요인이 될 것으로 예측됩니다.

그러나 합성 윤활유 및 바이오 윤활유의 비용이 높다는 것은 예측 기간 동안 시장 성장을 방해하는 것으로 예상됩니다.

생분해성 윤활유의 주목도 증가는 예측 기간 동안 시장 성장의 기회가 될 것으로 예상됩니다.

예측 기간 동안 아시아태평양은 세계 농업용 윤활유 시장을 독점할 것으로 예상됩니다.

농업용 윤활유 시장 동향

엔진 오일이 시장을 독점

- 엔진 오일 또는 모터 오일은 내연 엔진의 윤활에 널리 사용되고 있으며, 주로 75%-90%의 기유와 10%-25%의 첨가제로 구성되어 있습니다.

- 농업 부문에서 엔진 오일은 트랙터, 수확기, 사료 기계에 사용되며 유지 보수 경감, 마모 및 부식 방지, 엔진 신뢰성 향상, 연비 개선에 도움이 됩니다.

- Pacific Fuel Solutions에 따르면 농업용 윤활유와 오일은 다양한 기능에 사용되지만, 가장 두드러진 예 중 하나가 엔진 오일입니다.

- Total, Royal Dutch Shell Plc, Chevron Lubricants, CONDAT Group, Schaeffer Manufacturing Co.는 다양한 종류의 농업기계용 엔진오일을 제공하는 중요한 윤활유 제조업체입니다

- 일부 대형 벤더는 혁신적인 장비를 개발하고 트랙터 시장의 골격을 강화하기 위해 연구 개발에 투자하고 있습니다.

- 농업의 자동화가 진행되어 식량의 증산과 농지의 확대가 더해져, 농업기계나 농업용 기기의 신품 및 중고품 수요는 해마다 증가할 것으로 예측됩니다.

- 예를 들어 국제곡물협회(International Grains Council)는 2023-24년 시즌의 곡물 생산량을 2022-23년 시즌의 22억 5,400만 톤에서 1.77% 증가한 22억 9,400만 톤으로 예측했습니다.

- Lemken의 Anthony van der LeyCEO에 따르면 지난 12개월 동안 모든 국제 시장에서 볼 수 있는 인플레이션률의 상승과 이에 따른 금리에 대한 영향으로 2024년에는 국제적인 농기계 판매량이 6-7% 감소할 가능성이 높습니다.

- 게다가 Progressive Dairy에 따르면, 캐나다의 중고 농기 시장은 금리 상승 때문에 2023년의 대부분으로부터 2024년까지 견조하게 추이할 것으로 예상되고 있습니다.

- 예측 기간 동안, 상기의 모든 요인이 농업용 윤활유 시장에 있어서의 엔진 오일의 우위성에 영향을 미칠 것으로 예측됩니다.

아시아태평양 급성장

- 중국은 세계 최대의 윤활유 소비국입니다.

- 이 나라는 쌀, 면화, 감자 등 다양한 작물의 가장 큰 생산국입니다.

- 예를 들어, 경작 면적 증가는 중국에서의 농업 기계 수요를 높이고 있습니다.

- 인도는 이 지역에서는 제2위, 세계적으로는 미국과 중국에 이어 제3위의 윤활유 소비국입니다.

- 인도는 농업에 크게 의존하고 있는 경제의 하나입니다.

- 2022년, 인도에서의 트랙터 수출은 6% 증가해, 13만 1,850대에 이르렀습니다.

- 게다가 일본 정부는 농업 생산을 2013년 5,000만 톤에서 2025년까지 5,400만 톤으로 늘릴 계획입니다. 또한 정부는 농업 생산량과 수익의 향상과 비용 절감에 의해 생산자 소득을 290억 달러에서 350억 달러로 동기간에 약 21% 증가할 계획입니다.

- 아시아태평양의 농업에 있어서의 이러한 동향은 예측 기간중, 농업용 윤활유 시장의 성장을 세계 최고속으로 견인할 것으로 예상됩니다.

농업용 윤활유 산업 개요

농업용 윤활유 시장은 본질적으로 부분적으로 통합되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 인도 정부와 중국 정부에 의한 농업 기계에의 보조금 지급

- 신흥 국가의 농업 기계화율 상승

- 농업노동비용 상승

- 억제요인

- 합성 및 바이오 윤활유의 높은 비용

- 기타 억제요인

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 제품 유형

- 엔진 오일

- 변속기 및 유압 작동유

- 그리스

- 기타

- 지역

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 기타

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율(%)**/랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- BP plc

- Chevron Corporation

- CLASS KGaA mbH

- CONDAT

- Cougar Lubricants International Ltd.

- Exol Lubricants Limited

- Exxon Mobil Corporation

- FRONTIER PERFORMANCE LUBRICANTS, INC.

- Fuchs

- Gulf Oil International Ltd.

- Hf Sinclair Corporation

- Lubrication Engineers

- Morris Lubricants

- Pennine Lubricants

- Phillips 66 Company

- Repsol

- Rymax Lubricants

- Schaeffer Manufacturing Co.

- Shell plc

- TotalEnergies SE

- Unil

- Witham Group

제7장 시장 기회와 앞으로의 동향

- 생분해성 윤활유의 중요성 증가

- 기타 기회

The Agriculture Lubricants Market size is estimated at 1.61 million tons in 2025, and is expected to reach 1.89 million tons by 2030, at a CAGR of 3.26% during the forecast period (2025-2030).

In 2020, the agricultural lubricants market was affected negatively due to the outbreak of the COVID-19 virus, which resulted in lockdowns and different government restrictions worldwide. As a result, the agriculture equipment industry witnessed challenges as several companies struggled to remain operational because of the pandemic. However, in 2021 and 2022, the increased number of vaccinations helped the countries to gradually uplift restrictions like lockdowns. This also marked the recovery of the agriculture equipment industry and, thus, of the agricultural lubricants.

Factors such as the provision of subsidies for farm machinery by the Indian and Chinese governments, increasing farm mechanization rates in developing countries, and increasing cost of farm labor are projected to be the prominent drivers of the market.

However, the high cost of synthetic and bio-based lubricants will likely hinder market growth during the forecast period.

The growing prominence of biodegradable lubricants will likely act as an opportunity for market growth during the forecast period.

Asia-Pacific is expected to dominate the global agricultural lubricants market during the forecast period.

Agricultural Lubricants Market Trends

Engine Oil Dominates the Market

- Engine or motor oils are widely used for lubricating internal combustion engines and are mainly composed of 75% to 90% base oils and 10% to 25% additives. They protect the engines from corrosion and keep them cool while in use.

- In the agricultural sector, engine oils are used in tractors, harvesters, and forage equipment to reduce maintenance, enhance wear and corrosion protection, improve engine reliability, and improve fuel efficiency.

- According to Pacific Fuel Solutions, Agricultural lubricants or oils can be used for plenty of different functions, but one of the most noticeable examples is engine oil. Farm machinery such as tractors and harvesters need to be effectively lubricated to maintain the parts in good working order while still being appropriate for use in the circumstances.

- Total, Royal Dutch Shell Plc, Chevron Lubricants, CONDAT Group, and Schaeffer Manufacturing Co. are some of the significant lubricant manufacturers offering various types of engine oils for agricultural equipment.

- Several leading vendors are investing in research and development to develop innovative equipment and maintain a strong tractor market foothold. Companies like Case IH and New Holland launched new autonomous tractors.

- Due to growing automation in farming practices combined with the increasing production of food and farmland expansions, the demand for new and used farm machinery or agriculture equipment is projected to increase year-on-year. This will substantially increase demand for engine oil in the agricultural lubricants market worldwide as it ensures longer life of the equipment because when the engine starts getting old, its engine oil consumption starts to increase.

- For instance, the International Grains Council projected that about 2.294 billion metric tons of grains were to be produced globally in the 2023-24 season, a 1.77% increase from a forecast of 2.254 billion tons for the 2022-23 season.

- According to Lemken CEO Anthony van der Ley, a 6-7% drop in international farm machinery sales will likely occur in 2024 due to the rise in inflation witnessed across all international markets over the past 12 months and the accompanying impact this has had on interest rates.

- Furthermore, according to Progressive Dairy, the used farm equipment market of Canada was expected to stay robust for most of 2023 and into 2024 because of the rising interest rates. Such trends of using aging engines propel the demand for engine oil.

- During the forecast period, all the factors mentioned above are projected to influence the dominance of engine oil in the agricultural lubricants market.

Asia-Pacific to witness Fastest Growth

- China is the largest lubricant consumer globally. China accounts for around 7% of the overall agricultural acreage globally, thus feeding 22% of the world population.

- The country is the largest producer of various crops, including rice, cotton, potatoes, and others. Owing to the large-scale agricultural activities in the country, a high demand for various types of agricultural machinery is present and will likely grow in the future. This will subsequently increase the demand for agricultural lubricants.

- For instance, the increasing area under cultivation enhanced the demand for agricultural machinery in China. For instance, corn acreage in China rose to 5% in 2022, and the output rose to 4.6%.

- India is the second-largest lubricant consumer in the region and the third-largest globally, after the United States and China.

- India is one of the economies that are largely dependent on agriculture. Agriculture is still the primary source of livelihood for more than 55% of the country's population.

- In 2022, tractor exports from India increased by 6%, reaching 131,850 units. It is the highest annual export in Indian history, up from 124,901 units in 2021. India accounts for nearly 2.1% of global tractor sales.

- Moreover, the Japanese government plans to increase agricultural production to 54 million tons by 2025, from 50 million tons in 2013. Additionally, the government plans to increase the producer income from USD 29 billion to USD 35 billion, an increase of approximately 21% over the same period, by enhancing agricultural output quantity and revenue and cutting costs.

- Such trends in the agriculture industry of the Asia-Pacific are expected to drive agricultural lubricants market growth at the fastest rate globally during the forecast period.

Agricultural Lubricants Industry Overview

The agricultural lubricants market is partially consolidated in nature. Some of the major players (not in any particular order) in the market studied include Shell plc, Fuchs, Exxon Mobil Corporation, TotalEnergies SE, and BP p.l.c., among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Provision of Subsidy for Farm Machinery by the Indian and Chinese Governments

- 4.1.2 Increasing Farm Mechanization Rates in Developing Countries

- 4.1.3 Increasing Cost of Farm Labor

- 4.2 Restraints

- 4.2.1 High Cost of Synthetic and Bio-based Lubricants

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 Product Type

- 5.1.1 Engine Oil

- 5.1.2 Transmission and Hydraulic Fluid

- 5.1.3 Grease

- 5.1.4 Other Product Types

- 5.2 Geography

- 5.2.1 Asia-Pacific

- 5.2.1.1 China

- 5.2.1.2 India

- 5.2.1.3 Japan

- 5.2.1.4 South Korea

- 5.2.1.5 Rest of Asia-Pacific

- 5.2.2 North America

- 5.2.2.1 United States

- 5.2.2.2 Canada

- 5.2.2.3 Mexico

- 5.2.3 Europe

- 5.2.3.1 Germany

- 5.2.3.2 United Kingdom

- 5.2.3.3 France

- 5.2.3.4 Italy

- 5.2.3.5 Spain

- 5.2.3.6 Rest of Europe

- 5.2.4 Rest of the World

- 5.2.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BP p.l.c.

- 6.4.2 Chevron Corporation

- 6.4.3 CLASS KGaA mbH

- 6.4.4 CONDAT

- 6.4.5 Cougar Lubricants International Ltd.

- 6.4.6 Exol Lubricants Limited

- 6.4.7 Exxon Mobil Corporation

- 6.4.8 FRONTIER PERFORMANCE LUBRICANTS, INC.

- 6.4.9 Fuchs

- 6.4.10 Gulf Oil International Ltd.

- 6.4.11 Hf Sinclair Corporation

- 6.4.12 Lubrication Engineers

- 6.4.13 Morris Lubricants

- 6.4.14 Pennine Lubricants

- 6.4.15 Phillips 66 Company

- 6.4.16 Repsol

- 6.4.17 Rymax Lubricants

- 6.4.18 Schaeffer Manufacturing Co.

- 6.4.19 Shell plc

- 6.4.20 TotalEnergies SE

- 6.4.21 Unil

- 6.4.22 Witham Group

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Growing Prominence of Biodegradable Lubricants

- 7.2 Other Opportunities