|

시장보고서

상품코드

1689849

채혈관 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Blood Collection Tubes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

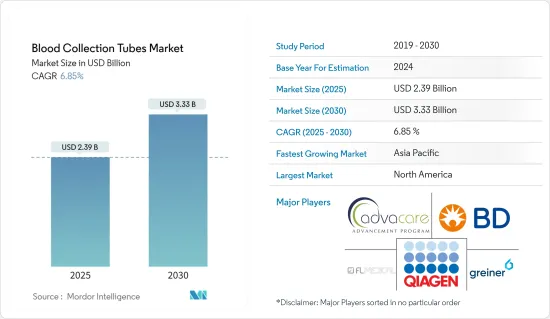

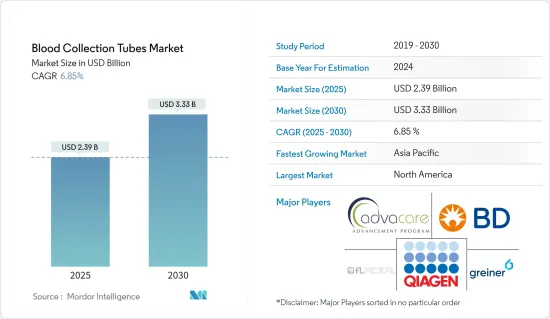

세계의 채혈관 시장 규모는 2025년 23억 9,000만 달러로 예측되고, 2030년 33억 3,000만 달러에 이를 것으로 예측되며, 예측 기간 중(2025-2030년) CAGR 6.85%로 예상됩니다.

팬데믹은 시장에 영향을 미쳤습니다. 2021년 2월 WHO는 준비와 신속한 대응의 중요성을 강조하고, 유행시 혈액 공급의 안전성과 만족도에 대한 잠재적인 위험을 줄이기 위해 혈액 서비스가 취해야 할 주요 행동과 대책을 개설했습니다. 게다가 2022년 4월에 National Library of Medicine에 게재된 연구에 따르면, 혈액 센터는 바이러스가 혈액의 안전성을 직접 위협하지 않기 때문에 자국의 혈액 공급량을 늘리기 위한 노력과 정책을 시작하는 데 더욱 집중해야 합니다. 마찬가지로 채혈 가정용 튜브 등의 제품 출시를 늘리는 등의 노력도 예측 기간 동안 시장 성장을 높일 것으로 예상됩니다. 예를 들어, 2021년 12월, Ethos Laboratories사는 COVID-19 중화 항체 검사용 지자기 자기 채취 키트 Tru-Immune을 출시했습니다. 이러한 제품의 출시는 가정에서의 안전한 채혈 절차를 제공하기 때문에 이러한 제품의 채용이 증가할 것으로 예상되지만, 현재 유행은 침전되고 있기 때문에 시장의 견인력은 약해지고 있으며, 본 조사의 예측 기간 동안 안정된 성장이 예상됩니다.

시장 성장의 주요 요인은 노인 인구 증가와 만성 질환의 이환율 증가입니다. 또한 다양한 질병과 사고로 인한 수술 건수 증가가 시장을 밀어 올리고 있습니다. 염증성 질환과 감염성 질환의 부담이 증가함에 따라 이러한 질병에 대한 인식도 높아지고 채혈에 대한 수요도 증가하고 있기 때문에 이러한 질병의 부담 증가는 시장에 큰 영향을 미칠 것으로 예상되며, 이 부문의 성장에 큰 영향을 줄 것으로 기대됩니다. 예를 들어, 세계보건기구(WHO)의 2022년 10월 갱신에 따르면, 2021년 결핵 이환 환자 수는 전 세계적으로 약 1,060만 명으로 추정되며, 그 중 120만 명은 소아입니다. 마찬가지로 수술 건수 증가가 시장 성장을 높일 것으로 예상됩니다. 2022년 8월에 갱신된 경제협력개발기구에 따르면 2021년 포르투갈, 덴마크, 아일랜드, 노르웨이 등 유럽 국가에서 실시된 수술건수(단위: 천건)는 각각 94.87건, 49.33건, 32.84건, 21.5건이었습니다. 신흥 유럽 국가에서 이러한 방대한 수술 건수는 채혈관 수요 증가로 이어져 시장 개척의 원동력이 됩니다. 따라서 위의 요인은 시장 성장을 증가시킬 것으로 예상됩니다.

또한, 시장 기업 간의 협정도 시장 성장의 요인 중 하나입니다. 예를 들어, 2021년 11월, Q-Sera Pty Ltd는 Terumo Corporation와 Q-Sera의 혈청 신속 채혈관 기술 RAPClot을 일본에서 제조 및 판매하는 독점 계약을 체결했습니다. 이러한 계약은 시장에서 제품의 가용성을 높이고 예측 기간 동안 시장 성장을 기대합니다.

그러나 비위생적인 수혈로 인한 감염의 위험은 시장 성장의 어려움이 되었습니다.

채혈관 시장 동향

예측 기간 동안 EDTA 튜브 부문이 큰 시장 점유율을 차지할 전망

EDTA 튜브는 임상 혈액학 및 각종 혈구 검사 장비에 널리 사용됩니다. EDTA는 혈액 중의 칼슘과 결합하여 혈액을 응고시키지 않도록 함으로써 기능합니다. 이 튜브는 절제 치료 및 수혈과 같은 대부분의 혈액 학적 치료에 사용됩니다. 주로 전혈구 계산에 사용됩니다. 2021년 10월에 National Library of Medicine에 게재된 조사 논문에 따르면, 혈소판 EV의 농도 안정화와 관련하여, EDTA는 구연산염보다 항응고제로서 더 낫습니다. 게다가, 1회의 동결 융해 사이클에서의 혈소판 EV의 안정성은 어느 항응고제에서도 동등하기 때문에 EV 연구를 위한 바이오리포지토리를 확립하기 위한 항응고제로서 EDTA가 추천되고 있습니다.

이 부문의 주요 점유율은 당뇨병과 같은 광범위한 질병과 함께 노화 인구가 증가하고 있기 때문입니다. 당뇨병의 유병률은 최근 증가하고 있으며, 유병률은 앞으로 더욱 증가할 것으로 예측되고 있습니다. 예를 들어, 국제 당뇨병 연합에 의한 2021년 12월의 보고에 따르면, 2021년에는 약 5억 3,700만명의 성인(20-79세)이 당뇨병을 앓고 있습니다. 당뇨병 환자의 총 수는 2030년에는 6억 4,300만 명, 2045년에는 7억 8,300만 명으로 증가할 것으로 예측됩니다. 다양한 만성 질환을 앓고 있는 환자 수 증가는 혈액 검사 수요를 증가시키고 연구 부문의 성장에 기여할 것으로 보입니다.

마찬가지로 주요 시장 기업의 출시도 시장 성장의 또 다른 요소입니다. 예를 들어, 2022년 5월, Tethis SpA는 액체 생검 분석을 위한 최초의 범용 혈액 샘플 준비 장비 See.d를 발표했습니다. 이 혁신적인 기술은 채혈 당시 혈액 샘플 준비를 완전히 자동화하고 표준화합니다. 세포 분획은 CTC를 포함한 희소 세포 검출을 위해 독특한 나노 코팅 SBS 슬라이드에서 부드럽게 안정화되는 반면, 혈장은 무세포 성분 분석에 사용할 수 있습니다. See.d는 EDTA 튜브에 채취한 신선한 혈액을 채취 직후(4-6시간 이내) 처리하여 샘플의 무결성을 최대한 유지합니다. 이러한 개발은 EDTA 채혈관의 사용과 수요를 촉진하여 시장 개척에 기여할 것으로 기대됩니다.

예측기간 중 북미가 큰 시장 점유율을 차지할 전망

북미는 예측기간을 통해 큰 성장이 예상됩니다. 시장 성장의 요인으로는 주요 기업의 존재, 사고와 높은 만성 질환의 유병률, 헬스 케어 인프라의 확립 등을 들 수 있습니다. 미국은 지원 헬스케어 정책, 환자 수가 많고 헬스케어 시장 개척으로 이 지역에서 가장 큰 점유율을 차지하고 있습니다.

또한 미국에서는 당뇨병, 갑상선, 혈액 검사를 필요로 하는 기타 질환 등 만성 질환 부담이 증가하고 있는 것도 조사 대상 시장을 밀어올릴 것으로 보입니다. 당뇨병 연구개발을 위한 캐나다 정부의 투자 증가에 따른 당뇨병 발생률 증가는 이 나라에서 조사 시장 성장을 가속하고 있습니다. 예를 들어, 2021년 8월에 발표된 캐나다 정부의 보도 자료에 따르면 당뇨병은 캐나다인에게 영향을 미치는 주요 만성 질환 중 하나이며, 인구의 8.8%에 해당하는 300만명 이상의 캐나다인이 당뇨병으로 진단되고 2021년 8월 현재, 캐나다 성인의 6.1% 당뇨병 환자 증가 문제를 돕기 위해 캐나다의 2021년 예산은 당뇨병 연구, 감시, 예방, 당뇨병의 국가적 틀 개발에 대한 새로운 투자를 제안했습니다. 그 일환으로 캐나다 보건연구소(CIHR)를 통해 캐나다 정부의 홍보 담당자는 당뇨병을 박멸하기 위한 JDRF와 CIHR의 파트너십에 재투자할 예정이며, 연구효과 총액 3,000만 달러를 위해 1,500만 달러를 상한에 투자했습니다. 따라서 당뇨병의 이환율 증가와 정부 투자는 캐나다에서 연구 시장의 성장을 가속할 것으로 예상됩니다.

그러나 이 나라의 주요 시장 기업이 획득한 다양한 전략이 시장 성장을 예상했습니다. 예를 들어, 2022년 7월 Rhinostics사는 소량 채혈에 특화된 특허 출원 중인 Veristic 채혈 장치를 출시하여 자동 샘플 채취 기술을 도입했습니다.

따라서 위의 모든 요인을 고려하면 시장은 예측 기간 동안 건전한 성장을 보일 것으로 예상됩니다.

채혈관 산업 개요

채혈관 시장은 적당한 경쟁을 가지고 있으며 여러 대형 기업으로 구성되어 있습니다. 현재 시장을 독점하고 있는 기업으로는 Becton, Dickinson and Company, Greiner AG, Qiagen NV, FL MEDICAL SRL, AdvaCare Pharma, Sarstedt AG & Co., Narang Medical Limited 등이 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 시장 개요

- 시장 성장 촉진요인

- 수술건수와 사고 증가

- 질병의 만연에 수반하는 고령화 인구 증가

- 세계의 채혈 및 헌혈 프로그램 증가

- 시장 성장 억제요인

- 비위생적인 수혈에 의한 감염증의 위험

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 세분화

- 제품 유형별

- 혈청 분리 튜브

- EDTA 튜브

- 혈장 분리 튜브

- 신속 혈청 튜브

- 기타 제품 유형

- 지역

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 기업 프로파일

- Becton, Dickinson and Company

- Greiner AG

- Qiagen NV

- FL Medical SRL

- AdvaCare Pharma

- Narang Medical Limited

- Sarstedt AG & Co KG

- Hindustan Syringes & Medical Devices Ltd

- Terumo Corporation

- DWK Life Sciences

- RAM Scientific

제7장 시장 기회와 앞으로의 동향

JHS 25.04.07The Blood Collection Tubes Market size is estimated at USD 2.39 billion in 2025, and is expected to reach USD 3.33 billion by 2030, at a CAGR of 6.85% during the forecast period (2025-2030).

The pandemic had an effect on the market. In February 2021, the WHO emphasized the importance of being prepared and responding quickly and outlined key actions and measures that the blood services should take to mitigate the potential risk to the safety and sufficiency of blood supplies during the pandemic. Additionally, as per an April 2022 study published in the National Library of Medicine blood centers should focus more on launching initiatives and policies that would increase their countries' blood supply as the virus has no direct threat to blood safety. Similarly, initiatives such as increasing product launches such as blood collection home tubes are expected to increase market growth during the forecast period. For instance, in December 2021, Ethos Laboratories launched Tru-Immune, a finger prick, self-collection kit for its COVID-19 neutralizing antibody test. Such product launches provide a safe procedure of blood collection at home which is expected to increase the adoption of such products, however, currently as the pandemic has subsided the market has lost some traction, thus the market is expected to have a stable growth during the forecast period of the study.

The major factor attributing to the growth of the market is the increase in the geriatric population and the increasing incidence of chronic diseases. Furthermore, the rising number of surgeries due to various conditions and accidents boosts the market. The rising burden of these diseases is expected to have a significant impact on the market as with the rising burden of inflammatory and infectious diseases, the awareness about these diseases is also increasing in demand for blood collection which is expected to have a significant and positive impact on the segment's growth. For instance, as per the October 2022 update of the World Health Organization, the incidence of tuberculosis (TB) was estimated to be around 10.6 million people in 2021, globally, of which 1.2 million were children. Similarly, the increasing number of surgeries is expected to increase the market growth. According to the Organization for Economic Co-operation and Development updated in August 2022, the number of surgeries (in thousand) performed in some European countries such as Portugal, Denmark, Ireland, and Norway in 2021 include 94.87, 49.33, 32.84, 21.5., respectively. Such a huge number of surgeries in developed European countries will lead to increased demand of blood collection tubes, driving market growth. Thus, the abovementioned factors are expected to increase the market growth.

Furthermore, agreements between market players are another factor in market growth. For instance, in November 2021, Q-Sera Pty Ltd entered an exclusive agreement with Terumo Corporation to manufacture and market Q-Sera's RAPClot rapid serum blood collection tube technology in Japan. Such agreements are expected to increase the availability of products in the market which is expected to increase market growth over the forecast period.

However, the risk of acquiring infections due to unhygienic blood transfusion is a drawback of market growth.

Blood Collection Tubes Market Trends

EDTA Tubes Segment is Expected to Hold a Significant Market Share Over the Forecast Period

EDTA Tube is widely used in clinical hematology and various kinds of blood cell test instruments. EDTA functions by binding calcium in the blood and keeping the blood from clotting. These tubes are used for most hematology procedures like ablation therapy, blood transfusions, etc. It is majorly used for a complete blood count. A research article published in the National Library of Medicine in October 2021, shows that EDTA is superior to citrate as an anticoagulant concerning stabilization of the concentration of platelet EVs. Moreover, because the stability of platelet EVs is comparable for both anticoagulants during a single freeze-thaw cycle, EDTA is recommended as an anticoagulant to establish biorepositories for EV research.

The major share of the segment can be attributed to the increase in the aging population along with widespread diseases, such as diabetes. The prevalence of diabetes has increased in recent years, and it is predicted that prevalence will increase further in the future. For instance, as per the December 2021 report by the International Diabetes Federation, approximately 537 million adults (20-79 years) lived with diabetes in 2021. The total number of people living with diabetes is projected to rise to 643 million by 2030 and 783 million by 2045. The rising number of patients suffering from various chronic disorders will increase the demand for blood testing, which will help grow the studied segment.

Similarly, launches by key market players are another factor in market growth. For instance, in May 2022, Tethis SpA released See.d, the first universal blood sample preparator for liquid biopsy analysis. This innovative technology performs a completely automated and standardized preparation of a blood sample at the point of blood collection. Cellular fraction is gently stabilized on proprietary, nanocoated SBS slides for rare cell detection, including CTCs, while plasma is made available for the analysis of cell-free content. See.d processes fresh blood collected in EDTA tubes shortly after collection (within 4 to 6 hours), favoring maximum sample integrity. Such developments are expected to fuel the usage and demand for EDTA blood collection tubes, thereby contributing to market growth.

North America is Expected to Have a Significant Market Share Over the Forecast Period

North America is expected to witness significant growth throughout the forecast period. The market growth is due to the factors such as the presence of key players, the high prevalence of accidents and chronic diseases in the region, and established healthcare infrastructure are some of the key factors accountable for its large share in the market. The United States has the maximum share in this region due to supportive healthcare policies, the high number of patients, and a developed healthcare market.

Furthermore, the rising burden of chronic diseases in the United States, such as diabetes, thyroid, and other diseases requiring blood tests, will boost the studied market. The increasing incidence of diabetes in compliance with the rising investment from the Canadian government for diabetes research and development is propelling the growth of the studied market in the country. For instance, as per a press release by the government of Canada published in August 2021, diabetes is one of the major chronic diseases affecting Canadians where over 3 million Canadians, or 8.8% of the population were diagnosed with diabetes and 6.1% of Canadian adults were at high risk of developing diabetes as of August 2021. To aid the issue of increasing cases of diabetes, Canada's Budget 2021 proposed new investments in diabetes research, surveillance, prevention, and the development of a national framework for diabetes. As part of this, the spokesperson of the government of Canada through the Canadian Institutes of Health Research (CIHR) is planning to recommit to the JDRF-CIHR partnership to Defeat Diabetes and invested up to USD 15 million for a total research impact of USD 30 million. Thus, the increasing incidence of diabetes and government investments are anticipated to drive the studied market growth in Canada.

However, various strategies acquired by the key market players in the country anticipated market growth. For instance, in July 2022, Rhinostics introduced automated sample collection technologies with the launch of the patent-pending VERIstic collection device focused on small volume blood collection.

Thus, considering all the factors mentioned above, the market is expected to witness healthy growth over the forecast period.

Blood Collection Tubes Industry Overview

The blood collection tube market is moderately competitive and consists of several major players. Some companies currently dominating the market are Becton, Dickinson and Company, Greiner AG, Qiagen NV, FL MEDICAL SRL, AdvaCare Pharma, Sarstedt AG & Co., Narang Medical Limited, etc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in the Number of Surgical Procedures and Accidents

- 4.2.2 Increase in Aging Population Coupled with Widespread of Diseases

- 4.2.3 Increasing Blood Collection and Blood Donation Programs Globally

- 4.3 Market Restraints

- 4.3.1 Risks of Acquiring Infections Due to Unhygienic Blood Transfusion

- 4.4 Porter's Five Force Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 By Product Type

- 5.1.1 Serum Separating Tubes

- 5.1.2 EDTA Tubes

- 5.1.3 Plasma Separation Tubes

- 5.1.4 Rapid Serum Tubes

- 5.1.5 Other Product Types

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Becton, Dickinson and Company

- 6.1.2 Greiner AG

- 6.1.3 Qiagen NV

- 6.1.4 F.L. Medical SRL

- 6.1.5 AdvaCare Pharma

- 6.1.6 Narang Medical Limited

- 6.1.7 Sarstedt AG & Co KG

- 6.1.8 Hindustan Syringes & Medical Devices Ltd

- 6.1.9 Terumo Corporation

- 6.1.10 DWK Life Sciences

- 6.1.11 RAM Scientific