|

시장보고서

상품코드

1689908

브레이크 오일 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Brake Fluids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

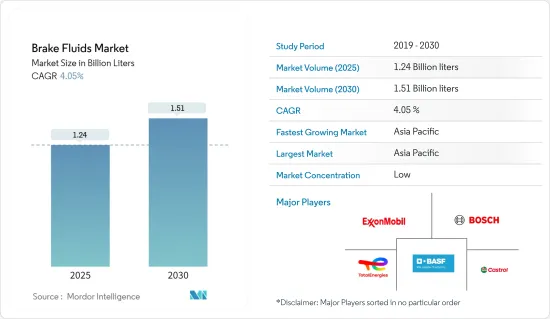

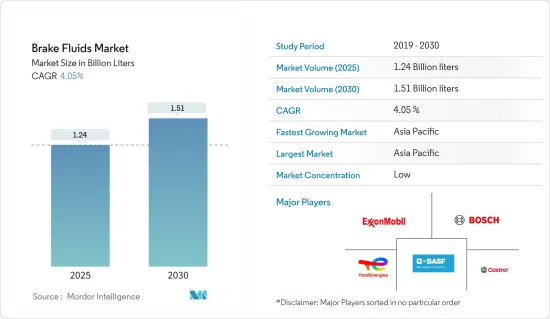

브레이크 오일 시장 규모는 2025년에 12억 4,000만 리터로 추정되고, 2030년에는 15억 1,000만 리터에 이를 것으로 예측되며, 예측기간(2025-2030년)의 CAGR은 4.05%를 나타낼 전망입니다.

브레이크 오일 시장은 코로나19 팬데믹으로 인해 상당한 어려움에 직면했습니다.

주요 하이라이트

- 단기적으로는 전기 및 하이브리드 차량의 채택이 증가하고 차량 인구가 급증하는 것이 연구 대상 시장의 수요를 견인하는 주요 요인입니다.

- 그러나 브레이크 오일의 사용과 관련된 엄격한 안전 기준이 시장의 성장을 저해할 것으로 예상됩니다.

- 그러나 자동차 시스템의 기술적 발전은 시장에 새로운 기회를 가져올 것으로 기대되고 있습니다.

- 아시아태평양 지역이 시장을 지배할 것으로 예상되며, 대부분의 수요는 중국과 인도에서 발생할 것으로 예상됩니다.

브레이크 오일 시장 동향

시장을 독점하는 소형 상용차

- 밴, 트럭, 버스 등의 소형 상용차(LCV)에서는 브레이크 오일가 안전하고 안정적인 제동력을 보장합니다.

- 브레이크 오일에 대한 수요가 높아지는 것은 신흥 시장에서 경량 고성능 자동차에 대한 수요 증가, 새로운 자동차 허브의 구축, 가처분 소득의 증가 등이 브레이크 액 수요 증가의 원인입니다.

- 2023년 세계 신차 판매 대수는 2022년 대비 11.9% 증가한 9,270만대 이상으로 견조한 성장세를 보였습니다고 국제 자동차 제조자 기구(OICA)가 보고하고 있습니다.

- 또한 OICA의 데이터에 따르면 2023년 소형 상용차 생산 대수는 2,144만대로 전년대비 9% 증가하여 시장 성장을 더욱 뒷받침했습니다.

- 아시아-오세아니아 지역의 국가들은 전략적으로 글로벌 시장에서 떠오르는 자동차 허브로 자리매김하고 있습니다. 아시아-오세아니아 지역은 다른 지역에 비해 가장 많은 수의 차량을 등록했습니다.

- 그러나 인도에서는 상용차(CV) 판매 대수는 24년도에 2-5%의 소폭 성장을 보인 뒤 2024-2025년에는 떨어질 것으로 예측되고 있습니다.

- OICA에 따르면 2023년 북미의 자동차 생산 대수는 1,914만대로 2022년 1,775만대에서 7.8% 증가했습니다.

- 연방 자동차 교통국의 데이터에 따르면 독일의 자동차 대수는 2022년의 5,305만대에서 2023년에는 5,350만대에 이르렀습니다.

- OICA의 데이터에 따르면, 2023년 독일의 상용차 등록 대수는 35만 9,000대를 넘어 전년의 31만 2,000대에서 증가했습니다.

- OICA의 데이터에 따르면, 브라질의 소형 상용차 생산 대수는 2023년에 42만 2,000대에 이르렀고, 전년 대비 20% 증가했습니다.

- 이러한 움직임을 근거로 하면, 브레이크 오일에 대한 수요는 향후 몇 년 동안 성장할 것으로 예상됩니다.

아시아태평양이 시장을 독점

- 아시아태평양 지역은 중국, 인도, 일본, 한국과 같은 주요 자동차 생산업체가 존재하기 때문에 가장 큰 브레이크 오일 시장을 차지할 것으로 예상됩니다.

- 중국의 자동차 산업은 강력한 차량 증가와 기술 발전을 반영하여 윤활유의 주요 소비국으로 부상하고 있습니다.

- OICA의 데이터에 따르면 2023년 중국은 약 230만 대를 생산하며 소형 상용차 생산량을 주도했고, 태국이 126만 대로 그 뒤를 이었습니다.

- 인도 자동차 제조업체 협회(SIAM)의 데이터에 따르면 2024년 1월부터 3월까지 인도에서 승용차, 상용차, 삼륜차, 이륜차, 사륜차의 생산량은 739만 대에 달했습니다.

- 한국은 현대, 르노, 삼성, 기아 등 유명 브랜드를 보유한 성숙한 자동차 산업을 자랑합니다.

- OICA 데이터에 따르면 2023년 국내 자동차 판매량은 2022년보다 3% 이상 증가한 174만 대에 달했습니다. 승용차 판매량은 4.8% 증가한 140만 대를 기록했지만, 상용차는 전년 대비 1.1% 감소한 26만 대를 판매하며 소폭 하락세를 보였습니다.

- 게다가 OICA에 의하면, 2023년의 일본의 자동차 판매 대수는 470만대에 이르렀고, 2022년부터 13% 증가했습니다.

- 이러한 움직임을 감안하면, 아시아태평양 지역의 브레이크 오일 수요는 증가할 것으로 예상됩니다.

브레이크 오일 산업 개요

세계의 브레이크 오일 시장은 부분적으로 단편화되어 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 역학

- 성장 촉진요인

- 전기차와 하이브리드차의 채택 확대

- 브레이크 오일 수요를 주도하는 차량 인구 급증

- 기타

- 억제요인

- 브레이크 오일의 사용과 관련된 엄격한 안전 기준

- 기타

- 산업 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 세분화

- 후루드 유형별

- 석유

- 비석유

- 제품 유형별

- DOT 3

- DOT 4

- DOT 5

- DOT 5.1

- 용도별

- 소형 상용차

- 승용차

- 기타

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 말레이시아

- 태국

- 인도네시아

- 베트남

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 튀르키예

- 러시아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 카타르

- 아랍에미리트(UAE)

- 나이지리아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- M&A, 합작사업, 제휴, 협정

- 시장 점유율 분석(%) 및 랭킹 분석

- 주요 기업의 전략

- 기업 프로파일

- BASF SE

- CASTROL LIMITED

- Chevron Corporation

- China Petrochemical Corporation(SINOPEC)

- Dow

- Exxon Mobil Corporation

- FUCHS

- Hi-Tec Oils Pty Ltd

- Morris Lubricants

- Motul

- Repsol

- Robert Bosch LLC

- TotalEnergies SE

- Valvoline

제7장 시장 기회와 앞으로의 동향

- 자동차 시스템의 기술 발전

- 기타 기회

The Brake Fluids Market size is estimated at 1.24 billion liters in 2025, and is expected to reach 1.51 billion liters by 2030, at a CAGR of 4.05% during the forecast period (2025-2030).

The brake fluids market faced significant challenges due to the COVID-19 pandemic. Global lockdowns and stringent government regulations led to widespread shutdowns of production hubs. However, the market rebounded in 2021 and is projected to grow substantially in the years ahead.

Key Highlights

- Over the short term, increasing adoption of electric and hybrid vehicles and surging vehicle population are the major factors driving the demand for the market studied.

- However, stringent safety standards associated with using brake fluids are expected to hinder the market's growth.

- Nevertheless, technological advancements in the automobile systems are expected to create new opportunities for the market studied.

- Asia-Pacific is expected to dominate the market, with most of demand coming from China and India.

Brake Fluids Market Trends

Light Commercial Vehicles to Dominate the Market

- In Light Commercial Vehicles (LCVs) like vans, trucks, and buses, brake fluid ensures safe and reliable stopping power. These vehicles, often handling heavy payloads and facing diverse driving conditions, depend on a robust braking system. The significance of brake fluid in this system is paramount.

- Rising demand for brake fluids includes a growing appetite for lightweight, high-performance cars in emerging markets, the establishment of new automotive hubs, and an uptick in disposable income.

- In 2023, global new vehicle sales saw a robust growth of 11.9% over 2022, totaling over 92.7 million units, as reported by the Organisation Internationale des Constructeurs d'Automobiles (OICA). Specifically, new commercial vehicle registrations worldwide rose to 27.5 million units in 2023, marking a notable 13.3% increase from the 24.2 million units recorded in 2022.

- Additionally, light commercial vehicle production climbed to 21.44 million units in 2023, marking a 9% rise from the previous year, according to OICA data, further fueling the market's growth.

- The countries in the Asia-Oceania region are strategically positioning themselves as the emerging automotive hub in the global market. The Asia-Oceania region registered the largest number of vehicles compared to other regions. Registration in this region is dominated mainly by China, Japan, South Korea, and India. In 2023, the region witnessed a 10.9% increase in new commercial vehicle sales compared to 2022, with 7.96 million units registered in 2023, compared to 7.17 million units in 2022.

- However, in India, commercial vehicle (CV) sales are projected to dip in the financial year 2024-25 (FY25) after a modest 2-5% growth in FY24. The data from ICRA (Investment Information and Credit Rating Agency of India Limited) forecasts a 4-7% decline in FY25.

- North America's motor vehicle production in 2023 hit 19.14 million units, a 7.8% increase from 2022's 17.75 million units, according to OICA. Light commercial vehicles constituted a significant portion, rising from 12.24 million units in 2022 to 13.30 million units in 2023.

- Data from the Federal Motor Transport Authority indicates that Germany's motor vehicle count reached 53.50 million in 2023, up from 53.05 million in 2022. Furthermore, the Kraftfahrt-Bundesamt highlighted that car registrations in Germany saw a slight uptick, with 48.76 million in 2023 compared to 48.54 million the previous year.

- According to OICA, Germany registered over 359 thousand commercial vehicles in 2023, up from 312 thousand units the previous year.

- OICA data reveals that Brazil's light commercial vehicle production hit 422 thousand units in 2023, marking a 20% increase from the prior year. South Africa also saw a boost, with production reaching 263 thousand units in 2023, a 22% rise from the previous year, bolstering the market's growth.

- Given these dynamics, the demand for brake fluids is poised for growth in the coming years.

Asia-Pacific to Dominate the Market

- The Asia-Pacific region is expected to account for the largest brake fluid market due to the presence of leading automobile producers such as China, India, Japan, and South Korea. These countries are working hard to strengthen the manufacturing base for vehicles and develop efficient supply chains for greater profitability.

- China's automotive industry stands out as the leading consumer of lubricants, reflecting its robust vehicle fleet growth and technological advancements. In 2023, both automobile sales and production in China reached a milestone, hitting 30 million units each, marking a double-digit increase from the previous year, as per the data from the China Association of Automobile Manufacturers (CAAM).

- As per the data from OICA, China led in the production of light commercial vehicles in 2023, churning out approximately 2.30 million vehicles, with Thailand trailing at 1.26 million.

- In India, data from the Society of Indian Automobile Manufacturers (SIAM) indicates that from January to March 2024, the production of passenger vehicles, commercial vehicles, three-wheelers, two-wheelers, and quadricycle reached 7.39 million units. Specifically, sales for passenger and commercial vehicles were 1.14 million units and 268 thousand units, respectively.

- South Korea boasts a mature automotive industry with notable brands like Hyundai, Renault, Samsung, and Kia. Projections from the Automobile Manufacturers Association and The Korea Automobile Research Institute anticipate a 1.0% rise in domestic automobile production for 2024, reaching 4.36 million units. This growth is expected to drive demand in the studied market.

- OICA data shows that in 2023, vehicle sales in the country reached 1.74 million units, up over 3% from 2022. Passenger vehicle sales climbed 4.8% to 1.4 million units, but commercial vehicles saw a slight dip, selling 0.26 million units, down 1.1% from the previous year.

- Further, OICA reports that Japan's vehicle sales in 2023 touched 4.7 million units, marking a 13% uptick from 2022. Breaking it down, passenger vehicle sales rose over 15% to 3.9 million units, while commercial vehicles saw a modest 4% increase, totaling 0.78 million units.

- Given these dynamics, the demand for brake fluids in the Asia-Pacific is set to rise.

Brake Fluids Industry Overview

The global brake fluids market is partially fragmented in nature. The major players (not in any particular order) include TotalEnergies SE, Robert Bosch LLC, CASTROL LIMITED, Exxon Mobil Corporation, and BASF SE.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Drivers

- 4.1.1 Increasing Adoption of Electric and Hybrid Vehicles

- 4.1.2 Surging Vehicle Population to Drive the Demand for Brake Fluids

- 4.1.3 Other Drivers

- 4.2 Restraints

- 4.2.1 Stringent Safety Standard Associated With the Use of Braking Fluids

- 4.2.2 Other Restraints

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 MARKET SEGMENTATION (Market Size in Volume)

- 5.1 By Fluid Type

- 5.1.1 Petroleum

- 5.1.2 Non-petroleum

- 5.2 By Product Type

- 5.2.1 DOT 3

- 5.2.2 DOT 4

- 5.2.3 DOT 5

- 5.2.4 DOT 5.1

- 5.3 By Application

- 5.3.1 Light Commercial Vehicles

- 5.3.2 Passenger Cars

- 5.3.3 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Malaysia

- 5.4.1.6 Thailand

- 5.4.1.7 Indonesia

- 5.4.1.8 Vietnam

- 5.4.1.9 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Turkey

- 5.4.3.8 Russia

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 Qatar

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 South Africa

- 5.4.5.7 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Mergers and Acquisitions, Joint Ventures, Collaborations, and Agreements

- 6.2 Market Share Analysis (%)**/Ranking Analysis

- 6.3 Strategies Adopted by Leading Players

- 6.4 Company Profiles

- 6.4.1 BASF SE

- 6.4.2 CASTROL LIMITED

- 6.4.3 Chevron Corporation

- 6.4.4 China Petrochemical Corporation (SINOPEC)

- 6.4.5 Dow

- 6.4.6 Exxon Mobil Corporation

- 6.4.7 FUCHS

- 6.4.8 Hi-Tec Oils Pty Ltd

- 6.4.9 Morris Lubricants

- 6.4.10 Motul

- 6.4.11 Repsol

- 6.4.12 Robert Bosch LLC

- 6.4.13 TotalEnergies SE

- 6.4.14 Valvoline

7 MARKET OPPORTUNITIES AND FUTURE TRENDS

- 7.1 Technological Advancements in the Automotive Systems

- 7.2 Other Opportunities