|

시장보고서

상품코드

1692112

로직 IC(집적 회로) 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Logic IC (Integrated Circuit) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

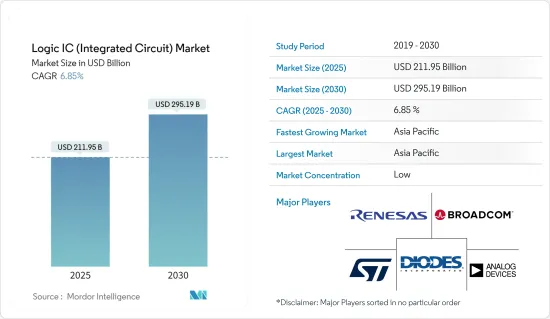

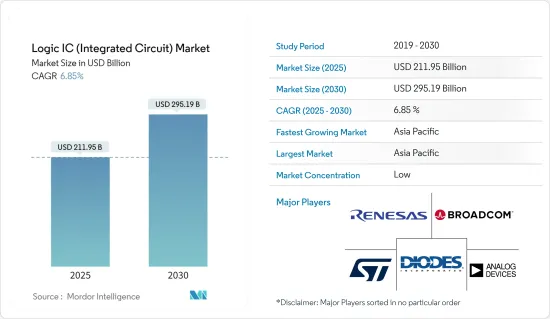

로직 IC 시장 규모는 2025년에 2,119억 5,000만 달러로 추정되고, 예측 기간인 2025-2030년 CAGR 6.85%로 성장할 전망이며, 2030년에는 2,951억 9,000만 달러에 달할 것으로 예측됩니다.

출하량에서는 2025년 679억 7,000만 개에서 2030년에는 834억 6,000만 개로 성장할 것으로 예측되며, 예측 기간인 2025-2030년 CAGR 4.19%로 성장할 전망입니다.

반도체 제조 공정의 개발이 진행되고 있으며, 보다 복잡하고 효율적인 로직 IC가 개발되고 있습니다. 트랜지스터 사이즈의 소형화, 성능의 향상, 소비 전력의 저감에 의해 폭넓은 용도에 대응하는 고성능 로직 IC의 개발이 가능하게 되었습니다. 로직 IC는 매우 유연하며 다양한 용도에 사용할 수 있습니다. AND, OR, NOT, XOR 등 여러 논리 기능을 수행하도록 구성할 수 있습니다. 이러한 유연성을 통해 가전, 자동차, 통신, 산업 자동화 등 다양한 산업 요구사항을 충족하는 지능형 회로를 설계 및 개발할 수 있습니다.

주요 하이라이트

- 로직 IC는 전자기기의 소형화와 집적화에 크게 공헌해 왔습니다. 최근의 반도체 제조 기술의 개발에 의해, 소형으로 복잡한 로직 회로가 원칩화되고 있습니다. 이 집적화로 전자 시스템의 물리적 크기와 에너지 소비량을 줄이면서 기능을 향상시킬 수 있기 때문에 휴대 기기나 무선 기술 혹은 공간에 제약이 있는 용도에서도 사용할 수 있게 되었습니다. 디스플레이 드라이버, 범용 로직, MOS 터치스크린 컨트롤러는 최근 시장을 크게 견인하고 있는 로직 컴포넌트의 일부입니다.

- 또한 최종 사용자 산업의 진보로 작고 견고한 반도체 장치에 대한 요구가 증가하고 있습니다. 예를 들어, 최근 스마트폰에서는 기존의 PCB 기판과 달리 더 작은 PCB 기판이 필요합니다. 또, 불규칙하고 다른 형상을 가지는 웨어러블 등의 IoT 디바이스의 출현도 있어, 이것은 소형화에 의해서만 실현할 수 있습니다. 이 때문에 소형화 IC 부품의 요구가 크게 높아질 것으로 예상됩니다.

- IoT나 IIoT의 등장은 스마트 홈, 오피스, 웨어러블, 원격 감시, 제어 등의 기술의 도입으로 전자기기의 설계나 크기에 큰 영향을 주고 있습니다. 게다가 OEM이나 설계자는, 웨어러블 기술을 개발할 때에, 소형화를 제일로 생각하고 있습니다.

- 소형화된 전자부품을 필요로 하는 또 다른 진보는 휴대 전자기기이며, 공간 절약화 및 소형화를 위해 보다 작고 얇은 반도체 시스템이 필요합니다. 항공우주나 전기차와 같은 고도로 통합된 고속 용도 때문에 노이즈의 영향을 최소화하기 위한 전기적 성능 향상에 대한 요구도 분명합니다. 최종 제품을 설계할 때 이러한 점을 고려한 결과 로직 IC 컴포넌트는 고도의 전자 시스템 개발에서 점점 더 중요해지고 있습니다.

- 로직 IC는 다양한 복잡한 기능을 수행할 것으로 기대되고 있습니다. 기술의 진보에 따라, 전자 기기에는 보다 최첨단의 기능이나 성능이 요구되고 있습니다. 설계자는 이러한 요구를 충족시키기 위해 복잡한 논리 회로와 알고리즘을 통합해야 합니다. 이러한 기능의 증가는 설계의 대규모화, 복잡화로 이어져 다양한 컴포넌트 간의 복잡한 상호작용을 관리하고 최적화하는 것을 과제로 하고 있습니다.

- COVID-19의 대유행으로 시장은 큰 변화를 이루었고, 고객 행동, 사업 수익, 기업 운영의 다양한 측면에 영향을 주었습니다. 팬데믹은 공급 측에서 그동안 알지 못했던 위험을 밝혀 필수 부품과 구성 요소의 부족을 초래할 수 있습니다. 그 결과 반도체 기업들은 회복력을 높이기 위해 공급망을 적극적으로 재구축하고 있으며, 이러한 조정은 팬데믹 이후 시대에도 지속될 가능성이 있습니다.

로직 IC(집적 회로) 시장 동향

급성장하는 자동차 부문

- 로직 IC는 자동차의 제어 시스템과 통신 시스템에 필수적입니다. 엔진 컨트롤 유닛(ECU), 변속기 컨트롤 유닛(TCU), 앤티록 브레이크 시스템, 인포테인먼트, 에어백 컨트롤 모듈, 시스템, 기타 다양한 전자 제어 유닛에서 사용되고 있습니다. IC는 차량 제어, 감시, 통신을 위한 고급 알고리즘과 논리 기능을 처리하고 실행할 수 있습니다.

- 소비자는 ADAS(선진운전지원시스템), 지능형 조명시스템, 개인화 설정, 음성 컨트롤 등 쾌적성, 안전성, 편리성을 포함한 선진적인 기능, 편리성, 원활한 사용자 체험을 제공할 것을 자동차에 기대하고 있습니다. 소비자의 기대에 부응하고 혁신적인 기능을 제공하는 것이 자동차 산업에서 로직 IC의 수요를 촉진하고 있습니다.

- 자동 긴급 브레이크, 차선 편차 경고, 적응형 크루즈 컨트롤 등 다양한 ADAS 기술이 최신 자동차에 널리 사용되고 있습니다. 로직 IC는 센서 데이터 처리, 실시간 의사결정, 차량 기능 제어에 필수적입니다. 향후의 동향으로서 보다 고도의 ADAS 기능의 개발이 이루어질 가능성이 있으며, 보다 높은 연산 능력, 낮은 레이턴시, 센서 및 퓨전 기능의 강화를 갖춘 로직 IC가 필요합니다.

- 자동차 산업에서는 안전성과 기능 요구 사항이 매우 중요합니다. 로직 IC는 ADAS, 자율주행, 파워트레인 제어 등 다양한 자동차 시스템의 안전하고 신뢰성 높은 동작을 보장합니다. ISO 26262와 같은 까다로운 안전 규격을 충족하는 고성능, 신뢰성 높은 로직 IC에 대한 요구가 자동차 시장에서의 수요를 견인하고 있습니다.

- 자율주행차의 추구는 자동차 산업에 있어서의 중요한 동향입니다. 로직 IC는 자율 주행에 필요한 복잡한 처리 및 의사 결정에 필수적입니다.

- 롤랜드 베르거에 따르면, 2025년, 레벨 4의 경자율 주행차의 보급률은 1%가 될 것으로 예상되고, 그 후 시장 점유율은 서서히 증가합니다. 게다가 2030년에는 세계 시장의 5%가 레벨 4의 소형 자율주행차가 될 것으로 예상되고 있습니다. 자율주행 기술이 발전함에 따라 처리 능력 향상, 고도의 센서 통합, 견고한 안전 기능을 갖춘 로직 IC가 요구될 것으로 보입니다.

- 또한, 환경문제와 정부의 규제로 전기차로의 이동이 가속화되고 있습니다. EV는 첨단 파워 일렉트로닉스 및 배터리 관리를 기반으로 하므로 최적의 에너지 사용, 모터 제어 및 충전 인프라의 통합을 보장하기 위해 특수 로직 IC가 필요합니다.

- IEA의 최신 보고서에 따르면 2022년에는 세계에서 1,000만 대 이상의 전기차가 구입되었으며, 2023년에는 판매량이 35% 증가하여 1,400만 대에 달한 것으로 평가되고 있습니다. 2023년에는 중국, 유럽, 미국 및 기타 지역에서 1,390만 대의 전기자동차가 판매되었습니다.

큰 성장을 기록하는 아시아태평양

- 아시아태평양은 중국과 일본만의 분석으로 구성되어 있습니다. 이 지역은 세계 반도체 산업에서 역동적이고 급성장하는 부문입니다. 신흥경제국, 강력한 제조능력, 전자기기에 대한 수요 증가를 배경으로 아시아태평양은 로직IC의 기술 혁신, 생산, 소비를 추진하는 데 있어 매우 중요합니다.

- 아시아태평양은 반도체 제조 세계의 허브이며 중국과 일본 등이 반도체 제조와 조립을 선도하고 있습니다. 대형 반도체 주조소, 조립 및 시험 시설, 전자기기 제조 서비스가 존재하기 때문에 로직 IC의 효율적이고 비용 효율적인 생산이 가능합니다. 중국에는 산업화와 자동화의 진전에 따라 ADAS와 EV의 개발이 진행되는 광대하고 급속하게 확대하는 소비자 전자기기 시장과 자동차 시장이 있습니다.

- 중국은 국내 시장의 안정적인 업적과 그 거대한 잠재력으로 자동차 및 모빌리티 산업의 세계 리더로 알려져 있습니다. 중국 공업정보화부는 국내 자동차 생산량이 2025년까지 3,500만 대에 달해 세계 유수의 자동차 업체로서의 위상을 더욱 강화할 것으로 예측하고 있습니다. CAAM에 따르면 2023년 8월 중 중국의 신에너지 차량 판매량은 84만 6,000대로 그 중 80만 8,000대가 승용 EV, 3만 9,000대가 상용 EV였습니다. BEV는 55만 9,000대, PHEV는 24만 8,000대였습니다.

- 또한 중국의 자동차 물류 시장 예측에 따르면 새로운 에너지 승용차 카테고리의 배터리 전기자동차(BEV)는 2025년까지 시장 점유율의 84%를 차지할 것으로 예상되며, 이는 BEV에 ADAS 통합과 같은 부문의 주요 기술 진보로 이어질 것입니다. 2024년에는 중국은 지능형 운전 시스템 채택에서 문턱값을 달성할 가능성이 높습니다. 자동차 교체 주기는 예상보다 AD 레벨의 채택이 빠르게 진행됨에 따라 단축될 수 있습니다. 공급 증가는 집중적인 소비자 교육과 미디어 노출을 동반할 수 있어 중국 소비자들의 스마트 운전으로의 전환을 가속화할 것으로 보입니다.

- 아시아태평양의 EV 시장의 급성장은 로직 집적 회로(IC) 시장에 큰 영향을 미칠 것으로 예측됩니다. EV가 ADAS와 인텔리전트 드라이빙 시스템 등 보다 고급 기술을 접목함에 따라 IC, 특히 처리 및 제어 시스템용 IC 수요가 급증할 가능성이 높습니다. 또, EV로의 시프트에 수반해, 충전 인프라의 개발이 필요하지만, IC 기술에 크게 의존하고 있습니다. 그 결과, 로직 IC를 전문으로 하는 반도체 기업은, 지역 전체에서 확대되는 EV 시장으로부터 이익을 얻을 태세를 갖추고 있습니다.

로직 IC(집적 회로) 시장 개요

로직 IC 시장은 세계 기업과 중소기업 모두가 존재하기 때문에 단편화되어 있습니다. 이 시장의 주요 기업으로는 STMicroelectronics NV, Renesas Electronics Corporated, Analog Device Inc., Broadcom Inc., Diodes Incorporated 등이 있습니다. 시장의 다양한 기업들은 제품 라인업을 강화하고 지속 가능한 경쟁 우위를 획득하기 위해 인수 및 제휴 등 다양한 전략을 채택하고 있습니다.

- 2024년 4월-Centrica Energy와 STMicroelectronics간에, 이탈리아의 신재생 에너지에 의한 전력 공급에 관한 장기 계약이 체결되었습니다. 이것은 이탈리아의 새로운 태양광 발전소에서 생산되는 에너지에 관한 10년간의 계약입니다.

- 2024년 4월-르네사스는 웨이퍼 전용 공장인 고후 공장의 조업을 개시했습니다. 야마나시현 카이시에 위치합니다. 고후 공장은 지금까지, 르네사스의 자회사인 르네사스 세미컨덕터 매뉴팩처링 주식회사아래에서 150mm와 200mm의 웨이퍼 제조 라인을 운영하고 있었습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 인사이트

- 시장 개요

- 업계의 밸류체인 및 공급망 분석

- 업계의 매력도-Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 경쟁 기업간 경쟁 관계

- 대체품의 위협

- 시장의 거시경제 동향 분석

- 기술 스냅샷

제5장 시장 역학

- 시장 성장 촉진요인

- 디바이스 통합에 대한 주목의 향상

- 생산 능력 증강을 위한 공장 설비투자 증가

- 시장 성장 억제요인

- 로직 IC 설계의 복잡화

제6장 시장 세분화

- IC 유형별

- 디지털 바이폴라

- MOS 로직별

- MOS 범용

- MOS 게이트 어레이

- MOS 드라이버 및 컨트롤러

- MOS 표준 셀

- MOS 특수 용도

- 용도별

- 소비자용 전자 기기

- 자동차

- IT 및 통신

- 컴퓨터

- 기타

- 지역별

- 아메리카

- 유럽

- 아시아

- 호주 및 뉴질랜드

- 중동 및 아프리카

제7장 경쟁 구도

- 기업 프로파일

- STMicroelectronics NV

- Renesas Electronics Corp.

- Analog Devices Inc.

- Broadcom Inc.

- Diodes Incorporated

- NXP Semiconductors NV

- ON Semiconductor Corporation

- Texas Instruments Inc.

- Intel Corporation

- Toshiba Corporation

제8장 투자 분석

제9장 시장의 미래

AJY 25.05.14The Logic IC Market size is estimated at USD 211.95 billion in 2025, and is expected to reach USD 295.19 billion by 2030, at a CAGR of 6.85% during the forecast period (2025-2030). In terms of shipment volume, the market is expected to grow from 67.97 billion units in 2025 to 83.46 billion units by 2030, at a CAGR of 4.19% during the forecast period (2025-2030).

Ongoing advancements in semiconductor manufacturing processes have led to the development of more complex and efficient logic ICs. Smaller transistor sizes, improved performance, and lower power consumption enable the creation of high-performance logic ICs for a wide range of applications. A logic IC is very flexible and can be used in various applications. One can configure them to perform multiple logical functions, such as AND, OR, NOT, and XOR. This flexibility allows for designing and developing intelligent circuits that meet requirements in different industries, such as consumer electronics, automotive, telecommunications, and industry automation.

Key Highlights

- Logic ICs have significantly aided the miniaturization and integration of electronic devices. The development of the technology to manufacture semiconductors has produced small, more complex logic circuits on a single chip in recent years. This integration increases functionality while reducing electronic systems' physical size and energy consumption so that they can be used in portable devices, wireless technology, or space-constrained applications. Display drivers, general purpose logic, and MOS touch screen controllers are some of the logic components that have gained significant market traction in recent years.

- Furthermore, advances in end-user industries have created the need for small and robust semiconductor devices. For instance, nowadays, smartphones require a smaller PCB board, unlike traditional PCB boards. There has also been the advent of IoT devices, such as wearables with irregular and different shapes, which can only be achieved through miniaturization. This is expected to boost the need for miniaturized IC components significantly.

- The advent of the IoT and IIoT has largely impacted the design and size of electronics, with the introduction of technologies like smart homes, offices, wearables, remote monitoring, and control. Moreover, OEMs and designers consider miniaturization a primary focus while creating wearable technologies.

- Another advancement that demands miniaturized electronic components is portable electronic equipment, which requires smaller and thinner semiconductor systems for saving space and miniaturization. Due to highly integrated, high-speed applications like aerospace and electric vehicles, the demand for improved electrical performance to minimize noise effects is also evident. As a result of these considerations when designing end products, logic IC components are becoming increasingly important in developing advanced electronic systems.

- Logic ICs are expected to perform a wide range of complex functions. The demand for more state-of-the-art features and capabilities in electronic devices grows as technology advances. Designers need to incorporate complex logic circuits and algorithms to meet these requirements. This increased functionality leads to larger and more intricate designs, making it challenging to manage and optimize the complex interactions between different components.

- The market has undergone substantial changes due to the COVID-19 pandemic, impacting customer behavior, business revenues, and various aspects of corporate operations. The pandemic revealed previously unnoticed risks on the supply side, potentially resulting in shortages of essential parts and components. Consequently, semiconductor companies are proactively restructuring their supply chains to enhance resilience, and these adjustments may persist in the post-pandemic era.

Logic IC (Integrated Circuit) Market Trends

The Automotive Segment to Witness Rapid Growth

- Logic ICs are essential in vehicle control and communications systems. They are used in engine control units (ECUs), transmission control units (TCUs), antilock braking systems infotainment, airbag control modules, systems, and various other electronic control units. ICs can process and execute sophisticated algorithms and logical functions for vehicle control, monitoring, and communication.

- Consumers expect vehicles to offer advanced features, convenience, and a seamless user experience, including comfort, safety, and convenience, such as advanced driver assistance, intelligent lighting systems, personalized settings, and voice control. Meeting consumer expectations and providing innovative features drive the demand for logic ICs in the automotive industry.

- Various ADAS technologies, such as automatic emergency braking, lane departure warning, and adaptive cruise control, are becoming more prevalent in modern vehicles. Logic ICs are critical in processing sensor data, enabling real-time decision-making, and controlling vehicle functions. Future trends may involve the development of more advanced ADAS features, requiring logic ICs with higher computational power, low latency, and enhanced sensor fusion capabilities.

- In the automotive industry, safety and functional requirements are of great importance. Logic ICs ensure various automotive systems' safe and reliable operation, including ADAS, autonomous driving, and powertrain control. The need for high-performance, reliable logic ICs that meet stringent safety standards, such as ISO 26262, drives the demand in the automotive market.

- The pursuit of autonomous vehicles is a significant trend in the automotive industry. Logic ICs are essential for the complex processing and decision-making required for autonomous driving.

- According to Roland Berger, in 2025, the penetration rate of level 4 light autonomous vehicles is expected to be 1%, with a gradually increasing market share in subsequent years. Furthermore, 5% of the global market is anticipated to comprise level 4 light autonomous vehicles by 2030. As self-driving technology advances, logic ICs with increased processing power, advanced sensor integration, and robust safety features are likely to be in demand.

- Moreover, due to environmental concerns and government regulations, the shift toward the use of electric vehicles is gaining momentum. EVs are based on advanced power electronics and battery management, which requires specialized logic ICs to ensure optimum energy use, motor control, or charging infrastructure integration.

- According to the latest report from IEA, over 10 million electric vehicles were bought worldwide in 2022, and sales were estimated to increase by 35% in 2023 to reach 14 million. In 2023, China, Europe, the United States, and other regions sold 13.9 million electric vehicles.

Asia-Pacific to Register Major Growth

- Asia-Pacific consists of the analysis of only China and Japan. The region is a dynamic and rapidly growing segment of the global semiconductor industry. With emerging economies, strong manufacturing capabilities, and growing demand for electronic devices, Asia-Pacific is pivotal in driving innovation, production, and consumption of logic ICs.

- Asia-Pacific is a global manufacturing hub for semiconductor production, with countries such as China and Japan leading in semiconductor manufacturing and assembly. The presence of leading semiconductor foundries, assembly and testing facilities, and electronics manufacturing services enables efficient and cost-effective production of logic ICs. It is home to a vast and rapidly expanding consumer electronics market and automotive market with developments in ADAS and EVs along with increasing industrialization and automation.

- China is known as a global leader in the automotive and mobility industry owing to the consistent performance of the domestic market and its enormous potential. The Chinese Ministry of Industry and Information Technology projects that domestic vehicle production will reach 35 million by 2025, further strengthening its position as the world's leading car manufacturer. According to CAAM, China's new energy vehicle sales amounted to 846,000 units, 808,000 of which were passenger EVs and 39,000 were commercial electric vehicles during August 2023. Sales of BEVs and PHEVs recorded 559,000 and 248,000 vehicles, respectively.

- Furthermore, according to the forecast from China's automotive logistics market, it is expected that the battery electric vehicles (BEV) in the new energy passenger vehicle category will have 84% of the market share by 2025, which leads to major technological advancements in the segment like integration of ADAS in BEVs. In 2024, China is likely to achieve a threshold in adopting intelligent driving systems. The replacement cycle of vehicles could be shortened by more rapid adoption of AD levels than anticipated. An increase in supply may be accompanied by intensive consumer education and media exposure, which will accelerate Chinese consumers' shift toward smart driving.

- The rapid growth of EV markets in Asia-Pacific is expected to impact the logic integrated circuit (IC) market significantly. As EVs incorporate more advanced technologies like ADAS and intelligent driving systems, the demand for ICs, especially those for processing and control systems, will likely surge. Additionally, the shift toward EVs necessitates developing charging infrastructure, which relies heavily on IC technology. As a result, semiconductor companies specializing in logic ICs are poised to benefit from the expanding EV markets across the region.

Logic IC (Integrated Circuit) Market Overview

The logic IC market is fragmented due to the presence of both global players and small and medium-sized enterprises. Some of the major players in the market are STMicroelectronics NV, Renesas Electronics Corp., Analog Devices Inc., Broadcom Inc., and Diodes Incorporated. The various players in the market are adopting different strategies, such as acquisitions and partnerships, to enhance their product offerings and gain a sustainable competitive advantage.

- In April 2024, a long-term agreement was signed between Centrica Energy and STMicroelectronics for the supply of electricity produced from renewable sources in Italy. It is a 10-year contract for energy produced by a new solar farm in Italy.

- In April 2024, Renesas started the operation of Kofu Factory, a dedicated wafer fab. It is located in Kai City, Yamanashi Prefecture, Japan. The Kofu Factory previously operated both 150 mm and 200 mm wafer fabrication lines under Renesas Semiconductor Manufacturing Co., a subsidiary of Renesas.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET INSIGHTS

- 4.1 Market Overview

- 4.2 Industry Value Chain/Supply Chain Analysis

- 4.3 Industry Attractiveness - Porter's Five Forces Analysis

- 4.3.1 Bargaining Power of Suppliers

- 4.3.2 Bargaining Power of Buyers

- 4.3.3 Threat of New Entrants

- 4.3.4 Intensity of Competitive Rivalry

- 4.3.5 Threat of Substitutes

- 4.4 Analysis of Macroeconomic Trends on the Market

- 4.5 Technology Snapshot

5 MARKET DYNAMICS

- 5.1 Market Drivers

- 5.1.1 Increasing Focus on Device Integration

- 5.1.2 Increasing Capital Expenditure of Fabs to Augment Production Capacity

- 5.2 Market Restraints

- 5.2.1 Complexity Associated with Logic IC Design

6 MARKET SEGMENTATION

- 6.1 By IC Type

- 6.1.1 Digital Bipolar

- 6.1.2 By MOS Logic

- 6.1.2.1 MOS General Purpose

- 6.1.2.2 MOS Gate Arrays

- 6.1.2.3 MOS Drivers/Controllers

- 6.1.2.4 MOS Standard Cells

- 6.1.2.5 MOS Special Purpose

- 6.2 By Application

- 6.2.1 Consumer Electronics

- 6.2.2 Automotive

- 6.2.3 IT and Communication

- 6.2.4 Computer

- 6.2.5 Other Applications

- 6.3 By Geography

- 6.3.1 Americas

- 6.3.2 Europe

- 6.3.3 Asia

- 6.3.4 Australia and New Zealand

- 6.3.5 Middle East and Africa

7 COMPETITIVE LANDSCAPE

- 7.1 Company Profiles

- 7.1.1 STMicroelectronics NV

- 7.1.2 Renesas Electronics Corp.

- 7.1.3 Analog Devices Inc.

- 7.1.4 Broadcom Inc.

- 7.1.5 Diodes Incorporated

- 7.1.6 NXP Semiconductors NV

- 7.1.7 ON Semiconductor Corporation

- 7.1.8 Texas Instruments Inc.

- 7.1.9 Intel Corporation

- 7.1.10 Toshiba Corporation