|

시장보고서

상품코드

1693938

유럽의 위성 발사체 시장(2025-2030년) : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측Europe Satellite Launch Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

■ 보고서에 따라 최신 정보로 업데이트하여 보내드립니다. 배송일정은 문의해 주시기 바랍니다.

가격

※ 부가세 별도

한글목차

영문목차

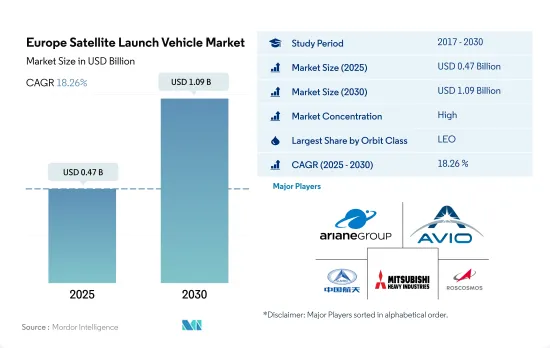

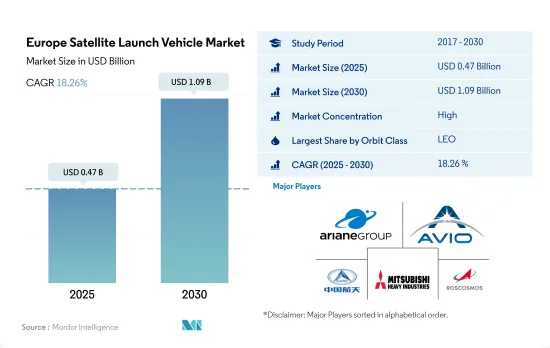

유럽의 위성 발사체 시장 규모는 2025년에 4억 7,000만 달러로 추정되고, 2030년에는 10억 9,000만 달러에 이를 전망이며 예측 기간(2025-2030년) 동안 CAGR 18.26%를 보일 것으로 예측됩니다.

유럽의 궤도 발사 시스템 수요 증가

- 위성과 우주선은 발사 후에 대개 지구를 돌아다니는 많은 특별한 궤도 중 하나에 배치됩니다. 중궤도 위성에는 특정 지역을 모니터링하도록 설계된 항법 위성과 특수 위성이 포함됩니다.

- 소형 로켓은 기존의 대형 로켓과 달리 특정 궤도까지 들어올 수 있는 페이로드의 양과 발사 비용에 따라 기체의 성능이 달라집니다. 소형 위성 로켓은 차세대의 미래를 담당할 것으로 기대되고 있습니다.

- 2022년 10월, 유럽우주국은 일상 기기에 더 정확한 위치 데이터를 제공하기 위해 기존의 위성보다 훨씬 지구에 가까운 궤도를 주회하는 새로운 항법 위성의 검사를 계획했습니다. GPS 위성은 주로 10,000-20,000km의 지구 중간 궤도에 배치됩니다.

저비용 발사 시스템에 대한 수요가 증가하고 있으며 이 지역의 시장 성장을 가속하고 있습니다.

- 발사 장비 산업은 유럽에서 상업 위성 개발에 이어 두 번째로 큰 우주 제조 활동으로, 유럽 시장의 성장을 뒷받침하고 있습니다. 유럽은 유럽 정부의 모든 요구와 상업 시장의 대부분을 충족하는 능력과 유연성을 갖춘 일련의 로켓을 이용하여 유럽의 사회 경제적 이익과 우주에 대한 접근성을 높이고 있습니다.

- 유럽의 위성 발사체 시장 특징은 여러 참가 기업이 존재하는 점입니다.

- 위성 발사체 산업은 군사 모니터링, 통신, 네비게이션에서 지구 관측에 이르기까지 폭넓은 용도의 위성 수요에 의해 견인되고 있습니다. 이를 바탕으로 2017-2022년 사이에 이 지역에서는 총 570기 이상의 위성이 발사되었습니다.

- 국가가 운용하는 위성의 수에서는 2017-2022년 사이에 발사된 위성이 462기 이상으로 영국이 1위이며, 이어서 러시아가 65기, 독일이 34기 순입니다. 우주 기관과 비공개 회사는 최근 위성 발사 시스템의 비용 절감에 노력하고 있습니다. 2023-2029년에 걸쳐 예측 기간 동안 시장은 213% 급성장할 것으로 예측됩니다.

유럽 위성 발사체 시장 동향

유럽 발사체 시장 수요 증가와 경쟁

- 유럽 발사체는 다양한 궤도에 다양한 페이로드를 발사할 수 있는 폭넓은 옵션으로 알려져 있습니다. 유럽 발사체 수요를 견인하는 주요 요인은 상업 우주 산업의 성장입니다. 위성 및 기타 우주 자산을 궤도에 발사하려는 기업이 늘어남에 따라 신뢰성이 높고 비용 효율적인 솔루션으로 유럽 발사체가 주목받고 있습니다. 유럽 발사체 회사는 재사용 가능한 로켓, 전기 추진 시스템, 인공지능 등 신기술에 투자하여 발사 능력을 향상시키고 시장 경쟁을 유지하고 있습니다. 예를 들어, ArianeGroup은 재사용 가능한 Ariane Next 로켓을 개발하고 있으며, Airbus는 Ariane 로켓의 재사용 가능한 첫 번째 단을 포함하는 Adeline 컨셉을 개발하고 있습니다.

- 또한 소형 위성 발사에 대한 수요가 증가하고 있으며, 이는 유럽 기업에 의한 소형 발사체 개발을 뒷받침하고 있습니다. 예를 들어, PLD Space는 소형 위성 발사용 Miura 1 로켓과 Miura 5 로켓을 개발하고 있으며, Isar Aerospace도 같은 목적으로 스펙트럼 로켓을 개발하고 있습니다. 우주산업에서는 국제협력의 경향이 강해지고 있으며, 유럽의 발사체 제조업체는 세계의 기업이나 조직과 제휴하고 있습니다. 이 배경은 우주 임무의 복잡성 외에도 자원과 전문 지식을 공유해야합니다. Arianespace 회사는 유럽 우주 기관과 프랑스 우주청, PLD Space는 유럽 우주 기관 및 스페인 정부와 제휴하고 있습니다.

유럽 위성 발사체 시장의 투자 기회 증가 요인

- 유럽 국가들은 우주 부문에서 다양한 투자의 중요성을 인식하고 있으며 세계 우주 산업에서 경쟁과 혁신을 유지하기 위해 다양한 우주 프로그램에 대한 지출을 늘리고 있습니다. 2022년 11월, 유럽우주국(ESA)은 2023-2025년에 185억 유로의 예산을 지원하도록 22개국에 요청했다고 발표했습니다. 유럽은 2023년 4분기에 차세대 우주 로켓인 Ariane 6의 1호기 발사를 계획하고 있습니다. 해당 로켓은 39억 달러 미만을 들여 개발되었으나 당초 2020년 7월 첫 발사를 예정하고 있던 이 프로젝트는 잇따라 연기되고 있습니다. 프랑스, 독일, 이탈리아의 3개국 정부는 유럽의 로켓 경쟁을 강화하는 동시에 유럽의 우주에 대한 독립적인 접근을 보장하기 위해 "유럽 로켓 개발의 미래"에 관한 협정에 서명했다고 발표했습니다.

- 2022년 9월 프랑스 정부는 지난 3년간 약 25% 증가한 90억 달러 이상을 우주 활동에 충당할 예정이라고 발표했습니다. Ariane 6은 우주로 페이로드를 운반하는 새로운 유럽의 로켓이 될 전망입니다. 독일은 Ariane 6의 추가 개발과 시장 도입에 총액 1억 6,200만 유로를 투자하고 있습니다. 독일은 LEAP(Launchers Exploitation Accompaniment) 프로그램에 약 5,200만 유로를 투자하고 있습니다.

유럽 위성 발사체 산업 개요

유럽의 위성 발사체 시장은 상당히 통합되어 있으며 상위 5개 기업에서 99.01%를 차지하고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 서포트

목차

제1장 주요 요약과 주요 조사 결과

제2장 보고서 제안

제3장 소개

- 조사의 전제조건과 시장 정의

- 조사 범위

- 조사 방법

제4장 주요 산업 동향

- 위성의 소형화

- 발사체 소유자

- 우주 개발에의 지출

- 규제 프레임워크

- 프랑스

- 독일

- 러시아

- 영국

- 밸류체인과 유통채널 분석

제5장 시장 세분화

- 궤도 클래스

- GEO

- LEO

- MEO

- 로켓

- 대형

- 소형

- 중형

- 발사국

- 러시아

제6장 경쟁 구도

- 주요 전략 동향

- 시장 점유율 분석

- 기업 상황

- 기업 프로파일

- Ariane Group

- Avio

- Blue Origin

- China Aerospace Science and Technology Corporation(CASC)

- Indian Space Research Organisation(ISRO)

- Mitsubishi Heavy Industries

- Rocket Lab USA, Inc.

- ROSCOSMOS

- Space Exploration Technologies Corp.

- The Boeing Company

- Virgin Orbit

제7장 CEO에 대한 주요 전략적 질문

제8장 부록

- 세계 개요

- 개요

- Porter's Five Forces 분석 프레임워크

- 세계의 밸류체인 분석

- 시장 역학(DROs)

- 정보원과 참고문헌

- 도표 일람

- 주요 인사이트

- 데이터 팩

- 용어집

The Europe Satellite Launch Vehicle Market size is estimated at 0.47 billion USD in 2025, and is expected to reach 1.09 billion USD by 2030, growing at a CAGR of 18.26% during the forecast period (2025-2030).

Rising demand for orbital launch systems in Europe

- At launch, a satellite or spacecraft is usually placed into one of many special orbits around the Earth, or it can be launched into an interplanetary journey. Many weather and communication satellites tend to have high Earth orbits farthest from the surface. Satellites in the mean (medium) Earth orbit include navigational and specialized satellites that are designed to monitor a specific area. Most science satellites, including ESA's Earth Observation System team, are in low Earth orbit

- Light launchers differ from conventional heavy launchers in the vehicle's performance, which depends on the amount of payload the vehicle can lift to a particular orbit and the launch cost. With the expansion of the capabilities of small satellites, the space industry is developing strategic utility, which, in turn, leverages various stakeholders, including governments, space agencies, and private companies, to expand. Small satellite launchers are expected to be the future of the next generation. These types of launchers are essential for launching satellites, carrying out science missions, and resupplying the International Space Station. The increasing number of satellites being launched into orbit due to increased space activities is driving the demand for medium-range launch vehicles.

- In October 2022, the European Space Agency planned to test new navigation satellites that would orbit much closer to Earth than existing ones to provide more accurate position data for everyday devices. The Global Positioning Satellite System is typically placed in mid-Earth orbit about (10,000 to 20,000 km) from the Earth's surface. During 2017-2022, a total of 590+ satellites were launched in the region. The market is expected to witness a growth of 210% during the forecast period between 2023 and 2029.

There is a rising demand for low-cost launch systems aiding the market growth in the region

- The launch equipment industry is the second-largest space manufacturing activity in Europe after the development of commercial satellites, which is aiding the growth of the European market. Ariane 5, Soyuz, and Vega take off from Europe's spaceport in French Guiana. Europe benefits from this line of launchers with the ability and flexibility to meet all the needs of the European government and most of the commercial market, thereby increasing its socioeconomic benefits and access to space in Europe

- The European satellite launch vehicles market is characterized by the presence of several players. The major launch vehicles in this region are Ariane 5, Soyuz, and Vega, among others. Space organizations like EASA have partnered with private players like SpaceX in the production and launch of satellites in the field.

- The satellite launch vehicle industry is driven by demand for satellites for applications ranging from military surveillance, communications, and navigation to Earth observation. As a result, the demand for satellites from the civilian/government, commercial and military sectors is increasing. On this basis, during the period 2017-2022, a total of more than 570+ satellites were launched in the region. The growth in the number of satellites launched from 2020 to 2021 is 140% after the impact of the COVID-19 pandemic.

- In terms of the number of satellites operated by a country, the United Kingdom leads with more than 462 satellites launched between 2017 and 2022, followed by Russia and Germany with 65 and 34, respectively. Space agencies and private companies have tried to reduce the cost of satellite launch systems in recent years. Between 2023 and 2029, the market is expected to surge by 213% during the forecast period.

Europe Satellite Launch Vehicle Market Trends

Growing demand and competition in the European launch vehicle market

- European launch vehicles are known for their versatility, capable of launching a wide range of payloads into various orbits. A key factor driving the demand for European launch vehicles is the growing commercial space industry. As more and more companies seek to launch satellites and other space-based assets into orbit, they are turning to European launch vehicles as a reliable and cost-effective solution. European launch companies are investing in new technologies, such as reusable launch vehicles, electric propulsion systems, and artificial intelligence, to improve their launch capabilities and stay competitive in the market. For example, ArianeGroup is developing the Ariane Next reusable rocket, and Airbus is developing the Adeline concept, which involves a reusable first stage for the Ariane rocket.

- Additionally, the demand for small satellite launches is increasing, which is driving the development of smaller launch vehicles by European companies. For example, PLD Space is developing the Miura 1 and Miura 5 rockets for small satellite launches, while Isar Aerospace is developing the Spectrum rocket for the same purpose. There is a growing trend toward international collaboration in the space industry, with European launch vehicle manufacturers partnering with companies and organizations across the world. This is driven by the increasing complexity of space missions, as well as the need to share resources and expertise. On this note, Arianespace has partnerships with the European Space Agency and the French Space Agency, and PLD Space is working with the European Space Agency and the Spanish government.

Increasing investment opportunities in the European satellite launch vehicle market is the driver

- European countries are recognizing the importance of various investments in the space domain. They are increasing their spending on various space programs to stay competitive and innovative in the global space industry. In November 2022, the European Space Agency (ESA) announced that it requested its 22 nations to back a budget of EUR 18.5 billion for 2023-2025. Europe plans to launch the first Ariane 6 rocket, its next-generation space launcher, in the fourth quarter of 2023. Developed at a cost of just under USD 3.9 billion and originally set for an inaugural launch in July 2020, the project has been hit by a series of delays. The governments of France, Germany, and Italy announced that they had signed an agreement on "the future of launcher exploitation in Europe" to enhance the competitiveness of European vehicles while also ensuring independent European access to space.

- In September 2022, the French government announced that it is planning to allocate more than USD 9 billion to space activities, an increase of about 25% over the past three years. In November 2022, Germany announced that about EUR 2.37 billion was allocated for various space-related projects. The country mentioned that from the end of 2023, Ariane 6 is expected to be the new European launcher to carry payloads into space. Germany is contributing a total of EUR 162 million to the further development of Ariane 6 and its market introduction. The country is investing around EUR 52 million in the optional LEAP (Launchers Exploitation Accompaniment) program, which also includes the operation of DLR's test facility for rocket engines in Lampoldshausen.

Europe Satellite Launch Vehicle Industry Overview

The Europe Satellite Launch Vehicle Market is fairly consolidated, with the top five companies occupying 99.01%. The major players in this market are Ariane Group, Avio, China Aerospace Science and Technology Corporation (CASC), Mitsubishi Heavy Industries and ROSCOSMOS (sorted alphabetically).

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 EXECUTIVE SUMMARY & KEY FINDINGS

2 REPORT OFFERS

3 INTRODUCTION

- 3.1 Study Assumptions & Market Definition

- 3.2 Scope of the Study

- 3.3 Research Methodology

4 KEY INDUSTRY TRENDS

- 4.1 Satellite Miniaturization

- 4.2 Owner Of Launch Vehicle

- 4.3 Spending On Space Programs

- 4.4 Regulatory Framework

- 4.4.1 France

- 4.4.2 Germany

- 4.4.3 Russia

- 4.4.4 United Kingdom

- 4.5 Value Chain & Distribution Channel Analysis

5 MARKET SEGMENTATION (includes market size in Value in USD, Forecasts up to 2030 and analysis of growth prospects)

- 5.1 Orbit Class

- 5.1.1 GEO

- 5.1.2 LEO

- 5.1.3 MEO

- 5.2 Launch Vehicle Mtow

- 5.2.1 Heavy

- 5.2.2 Light

- 5.2.3 Medium

- 5.3 Country

- 5.3.1 Russia

6 COMPETITIVE LANDSCAPE

- 6.1 Key Strategic Moves

- 6.2 Market Share Analysis

- 6.3 Company Landscape

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and Analysis of Recent Developments).

- 6.4.1 Ariane Group

- 6.4.2 Avio

- 6.4.3 Blue Origin

- 6.4.4 China Aerospace Science and Technology Corporation (CASC)

- 6.4.5 Indian Space Research Organisation (ISRO)

- 6.4.6 Mitsubishi Heavy Industries

- 6.4.7 Rocket Lab USA, Inc.

- 6.4.8 ROSCOSMOS

- 6.4.9 Space Exploration Technologies Corp.

- 6.4.10 The Boeing Company

- 6.4.11 Virgin Orbit

7 KEY STRATEGIC QUESTIONS FOR SATELLITE CEOS

8 APPENDIX

- 8.1 Global Overview

- 8.1.1 Overview

- 8.1.2 Porter's Five Forces Framework

- 8.1.3 Global Value Chain Analysis

- 8.1.4 Market Dynamics (DROs)

- 8.2 Sources & References

- 8.3 List of Tables & Figures

- 8.4 Primary Insights

- 8.5 Data Pack

- 8.6 Glossary of Terms