|

시장보고서

상품코드

1836429

생물학적 안전성 시험 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Biological Safety Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

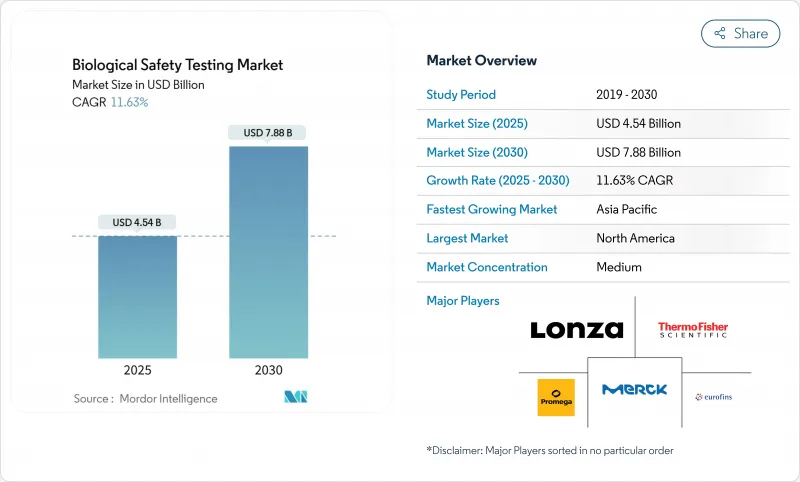

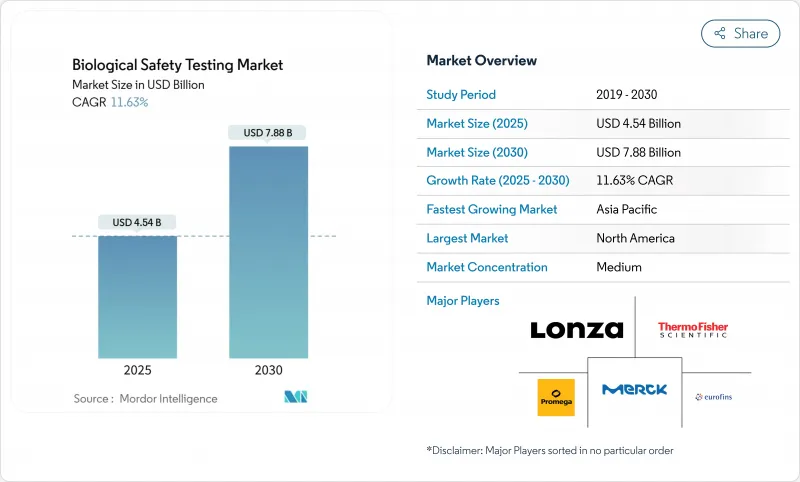

생물학적 안전성 시험 시장 규모는 2025년에 45억 4,000만 달러에 달하고, 2030년에는 78억 8,000만 달러에 이를 것으로 예상되며, 시장 추계·예측 기간(2025-2030년)의 CAGR은 11.63%를 나타낼 전망입니다

규제 당국은 현재 보다 풍부한 바이러스 및 마이코플라즈마의 안전성 데이터 세트를 요구하고 있는 반면, 제조업체는 집중적인 오염 관리가 필요한 첨단 치료제(ATMP)의 규모를 확대하고 있습니다. AI를 활용한 인실리코 바이오 세이프티 모델링이 품질 관리 워크플로우에 통합되고 있어 배치 불량률을 저감하고 릴리스 시간을 단축하고 있습니다. BARDA와 EU-HERA에 의한 생물 위협 대책에 대한 지출은 기존의 바이오파마 고객층 이외에도 수요를 넓히고 있습니다. 아시아에 기반을 둔 CDMO, 특히 중국의 CDMO에 대한 품질관리 아웃소싱은 일본의 실험실이 국제 인증을 받으면서 공급망을 재구성하고 있습니다.

세계의 생물학적 안전성 시험 시장 동향과 인사이트

세계 의약품 및 생명공학 파이프라인 및 벤처 자금 조달 성장

종양학, 면역학 및 유전자 요법의 거래 흐름은 과거 최고를 기록했습니다. 보다 큰 라운드에서는 보다 풍부한 전임상 데이터세트에 자금이 제공되므로 보다 확장된 바이오 세이프티 테스트 패널이 필요합니다. Aclid와 같은 신흥 기업은 오염 위험을 줄이는 DNA 합성 스크리닝 플랫폼을 위해 시드 캐피탈을 조달하여 수탁 시험 회사로 수량을 밀어 올리고 있습니다. 파이프라인의 확대는 제약회사가 사내에 능력을 유지하는 것보다 안전성 시험을 전문업자에게 위탁하는 경향이 강해지고 있기 때문에 수탁시험기관에 특히 이익을 가져옵니다.

첨단 치료제(ATMPs) 제조의 스케일 업

2024년 유럽 의약청의 지침 업데이트와 FDA의 병행 초안을 통해 ATMP 제조업체는 부정형 바이러스 및 세포주 인증 분석을 확대했습니다. Lonza의 Vacaville에서 12억 달러의 토지 취득은 이러한 고급 QC 스위트를 설치하는 데 필요한 자본 집계를 보여줍니다. 부정형 바이러스 검출 및 세포 특성화와 같은 ATMP에 필요한 독특한 검사는 더 높은 마진과 기술 진입 장벽을 가진 특수 시장 부문을 생성합니다.

새로운 신속한 마이크로 방법의 긴 검증주기

FDA의 프로세스 분석 기술 프레임워크의 장려에도 불구하고 세계 검증은 Compendial Method와의 사이드 바이 사이드 테스트를 18-24개월 요구합니다. Rapid Micro Biosystems와 같은 공급업체는 1-3일 내에 무균성을 읽을 수 있음을 입증하지만, 스폰서는 규제상의 편안함이 입증될 때까지 기존 분석을 병행하여 수행합니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 바이러스 및 마이코플라스마 오염에 관한 규제 강화

- 비용 효율적인 QC 서비스를 요구하는 아시아 기반 CDMO에 아웃소싱 급증

- 자격을 갖춘 바이오 안전 인력 부족과 높은 교육 비용

부문 분석

시약 및 키트는 2024년에 45.12%의 매출을 획득했는데, 이는 무균 주사제와 ATMP의 릴리스 로트에서 시험량이 확대됨에 따라 소모품의 풀스루를 반영하고 있습니다. 시약으로 인한 생물학적 안전성 시험 시장 규모는 오염 검사 빈도가 증가함에 따라 확대됩니다. 일회용 필터와 재조합 C 인자 내독소 바이알이 구매 주문의 대부분을 차지하고 있지만, PFAS에 기인하는 PVDF 필터의 단계적 폐지가 재설계에 박차를 가하고 있습니다. 자동 플레이트 판독 시스템, ddPCR 분석, 실시간 인큐베이션 챔버가 견인하고 장비 매출은 CAGR 12.12%를 나타낼 전망입니다. 벤더는 AI 모듈을 통합하고 비정상적으로 플래그를 지정하거나 위양성을 미연에 방지함으로써 편차 조사를 축소하고 있습니다. 제약 스폰서가 무균, 내독소, 세포주 인증을 전문 실험실에 아웃소싱하고 샘플 물류 및 데이터 무결성 감사를 포함한 일괄 계약을 활용하여 서비스 수익이 증가합니다. ATMP 파이프라인 증가는 특주 어드벤티셔스 바이러스 패널에 지출을 기울여, 이들은 가격이 비쌉니다.

2024년 생물학적 안전성 시험 시장 점유율은 무균성 시험이 32.69%를 차지했으며 비경구 제형의 모든 배치에서 출시에 필수적인 단계임에 변함이 없습니다. 인큐베이션 기반 프로토콜은 여전히 신청 건수의 대부분을 차지하고 있지만, BACT/ALERT와 같은 연속 모니터링 시스템은 최종 승인까지의 기간을 단축합니다. 마이코플라즈마 검출은 PCR 기반 키트와 RNA-시퀀싱 워크플로우의 조합이 28일간의 배양 대기를 대체할수록 11.71%의 연평균 복합 성장률(CAGR)을 나타냈습니다. PCR의 수용을 둘러싼 규제의 수렴은 특히 세포 치료 중간체의 채용을 가속합니다. 내독소 검사는 재조합형 팩터 C로 이행하고 있으며, 딱정벌레 용해액의 부족으로부터 공급을 분리해, 지속가능성을 높이고 있습니다. 첨단 바이러스 감지로 차세대 시퀀서에 대한 의존도가 증가하고 있으며 스폰서는 타임라인을 연장하지 않고 병원체 패널을 확장할 수 있습니다.

생물학적 안전성 시험 시장 보고서는 제품 및 서비스(제품 (시약, 키트, 기타), 서비스 (무균 시험 서비스, 기타)), 시험 유형(무균 시험, 바이오바덴 시험 등), 용도, 최종 사용자, 지역(북미, 유럽, 아시아태평양, 중동, 아프리카, 남미)에서 업계를 세분화합니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미는 FDA 규제의 엄격함, BARDA 조달, 주요 단일클론항체 제조업체의 존재에 힘입어 2024년에 세계 매출의 46.25%를 창출했습니다. 이 지역의 스폰서는 AI를 활용한 오염 위험 알고리즘을 시험적으로 도입하는 경우가 늘고 있으며, 소프트웨어 일체형 인큐베이터 수요를 뒷받침하고 있습니다. 유럽은 독일과 영국의 ATMP 과학 클러스터와 endotoxin 방법의 변화를 가속화하는 rFC의 약전 승인에서 이익을 얻고 있습니다. PFAS 규제의 소모품이 단계적 폐지에 직면하고 EU의 실험실이 대체품의 재인정을 강요받는 등 공급망에 스트레스가 발생하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 17.24%를 나타내 가장 높으며, 이는 중국의 대규모 CDMO 건설, 싱가포르의 세포 치료 혁신 허브, 일본의 수출 장벽을 완화하는 ISO에 준거한 PMDA 규칙이 뒷받침하고 있습니다. 현지 실험실은 FDA의 다지역 검사를 보장하고 낮은 비용 지점에서 신뢰성을 검증합니다. 그러나 지정학적 긴장과 BIOSECURE Act의 시행이 불투명하기 때문에 일부 스폰서들은 QC의 배치를 아시아와 국내의 거점으로 나누어 중복성을 확보하려고 하고 있습니다.

중동 및 아프리카와 남미는 아직 발전도상이지만 전략적인 지역입니다. 브라질과 사우디아라비아의 국립 백신 연구소는 세계 은행의 의료 안보 보조금의 지원을 받아 GMP 등급 무균 및 마이코플라스마 설비에 투자하고 있습니다. 제한된 숙련된 인력과 간헐적인 전력 공급이 속도를 제약하고 있지만, 지역 제조 자주성에 대한 장기적인 헌신은 QC 수요 증가를 지원합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 의약품 및 바이오테크놀러지 파이프라인의 성장과 벤처 자금 조달

- 첨단 치료제(ATMPs) 제조의 스케일업

- 바이러스·마이코플라스마 오염에 대한 규제 강화

- 비용 효율적인 QC 서비스를 요구하는 아시아 기반 CDMO에 아웃소싱 급증

- AI를 활용한 인실리코·바이오 세이프티·모델링이 배치 실패 리스크를 저감

- 생물 위협 대책 프로그램(BARDA, EU-HERA)이 검사 수요 촉진

- 시장 성장 억제요인

- 신규 래피드 마이크로법의 검증 사이클의 길이

- 유자격 바이오 세이프티 인재의 부족과 높은 트레이닝 비용

- 주요 제약 회사의 가격 압력에 의한 CRO 마진 압축

- 단회 사용 시약(HEPA, LAL)공급 체인 취약성

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측(단위 : 달러)

- 제품 및 서비스별

- 제품

- 시약 및 키트

- 기기

- 일회용 소모품

- 서비스

- 무균 시험 서비스

- 내독소 및 발열원 시험 서비스

- 세포주 진위 확인 및 특성 분석

- 제품

- 시험 유형별

- 무균 시험

- 생물부하 시험

- 내독소/LAL 시험

- 마이코플라스마 검출

- 외래 바이러스 검출

- 용도별

- 재조합 단백질/단일클론항체

- 백신 및 치료제

- 세포 및 유전자 치료

- 혈액 및 혈액 기반 치료

- 기타 용도

- 최종 사용자별

- 바이오제약 및 바이오테크 기업

- 계약 개발 및 제조 기관(CDMO)

- 학술 및 연구 기관

- 의료기기 제조업체

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Charles River Laboratories

- Lonza Group

- Thermo Fisher Scientific

- Merck KGaA(MilliporeSigma)

- Eurofins Scientific

- WuXi AppTec

- SGS SA

- bioMerieux SA

- Avance Biosciences

- Cytovance Biologics

- Toxikon(Labcorp)

- Nelson Labs

- Pacific BioLabs

- Steris PLC

- Pall Corporation(Danaher)

- Sartorius AG

- Promega Corporation

- Creative BioLabs

- Microbac Laboratories

- Alcami Corporation

제7장 시장 기회와 전망

KTH 25.10.27The Biological Safety Testing Market size is estimated at USD 4.54 billion in 2025, and is expected to reach USD 7.88 billion by 2030, at a CAGR of 11.63% during the forecast period (2025-2030).

Regulatory agencies now demand richer viral- and mycoplasma-safety datasets, while manufacturers scale up advanced therapy medicinal products (ATMPs) that require intensive contamination control. AI-enabled in-silico biosafety modelling is increasingly embedded in quality-control workflows, reducing batch-failure rates and trimming release times. Biothreat-preparedness spending from BARDA and EU-HERA has broadened demand beyond the traditional biopharma customer base. Outsourced quality control to Asia-based CDMOs, especially in China, is reshaping supply chains as laboratories there gain international accreditation.

Global Biological Safety Testing Market Trends and Insights

Growth in Global Pharma-Biotech Pipeline & Venture Funding

Deal flow across oncology, immunology, and gene therapy is setting record highs. Larger round sizes fund richer pre-clinical datasets, which in turn require extended biosafety test panels. Several start-ups, such as Aclid, raise seed capital earmarked for DNA-synthesis screening platforms that ease contamination risk, pushing volumes toward contract testing firms. The pipeline expansion particularly benefits contract testing organizations, as pharmaceutical companies increasingly outsource safety testing to specialized providers rather than maintaining in-house capabilities.

Scale-Up of Advanced Therapy Medicinal Products (ATMPs) Manufacturing

Guidance updates from the European Medicines Agency in 2024 and parallel FDA drafts are drawing ATMP producers toward expanded adventitious virus and cell-line authentication assays. Lonza's USD 1.2 billion site acquisition in Vacaville exemplifies the capital intensity needed to house such high-grade QC suites. The unique testing requirements for ATMPs, including adventitious virus detection and cellular characterization, create specialized market segments with higher margins and technical barriers to entry.

Lengthy Validation Cycles for Novel Rapid-Micro Methods

Despite FDA encouragement under its Process Analytical Technology framework, global validation still demands 18-24 months of side-by-side testing against compendial methods. Suppliers such as Rapid Micro Biosystems demonstrate 1- to 3-day sterility reads, yet sponsors maintain parallel legacy assays until regulatory comfort is proven.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Tightening on Viral & Mycoplasma Contamination

- Outsourcing Surge To Asia-Based CDMOs for Cost-Effective QC Services

- Shortage of Qualified Biosafety Personnel & High Training Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits captured 45.12% revenue in 2024, reflecting their consumable pull-through as test volumes expand across sterile injectables and ATMP release lots. The biological safety testing market size attributed to reagents grows in tandem with heightened contamination-screening frequency. Single-use filters and recombinant Factor C endotoxin vials dominate purchase orders, although PFAS-driven PVDF-filter phase-outs are spurring redesigns. Instrument sales advance at a 12.12% CAGR, powered by automated plate-reading systems, ddPCR analytics, and real-time incubation chambers. Vendors integrate AI modules that flag anomalies and pre-empt false positives, shrinking deviation investigations. Service revenues climb as pharma sponsors outsource sterility, endotoxin, and cell-line authentication to specialist labs, using bundled contracts that include sample logistics and data-integrity auditing. Rising ATMP pipelines further tilt spending toward bespoke adventitious-virus panels, which carry premium pricing.

Sterility assays accounted for a 32.69% biological safety testing market share in 2024, remaining a release-critical step for every parenteral batch. Incubation-based protocols still dominate submissions, yet continuous-monitoring systems such as BACT/ALERT shorten final approval windows. Mycoplasma detection logs the highest 11.71% CAGR as PCR-based kits and combined RNA-sequencing workflows replace 28-day culture waits. Regulatory convergence around PCR acceptance accelerates adoption, especially for cell-therapy intermediates. Endotoxin testing is migrating to recombinant Factor C, decoupling supply from horseshoe-crab lysate shortages and enhancing sustainability. Adventitious-virus detection relies increasingly on next-generation sequencing, allowing sponsors to widen pathogen panels without extending timelines.

The Biological Safety Testing Market Report Segments the Industry Into by Product & Service (Products [Reagents & Kits, and More], Services [Sterility Testing Services, and More]), Test Type (Sterility Tests, Bioburden Tests, and More), Application, End User, and Geography (North America, Europe, Asia-Pacific, Middle-East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 46.25% of global revenue in 2024, supported by FDA regulatory rigor, BARDA procurement, and the presence of major monoclonal-antibody producers. Sponsors in the region increasingly pilot AI-driven contamination-risk algorithms, propelling demand for software-integrated incubators. Europe follows, benefitting from ATMP science clusters across Germany and the United Kingdom and from pharmacopoeial acceptance of rFC, which accelerates endotoxin-method shifts. Supply-chain stress does arise, as PFAS-regulated consumables face looming phase-outs that compel EU labs to re-qualify alternatives.

Asia-Pacific posts the highest 17.24% CAGR to 2030, propelled by China's vast CDMO build-out, Singapore's cell-therapy innovation hubs, and Japan's ISO-aligned PMDA rules that ease export barriers. Local labs secure FDA multi-regional inspections, validating reliability at lower cost points. Still, geopolitical tensions and the pending BIOSECURE Act introduce uncertainty, pushing some sponsors to split QC placement between Asia and domestic sites for redundancy.

Middle East & Africa and South America remain nascent but strategic. National vaccine institutes in Brazil and Saudi Arabia invest in GMP-grade sterility and mycoplasma suites, supported by World Bank health-security grants. Limited skilled-personnel pools and intermittent power supply constrain pace, yet long-term commitments to regional manufacturing autonomy sustain incremental QC demand.

- Charles River

- Lonza Group

- Thermo Fisher Scientific

- Merck KGaA (MilliporeSigma)

- Eurofins

- WuXi App Tec

- SGS

- bioMerieux

- Avance Biosciences

- Cytovance Biologics

- Toxikon (Labcorp)

- Nelson Labs

- Pacific BioLabs

- STERIS

- Pall Corporation (Danaher)

- Sartorius

- Promega

- Creative BioLabs

- Microbac Laboratories

- Alcami

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growth in Global Pharma-Biotech Pipeline & Venture Funding

- 4.2.2 Scale-Up of Advanced Therapy Medicinal Products (ATMPs) Manufacturing

- 4.2.3 Regulatory Tightening on Viral & Mycoplasma Contamination

- 4.2.4 Outsourcing Surge To Asia-Based CDMOs for Cost-Effective QC Services

- 4.2.5 AI-Enabled In-Silico Biosafety Modelling Reduces Batch-Failure Risk

- 4.2.6 Biothreat Preparedness Programs (BARDA, EU-HERA) Elevating Testing Demand

- 4.3 Market Restraints

- 4.3.1 Lengthy Validation Cycles for Novel Rapid-Micro Methods

- 4.3.2 Shortage of Qualified Biosafety Personnel & High Training Costs

- 4.3.3 Price Pressure from Large Pharma Driving Margin Compression for CROs

- 4.3.4 Supply-Chain Fragility for Single-Use Reagents (HEPA, LAL)

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product & Service

- 5.1.1 Products

- 5.1.1.1 Reagents & Kits

- 5.1.1.2 Instruments

- 5.1.1.3 Single-use Consumables

- 5.1.2 Services

- 5.1.2.1 Sterility Testing Services

- 5.1.2.2 Endotoxin & Pyrogen Testing Services

- 5.1.2.3 Cell Line Authentication & Characterisation

- 5.1.1 Products

- 5.2 By Test Type

- 5.2.1 Sterility Tests

- 5.2.2 Bioburden Tests

- 5.2.3 Endotoxin/LAL Tests

- 5.2.4 Mycoplasma Detection

- 5.2.5 Adventitious Virus Detection

- 5.3 By Application

- 5.3.1 Recombinant Protein/Monoclonal Antibodies

- 5.3.2 Vaccine and Therapeutics

- 5.3.3 Cellular and Gene Therapy

- 5.3.4 Blood and Blood-based Therapy

- 5.3.5 Other Application

- 5.4 By End User

- 5.4.1 Biopharma & Biotech Companies

- 5.4.2 Contract Development & Manufacturing Organisations

- 5.4.3 Academic & Research Institutes

- 5.4.4 Medical Device Manufacturers

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Charles River Laboratories

- 6.3.2 Lonza Group

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Merck KGaA (MilliporeSigma)

- 6.3.5 Eurofins Scientific

- 6.3.6 WuXi AppTec

- 6.3.7 SGS SA

- 6.3.8 bioMerieux SA

- 6.3.9 Avance Biosciences

- 6.3.10 Cytovance Biologics

- 6.3.11 Toxikon (Labcorp)

- 6.3.12 Nelson Labs

- 6.3.13 Pacific BioLabs

- 6.3.14 Steris PLC

- 6.3.15 Pall Corporation (Danaher)

- 6.3.16 Sartorius AG

- 6.3.17 Promega Corporation

- 6.3.18 Creative BioLabs

- 6.3.19 Microbac Laboratories

- 6.3.20 Alcami Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment