|

시장보고서

상품코드

1836442

자동차 압력 센서 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Pressure Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

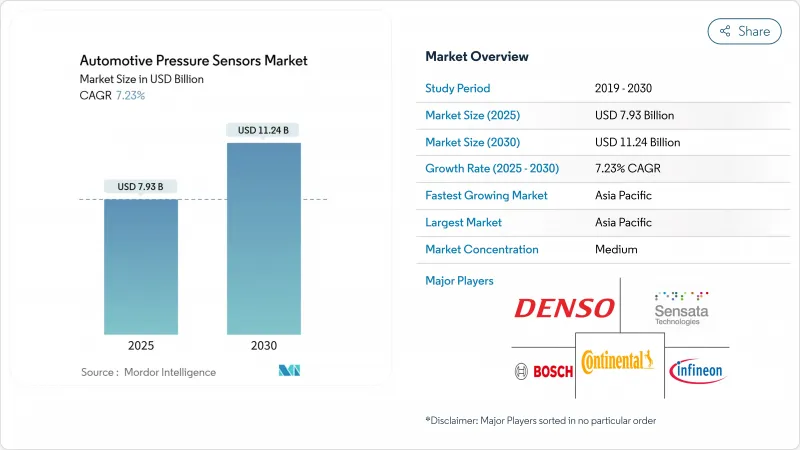

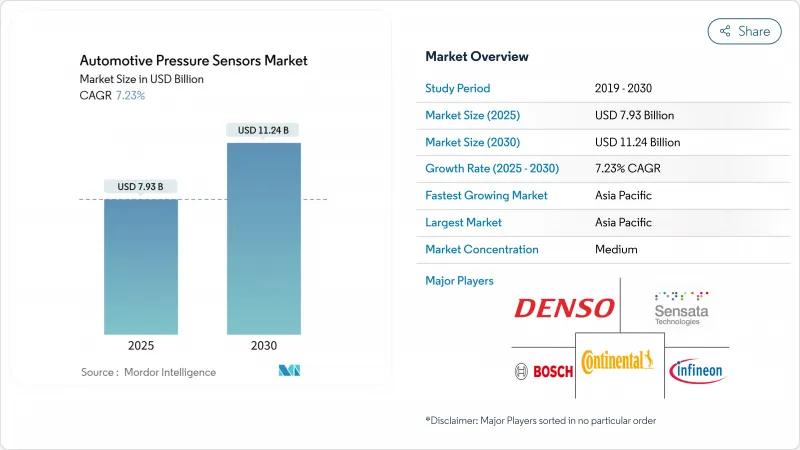

자동차 압력 센서 시장 규모는 2025년에 79억 3,000만 달러, 2030년에는 112억 4,000만 달러에 이를 것으로 예측되며, CAGR은 7.23%를 나타낼 전망입니다.

제조체가 기계식 게이지를 소프트웨어 정의 차량 플랫폼에 데이터를 공급하는 솔리드 스테이트 디바이스로 교체하면 견고한 수요가 발생합니다. 전기 추진, 자율 주행이 가능한 Brake-by-wire 시스템, 세계적으로 조화된 배출 가스 규제는 각각 차량당 더 많은 압력 노드를 요구하고 센서의 수량과 평균값을 모두 올리고 있습니다. 아시아태평양은 계속 생산 규모와 신에너지 차량의 전개로 페이스를 잡고 있는 한편, 유럽과 북미는 모든 신차 클래스의 타이어 공압 감시를 의무화하는 EU 일반 안전 규칙 II에 준거하기 위해 차량을 업그레이드하고 있습니다. 한편, 공급업체는 보다 고온의 배기 및 배터리 냉각수의 압력 저하를 견디는 탄화규소나 정전용량식 MEMS 설계에 투자하여 자동차 압력 센서 시장의 대응 가능 범위를 확대하고 있습니다.

세계의 자동차 압력 센서 시장 동향과 인사이트

정부에 의한 TPMS 장착 의무화

규제 당국은 현재 타이어 공압 데이터를 최전선 안전 정보로 취급하고 있습니다. 2024년 7월부터 EU 일반 안전 규정 II는 모든 신차 승용차, 버스, 트럭 및 트레일러에 TPMS를 장착할 것을 의무화했습니다. 미국에서는 이미 같은 의무화가 이루어지고 있으며, 남미와 동남아시아의 각국 정부도 이에 대응하는 규칙을 기초하고 있습니다. OEM은 의무화된 무선 백본을 활용하여 트레드 마모 분석 및 클라우드 경고를 거듭하고 센서의 가치를 높이고 사이버 보안 감사를 통과하는 암호화 프로토콜을 제공하는 공급업체를 선호합니다.

전동 파워트레인 생산 확대

배터리 전기 플랫폼은 냉각수 루프, Brake-by-wire 회로 및 밀폐 냉매 시스템에 여분의 압력 노드를 도입합니다. 정확한 피드백은 열 폭주를 방지하고 빠른 충전 온도 창을 최적화합니다. 중국 어셈블러는 모듈당 여러 개의 저압 MEMS 다이를 통합하지만 유럽의 고급 브랜드는 보다 강력한 전기 절연이 필요한 800 볼트 아키텍처로 전환합니다. 데이터 포인트 수가 증가함에 따라 수량과 복잡성이 모두 증가하고 자동차 압력 센서 시장에서 견고한 하드웨어와 팩 건강 알고리즘을 결합한 공급업체가 보상됩니다.

센서 가격 침식 및 마진 압력

자동차 제조업체는 매니폴드와 TPMS 게이지에 대해 매년 2-3%의 비용 절감을 협상하고 있지만 동남아시아의 위탁 파운드리은 성숙한 설계를 복제하여 마진을 압축하고 있습니다. 가격을 보호하기 위해 공급업체는 구독 수익을 창출하는 진단 및 예측 유지보수 API를 번들로 제공합니다. 그럼에도 불구하고 끊임없는 비용 절감 목표는 낭비 없는 패키징, 외부 위탁 테스트, 적극적인 다이 축소를 요구하고, 중소기업에 과제를 던져 자동차 압력 센서 시장의 단기 수익성을 약화시키고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- ADAS와 자율시스템의 통합 증가

- 세계적인 배출가스와 연비 규범의 엄격화

- 반도체 공급망의 불안정성

부문 분석

세계적인 생산 규모와 전기 추진으로의 급속한 변화를 반영하여 승용차가 도입 대수의 대부분을 차지하고 있습니다. 2024년 승용차 플랫폼은 자동차 압력 센서 시장 점유율의 65.18%를 차지했으며 2030년까지 연평균 복합 성장률(CAGR)은 8.15%를 나타낼 전망입니다. 고급 차량이 적응형 에어 서스펜션, 액티브 에어로 다이내믹스 및 예측 브레이크 서비스를 통합함에 따라 채용이 가속화됩니다. 전기 세단은 배터리 냉각 장치와 캐빈 히트 펌프에 저압 노드를 추가하여 차량당 센서 수를 늘립니다. 상용 밴과 소형 트럭은 대수에서는 후진을 숭배하고 있지만, 부하 모니터링과 회생 브레이크의 최적화를 요구하는 라스트 마일 딜리버리 플릿으로부터 주목을 받고 있습니다. 중형·대형 트럭은 EU의 새로운 인가로 TPMS의 의무화에 직면하고 있으며, 보다 가혹한 듀티 사이클로 활약하는 고레인지의 게이지에 박차가 걸려 있습니다. 자율주행화물의 조종사는 장애 조치 기준을 충족하기 위해 중복 압력 회로를 채택합니다. 그 결과, 자동차 클래스간에 다양한 제품을 제공함으로써 공급업체는 단일 부문의 주기적 연화를 헤지할 수 있어 자동차 압력 센서 시장의 지속적인 성장을 지원하고 있습니다.

두 번째 층의 성장은 유압 작업과 장기간의 의무로 인해 높은 내압 다이어프램에 대한 수요가 증가하는 특수 오프 하이웨이 차량에서 가져옵니다. 농업 기계는 토양 압축 관리를 위해 타이어의 공기압을 디지털 방식으로 제어하고 건설 기계는 유압의 건강 상태를 실시간으로 추적합니다. 이 센서에는 스테인레스 스틸 또는 세라믹 셀과 밀폐형 커넥터가 장착되어 있기 때문에 수량이 겸손해도 ASP가 상승합니다. 따라서 승용차의 리더십은 무거운 물체 응용 분야의 수익성이 높은 틈새 시장과 공존하여 자동차 압력 센서 산업의 전반적인 가치 획득을 풍부하게합니다.

타이어 공압 모니터링 시스템은 2024년 매출액의 39.25%를 차지하고 신규제 입구 역할을 굳혔습니다. 각 경차에는 4-6개의 휠 웰 센서가 탑재되어 프리미엄 장비에서는 5번째 예비 휠 유닛이 추가됩니다. 센서의 배터리 수명은 최대 10년이며 연금과 같은 애프터마켓이 형성되어 있습니다. 그러나 Euro 7에서는 지속적인 압력 피드백이 필요한 배기 가스 재순환, 미립자 트랩 및 SCR 투여 서브시스템에 대한 지출이 증가합니다. 이 배기 모듈은 CAGR로 가장 빠른 10.45%를 나타내며 일반적인 TPMS 장치의 2배의 ASP를 요구하는 고온 탄화규소 다이가 필요합니다. 브레이크와 ABS의 압력 감지는 안정적인 코어로 유지되지만 Brake-by-wire로의 전환은 분해능과 중복성을 향상시키고 장치 수를 증가시킵니다. 엔진 매니폴드, 연료 레일, 터보 부스트 센싱은 큰 압력 변동에 대해 보다 정밀하게 진화하고 전동화가 진행되어도 레거시 수요는 그대로 유지됩니다. 모든 대역폭에서 자동차 압력 센서 시장은 다양한 애플리케이션의 인수로부터 이익을 얻고 있으며, 컴플라이언스에 대한 투자는 단기적인 스파이크를 촉진하고 소프트웨어 지원 건전성 기능은 장기적인 수익을 창출합니다.

차량 내에서 스마트 에어백 모듈은 기압 정보를 활용하여 탑승자 분류를 개선합니다. 차세대 에어컨 제어는 EV에 대한 일반적인 히트 펌프의 냉매 충전량을 최적화하기 위해 증기 압축 모니터링을 활용합니다. 라이드 컨트롤 시스템은 10kHz의 고속 압력 픽업을 내장하고 세미 액티브 댐퍼를 조정합니다. 센서의 수가 늘어남에 따라 멀티플렉싱된 디지털 버스가 아날로그 라인을 대체하여 하네스의 무게를 단순화하고 신뢰성을 높입니다. 자동차 압력 센서 시장이 단일 목적 아날로그 게이지에서 중앙 집중식 도메인 컨트롤러에 공급하는 네트워크화된 디지털 노드로 계속 전환하고 있음을 이 범위의 확대는 뒷받침하고 있습니다.

자동차 압력 센서 시장 보고서는 차량 유형(승용차, 소형 상용차, 기타), 용도(타이어 공압 모니터링 시스템(TPMS), 기타), 압력 유형(절대압, 차압, 기타), 센서 기술(피에조 저항 MEMS, 기타), 판매 채널(OEM 장착, 애프터마켓), 지역별로 분류되어 있습니다. 시장 예측은 금액(달러)과 수량(단위)으로 제공됩니다.

지역 분석

아시아태평양은 자동차 압력 센서 시장의 볼륨 엔진으로 2024년에 49.66%의 점유율로 선도했습니다. 이 지역은 중국이 전기자동차 생산을 가속화하고 배터리 안전을 위해 여러 개의 저압 노드를 통합하기 때문에 2030년까지 연평균 복합 성장률(CAGR) 9.66%를 나타내거나 더 성장할 것으로 예측됩니다. 현지 제조업체는 MEMS의 국내 조달에 인센티브를 제공하는 국가 컨텐츠 의무화의 혜택을 받았으며 수입에 대한 의존도가 떨어지고 있습니다. 인도는 구자라트와 타밀 나두의 자동차 조립 클러스터를 확장하고 파워트레인 일렉트로닉스와 함께 지역 센서 공급망을 육성합니다. 일본은 마이크로 머시닝 툴의 리더십을 유지하고 세계 브랜드의 웨이퍼 제조 아웃소싱에 공급합니다. 스마트 이동성 실험실에 대한 정부 보조금은 지역 설계 사이클을 단축하고 경쟁력을 강화합니다.

북미에서는 규제에 의한 철수와 기술에 의한 뒷받침이 결합되어 있습니다. TPMS에 관한 NHTSA의 규칙과 EPA의 배기가스 기준이 기준선 수요를 확보하는 한편, 실리콘밸리의 소프트웨어 스택이 디지털 압력 프로토콜을 선호하는 집중형 도메인으로의 이행을 가속시킵니다. 디트로이트 OEM은 배터리 팩 조립 및 열 관리 통합을 현지화하여 국내 센서 수를 늘립니다. 캐나다의 대형 트럭 부문이 연비 향상을 위해 고정밀도의 타이어 공압 제어를 채용해, 센서의 사용이 직업용 용도에까지 확대. 멕시코 Tier-2 에코시스템은 성형 하우징과 리드프레임 스탬핑을 제공하여 자동차 압력 센서 시장 전체의 지역 비용 최적화를 지원합니다.

유럽의 정책 상황은 가장 엄격합니다. Euro 7에서는 실시간 배기 가스 모니터링이 의무화되어 SiC 고온 센서의 보급을 촉진하고 있습니다. 일반 안전 규정(General Safety Regulation)에서는 모든 차량 등급에서 TPMS 장착이 의무화되어 트레일러와 객차의 센서 밀도를 높이고 있습니다. 독일의 프리미엄 OEM은 레벨 3 자율 주행 허가를 위해 이중 중복 브레이크 압력 모듈을 지정. 프랑스와 이탈리아는 선진적인 배터리 냉각수 센싱을 통합한 전기 버스 프로젝트에 부흥 자금을 투입. 동유럽 공장은 새로운 MEMS 패키징 투자를 유치하고 공통 시장 내에 있으면서 경쟁력 있는 노동력을 활용하고 있습니다. 전반적으로 동조하는 규제와 정교한 최종 사용자가 자동차 압력 센서 시장의 장기 수요를 안정화시킵니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 정부에 의한 TPMS 장착 의무화

- 전동 파워트레인 생산 증가

- ADAS와 자율주행 시스템의 통합 증가

- 세계의 배기 가스·연비 규제의 강화

- SiC 베이스의 고온 센서가 배기측에서의 이용 사례를 개척

- OTA 예후 진단에는 자기 진단형 스마트 센서가 필요

- 시장 성장 억제요인

- 센서 가격 상승과 마진 압력

- 반도체 공급망 변동

- TPMS 신호 스푸핑에 의한 사이버 리스크

- 복잡한 복수 규격의 인증 부담

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측 : 금액(USD)·수량(유닛)

- 차량 유형별

- 승용차

- 소형 상용차

- 중대형 상용차

- 용도별

- 타이어 공기압 모니터링 시스템(TPMS)

- 브레이크 부스터 및 ABS

- 엔진 및 연료/매니폴드 관리

- 배기 가스 재순환/후처리

- 에어백 및 안전 구속 장치

- 차량 동역학 및 ESC

- 압력 유형별

- 절대압

- 게이지압(밀폐형/배기형)

- 차압

- 진공/저압

- 센서 기술별

- 압전 저항형 MEMS

- 정전 용량형 MEMS

- 공진형/쿼츠

- 광전자식 및 기타

- 판매 채널별

- OEM 장착형

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 이집트

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Robert Bosch GmbH

- Continental AG

- Sensata Technologies, Inc.

- DENSO Corporation

- Infineon Technologies AG

- STMicroelectronics NV

- NXP Semiconductors NV

- Texas Instruments Incorporated

- Autoliv Inc.

- Allegro MicroSystems, LLC

- TE Connectivity Ltd.

- Honeywell International Inc.

- Analog Devices, Inc.

- Melexis NV

- Aptiv PLC

- Amphenol Advanced Sensors

- Alps Alpine Co., Ltd.

- Bourns, Inc.

- Nidec-Copal Electronics

제7장 시장 기회와 전망

KTH 25.10.27The automotive pressure sensors market size was USD 7.93 billion in 2025 and is projected to reach USD 11.24 billion by 2030, reflecting a healthy 7.23% CAGR.

Robust demand arises as manufacturers replace mechanical gauges with solid-state devices that feed data into software-defined vehicle platforms. Electric propulsion, autonomous-ready brake-by-wire systems, and globally harmonized emission limits each call for more pressure nodes per vehicle, lifting both unit volumes and average sensor value. Asia-Pacific continues to set the pace in production scale and new-energy-vehicle rollouts, while Europe and North America upgrade fleets to comply with the EU General Safety Regulation II that obliges tire pressure monitoring on every new vehicle class . Meanwhile, suppliers invest in silicon-carbide and capacitive MEMS designs that survive hotter exhaust and lower battery-coolant pressures, expanding the total addressable scope of the automotive pressure sensors market.

Global Automotive Pressure Sensors Market Trends and Insights

Government Mandates for TPMS Fitment

Regulators now treat tire-pressure data as frontline safety information. From July 2024, the EU General Safety Regulation II requires TPMS on every new passenger car, bus, truck, and trailer . Comparable mandates already exist in the United States, while South American and Southeast Asian governments draft matching rules. OEMs exploit the mandatory wireless backbone to layer tread-wear analytics and cloud alerts, increasing sensor value, and they prefer vendors offering encrypted protocols that pass cybersecurity audits.

Escalating Electrified-Powertrain Production

Battery-electric platforms introduce extra pressure nodes in coolant loops, brake-by-wire circuits, and closed refrigerant systems; accurate feedback prevents thermal runaway and optimizes fast-charge temperature windows. Chinese assemblers embed several low-pressure MEMS dice per module, whereas European premium brands migrate to 800-volt architectures needing stronger electrical isolation. The growing datapoint count enlarges both volume and complexity, rewarding suppliers that marry robust hardware with pack-health algorithms inside the automotive pressure sensors market.

Sensor Price-Erosion and Margin Pressure

Automakers negotiate yearly 2-3% cost reductions on legacy manifold and TPMS gauges, while Southeast Asian contract foundries replicate mature designs, compressing margins. To defend pricing, suppliers bundle diagnostics and predictive-maintenance APIs that create subscription revenue. Nonetheless, relentless cost-down targets demand lean packaging, outsourced test, and aggressive die shrinks, challenging smaller firms and tempering short-term profitability inside the automotive pressure sensors market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Integration of ADAS and Autonomous Systems

- Stricter Global Emission and Fuel-Economy Norms

- Semiconductor Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars dominate deployments, reflecting both global production scale and the rapid shift toward electric propulsion. In 2024, passenger platforms held 65.18% of the automotive pressure sensors market share and are tracking an 8.15% CAGR to 2030. Adoption accelerates as luxury marques integrate adaptive air suspension, active aerodynamics, and predictive brake servicing. Electric sedans place additional low-pressure nodes in battery chillers and cabin heat pumps, expanding sensor counts per vehicle. Commercial vans and light trucks trail in volume yet attract attention from last-mile delivery fleets that demand load monitoring and regenerative braking optimization. Medium and heavy trucks face EU mandates for TPMS on new approvals, spurring higher-range gauges that thrive in harsher duty cycles. Autonomous freight pilots employ redundant pressure circuits to satisfy fail-operational criteria. Consequently, diversified offerings across vehicle classes allow suppliers to hedge cyclical softness in any single segment, supporting sustainable gains for the automotive pressure sensors market.

Second-tier growth comes from specialized off-highway vehicles where hydraulic workloads and extended duty drive demand for high-proof-pressure diaphragms. Agricultural machinery integrates digital tire inflation control for soil compaction management, while construction equipment adopts real-time hydraulic health tracking. Though unit volumes are modest, ASPs rise because these sensors pack stainless or ceramic cells and sealed connectors. Passenger car leadership therefore coexists with profitable niches in heavy applications, enriching the overall value capture of the automotive pressure sensors industry.

Tire pressure monitoring systems generated 39.25% of 2024 revenue, cementing their role as the entry point for new regulations. Each light vehicle carries four to six wheel-well sensors, and premium fitments add a fifth spare-wheel unit. Sensor batteries last up to 10 years, creating an annuity-like aftermarket. Yet Euro 7 shifts incremental expenditure toward exhaust gas recirculation, particulate trap, and SCR dosing subsystems that now need continuous pressure feedback. These exhaust modules post the fastest 10.45% CAGR and require high-temperature silicon-carbide dies that command double the ASP of common TPMS units. Brake and ABS pressure sensing remains a steady core, though migration to brake-by-wire introduces finer resolution and redundancy that raise device count. Engine manifold, fuel rail, and turbo boost sensing evolve toward higher accuracy at large pressure swings, keeping legacy demand intact even as electrification proceeds. Across every bandwidth, the automotive pressure sensors market benefits from diversified application pull, with compliance spend fueling near-term spikes and software-enabled health features creating longer-cycle revenue.

Inside the cabin, smart airbag modules employ barometric pressure information to improve occupant classification. Next-generation climate control leverages vapor-compression monitoring to optimize refrigerant charge in heat pumps common to EVs. Ride-control systems embed fast 10 kHz pressure pick-ups to regulate semi-active dampers. As sensor counts expand, multiplexed digital buses replace analog lines, simplifying harness weight and boosting reliability. The widening scope underlines how the automotive pressure sensors market continues to migrate from single-purpose analog gauges to networked digital nodes that feed centralized domain controllers.

The Automotive Pressure Sensors Market Report is Segmented by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Application (Tire Pressure Monitoring System (TPMS), and More), Pressure Type (Absolute, Differential, and More), Sensor Technology (Piezoresistive MEMS, and More), Sales Channel (OEM-Fitted and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific remains the volume engine for the automotive pressure sensors market, leading with 49.66% share in 2024. The region is further projected to grow with a 9.66% CAGR by 2030, as China accelerates electric-vehicle production and embeds multiple low-pressure nodes for battery safety. Local makers benefit from national content mandates that incentivize domestic MEMS sourcing, reducing import reliance. India scales automotive assembly clusters in Gujarat and Tamil Nadu, fostering regional sensor supply chains alongside powertrain electronics. Japan sustains leadership in micro-machining tools, feeding outsourced wafer fabrication for global brands, while South Korea leverages its consumer-electronics fabs to push sensor miniaturization. Government subsidies for smart mobility labs keep regional design cycles short, enhancing competitiveness.

North America combines regulatory pull with technology push. NHTSA rules on TPMS and EPA emission standards ensure baseline demand, while Silicon Valley software stacks accelerate the shift to centralized domains that favor digital pressure protocols. Detroit OEMs localize battery pack assembly and thermal management integration, increasing domestic sensor content. Canada's heavy-truck sector adopts high-accuracy tire inflation control for fuel-efficiency gains, extending sensor use into vocational applications. Mexico's Tier-2 ecosystem supplies molded housings and lead frame stampings, supporting regional cost optimization across the automotive pressure sensors market.

Europe's policy landscape is the most stringent. Euro 7 legislation forces real-time exhaust monitoring, driving uptake of SiC high-temperature sensors . The General Safety Regulation obliges TPMS on every vehicle class, elevating sensor density in trailers and coaches. Germany's premium OEMs specify dual-redundant brake pressure modules for Level-3 autonomous approval. France and Italy channel recovery funds into electric-bus projects that integrate advanced battery coolant sensing. Eastern European plants attract new MEMS packaging investments, exploiting competitive labor while staying inside the common market. Altogether, synchronized regulations and sophisticated end-users stabilize long-run demand across the automotive pressure sensors market.

- Robert Bosch GmbH

- Continental AG

- Sensata Technologies, Inc.

- DENSO Corporation

- Infineon Technologies AG

- STMicroelectronics N.V.

- NXP Semiconductors N.V.

- Texas Instruments Incorporated

- Autoliv Inc.

- Allegro MicroSystems, LLC

- TE Connectivity Ltd.

- Honeywell International Inc.

- Analog Devices, Inc.

- Melexis NV

- Aptiv PLC

- Amphenol Advanced Sensors

- Alps Alpine Co., Ltd.

- Bourns, Inc.

- Nidec-Copal Electronics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government mandates for TPMS fitment

- 4.2.2 Escalating electrified-powertrain production

- 4.2.3 Rising integration of ADAS and autonomous systems

- 4.2.4 Stricter global emission and fuel-economy norms

- 4.2.5 SiC-based high-temperature sensors open exhaust-side use-cases

- 4.2.6 OTA prognostics require self-diagnosing smart sensors

- 4.3 Market Restraints

- 4.3.1 Sensor price-erosion and margin pressure

- 4.3.2 Semiconductor supply-chain volatility

- 4.3.3 Cyber-risk of TPMS signal spoofing

- 4.3.4 Complex multi-standard certification burden

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.2 Light Commercial Vehicles

- 5.1.3 Medium and Heavy Commercial Vehicles

- 5.2 By Application

- 5.2.1 Tire Pressure Monitoring System (TPMS)

- 5.2.2 Brake Booster and ABS

- 5.2.3 Engine and Fuel/Manifold Management

- 5.2.4 Exhaust Gas Recirculation/After-treatment

- 5.2.5 Airbag and Safety Restraint Systems

- 5.2.6 Vehicle Dynamics and ESC

- 5.3 By Pressure Type

- 5.3.1 Absolute

- 5.3.2 Gauge (Sealed/Vent)

- 5.3.3 Differential

- 5.3.4 Vacuum/Low-pressure

- 5.4 By Sensor Technology

- 5.4.1 Piezoresistive MEMS

- 5.4.2 Capacitive MEMS

- 5.4.3 Resonant/Quartz

- 5.4.4 Opto-electronic and Others

- 5.5 By Sales Channel

- 5.5.1 OEM-Fitted

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Egypt

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Robert Bosch GmbH

- 6.4.2 Continental AG

- 6.4.3 Sensata Technologies, Inc.

- 6.4.4 DENSO Corporation

- 6.4.5 Infineon Technologies AG

- 6.4.6 STMicroelectronics N.V.

- 6.4.7 NXP Semiconductors N.V.

- 6.4.8 Texas Instruments Incorporated

- 6.4.9 Autoliv Inc.

- 6.4.10 Allegro MicroSystems, LLC

- 6.4.11 TE Connectivity Ltd.

- 6.4.12 Honeywell International Inc.

- 6.4.13 Analog Devices, Inc.

- 6.4.14 Melexis NV

- 6.4.15 Aptiv PLC

- 6.4.16 Amphenol Advanced Sensors

- 6.4.17 Alps Alpine Co., Ltd.

- 6.4.18 Bourns, Inc.

- 6.4.19 Nidec-Copal Electronics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment