|

시장보고서

상품코드

1836462

안과용 기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ophthalmic Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

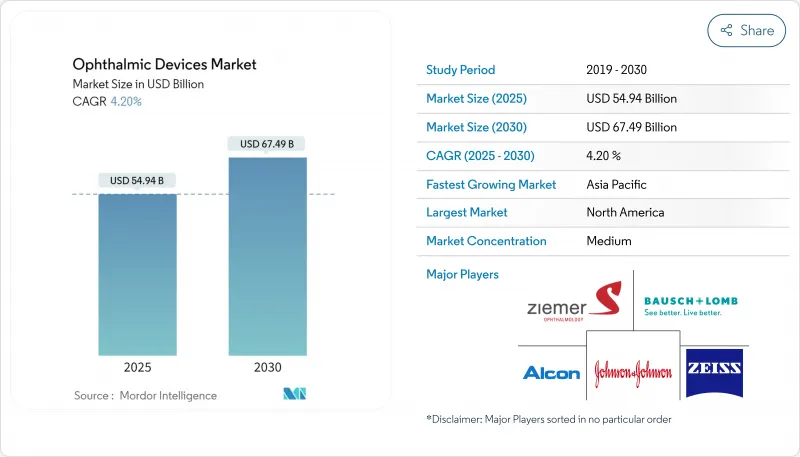

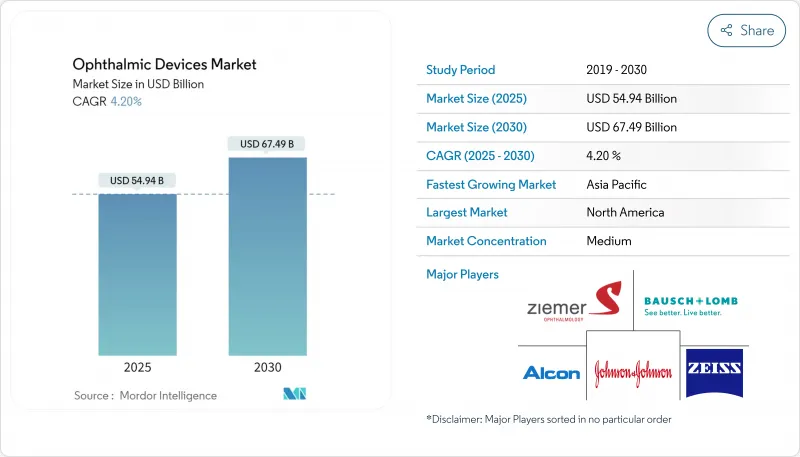

안과용 기기 시장은 2025년에 503억 5,000만 달러, 2030년에는 689억 8,000만 달러에 이르며, CAGR 6.53%를 나타낼 것으로 예측됩니다.

백내장 수술 건수 증가, 소아의 근시 증가, 진단 기기의 꾸준한 업그레이드가 가격 상한과 공급 충격을 능가하기 때문에 세계 수요는 견고함을 보이고 있습니다. 제조업체는 현재 라틴아메리카와 같은 입찰 주도 지역에서 마진을 보호하면서 단일 공급업체의 위험을 억제하기 위해 광학 및 전자 부품의 이중 조달 계약을 유지하고 있습니다. 주요 기업은 또한 제품 설계를 외래 환자의 우선순위(실적 축소, 회전 가속화, 통합 분석)에 맞추어 의료 현장이 제한된 수술 일정으로 더 많은 사례를 이동할 수 있도록 합니다. 정가보다 굴절 교정의 성과에 보답하는 새로운 상환 모델은 병원이 고급 안구 렌즈를 지정하도록 촉구하고, 안과용 기기 시장 전체에서 일시적인 자본 판매에서 연금 형식 소모품 및 서비스 계약으로의 수익 이행을 가속화하고 있습니다.

세계의 안과용 기기 시장 동향과 인사이트

근시유병률 증가와 고령화로 수요 증가

노안은 현재 추정 18억명에 영향을 미치고 있으며, 소아근시는 급격히 증가하고 있기 때문에 광학 개입에 대한 광범위하고 지속적인 수요곡선이 형성되고 있습니다. 국가의 의료 예산은 단발적인 아웃리치에서 영구적인 수술 인프라로 이동하고 있으며 공급업체는 Faco Console에 사례별 소모품을 번들하여 정기 수익을 보장하도록 촉구합니다. 동시에, 보호자는 ZEISS MyoCare와 같은 고급 근시 렌즈에 자금을 제공하고 정식 상환없이 기술 혁신을 추진하고 있습니다. 이 전략은 예방 광학을 둘러싼 가격 논의를 재구성하고 안과용 기기 시장에 지속적인 성장 추세를 제공합니다.

고급 백내장 수술 기술 채용 증가

백내장 환자의 약 40%는 현재 프리미엄 안구내 렌즈를 자기 부담하고 있으며, 지불자는 단초점 렌즈의 상환 상한을 검토하도록 촉구하고 있습니다. 병원은 존슨 엔드 존슨의 TECNIS Odyssey와 같은 벤치마크를 설정하고 굴절 교정의 치료 성적과 연관된 가치 기반 구매 계약을 협상하고 있습니다. 펨토 세컨드 플랫폼이 각막의 새로운 용도를 발견하면 공급자는 감가 상각비 회수를 가속화하고 보완적인 기기에 대한 자본 예산을 확대합니다. 이러한 역학은 프리미엄 렌즈의 업셀을 강화하고, 수술의 수익성을 확대하며, 안과용 기기 시장에서 제품의 점착성을 높입니다.

굴절 교정 수술에 영향을 미치는 소송과 규제 증가

7,500만 달러의 콘택트렌즈 독점 금지법에 관한 화해는 소비자의 가격 설정에 대한 엄격한 감시를 부각시켰습니다. 유통업체는 현재 동적 온라인 가격 조항을 요구하고 있으며 제조업체가 세계 최저 재판매 기준을 유지할 수 있는 능력을 복잡하게 하고 있습니다. 최근의 법적 해석으로 의약품과 기기의 병행 승인이 시작되고 일정이 연장됨에 따라 소규모 혁신자는 로열티를 부담하고 입증된 딜리버리 플랫폼 라이선스를 취득할 수밖에 없었습니다. 컴플라이언스 팀은 적응 가격 책정 소프트웨어 및 규제 당국과의 절충에 대한 투자를 실시하고, 연구 개발에서 자금을 빨아들이며, 안과용 기기 시장 전체의 단기적인 이익을 억제하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 원격 안과 의료에 의한 안과 의료에의 액세스 확대

- 프라이빗 주식 투자로 인프라 정비 추진

- 라틴아메리카의 불안정한 경제 상황과 가격 통제

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 근시 유병률의 상승과 고령화에 견인되는 수요의 확대

- 고급 백내장 수술 기술 채용 증가

- 원격 안과 의료에 의한 안과 의료에의 액세스 확대

- 인프라 정비를 추진하는 사모펀드 투자

- 세계 소아 시력 검사 프로그램의 정부 상환 프로그램

- 서유럽에서의 FLACS의 보급

- 시장 성장 억제요인

- 굴절 교정 수술에 영향을 미치는 소송과 규제 증가

- 라틴아메리카의 불안정한 경제 상황과 가격 통제

- 신흥 시장에서 높은 수입 관세와 제한된 수익성

- 유럽에서 클래스 IIb 안과 임플란트의 엄격한 MDR 문서화 비용

- 가치/공급망 분석

- 규제 전망

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액, 달러)

- 기기 유형별

- 진단 및 모니터링 기기

- OCT 스캐너

- 안저 및 망막 카메라

- 자동굴절계 및 각막경

- 각막 지형도 시스템

- 초음파 영상 시스템

- 시야계 및 안압계

- 기타 진단 및 모니터링 기기

- 수술용 기기

- 백내장 수술 기기

- 유리체망막 수술 기기

- 굴절 수술 기기

- 녹내장 수술 기기

- 기타 수술 기기

- 시력 관리 기기

- 안경테 및 렌즈

- 콘택트렌즈

- 진단 및 모니터링 기기

- 질병별

- 백내장

- 녹내장

- 당뇨병성 망막병증

- 기타 질환

- 최종 사용자별

- 병원

- 안과 전문 클리닉

- 외래수술센터(ASC)

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Alcon Inc.

- Johnson & Johnson Vision Care

- Lumibird Medical

- Bausch Lomb

- ZEISS Group

- HOYA

- Topcon Corporation

- Nidek Co., Ltd.

- HAAG-Streit Group

- Ziemer Ophthalmic Systems AG

- Glaukos Corporation

- STAAR Surgical

- Lumenis Be Ltd.

- CooperVision

- Heidelberg Engineering, Inc.

- Visionix

- Leica Microsystems

- Volk Optical

- OCULUS

제7장 시장 기회와 전망

KTH 25.10.27The ophthalmic devices market stands at USD 50.35 billion in 2025 and is forecast to reach USD 68.98 billion by 2030, advancing at a 6.53% CAGR.

Global demand shows resilience because rising cataract procedure volumes, growing myopia in children, and steady upgrades to diagnostic suites outweigh price caps and supply shocks. Manufacturers now maintain dual-sourcing contracts for optics and electronics to curb single-supplier risk while protecting margins in tender-driven regions such as Latin America. Leading companies also align product design with outpatient priorities-smaller footprints, faster turnover, and integrated analytics-so that care settings can move more cases through constrained operating schedules. New reimbursement models that reward refractive outcomes over list price further encourage hospitals to specify premium intraocular lenses, accelerating revenue migration from one-time capital sales to annuity-style consumables and service contracts across the ophthalmic devices market.

Global Ophthalmic Devices Market Trends and Insights

Growing Demand Driven by Increased Myopia Prevalence and Aging Populations

Presbyopia now affects an estimated 1.8 billion people, while childhood myopia climbs sharply, creating a broad and sustained demand curve for optical interventions. National health budgets are shifting from episodic outreach to permanent surgical infrastructure, prompting suppliers to bundle phaco consoles with per-case consumables and lock in recurring revenue. Simultaneously, parents fund premium myopia-control lenses such as ZEISS MyoCare, pushing innovation even in the absence of formal reimbursement. The strategy reshapes pricing discussions around preventive optics and gives the ophthalmic devices market durable growth momentum.

Increased Adoption of Advanced Cataract Surgery Techniques

Roughly 40% of cataract patients now self-pay for premium intraocular lenses, nudging payers to revisit monofocal reimbursement ceilings. Hospitals negotiate value-based purchasing contracts tied to refractive outcomes, setting benchmarks like Johnson & Johnson's TECNIS Odyssey, which reports minimal visual disturbances in 93% of recipients. As femtosecond platforms find additional corneal applications, providers accelerate depreciation recovery, enlarging capital budgets for complementary devices. These dynamics strengthen premium lens upselling, expand procedure profitability, and deepen product stickiness in the ophthalmic devices market.

Increased Litigation and Regulation Impacting Refractive Procedures

The USD 75 million contact-lens antitrust settlement highlights tougher oversight of consumer pricing. Distributors now demand dynamic online pricing clauses, complicating manufacturers' ability to sustain global minimum resale thresholds. Parallel drug-device approvals, triggered by recent legal interpretations, extend timelines, forcing smaller innovators to license proven delivery platforms at the cost of royalties. Compliance teams implement adaptive pricing software and regulatory-affairs investments, siphoning capital from R&D and tempering near-term gains across the ophthalmic devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Access to Eye Care through Tele-ophthalmology

- Private Equity Investment Driving Infrastructure Upgrades

- Volatile Economic Conditions and Price Controls in Latin America

For complete list of drivers and restraints, kindly check the Table Of Contents.

List of Companies Covered in this Report:

- Alcon

- Johnson & Johnson Vision Care

- Lumibird Medical

- Bausch + Lomb

- Carl Zeiss

- HOYA

- Topcon

- Nidek

- HAAG-Streit

- Ziemer Group

- Glaukos

- STAAR Surgical

- Lumenis

- The Cooper Companies

- Heidelberg Engineering, Inc.

- Visionix

- Danaher

- Volk Optical

- Oculus

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand Driven by Increased Myopia Prevalence and Aging Populations

- 4.2.2 Increased Adoption of Advanced Cataract Surgery Techniques

- 4.2.3 Expansion of Access to Eye Care through Tele-ophthalmology

- 4.2.4 Private Equity Investment Driving Infrastructure Upgrades

- 4.2.5 Government-Reimbursed Pediatric Vision Screening Programs Worldwide

- 4.2.6 Uptake of FLACS in Western Europe

- 4.3 Market Restraints

- 4.3.1 Increased Litigation and Regulation Impacting Refractive Procedures

- 4.3.2 Volatile Economic Conditions and Price Controls in Latin America

- 4.3.3 High Import Duties and Limited Profitability in Emerging Markets

- 4.3.4 Stringent MDR Documentation Costs for Class-IIb Ophthalmic Implants in Europe

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Device Type

- 5.1.1 Diagnostic & Monitoring Devices

- 5.1.1.1 OCT Scanners

- 5.1.1.2 Fundus & Retinal Cameras

- 5.1.1.3 Autorefractors & Keratometers

- 5.1.1.4 Corneal Topography Systems

- 5.1.1.5 Ultrasound Imaging Systems

- 5.1.1.6 Perimeters & Tonometers

- 5.1.1.7 Other Diagnostic & Monitoring Devices

- 5.1.2 Surgical Devices

- 5.1.2.1 Cataract Surgical Devices

- 5.1.2.2 Vitreoretinal Surgical Devices

- 5.1.2.3 Refreactive Surgical Devices

- 5.1.2.4 Glaucoma Surgical Devices

- 5.1.2.5 Other Surgical Devices

- 5.1.3 Vision Care Devices

- 5.1.3.1 Spectacles Frames & Lenses

- 5.1.3.2 Contact Lenses

- 5.1.1 Diagnostic & Monitoring Devices

- 5.2 By Disease Indication

- 5.2.1 Cataract

- 5.2.2 Glaucoma

- 5.2.3 Diabetic Retinopathy

- 5.2.4 Other Disease Indications

- 5.3 By End-user

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Ambulatory Surgery Centers (ASCs)

- 5.3.4 Other End-users

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Alcon Inc.

- 6.4.2 Johnson & Johnson Vision Care

- 6.4.3 Lumibird Medical

- 6.4.4 Bausch + Lomb

- 6.4.5 ZEISS Group

- 6.4.6 HOYA

- 6.4.7 Topcon Corporation

- 6.4.8 Nidek Co., Ltd.

- 6.4.9 HAAG-Streit Group

- 6.4.10 Ziemer Ophthalmic Systems AG

- 6.4.11 Glaukos Corporation

- 6.4.12 STAAR Surgical

- 6.4.13 Lumenis Be Ltd.

- 6.4.14 CooperVision

- 6.4.15 Heidelberg Engineering, Inc.

- 6.4.16 Visionix

- 6.4.17 Leica Microsystems

- 6.4.18 Volk Optical

- 6.4.19 OCULUS

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment