|

시장보고서

상품코드

1836482

북미의 자동차 에어필터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)North America Automotive Airfilters - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

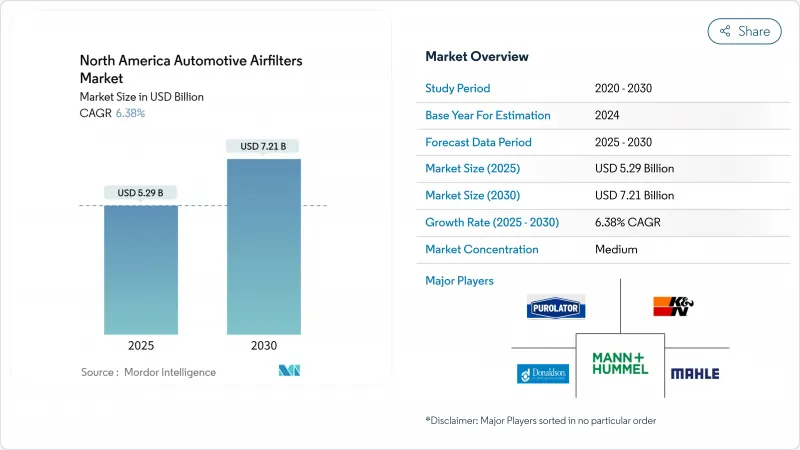

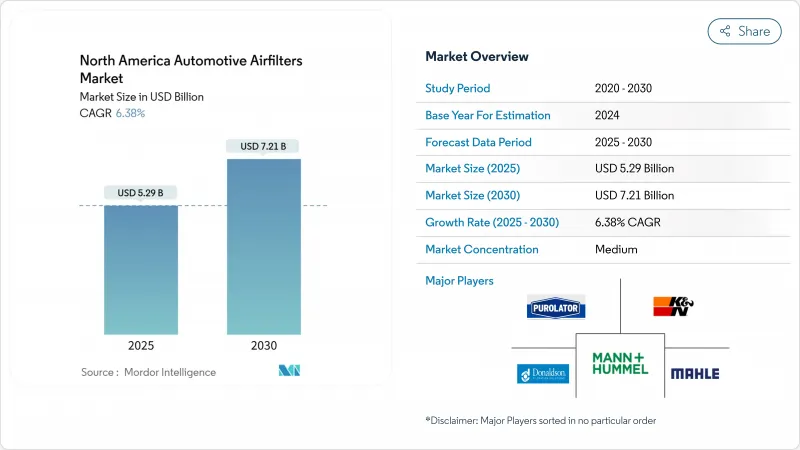

북미의 자동차 에어필터 시장은 2025년에 52억 9,000만 달러를 창출하고, 2030년에는 72억 1,000만 달러에 이를 것으로 예측되며, CAGR은 6.38%를 나타낼 전망입니다.

북미 자동차 에어필터 시장의 꾸준한 확대를 뒷받침하는 것은 노후화된 차량으로부터의 왕성한 교환 수요, 미국과 캐나다의 입자상 물질 규제와 NOx 규제의 강화, 프리미엄 캐빈 필터로의 이행입니다. 산불의 연기, 도시의 스모그, 장시간에 걸친 매일의 통근에 의해 여과가 유지관리의 잡용으로부터 건강 보호로 바뀌었기 때문에 캐빈 필터가 현재, 대수의 대부분을 차지하고 있습니다. 규제 당국이 공기 흐름을 악화시키지 않고 여과 효율을 높일 것을 요구하는 가운데, 나노섬유 미디어의 채용이 가속화되고 있는 한편, 온라인 소매는 소비자에게 투명한 가격 설정과 선택지를 제공하는 것으로, 시장에의 루트 투 마켓의 경제성을 재구축하고 있습니다. 동시에, 배터리 전기자동차의 점유율이 상승하고 장기적인 엔진 흡입 필터의 수량이 감소하기 때문에 공급업체는 북미의 자동차 에어필터 시장에서 HEPA 캐빈, 온도 관리, 스마트 센서 제품으로 축발을 옮길 수밖에 없습니다.

북미의 자동차 에어필터 시장 동향과 인사이트

미국과 캐나다의 PM과 NOx 배출 규제 강화가 필터 업그레이드 사이클을 촉진

2024년 12월에 승인된 캘리포니아의 Advanced Clean Cars II의 면제는 지역 기준을 더욱 엄격히 하고 늦게 북미의 자동차 에어필터 시장에 파급되었습니다. 나노섬유 복합재료는 보다 낮은 압력 손실로 필요한 포착 효율을 실현하고 연비를 유지함으로써 이익을 얻는다. PM2.5 규제가 9µg/m3로 엄격해지는 가운데 여과 성능을 증명할 수 있는 공급자는 가격 결정력을 확보할 수 있지만, 종래의 셀룰로오스 제품 라인은 마진의 압축에 시달립니다. 2027년부터 적용되는 헤비 듀티 기준은 내구성과 보증 임계값을 높이고 라이트 듀티 구매자에게 긴 수명 필터를 기본 가치로 인식하고 북미 자동차 에어필터 시장의 프리미엄층을 강화할 것으로 예상됩니다.

산불 후 급속한 캐빈 에어 품질 인식

2024년 기록적인 산불 연기가 몇 주 동안 캘리포니아, 오레곤, 브리티시컬럼비아 주를 덮고 미립자 물질의 측정치가 건강 경보 기준치를 웃돌아 HEPA 등급 캐빈 필터에 대한 소비자 수요에 불이 붙었습니다. 같은 생각이 차도에도 파급하고 있습니다. 통근객은 차를 구르는 쉼터로 취급하여 바이러스, 알레르겐, 연기 제거를 구한 필터를 요구합니다. 대중용 OEM은 과거에는 고급 트림에 한정되어 있던 다층 캐빈 카트리지를 제공함으로써 이것에 응해, 애프터마켓 각사는 구 모델용의 후부 키트를 패키지화하고 있습니다. 판촉 캠페인은 세계보건기구(WHO)의 PM2.5 지침과 어린이 호흡기 시스템의 건강을 강조하고 프리미엄 업셀을 정당화합니다. 내비게이션 앱이 연기 맵을 오버레이하고, 드라이버가 재순환을 활성화하고, 필터 교환을 상기시켜 피드백 루프를 향상시킵니다. 캐빈 미디어는 북미 자동차 에어필터 시장의 중심 존재입니다.

긴 수명을 씻을 수 있는 코튼 거즈 필터가 교환품과 공식

퍼포먼스 브랜드가 판매하는 재사용 가능한 코튼 거즈 필터는 서비스 수명을 12개월에서 5년 가까이 연장하고 있습니다. 매니아는 공기 흐름의 향상과 지속가능성의 메시지를 높이 평가하고 있으며, 특히 사막 지역에서는 전통적으로 먼지를 위해 자주 교환해야합니다. 소매업체는 50,000마일 보증과 평생 비용 절감을 강조하고 기존의 종이 라인에서 가치를 벗어났습니다. 메인스트림으로의 도입은 고가의 초기 비용과 매스 에어플로우 센서를 오염시킬 수 있는 귀찮은 오일 재충전 공정에 의해 제한된 채로 있습니다. 그럼에도 불구하고, 북미 자동차 에어필터 시장의 애프터마켓 부문에서는 약간의 전환율로도 수량이 깎여지고 있습니다. 제조업체 각사는 항균 라이닝을 실시한 세정 가능한 드롭 인식 캐빈 필터를 발매하는 것으로 대항해, 순환형 경제의 목표에 따라 수익을 회복하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 전용 HEPA 캐빈 필터를 채용하는 EV/HV 플랫폼

- IoT 대응 스마트 필터와 교환 예측 앱의 통합

- BEV의 채용에 의해 2035년까지 엔진 흡기 필터 수요 감소

부문 분석

규제 당국이 PM2.5의 포착에 주력하고 있기 때문에 나노섬유 복합재료는 2024년 CAGR이 8.30%를 나타내 어느 재료보다 빨랐습다. 종이/셀룰로오스는 여전히 북미 자동차 에어필터 시장의 43.25%를 나타내고 있지만, 종이와 셀룰로오스는 공기 흐름을 방해하는 주름을 두껍게 하지 않고 새로운 효율 목표를 달성하기 위해 노력하고 있습니다. 일렉트로스판 나노섬유는 저압력 손실로 300-500nm 입자를 99.9998% 제거합니다. 공급업체는 비용을 줄이고 기존 생산 라인을 사용하기 위해 나노 섬유 코팅과 셀룰로오스 점수를 혼합합니다. 식물 유래 폴리머와 재생 셀룰로오스는 OEM이 탄소 중립적인 공급망을 추구하면서 연구 개발 자금을 모으고 있습니다. 그래핀 산화물로 강화된 셀룰로오스 나노섬유는 토양에서 생분해하면서 실험실 시험에서 99.98%의 포착률을 달성하여 미래의 주류 전개에 대한 경로를 나타냈습니다.

폴리프로필렌과 펄프의 가격 변동은 헤지 전략이 약한 중소기업들에게 더해지며, 수탁 제조 및 특수 틈새 분야로의 진출을 강요합니다. 펄프 공장과 수지 공장을 갖춘 수직 통합형 다국적 기업은 비용면에서 유리하며, 멜트블로운, 스펀본드, 일렉트로스팬층을 혼합한 하이브리드 스택을 시험할 수 있습니다. 2025년부터 2030년에 걸쳐 나노섬유의 채용이 터보 가솔린 SUV에서 소형 상용밴으로 점차 진행되어 10년 후까지는 나노섬유가 차지하는 북미의 자동차 에어필터 시장 규모가 1자리대에서 10자리대 중반으로 확대됩니다.

캐빈필터는 이미 매출의 55.10%를 차지하고 있습니다. 북미의 자동차 에어필터 시장에 있어서, 쾌적성 기능이 구동계 부품을 웃도는 드문 예입니다. 캐빈 유닛은 CAGR 7.50%를 나타내, 산불 연기, 유행, HEPA의 위치가 뒷받침됩니다. 엔진 필터는 판매되는 내연 기관차에 여전히 필수적이지만 BEV 규모가 확대됨에 따라 점검 간격이 길어지고 수량도 점차 감소합니다. 미국 에너지부의 조사는 공기청정기의 에너지계수를 설정하고 간접적으로 자동차기술자를 보다 높은 CADR(청정공기 공급률) 목표로 향하게 합니다. 자동차 캐빈은 가정용 공기 청정기의 마케팅 언어를 복사합니다. 다층 미립자 탄소 항균 스택, 스마트폰 제어 재순환, LED 수명 표시 등입니다. 공급업체는 활성탄에 구리 이온과 은 이온을 함침시켜 차별화를 도모하고 몇 분 이내의 바이러스 불활성화를 약속하고 있습니다. 이 기술 변화는 캐빈 필터를 북미 자동차 에어필터 시장의 경제 성장 엔진으로 확고하게 합니다.

HEPA와 관련된 화려함과는 반대로, 양판차에는 비용의 상한을 만족하는 미립자만의 캐빈 필터가 탑재되고 있습니다. 그 갭을 메우는 것이 애프터마켓이며, 2025년에 온라인으로 판매되는 교환용 캐빈 필터의 30%는 카본 또는 HEPA로 업그레이드 되고 있습니다. 그 결과, 판매자는 평균 판매 가격이 상승하는 반면, 수량 구성이 변화하고 BEV가 엔진 필터를 제거해도 마진 공헌이 향상되는 것을 목격합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 미국과 캐나다에서 PM과 NOx 배출 규제 강화(EPA Tier-3, CARB LEV III)

- 산 불사 후의 급속한 차내 공기 공기질 인식

- 12.5년 이상 경과한 경차의 노후화가 애프터마켓 수요 확대

- 전용 HEPA 캐빈 필터를 채용하는 EV/HV 플랫폼

- IoT 대응 스마트 필터와 교환 예측 앱의 통합

- 터보 가솔린 SUV용 저 마찰 나노 화이버 엔진 미디어로의 OEM 변화

- 시장 성장 억제요인

- 긴 수명의 세탁 가능한 코튼 거즈제 필터가 교환 수요 잠식

- BEV의 보급에 의해 2035년경 엔진 흡기 필터 수요 소멸

- 폴리프로필렌과 셀룰로오스 펄프의 가격 변동이 마진 압박

- E-Commerce 필터의 모방품의 만연에 의한 브랜드 점유율의 저하

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 재료 유형별

- 종이/셀룰로오스

- 합성 거즈/면

- 폼

- 나노섬유 복합재

- 기타 활동(활성탄, 금속 메쉬)

- 필터 유형별

- 흡기(엔진) 에어필터

- 실내 에어필터

- 차종별

- 승용차

- 소형 상용차(LCV)

- 중대형 상용차(MHCV)

- 판매 채널별

- OEM

- 애프터마켓

- 독립계 애프터마켓

- 공인 서비스 센터

- 온라인 소매

- 국가별

- 미국

- 캐나다

- 멕시코

- 기타 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Mann Hummel

- Donaldson Company

- Purolator Filters LLC

- K&N Engineering

- AIRAID(Truck Hero)

- S&B Filters Inc.

- Mahle GmbH

- Bosch Automotive Aftermarket

- Denso Corporation

- Cummins Filtration

- Fram Group

- Clarcor(Part of Parker-Hannifin)

- ACDelco(GM)

- AFE Power

- Wix Filters

- Sogefi Group

- H&V(Engineered Media)

- Roki Co., Ltd.

- Champion Laboratories

- Luber-finer

제7장 시장 기회와 전망

KTH 25.10.27The North America Automotive Air Filters market generated USD 5.29 billion in 2025 and is forecast to climb to USD 7.21 billion by 2030, advancing at a 6.38% CAGR.

Robust replacement demand from an ageing vehicle parc, tightening U.S.-Canada particulate and NOx limits, and migration toward premium cabin filtration underpin this steady expansion of the North America automotive air filters market. Cabin filters now dominate unit volumes because wildfire smoke episodes, urban smog, and prolonged daily commutes convert filtration from a maintenance chore into a health safeguard. Nanofiber media adoption accelerates as regulators press for higher filtration efficiency without airflow penalties, while online retail reshapes route-to-market economics by giving consumers transparent pricing and choice. At the same time, the rising share of battery electric vehicles erodes long-term engine-intake filter volumes, forcing suppliers to pivot toward HEPA cabin, thermal-management, and smart-sensor products within the North American automotive air filters market.

North America Automotive Airfilters Market Trends and Insights

Stricter U.S.-Canada PM & NOx Emission Norms Drive Filter Upgrade Cycles

U.S. EPA light- and medium-duty standards for model years 2027-2032 push fleet average CO2 targets to 85 g/mile, compelling automakers to specify higher-efficiency engines and cabin media that capture finer particulates without throttling airflow.California's Advanced Clean Cars II waiver, approved in December 2024, further tightens regional benchmarks that sooner or later cascade across the North American automotive air filters market. Nanofiber composites benefit by delivering the required capture efficiency with lower pressure drop, preserving fuel economy. Suppliers capable of documenting filtration performance under the tougher PM2.5 limit of 9 µg/m3 secure pricing power, whereas legacy cellulose lines suffer margin compression. Heavy-duty standards effective from 2027 raise durability and warranty thresholds, nudging light-duty buyers to perceive long-life filters as baseline value, reinforcing premium tiers within the North America automotive air filters market.

Rapid Cabin-Air Quality Awareness Post-Wildfire Seasons

Record wildfire smoke in 2024 blanketed California, Oregon, and British Columbia for weeks, pushing particulate readings above health-alert thresholds and igniting consumer demand for HEPA-grade cabin filters. State policy reviews now mandate high-efficiency filtration for buildings exposed to smoke plumes.That same mindset spills onto driveways: commuters treat vehicles as rolling shelters and seek filters with viral, allergen, and smoke removal claims. Mass-market OEMs respond by offering multi-layer cabin cartridges once limited to luxury trims, while aftermarket players package retrofit kits for older models. Promotional campaigns highlight World Health Organization PM2.5 guidance and children's respiratory health to justify a premium upsell. The feedback loop tightens as navigation apps overlay smoke maps, nudging drivers to activate recirculation and reminding them to change filters. This human-health narrative cements Cabin Media as the North American automotive air filter market's heartbeat.

Long-Life Washable Cotton Gauze Filters Cannibalizing Replacements

Reusable cotton-gauze filters marketed by performance brands extend service life from 12 months to nearly 5 years. Enthusiasts appreciate airflow gains and sustainability messaging, especially in desert states where dust traditionally forces frequent swaps. Retailers emphasize 50,000-mile warranties and lifetime cost savings, pulling value away from conventional paper lines. Mainstream uptake remains capped by a higher upfront price and the messy oil-recharge process that can foul mass-airflow sensors. Nevertheless, even modest conversion rates shave volumes in the aftermarket segment of the North America automotive air filters market. Manufacturers counter by launching drop-in washable cabin filters with antimicrobial linings, recapturing revenue while aligning with circular-economy goals.

Other drivers and restraints analyzed in the detailed report include:

- EV/HV Platforms Adopting Dedicated HEPA Cabin Filters

- Integration of IoT-Enabled Smart Filters With Predictive Replacement Apps

- BEV Adoption: Eliminating Engine-Intake Filter Demand By 2035

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nanofiber composites held a modest slice in 2024 yet are on course for 8.30% CAGR, the fastest of any material, as regulators focus on PM2.5 capture. While Paper/Cellulose still accounts for 43.25% of the North American automotive air filters market, paper and cellulose struggle to meet new efficiency targets without thickening pleats that choke airflow. Electrospun nanofibers remove 99.9998% of 300-500 nm particles at low pressure drop, a metric validated in Macromolecular Materials and Engineering studies. Suppliers blend nanofiber coatings with cellulose cores to keep costs palatable and to use existing production lines. Sustainability pressures add complexity: plant-based polymers and recycled cellulose draw R&D funding as OEMs pursue carbon-neutral supply chains. Graphene-oxide-reinforced cellulose nanofibers delivered 99.98% capture in laboratory tests while biodegrading in soil, signaling pathways for future mainstream deployment.

Price volatility in polypropylene and pulp hampers smaller firms with weak hedging strategies, pushing them toward contract manufacturing or specialty niches. Vertically integrated multinationals with pulp plantations and resin plants enjoy cost leverage and can experiment with hybrid stacks mixing melt-blown, spunbond and electrospun layers. Over 2025-2030, nanofiber adoption trickles down from turbo-gasoline SUVs into light commercial vans, raising the North America automotive air filters market size captured by the material from single digits to mid-teens by decade's end.

Cabin filters already control 55.10% of revenue. They are fighting engine-intake filters for every incremental dollar, a rare instance where a comfort feature outranks a drivetrain component in the North America automotive air filters market. Cabin units grow 7.50% CAGR, boosted by wildfire smoke, pandemics, and HEPA positioning. Engine filters remain essential for sold internal-combustion vehicles but confront longer service intervals and gradual volume attrition as BEVs scale. Research from the U.S. Department of Energy sets energy factors for air cleaners, indirectly nudging automotive engineers toward higher CADR (clean air delivery rate) targets. Automotive cabins copy home-air-purifier marketing language: multi-layer particulate-carbon-antimicrobial stacks, smartphone-controlled recirculation, and LED life indicators. Suppliers differentiate by impregnating activated carbon with copper or silver ions, promising viral inactivation within minutes, a claim validated by ISO 18184 tests. This technology shift cements cabin filters as the North America automotive air filter market's economic growth engine.

Despite the glamour around HEPA, mass-market vehicles continue to ship with particulate-only cabin filters that comply with cost ceilings. The aftermarket fills the gap: 30% of replacement cabin filters sold online in 2025 carry carbon or HEPA upgrades. As a result, distributors watch average selling price climb while the volume mix changes, improving margin contribution even as BEVs delete engine filters.

The North America Automotive Air Filters Market is Segmented by Material Type (Paper / Cellulose, Synthetic Gauze / Cotton, and More), Filter Type (Intake Filters and Cabin Filters), by Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Sales Channel (OEMs and Aftermarket) and Country (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Mann+Hummel

- Donaldson Company

- Purolator Filters LLC

- K&N Engineering

- AIRAID (Truck Hero)

- S&B Filters Inc.

- Mahle GmbH

- Bosch Automotive Aftermarket

- Denso Corporation

- Cummins Filtration

- Fram Group

- Clarcor (Part of Parker-Hannifin)

- ACDelco (GM)

- AFE Power

- Wix Filters

- Sogefi Group

- H&V (Engineered Media)

- Roki Co., Ltd.

- Champion Laboratories

- Luber-finer

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter U.S.-Canada PM & NOx emission norms (EPA Tier-3, CARB LEV III)

- 4.2.2 Rapid cabin-air quality awareness post-wildfire seasons

- 4.2.3 Ageing light-vehicle parc greater than 12.5 yrs fueling aftermarket volumes

- 4.2.4 EV/HV platforms adopting dedicated HEPA cabin filters

- 4.2.5 Integration of IoT-enabled smart filters with predictive replacement apps

- 4.2.6 OEM shift toward low-restriction nanofiber engine media for turbo-gasoline SUVs

- 4.3 Market Restraints

- 4.3.1 Long-life washable cotton gauze filters cannibalising replacements

- 4.3.2 BEV adoption eliminating engine-intake filter demand by ~2035

- 4.3.3 Polypropylene & cellulose pulp price volatility squeezing margins

- 4.3.4 Proliferation of counterfeit e-commerce filters undermining branded share

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Material Type

- 5.1.1 Paper/Cellulose

- 5.1.2 Synthetic Gauze/Cotton

- 5.1.3 Foam

- 5.1.4 Nanofiber Composite

- 5.1.5 Others (Activated Carbon, Metal Mesh)

- 5.2 By Filter Type

- 5.2.1 Intake (Engine) Air Filters

- 5.2.2 Cabin Air Filters

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles (LCV)

- 5.3.3 Medium and Heavy Commercial Vehicles (MHCV)

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.4.2.1 Independent Aftermarket

- 5.4.2.2 Authorized Service Centers

- 5.4.2.3 Online Retail

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

- 5.5.4 Rest of North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Mann+Hummel

- 6.4.2 Donaldson Company

- 6.4.3 Purolator Filters LLC

- 6.4.4 K&N Engineering

- 6.4.5 AIRAID (Truck Hero)

- 6.4.6 S&B Filters Inc.

- 6.4.7 Mahle GmbH

- 6.4.8 Bosch Automotive Aftermarket

- 6.4.9 Denso Corporation

- 6.4.10 Cummins Filtration

- 6.4.11 Fram Group

- 6.4.12 Clarcor (Part of Parker-Hannifin)

- 6.4.13 ACDelco (GM)

- 6.4.14 AFE Power

- 6.4.15 Wix Filters

- 6.4.16 Sogefi Group

- 6.4.17 H&V (Engineered Media)

- 6.4.18 Roki Co., Ltd.

- 6.4.19 Champion Laboratories

- 6.4.20 Luber-finer

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment