|

시장보고서

상품코드

1836544

세팔로스포린 의약품 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Cephalosporin Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

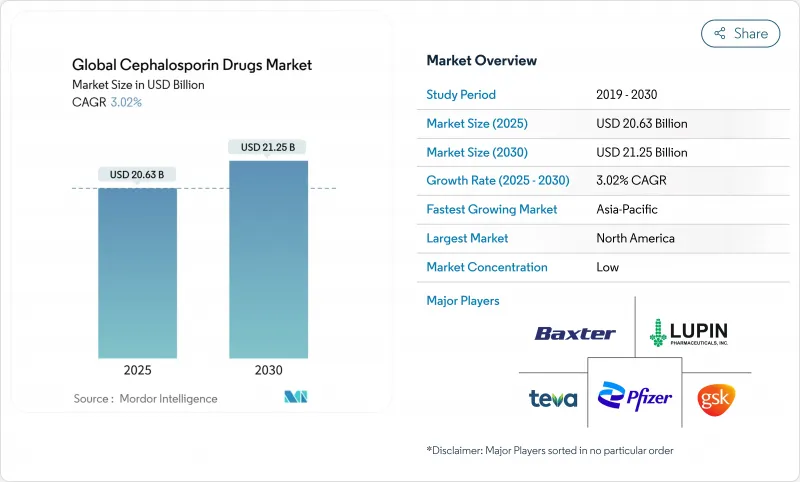

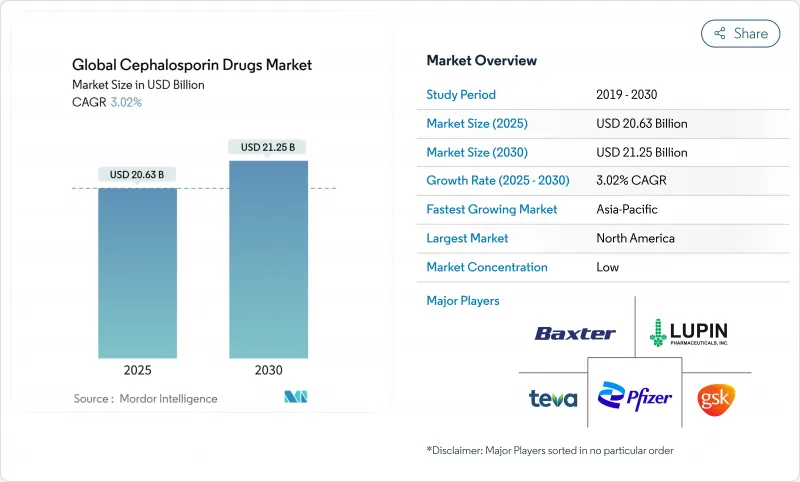

세계의 세팔로스포린 의약품 시장은 2025년 2,063만 달러로, CAGR 3.02%를 반영하여 2030년까지 2,125만 달러로 상승할 것으로 예측되고 있습니다.

세팔로스포린 의약품은 경쟁 제약 및 스튜어드십 규칙에 따라 급속한 확대가 제한되었음에도 불구하고 여전히 중증 병원 감염의 첫 번째 선택 약물이기 때문에 수요는 안정적입니다. 다제 내성 병원체용으로 설계된 신세대 약제의 채용, 예방 투여를 필요로 하는 수술 건수의 확대, 저소득 및 중소득 국가에서 세팔로스포린에 대한 접근을 장려하는 세계보건기구(WHO)의 AWaRe 프레임워크가 성장을 지지하고 있습니다. 반면에 입찰 기반 조달은 가격을 밀어 내고 파지 요법과 같은 항생제 이외의 기술의 상승은 장기 판매량을 위협합니다. 경쟁사와의 차별화는 베타-락타마제 억제제 배합제, 외래 치료용 장시간 작용형 점적 주사제, 적격한 감염증 치료제에 독점권을 부여하는 신속한 규제 패스웨이에 달려 있습니다.

세계 세팔로스포린 의약품 시장 동향과 통찰

다제 내성 그램 음성 감염 증가

현재, 다제 내성 그램 음성 병원체는 병원 감염 프로파일의 대부분을 차지하고 있으며, 임상의는 ESBL 생산 엔테로박테리아에 대한 활성을 보유하는 5세대 세팔로스포린 제형을 사용하는 경향이 있습니다. 폐렴 간균(Klebsiella pneumoniae) ST307 분리주는 3세대 약물에 대해 85%의 내성을 보이고 효능을 유지하는 세프트비프롤과 세페핌-엔메타조박탐 제제의 채용을 가속화하고 있습니다. 미국 감염증 학회(Infectious Diseases Society of America)의 2024년 지침에서는 이러한 첨단 약물이 권장 치료제로 자리매김했으며, 제네릭 의약품과의 경쟁에도 불구하고 가격이 비쌉니다. 병원은 특히 집중 치료실에서 베타 락타마제 억제제와의 병용 요법을 도입하여 고효능 세팔로스포린 변종에 대한 장기적인 수량 지지를 생성하고 있습니다.

수술과 원내 감염 증가

세계적인 수술 수 증가는 세팔로스포린 예방제 수요에 직결됩니다. 가이드라인은 대부분의 수술에 1세대 및 2세대 약물을 권장하며 절개 전 1시간 이내의 투여로 3%의 감염률을 달성하고 있습니다. 원내 폐렴과 패혈증의 프로토콜은 조기 광역 스펙트럼의 적용에 달려 있습니다. 세팔로스포린을 신속하게 투여하면 사망률이 현저하게 감소하는 것으로 연구에서 입증되었습니다. 외래 수술 증가는 단시간 작용형 제제의 필요성을 더욱 확대시키는 한편, 신흥국에서는 새로운 수술 설비가 대폭 증가하여 세팔로스포린 의약품 시장을 지원하고 있습니다.

입찰 기반 조달로 제네릭 의약품 가격 침식

특허실효에 의해 제네릭 의약품의 진입이 잇따르고, 집중 입찰에 의해 특히 제3세대 의약품은 급속하게 가격이 저하하고 있습니다. 엄격한 제한 정책을 실시한 병원에서는 최저가의 제네릭 의약품으로 전환한 후 46.2%의 지출 감소가 기록되어 있습니다. 시장 세분화는 세팔로스포린 의약품 시장의 통합을 강화하기 위해 제조 규모를 확대하거나 이익률이 낮은 분야에서 철수해야 합니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 신속한 QIDP와 항균제 풀 인센티브 프로그램 WHO

- AWaRe의 재분류에 의한 LMIC에서의 사용 촉진

- 세계 항생제 스튜어드십에 의한 광범위한 사용 제한

부문 분석

3세대 분자는 호흡기 감염, 비뇨기 감염, 복강내 감염을 확실히 커버하기 위해 2024년에는 세팔로스포린 의약품 시장 점유율의 44.6%를 차지했습니다. 그러나 지속적인 내성 압력은 5세대 약물을 뒷받침하고 있으며, 2030년까지 연평균 복합 성장률(CAGR)은 9.1%로 예측됩니다. 세프토비프롤이 2024년에 승인되었다는 것은 그램 양성 및 그램 음성 스펙트럼의 확대가 치료 가치를 높이고 프리미엄 가격을 유지한다는 것을 보여줍니다. 최신 베타-락타마제 억제제와 결합한 4세대 세페핌은 또한 난치성 요로 감염의 복합주 효율이 79.1%를 넘어서서 지지를 받고 있습니다. 따라서 첨단 세대 세팔로스포린 의약품 시장 규모는 수량이 나타내는 것보다 빨리 확대되고 있으며, 병원은 내성을 파괴하는 효능에 대해 프리미엄을 지불하고 있습니다.

QIDP 법에 통합된 재정 인센티브는 신규 배합제의 독점기간을 연장하므로 기업은 5세대 약제를 처방 계급의 정점에 위치시킬 수 있습니다. 그럼에도 불구하고 비용에 민감한 지불자는 일상적인 경우에는 3세대 제네릭 의약품을 사용하기 때문에 제조업체는 이익률이 높은 혁신과 판매량이 많은 레거시 프랜차이즈의 균형을 맞추어야 합니다. 이러한 역동성은 가격 전략과 항균제 성능이 채택을 결정하는 양극화된 경쟁 영역을 만들어 냅니다.

의료용 의약품은 복잡한 투여 요법과 내성에 대한 우려로 2024년 매출의 80.3%를 차지합니다. 그러나 아시아태평양 시장의 일부에서는 규제 당국이 경미한 감염증에 대한 약사의 지도에 의한 공급을 허용하고 있기 때문에 OTC 하위 부문은 CAGR 6.36%로 전진하고 있습니다. 이 통제된 자유화는 환자의 대기 시간을 단축하고, 1차 케어의 부담을 경감하고, 세팔로스포린 의약품 시장에의 진입을 확대하고 있습니다.

디지털 약국의 성장은 항생제 판매에 필요한 법적 요건을 충족하는 가상 진단 모듈을 통합함으로써 일반의약품(OTC)의 보급을 더욱 강화하고 있습니다. 대조적으로, 고소득층은 스튜어드십 우선순위를 이유로 처방전을 고수하고 있습니다. 그 결과 다국적 기업은 안전과 내성 모니터링에 주의를 기울이면서 SKU 포트폴리오를 다른 액세스 모델에 맞게 조정할 것입니다.

지역별 분석

북미가 2024년 매출 31.6%로 선도했으며, 그 이유는 첨단 병원, 높은 수술처리능력, QIDP 주도의 혁신 파이프라인이었습니다. 미국의 항생제 관리 규정은 적시 접근성을 저해하지 않으면서 합리적인 사용을 보장하며, 캐나다의 각 주 포뮬러리는 중환자 관리를 위한 보다 광범위한 스펙트럼 옵션을 유지하면서 비용 효율성을 선호합니다. 대규모 지불 시스템은 가파른 수량 할인을 협상하고 주요 성장은 억제되지만 세팔로스포린 의약품 시장 전체에서 일반 및 프리미엄 세팔로스포린 모두에 대한 기본 수요를 확고하게합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 7.9%를 기록했으며, 중국과 인도의 생산 능력 확대, 의료비 증가, 첨단 제제를 필요로 하는 우려할 수 있는 내성률을 뒷받침하고 있습니다. Orchid Pharma와 Cipla의 세페핌-엔메타조박탐 제제 출시와 같은 파트너십은 접근성 확대에서 현지 제조의 역할을 명확히 하는 것입니다. 국민 모두 보험제도와 연동한 정부 입찰은 대량 구매를 촉구하지만, 격렬한 가격경쟁으로 기업은 수익성과 규모의 균형을 잡아야 합니다.

유럽에서는 증거 기반 처방과 신속한 진단이 불필요한 사용을 억제하기 때문에 한 자릿수 중반의 안정적인 성장을 유지하고 있습니다. EMA(유럽 의약품청)의 승인이 조화됨으로써 미국과의 동시 발매가 가능하게 되어, 기업은 주요 시장에서 통일한 마케팅 캠페인을 전개할 수 있게 되었습니다. 영국의 EU 이탈 후 규제조정에는 중간 정도의 불확실성이 수반되지만, WHO의 스튜어드십 가이드를 전체적으로 준수함으로써 ESBL의 만연을 극복할 수 있는 새로운 조합에 특권을 주는 예측 가능한 수요 패턴이 탄생합니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- MDR 그램 음성 감염증 증가

- 외과 수술과 원내 감염 증가

- 신속한 QIDP 및 항균제 사용 장려 프로그램

- WHO Aware의 재분류가 LMIC에서의 사용을 뒷받침

- OPAT용 장시간 작용형 비경구 디포 제제

- 수의학 승인 및 농업용 항생제 사용 증가

- 시장 성장 억제요인

- 입찰 베이스의 조달에 의한 제네릭 의약품의 가격 저하

- 세계의 항생제 스튜어드십에 의한 광범위한 사용 제한

- 풀 인센티브에도 불구하고 연구 개발을 저해하는 낮은 ROI

- 새로운 비항생제 모달리티(파지, 크리스풀)

- 공급망 분석

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액)

- 세대별

- 제1세대

- 제2세대

- 제3세대

- 제4세대

- 제5세대

- 처방 유형별

- 처방약

- 일반의약품(OTC)

- 투여 경로별

- 경구

- 비경구

- 적응증별

- 호흡기 감염증

- 요로 감염증

- 피부 및 연부 조직 감염증

- 패혈증 및 수막염

- 유통 채널별

- 병원 약국

- 소매 약국

- 온라인 약국

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Pfizer Inc.

- F. Hoffmann-La Roche Ltd

- Merck & Co. Inc.

- GlaxoSmithKline plc

- Teva Pharmaceutical Industries Ltd

- Baxter International

- Lupin Pharmaceuticals Inc.

- Macleods Pharmaceuticals Ltd

- Mankind Pharma

- Sun Pharmaceutical Industries Ltd

- AbbVie Inc.

- Bristol-Myers Squibb Company

- Eli Lilly and Company

- Sandoz(Novartis generics)

- Aurobindo Pharma Ltd

- Hikma Pharmaceuticals plc

- Fresenius Kabi

- Cipla Ltd

- Shionogi & Co., Ltd

- Zydus Lifesciences Ltd

제7장 시장 기회와 전망

JHS 25.10.28The cephalosporin drugs market is valued at USD 20.63 million in 2025 and is forecast to climb to USD 21.25 million by 2030, reflecting a 3.02% CAGR.

Steady demand endures because cephalosporins remain first-line therapies for severe hospital infections, even as competitive generics and stewardship rules limit rapid expansion. Uptake of newer generations designed for multidrug-resistant pathogens, broader surgical volumes requiring prophylaxis, and the World Health Organization's AWaRe framework, which encourages cephalosporin access in low- and middle-income countries, underpin growth. On the other hand, tender-based procurement depresses prices, and the rise of non-antibiotic modalities such as phage therapy threatens long-term volumes. Competitive differentiation now hinges on beta-lactamase-inhibitor combinations, long-acting depot injections for outpatient therapy, and expedited regulatory pathways that add exclusivity for qualified infectious disease products.

Global Cephalosporin Drugs Market Trends and Insights

Escalating Prevalence of MDR Gram-Negative Infections

Multidrug-resistant gram-negative pathogens now dominate hospital infection profiles, pushing clinicians toward fifth-generation cephalosporins that retain activity against ESBL-producing Enterobacterales. Klebsiella pneumoniae ST307 isolates show 85% resistance to third-generation agents, accelerating the adoption of ceftobiprole and cefepime-enmetazobactam combinations that remain effective. The Infectious Diseases Society of America's 2024 guidance positions these advanced drugs as recommended therapy, enabling premium pricing despite generic competition. Hospitals also deploy combination regimens with beta-lactamase inhibitors, especially in intensive care units, creating long-run volume support for high-potency cephalosporin variants.

Growth in Surgical Procedures & Hospital-Acquired Infections

Increasing global surgical volumes correlate directly with cephalosporin prophylaxis demand. Guidelines endorse first- and second-generation agents for most interventions, achieving 3% infection rates when dozed within one hour before incision. Hospital-acquired pneumonia and sepsis protocols rely on early broad-spectrum coverage; studies demonstrate notable mortality reductions when cephalosporins are administered promptly. Outpatient surgery growth further expands need for short-acting formulations, while emerging economies add substantial new surgical capacity, sustaining the cephalosporin drugs market.

Generic Price Erosion from Tender-Based Procurement

Patent expirations invite numerous generic entrants, and centralized tenders drive prices down swiftly, particularly for third-generation drugs. Hospitals that implemented strict restriction policies documented 46.2% spending drops after switching to the lowest-priced generics. Manufacturers must now lean on manufacturing scale or exit low-margin segments, intensifying consolidation within the cephalosporin drugs market.

Other drivers and restraints analyzed in the detailed report include:

- Expedited QIDP & Antimicrobial Pull-Incentive Programs

- WHO AWaRe Re-Classification Boosting LMIC Usage

- Global Antibiotic Stewardship Restrictions on Broad Use

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Third-generation molecules held 44.6% of the cephalosporin drugs market share in 2024, owing to dependable coverage across respiratory, urinary, and intra-abdominal infections. However, continuous resistance pressure propels fifth-generation agents, which are forecast to clock a 9.1% CAGR through 2030. Ceftobiprole's 2024 approval illustrates how expanded gram-positive and gram-negative spectra elevate therapeutic value and sustain premium pricing. Fourth-generation cefepime, paired with modern beta-lactamase inhibitors, also gains traction because composite response rates top 79.1% in difficult urinary tract infections. The cephalosporin drugs market size for advanced generations is therefore widening faster than volumes indicate, as hospitals pay a premium for resistance-breaking efficacy.

Fiscal incentives embedded in QIDP statutes prolong exclusivity for novel combinations, encouraging firms to position fifth-generation drugs at the apex of formulary hierarchies. Nonetheless, cost-focused payers favor third-generation generics for routine cases, forcing manufacturers to balance high-margin innovation with high-volume legacy franchises. This dynamic generates a bifurcated competitive field where pricing strategy and antimicrobial performance co-determine adoption.

Prescription medicines commanded 80.3% of 2024 revenue because complex dosing regimens and resistance concerns require medical oversight. Yet the OTC sub-segment advances at a 6.36% CAGR as regulators in select Asia-Pacific markets permit pharmacist-guided supply for mild infections. This controlled liberalization lowers patient wait times and streamlines primary care burdens, broadening participation in the cephalosporin drugs market.

Growing digital pharmacies further bolsters OTC uptake by integrating virtual consultation modules that satisfy legal requisites for antibiotic sales. In contrast, high-income markets persist with prescription status, citing stewardship priorities. The resulting patchwork regulatory canvas leaves multinational firms tailoring SKU portfolios to disparate access models while maintaining vigilance on safety and resistance monitoring.

The Cephalosporins Market is Segmented by Generation (First, Second-Generation, and More), Prescription Type (Prescription and OTC), Route of Administration (Oral and Parenteral), Indication (Respiratory Tract, Urinary Tract Infections, and More), Indication (Hospital Pharmacies, and More), and by Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 31.6% revenue in 2024, due to advanced hospitals, high surgical throughput, and QIDP-driven innovation pipelines. U.S. antimicrobial stewardship rules ensure rational use without compromising timely access, and Canada's provincial formularies prioritize cost-effectiveness while retaining broader-spectrum options for critical care. Large payer systems negotiate steep volume discounts, restraining headline growth but cementing baseline demand for both generic and premium cephalosporins across the cephalosporin drugs market.

Asia-Pacific registers the fastest 7.9% CAGR through 2030, underpinned by capacity expansions in China and India, rising health expenditures, and alarming resistance rates that necessitate advanced formulations. Partnerships such as Orchid Pharma-Cipla's launch of cefepime-enmetazobactam underscore local manufacturing's role in broadening access. Government tenders linked to universal health schemes stimulate large-volume purchases, although intense price competition requires firms to balance profitability with scale.

Europe maintains steady mid-single-digit growth as evidence-based prescribing and rapid diagnostics temper unnecessary usage. Harmonized EMA approvals allow simultaneous launches with the U.S., enabling companies to leverage unified marketing campaigns across major markets. The United Kingdom's post-Brexit regulatory adjustments introduce moderate uncertainty, but overall adherence to WHO stewardship guidance creates predictable demand patterns that privilege newer combinations able to overcome endemic ESBL prevalence.

- Pfizer

- Roche

- Merck

- GlaxoSmithKline

- Teva Pharmaceutical Industries

- Baxter

- Lupin

- Macleods Pharmaceuticals

- Mankind Pharma

- Sun Pharmaceuticals Industries

- Abbvie

- Bristol-Myers Squibb

- Eli Lilly and Company

- Sandoz (Novartis generics)

- Aurobindo Pharma

- Hikma Pharmaceuticals

- Fresenius

- Cipla

- Shionogi

- Zydus Lifesciences Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Prevalence of MDR Gram-Negative Infections

- 4.2.2 Growth In Surgical Procedures & Hospital-Acquired Infections

- 4.2.3 Expedited QIDP & Antimicrobial Pull-Incentive Programs

- 4.2.4 Who Aware Re-Classification Boosting LMIC Usage

- 4.2.5 Long-Acting Parenteral Depot Formulations for OPAT

- 4.2.6 Increasing Veterinary Approvals & Agri-Antibiotic Use

- 4.3 Market Restraints

- 4.3.1 Generic Price Erosion from Tender-Based Procurement

- 4.3.2 Global Antibiotic Stewardship Restrictions on Broad Use

- 4.3.3 Poor Roi Despite Pull Incentives Deterring R&D

- 4.3.4 Emerging Non-Antibiotic Modalities (Phage, Crispr)

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Generation

- 5.1.1 First-generation

- 5.1.2 Second-generation

- 5.1.3 Third-generation

- 5.1.4 Fourth-generation

- 5.1.5 Fifth-generation

- 5.2 By Prescription Type

- 5.2.1 Prescription Drugs

- 5.2.2 OTC Drugs

- 5.3 By Route of Administration

- 5.3.1 Oral

- 5.3.2 Parenteral

- 5.4 By Indication

- 5.4.1 Respiratory Tract Infections

- 5.4.2 Urinary Tract Infections

- 5.4.3 Skin & Soft-Tissue Infections

- 5.4.4 Sepsis & Meningitis

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online Pharmacies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Pfizer Inc.

- 6.3.2 F. Hoffmann-La Roche Ltd

- 6.3.3 Merck & Co. Inc.

- 6.3.4 GlaxoSmithKline plc

- 6.3.5 Teva Pharmaceutical Industries Ltd

- 6.3.6 Baxter International

- 6.3.7 Lupin Pharmaceuticals Inc.

- 6.3.8 Macleods Pharmaceuticals Ltd

- 6.3.9 Mankind Pharma

- 6.3.10 Sun Pharmaceutical Industries Ltd

- 6.3.11 AbbVie Inc.

- 6.3.12 Bristol-Myers Squibb Company

- 6.3.13 Eli Lilly and Company

- 6.3.14 Sandoz (Novartis generics)

- 6.3.15 Aurobindo Pharma Ltd

- 6.3.16 Hikma Pharmaceuticals plc

- 6.3.17 Fresenius Kabi

- 6.3.18 Cipla Ltd

- 6.3.19 Shionogi & Co., Ltd

- 6.3.20 Zydus Lifesciences Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment