|

시장보고서

상품코드

1836551

세포 기반 분석 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Cell Based Assay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

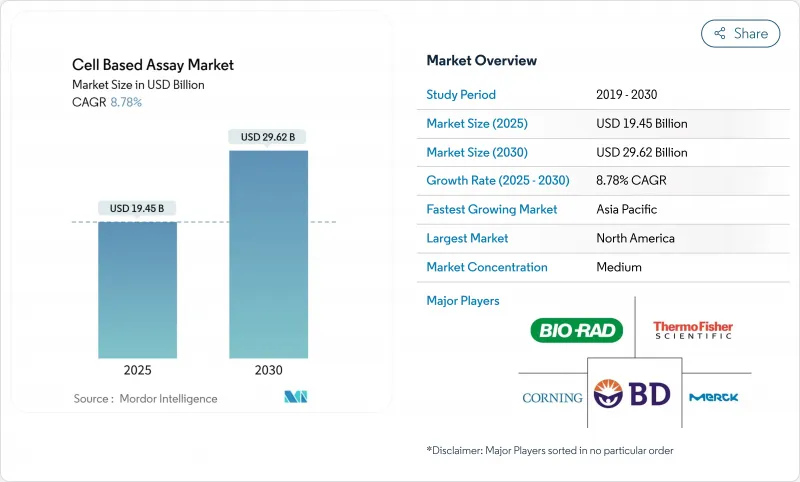

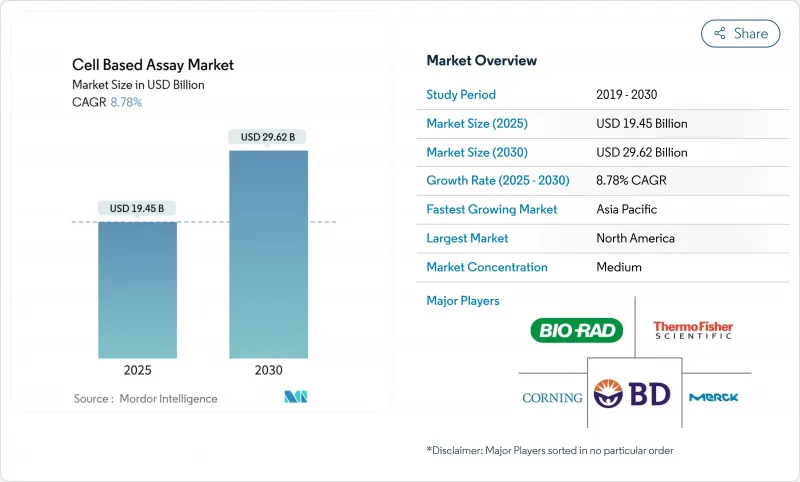

세계의 세포 기반 분석 시장 규모는 2025년 194억 5,000만 달러로 추정되며, 예측 기간 중(2025-2030년) CAGR은 8.78%를 나타낼 전망이며, 2030년까지 296억 2,000만 달러에 달할 것으로 예측됩니다.

2025년 4월 FDA는 동물 실험을 단계적으로 폐지하기로 결정했으며, 동물 실험에서 인간과 관련된 시험관 내 모델로의 전환이 진행되고, 검증된 세포 플랫폼이 규제에 따른 개발의 중심에 자리잡고 있습니다. 기업은 예측 정밀도 향상과 사이클 타임 단축을 통해 자동화, AI 주도 분석, 3D 오가노이드 모델을 빠르게 확대하고 있으며, 주요 바이오파머 그룹의 투자 흐름은 차세대 스크리닝 기술에 대한 자신감을 보여줍니다. 동시에, 만성 질환 증가, 종양학 파이프라인, 재생 의료 프로젝트는 고처리량 포맷과 라벨프리 검출 시스템에 대한 견조한 수요 전망을 유지하고 있습니다.

세계 세포 기반 분석 시장 동향과 통찰

만성 질환과 생활 습관병의 유병률 상승

암과 대사성 질환의 이환율 증가는 발견주기를 단축하는 정교한 표현형 스크리닝에 대한 수요를 강화하고 있습니다. 국립암연구소의 예산은 2024년에 4억 760만 달러 증가하여 암 영역의 파이프라인을 대상으로 한 하이컨텐트 플랫폼에 대한 자금이 계상되었습니다. Vertex Pharmaceuticals는 1형 당뇨병에 대한 줄기세포 치료제의 스케일업에 2억 4,000만 달러를 기부했습니다. 고령화로 임상 요구가 확대되는 가운데 제약 그룹은 오가노이드 패널과 멀티플렉스 플로우 사이토메트리를 통합하여 번역 관련성을 높임으로써 장기적인 성장을 강화하고 있습니다.

창약에 대한 제약 및 바이오테크놀러지 연구개발비 증가

Thermofisher Scientific은 세포 분석 기능을 포함한 미국의 제조 및 연구 개발 기지에서 20억 달러(2025-2028년)의 예산을 기록하고 있습니다. 메릴랜드 주에 있는 AstraZeneca의 3억 달러의 세포 치료 시설과 Novo Nordisk의 41억 달러의 주사제 치료 시설은 시험관내 검사 워크플로우에 대한 광범위한 자본 배분을 밝혔습니다. Fujifilm Diosynth와 같은 수탁 제조업체는 포유류 세포 프로세스에 초점을 맞춘 16억 달러의 확장으로 이어지며 세포 기반 분석 산업에 대한 다중 이해관계자의 신뢰를 보여주고 있습니다.

첨단 플랫폼의 높은 자본 비용과 유지 보수 비용

스펙트럼 흐름 시스템은 50만 달러를 넘어, 연간 서비스 계약은 그 20%를 상승시킵니다. Beckman Coulter의 모듈식 업그레이드를 포함한 대출 제도는 진입 장벽을 낮추려는 것이지만, 자본 지출은 세포 기반 분석 시장 침투 억제요인으로 남아 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 고처리량 및 라벨프리 어세이의 끊임없는 개발 진보

- 정밀 종양학에서 3D 오가노이드 모델 채용 확대

- 학제 간 분석 개발 인력 부족

부문 분석

시약 및 키트는 2024년 세포 기반 분석 시장의 51.33%를 반복 구매 경제성을 바탕으로 소모품 수익 기반을 지원합니다. 그러나 세포주는 매우 중요한 혁신적인 엔진으로, 인공 다능성 줄기세포의 진보와 CRISPR에 의한 질병 모델을 배경으로 CAGR 10.17%로 확대되고 있습니다. TreeFrog Therapeutics가 Vertex와 2억 4,000만 달러의 C-Stem 라이선싱 계약을 맺은 것은 확장 가능하고 고품질의 세포 재료에 대한 평가가 높아지고 있음을 뒷받침합니다.

마이크로플레이트 하위 부문은 실험실의 자동화 적합성으로부터 꾸준한 이익을 누리며, 특수 배지 및 완충액은 시장 전체의 확대를 반영합니다. 줄기세포 유래 균주는 고함량 스크리닝에 필수적인 일관성 향상으로 초대 배양을 대체하는 것이 증가하고 있습니다.

고처리량 스크리닝(HTS) 플랫폼은 오랫동안 신약개발의 핵심 기술이었으며 2024년 매출은 42.19%였습니다. 그러나 수요는 보다 정확하게 생체내 생물학을 재현하는 생리학적으로 적합한 3차원 모델로 이동하고 있습니다. 3D 배양 부문의 CAGR 8.25%는 오가노이드의 표준화와 규제 당국의 승인에 의해 추진되고 있습니다. BD의 스펙트럼 흐름 통합과 로봇 암은 기존 벤더가 자동화 및 멀티모달 감지를 통해 HTS의 미래를 어떻게 담보하는지 보여줍니다.

라벨프리 검출 및 스펙트럼 세포측정법은 분석 판독을 넓히고, 자동 액체 처리기는 샘플 전처리 시간을 단축하고 처리량을 향상시킵니다. 이러한 진보가 함께 통합 플랫폼의 세포 기반 분석 시장 규모는 확대되고 있으며, 암 영역의 워크플로우에서 2자리 성장이 기대됩니다.

지역별 분석

북미는 2024년 매출의 41.23%를 차지했며 바이오 의약품 파이프라인의 충실, NIH의 자금 지원, 인간 관련 모델을 지지하는 FDA 지침에 뒷받침되고 있습니다. Thermofisher Scientific의 20억 달러 계획을 포함하여 정부의 우대 조치와 국내 제조에 대한 투자는 지역 공급망을 강화하고 세포 기반 분석 시장을 확대합니다.

아시아태평양은 CAGR 9.13%로 가장 빠르게 확대되고 있습니다. 중국의 인재 풀과 인프라는 급속히 확대되고 있으며, 고차원 사이토메트리 시스템을 타겟으로 하는 Cytek Biosciences의 우시에서 50,000평방피트의 제조 허브가 각광을 받고 있습니다. 일본에서는 세포치료와 유전자치료의 승인이 신속화됨으로써 분석에 의존하는 제품의 상업화가 가속화되고 3차원 배양과 AI를 활용한 분석에 대한 수요가 높아지고 있습니다.

유럽은 독일, 스위스, 영국에 정착한 제약 클러스터를 통해 상당한 점유율을 유지하고 있습니다. 대체 검사 규정의 미국 표준과의 조화는 라벨프리 검출 및 장기 온칩 플랫폼으로의 업그레이드를 촉진합니다. 한편, 라틴아메리카, 중동 및 아프리카는 기술 이전과 공동 프로그램이 고자본 진입 장벽을 완화할 새로운 기회를 제공합니다. 이 지역을 합치면 규제 수렴이 진행되는 반면, 세계의 세포 기반 분석 시장에 새로운 볼륨이 추가됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 도입

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 만성질환 및 생활습관병 증가

- 제약 및 바이오테크놀러지 기업의 신약개발 연구 개발비 증가

- 높은 처리량 및 라벨프리 분석의 지속적인 발전

- 정밀 종양학에서 3D 오가노이드 모델의 채용 확대

- 스크리닝 사이클을 가속화하는 AI를 활용한 하이 컨텐츠 분석

- 동물실험을 대체하는 시험관내 시험으로의 세계적 규제 전환

- 시장 성장 억제요인

- 고급 플랫폼의 높은 자본 비용과 유지 보수 비용

- 다분야에 걸친 분석 개발 인력의 부족

- 데이터 통합 및 분석 상호 운용성을 위한 어려운 학습 곡선

- 유행 후 취약한 특수 시약 공급망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(단위 : 달러)

- 제품별

- 세포 라인

- 단일세포 라인

- 줄기세포 라인

- 인공 다능성 세포 라인

- 유전자 재조합 세포주

- 기타

- 시약 및 키트

- 분석 시약

- 리포터 유전자 및 기질 키트

- 버퍼 및 배지

- 기타 시약

- 마이크로플레이트

- 기타 소모품

- 세포 라인

- 기술별

- 고처리량 스크리닝

- 플로우 사이토메트리

- 자동 액체 핸들링

- 라벨프리 검출

- 3차원 세포 배양 분석

- 기타

- 용도별

- 신약개발 및 의약품 개발

- ADME 및 톡시콜로지 연구

- 기초연구

- 정밀 및 재생의료

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 수탁연구기관

- 학술 및 정부기관

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Becton, Dickinson and Company

- Thermo Fisher Scientific Inc.

- Danaher Corporation

- Merck KGaA

- PerkinElmer Inc.

- Bio-Rad Laboratories Inc.

- Corning Incorporated

- Lonza Group AG

- Promega Corporation

- Cell Signaling Technology Inc.

- Agilent Technologies Inc.

- Charles River Laboratories

- Eurofins Scientific SE

- DiscoverX Corporation

- Revvity Life Sciences

- Abcam plc

- GE HealthCare Technologies Inc.

- Miltenyi Biotec

- Sartorius AG

- ATCC

제7장 시장 기회와 전망

JHS 25.10.28The Cell Based Assay Market size is estimated at USD 19.45 billion in 2025, and is expected to reach USD 29.62 billion by 2030, at a CAGR of 8.78% during the forecast period (2025-2030).

The transition from animal studies to human-relevant in vitro models, bolstered by the April 2025 FDA decision to phase out animal testing, positions validated cellular platforms at the center of regulatory-compliant development. Companies are rapidly expanding automation, AI-driven analytics, and 3-D organoid models to improve predictive accuracy and reduce cycle times, while investment flows from major biopharma groups signal confidence in next-generation screening technologies. At the same time, rising chronic-disease prevalence, oncology pipelines, and regenerative-medicine projects sustain a robust demand outlook for high-throughput formats and label-free detection systems.

Global Cell Based Assay Market Trends and Insights

Rising Prevalence of Chronic & Lifestyle Diseases

Escalating cancer and metabolic-disease incidence is intensifying demand for sophisticated phenotypic screens that shorten discovery cycles. The National Cancer Institute budget rose by USD 407.6 million in 2024, earmarking funds for high-content platforms aimed at oncology pipelines. Vertex Pharmaceuticals committed USD 240 million to scale stem-cell therapeutics for type 1 diabetes, illustrating how disease-driven investment accelerates the cell-based assay market. As aging demographics widen clinical need, pharmaceutical groups integrate organoid panels and multiplex flow cytometry to improve translational relevance, reinforcing long-term growth.

Escalating Pharma-Biotech R&D Spending on Drug Discovery

Thermo Fisher Scientific has budgeted USD 2 billion (2025-2028) for U.S. manufacturing and R&D sites that include cell-analysis capabilities. AstraZeneca's USD 300 million cell-therapy facility in Maryland and Novo Nordisk's USD 4.1 billion injectable-therapeutic plant reveal broad capital reallocation toward in vitro testing workflows. Contract manufacturers such as Fujifilm Diosynth follow with USD 1.6 billion expansions focused on mammalian-cell processes, indicating multistakeholder confidence in the cell based assay industry

High Capital & Maintenance Costs of Advanced Platforms

Spectral flow systems can exceed USD 500,000, while annual service contracts add 20% of that figure, limiting uptake in price-sensitive academic and emerging-market settings. Financing schemes, including Beckman Coulter's modular upgrades, seek to lower entry barriers, but capital outlays remain a gating factor for broader cell-based assay market penetration.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Advances in High-Throughput & Label-Free Assays

- Growing Adoption of 3-D Organoid Models for Precision Oncology

- Shortage of Multi-Disciplinary, Assay-Development Talent

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and kits, benefiting from repeat-purchase economics, contributed 51.33% of the cell-based assay market in 2024, anchoring the consumables revenue base. Cell lines, however, represent the pivotal innovation engine, expanding at 10.17% CAGR on the back of induced pluripotent stem cell advances and CRISPR-engineered disease models. TreeFrog Therapeutics' USD 240 million C-Stem licensing deal with Vertex underscores rising valuations for scalable, high-quality cellular material.

The microplates subsegment enjoys steady gains from laboratory-automation compatibility, while specialty media and buffers mirror overall market expansion. Stem-cell-derived lines increasingly replace primary cultures due to improved consistency, a critical requirement for high-content screens.

High-throughput screening (HTS) platforms, long the backbone of pharmaceutical discovery, delivered 42.19% revenue in 2024. Yet, demand is shifting toward physiologically relevant 3-D models that more accurately recapitulate in-vivo biology. The 3-D culture segment's 8.25% CAGR is propelled by organoid standardization and regulatory endorsement. BD's spectral flow integration with robotic arms illustrates how established vendors are future-proofing HTS through automation and multi-modal detection.

Label-free detection and spectral cytometry broaden assay readouts, while automated liquid handlers compress sample-prep times, enhancing throughput. Together, these advances are expanding the cell based assay market size for integrated platforms expected to post double-digit growth within oncology workflows.

The Cell Based Assay Market Report is Segmented by Product (Cell Lines, Reagents and Kits, and More), Technology (High-Throughput Screening, and More), Application (Drug Discovery and Development, and More), End User (Pharmaceutical and Biotechnology Companies, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 41.23% of 2024 revenue, underpinned by deep biopharma pipelines, NIH funding, and FDA guidance favoring human-relevant models. Government incentives and domestic manufacturing investments, for example, Thermo Fisher Scientific's USD 2 billion plan, fortify regional supply chains and enlarge the cell based assay market.

Asia-Pacific posts the fastest expansion at 9.13% CAGR. China's talent pool and infrastructure are scaling rapidly, highlighted by Cytek Biosciences' 50,000 sq ft manufacturing hub in Wuxi targeting high-dimensional cytometry systems. Japan's fast-track approval path for cell and gene therapies accelerates commercialization of assay-dependent products, reinforcing demand for 3-D cultures and AI-enhanced analytics.

Europe retains a substantial share through entrenched pharma clusters in Germany, Switzerland, and the UK. Harmonization of alternative-testing regulations with U.S. standards is catalyzing upgrades to label-free detection and organ-on-chip platforms. Meanwhile, Latin America, the Middle East, and Africa offer emerging opportunities where technology transfer and collaborative programs mitigate high-capital entry barriers. Collectively these regions add incremental volume to the global cell based assay market while progressing toward regulatory convergence.

- Beckton Dickinson

- Thermo Fisher Scientific

- Danaher

- Merck

- PerkinElmer

- Bio-Rad Laboratories

- Corning

- Lonza Group

- Promega

- Cell Signaling Technology

- Agilent Technologies

- Charles River

- Eurofins

- DiscoverX Corporation

- Revvity Life Sciences

- Abcam

- GE HealthCare Technologies Inc.

- Miltenyi Biotec

- Sartorius

- ATCC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Chronic & Lifestyle Diseases

- 4.2.2 Escalating Pharma-Biotech R&D Spending on Drug Discovery

- 4.2.3 Continuous Advances in High-Throughput & Label-Free Assays

- 4.2.4 Growing Adoption of 3-D Organoid Models for Precision Oncology

- 4.2.5 AI-Powered High-Content Analytics Accelerating Screening Cycles

- 4.2.6 Global Regulatory Shift Toward In Vitro Alternatives to Animal Tests

- 4.3 Market Restraints

- 4.3.1 High Capital & Maintenance Costs of Advanced Platforms

- 4.3.2 Shortage of Multi-Disciplinary, Assay-Development Talent

- 4.3.3 Steep Learning Curve for Data Integration & Assay Interoperability

- 4.3.4 Fragile, Specialty-Reagent Supply Chains Post-Pandemic

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Product

- 5.1.1 Cell Lines

- 5.1.1.1 Primary Cell Lines

- 5.1.1.2 Stem Cell Lines

- 5.1.1.3 Induced Pluripotent Cell Lines

- 5.1.1.4 Engineered / Recombinant Lines

- 5.1.1.5 Others

- 5.1.2 Reagents & Kits

- 5.1.2.1 Assay Reagents

- 5.1.2.2 Reporter Gene & Substrate Kits

- 5.1.2.3 Buffers & Media

- 5.1.2.4 Other Reagents

- 5.1.3 Microplates

- 5.1.4 Other Consumables

- 5.1.1 Cell Lines

- 5.2 By Technology

- 5.2.1 High-Throughput Screening

- 5.2.2 Flow Cytometry

- 5.2.3 Automated Liquid Handling

- 5.2.4 Label-free Detection

- 5.2.5 3-D Cell-Culture Assays

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Drug Discovery & Development

- 5.3.2 ADME & Toxicology Studies

- 5.3.3 Basic Research

- 5.3.4 Precision & Regenerative Medicine

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Contract Research Organizations

- 5.4.3 Academic & Government Institutes

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Becton, Dickinson and Company

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Danaher Corporation

- 6.3.4 Merck KGaA

- 6.3.5 PerkinElmer Inc.

- 6.3.6 Bio-Rad Laboratories Inc.

- 6.3.7 Corning Incorporated

- 6.3.8 Lonza Group AG

- 6.3.9 Promega Corporation

- 6.3.10 Cell Signaling Technology Inc.

- 6.3.11 Agilent Technologies Inc.

- 6.3.12 Charles River Laboratories

- 6.3.13 Eurofins Scientific SE

- 6.3.14 DiscoverX Corporation

- 6.3.15 Revvity Life Sciences

- 6.3.16 Abcam plc

- 6.3.17 GE HealthCare Technologies Inc.

- 6.3.18 Miltenyi Biotec

- 6.3.19 Sartorius AG

- 6.3.20 ATCC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment