|

시장보고서

상품코드

1836620

북미의 단백질체학 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)North America Proteomics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

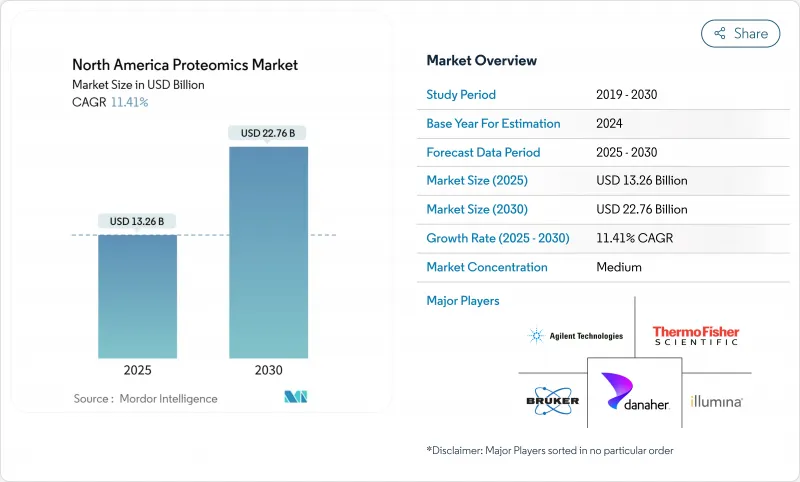

북미의 단백질체학 시장 규모는 2025년에 132억 6,000만 달러, 2030년에는 227억 6,000만 달러에 이를 것으로 예측되며, CAGR은 11.41%를 나타낼 전망입니다.

인공지능과 최신 질량분석 플랫폼의 통합이 진행됨에 따라 장비 공급업체 간의 통합이 꾸준히 진행되고 있으며, 멀티오믹스 신흥 기업으로의 벤처 캐피탈 유입이 확대되고 있습니다. Thermofisher Scientific의 올링크 인수(31억 달러)와 같은 전략적 거래는 기존 기업이 차세대 단백질 분석 자산을 둘러싸고 탐색 기간을 단축하는 방법을 보여줍니다. 미국에 기반을 둔 제약 스폰서는 높은 처리량 워크플로우에 대한 초기 단계 수요를 독점하고 있지만, 중소 바이오테크놀러지 기업과 학술기관의 사용자는 자본 장벽을 상쇄하기 위해 위탁연구기관에 대한 의존을 강화하고 있습니다. 장기적인 성장의 원동력은 임상 실험실이 단백질체학 진단을 채택하기 위한 명확한 경로를 제공하고, 병원이나 레퍼런스 실험실에 분석기기의 현대화를 촉진하는 규제의 움직임에도 있습니다.

북미의 단백질체학 시장 동향과 통찰

맞춤형 의료 도입 가속

Precision 종양 프로그램은 현재 개별 종양 세포 수준에서 치료 선택을 유도하기 위해 깊은 시각적 단백질체학를 통합하고 있습니다. FDA는 2024년에 4가지 펩티드 기반 치료제를 승인하였으며, 단백질 주도의 개입에 대한 규제 당국의 신뢰성을 보여주고 있습니다. 실시간 단백질 시그니처가 유전체 마커 단독보다 치료 예측 정확도를 향상시킨다는 것을 헬스케어 시스템이 인식하게 되었습니다. 따라서 임상 샘플에서 낮은 존재량의 단백질을 직접 정량할 수 있는 고감도 장치 수요가 높아지고 있습니다. 이러한 요구는 분석 깊이를 유지하면서도 실행 시간을 단축하는 새로운 궤도 트랩과 음향 방출 플랫폼의 프리미엄 가격을 지원합니다. 지불자가 의료 보상을 측정 가능한 결과와 연계함에 따라 검사 시설은 단백질 역학을 실용적인 의사 결정으로 전환하는 분석을 선호하게 되었고, 북미의 단백질체학 시장은 더욱 활성화되고 있습니다.

단백질체학에 특화된 자금 조달 급증

벤처 투자자는 생세포 이미징과 AI 애널리틱스를 결합한 기업에 대규모 팔로우 온 커밋을 실시했습니다. Eikon은 2025년 2월에 3억 5,100만 달러를 조달했고, 이 회사의 평가 금액을 31억 달러로 끌어올려 단백질 추적형 의약품 엔진에 대한 광범위한 신뢰를 보였습니다. 공적 지원은 민간의 열정을 반영합니다. 캐나다의 기술 전략은 2029년까지 6만 5,000명의 바이오 이코노미 종사자가 늘어날 것으로 예측하고 있으며, 그 중에는 바이오 제조에 특화된 1만 6,140명의 직무도 포함되어 있습니다. 새로운 자본을 얻은 신흥기업은 지금까지 없는 규모로 독자적인 상호작용 데이터세트를 만들어 내고 기존 기업이 제휴와 인수를 통해 대처해야 하는 진입장벽을 구축하고 있습니다. 유동성의 높이는 명확한 임상 이용 사례와 함께 북미의 단백질체학 시장의 확대를 지원하는 자금 조달의 파도를 지원합니다.

장비의 높은 자본 비용

플래그십의 질량분석기는 100만 달러를 초과할 수 있으며, 이 장애물은 2024년 주문을 늦추고 있습니다. 바이오 래드 래버러토리즈는 고객이 구매를 연기했기 때문에 생명 과학 분야의 매출이 2024년 2분기에 16.5% 감소했습니다. 소규모 생명 공학 기업과 학술 센터는 균형 시트의 유연성이 부족하기 때문에 핵심 시설의 시간을 빌리거나 서비스 실험실을 활용합니다. 임대는 현금 흐름을 원활하게 하지만 평생 영업 비용을 증가시킵니다. 또한 급속한 혁신은 감가상각주기를 단축하기 때문에 구매자는 조심해야 하며 북미의 단백질체학 시장의 단기 성장이 억제됩니다.

보고서에서 분석된 기타 촉진요인 및 억제요인/p>

- 고속 처리량 MS 플랫폼의 혁신

- 바이오파마의 단백질체학 지출 확대

- 바이오인포매틱스의 인력 부족

부문 분석

시약은 2024년 북미 단백질체학 시장 점유율의 63.41%를 차지했습니다. 각 실험마다 신선한 항체, 효소, 완충액, 표지 키트가 필요하기 때문입니다. 공급업체는 소모품을 장비에 번들하여 예측 가능한 수익을 보장합니다. 소프트웨어 및 서비스 슬라이스는 상당히 작지만 CAGR은 12.85%를 나타냅니다. 사전 훈련된 AI 모델을 갖춘 클라우드 플랫폼은 스펙트럼 주석, 단백질 간 상호작용 매핑 및 임상시험 보고를 간소화합니다. 장비는 높은 가격으로 거래되지만 주기적으로 교체가 이루어집니다. 이를 통해 공급업체는 서비스 계약을 하드웨어와 연결하여 북미 단백질체학 시장의 현금 흐름을 원활하게 하고 고객 유지를 개선하고 있습니다.

소프트웨어의 성장은 구독 모델로의 전환도 반영합니다. 데이터 분석 포털은 각 샘플 또는 월별로 청구되며 예측 불가능한 자본 지출을 운영 예산으로 바꿉니다. 매니지드 서비스 회사는 현재 LIMS, 통계 파이프라인, 규제 등급 감사 추적을 통합하고 있으며, 인력 부족 병원은 전임 바이오인포매티션을 고용하지 않고 최신 기능을 얻을 수 있습니다. 데이터 양이 증가함에 따라 암호화된 클라우드 스토리지, 백업 및 사이버 보안 감사에 대한 수요도 증가하고 있습니다. 이러한 추세는 모두 북미의 단백질체학 업계에 기세를 주고 시약에서 보고서까지 원활한 워크플로우를 가능하게 하는 개발자에게 장기적인 플랫폼의 가치를 높이는 것입니다.

질량 분석계는 2024년 북미 단백질체학 시장 규모의 28.27%를 차지했는데, 이는 수십년에 걸친 신뢰성, 방대한 레거시 데이터세트, 광범위한 규제 당국의 수용을 반영하고 있습니다. 고해상도 오비 트랩과 비행 시간 시스템은 현재 스펙트럼의 품질과 번역 후 수정을 실시간으로 예측하는 기본 AI 모델과 쌍을 이루고 있습니다. 차세대 시퀀서 플랫폼은 공급업체가 유전체학, 전사체학 및 단백질체학를 단일 멀티오믹스 리드에 통합했기 때문에 13.02%의 연평균 복합 성장률(CAGR)을 기록했습니다. 일루미나는 2026년까지 공간 전사체학 애드온의 상품화를 계획하고 있으며, 시퀀서와 엔비디아 GPU를 조합함으로써 종양학 연구에서 단백질 구조의 통찰을 가속화하고 있습니다.

마이크로플루이딕스 시료 취급 도구는 반응 부피를 줄이고 감염성 프로테오타이핑을 위한 저렴한 비용의 요점 점검을 가능하게 합니다. 크로마토그래피 및 모세관 전기영동은 샘플 정리를 위한 틈새 관련성을 유지하며, 단백질 마이크로어레이는 높은 처리량의 항체 탐색을 지원합니다. MS, NGS, 형광 이미징 모듈을 결합한 하이브리드 장치는 실험실 실적를 줄이고 자산 활용을 극대화합니다. 이러한 융합은 워크플로우의 효율성을 향상시키고 최종 사용자를 총 솔루션을 제공하는 공급업체로 연결하여 북미의 단백질체학 시장을 확대합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 맞춤형 의료의 보급

- 단백질체학에 특화한 자금 조달의 급증

- 처리량이 많은 MS 플랫폼의 혁신

- 바이오파마의 단백질체학 연구비 확대

- AI 대응 프로테오 유전체 결정 툴

- 현장 전개 가능한 마이크로플루이딕스 샘플 전처리 키트

- 시장 성장 억제요인

- 높은 자본 비용

- 바이오인포매틱스의 인재 부족

- 친화성 시약에 관한 특허 장벽

- 클라우드 멀티오믹스의 사이버 보안 위험

- 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측(금액)

- 구성요소별

- 기기

- 시약

- 소프트웨어 및 서비스

- 기술별

- 질량 분석

- 분광법

- 크로마토그래피

- 차세대 시퀀서

- 단백질 마이크로어레이

- 마이크로플루이딕스

- X선 결정 구조 분석

- 기타 기술

- 용도별

- 약물 발견 및 의약품 개발

- 임상 진단

- 바이오마커 탐색

- 정밀의료 및 맞춤형 의료

- 농업 및 환경 단백질체학

- 기타 용도

- 최종 사용자별

- 제약 및 바이오테크놀러지 기업

- 학술기관 및 연구기관

- 수탁연구기관

- 기타 최종 사용자

- 지역별

- 미국

- 캐나다

- 멕시코

제6장 경쟁 구도

- 시장 집중도

- 경쟁의 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- Agilent Technologies Inc.

- Alamar Biosciences, Inc.

- Bioinformatics Solutions Inc.

- Bio-Rad Laboratories Inc.

- Bruker Corporation

- Creative Proteomics

- Danaher Corporation

- GE Healthcare

- Illumina Inc.

- Merck KGaA

- Nautilus Biotechnology

- Oxford Nanopore Technologies

- Promega Corporation

- QIAGEN NV

- Revvity, Inc.

- Seer Inc.

- Shimadzu Corporation

- SomaLogic Inc.

- Thermo Fisher Scientific Inc.

- Waters Corporation

제7장 시장 기회와 전망

SHW 25.10.28The North America proteomics market size stands at USD 13.26 billion in 2025 and is forecast to reach USD 22.76 billion by 2030, registering an 11.41% CAGR.

Rising integration of artificial intelligence with modern mass-spectrometry platforms, steady consolidation among instrument suppliers, and expanding venture capital flows into multi-omics start-ups combined to keep the region ahead of global peers. Strategic deals, such as Thermo Fisher Scientific's USD 3.1 billion purchase of Olink, show how incumbents lock in next-generation protein-analysis assets to shorten discovery timelines. United States-based pharmaceutical sponsors dominate early-stage demand for high-throughput workflows, while smaller biotechnology firms and academic users increasingly rely on contract research organizations to offset capital barriers. Fuel for long-run growth also comes from regulatory moves that give clinical laboratories clearer pathways to adopt proteomic diagnostics, pushing hospitals and reference labs to modernize their analytical fleets.

North America Proteomics Market Trends and Insights

Escalating Adoption of Personalized Medicine

Precision oncology programs now embed deep-visual proteomics to guide therapy selection at the individual tumor-cell level. The FDA cleared four peptide-based therapeutics in 2024, demonstrating regulatory confidence in protein-driven interventions. Healthcare systems increasingly recognize that real-time protein signatures improve treatment prediction accuracy more than genomic markers alone, especially in cancers where expression profiles shift during disease progression. Demand therefore rises for high-sensitivity instruments able to quantify low-abundance proteins directly from clinical samples. These needs sustain premium pricing for novel Orbitrap and acoustic-ejection platforms that cut run times without sacrificing depth. As payers link reimbursement to measurable outcomes, laboratories prioritize assays that translate protein dynamics into actionable decisions, further lifting the North America proteomics market.

Surge in Proteomics-Specific Funding

Venture investors have made large follow-on commitments to companies combining live-cell imaging with AI analytics. Eikon's USD 351 million raise in February 2025 pushed the firm's valuation to USD 3.1 billion and signaled broad confidence in protein-tracking drug-discovery engines. Public support mirrors private enthusiasm: Canada's skills strategy projects 65,000 additional bioeconomy workers by 2029, including 16,140 roles focused on biomanufacturing. With new capital, start-ups generate proprietary interaction datasets at unprecedented scale, erecting entry barriers that established players must address through partnerships or acquisitions. High liquidity, coupled with clear clinical use-cases, sustains the funding wave that underpins expansion of the North America proteomics market.

High Capital Cost of Instruments

Flagship mass-spectrometry units can cost well above USD 1 million, a hurdle that delayed orders in 2024. Bio-Rad Laboratories saw its life-science sales slip 16.5% in Q2 2024 as customers deferred purchases, prompting the firm to guide full-year revenue down 2.5% to 4.0%. Smaller biotechs and academic centers lack balance-sheet flexibility, leading them to rent time at core facilities or engage service labs. Leasing smooths cash flow but raises lifetime operating expense. Rapid innovation also shortens depreciation cycles, forcing caution on buyers and trimming short-term growth for the North America proteomics market.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in High-Throughput MS Platforms

- Expansion of Biopharma Proteomics Spending

- Bioinformatics Talent Shortage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents captured 63.41% of the North America proteomics market share in 2024 because every experiment requires fresh antibodies, enzymes, buffers, and labeling kits. Suppliers lock in predictable revenue by bundling consumables with instruments. The software & services slice is much smaller, yet it delivers a 12.85% CAGR because laboratories must extract insights from high-volume data. Cloud platforms equipped with pretrained AI models simplify spectrum annotation, protein-protein interaction mapping, and clinical-trial report generation. Instruments command premium prices but represent a cyclical buy-decision. Vendors therefore tie service contracts to hardware to smooth cash flows and improve customer retention across the North America proteomics market.

Growth in software also reflects a pivot toward subscription models. Data analysis portals charge per sample or per month, turning unpredictable capital expenses into operating budgets. Managed-service firms now integrate LIMS, statistical pipelines, and regulatory-grade audit trails, letting understaffed hospitals gain modern capabilities without hiring full-time bioinformaticians. As data volumes swell, so does demand for encrypted cloud storage, backup, and cyber-security audits. Each of these trends adds momentum to the North America proteomics industry and lifts long-run platform value for developers who can enable seamless reagent-to-report workflows.

Mass spectrometry held 28.27% of the North America proteomics market size in 2024, reflecting decades of reliability, vast legacy datasets, and broad regulatory acceptance. High-resolution Orbitrap and time-of-flight systems now pair with foundation AI models that predict spectrum quality and post-translational modifications in real time. Next-generation sequencing platforms chart a 13.02% CAGR because vendors blend genomics, transcriptomics, and proteomics into single multi-omics reads. Illumina plans to commercialize spatial transcriptomics add-ons by 2026, combining its sequencers with NVIDIA GPUs to accelerate protein-structure insight within oncology studies.

Microfluidic sample-handling tools shrink reaction volumes, enabling low-cost point-of-care tests for infectious-disease proteotyping. Chromatography and capillary electrophoresis retain niche relevance for sample cleanup, while protein microarrays support high-throughput antibody discovery. Hybrid instruments that combine MS, NGS, and fluorescence-imaging modules reduce laboratory footprints and maximize asset utilization. Such convergence improves workflow efficiency, keeping end users loyal to suppliers that provide total solutions, thereby expanding the North America proteomics market.

The North America Proteomics Market Report is Segmented by Component (Instruments and More), Technology (Mass Spectrometry and More), Application (Drug Discovery & Development and More), End-User (Pharmaceutical & Biotechnology Companies and More), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Agilent Technologies

- Alamar Biosciences, Inc.

- Bioinformatics Solutions Inc.

- Bio-Rad Laboratories

- Bruker

- Creative Proteomics

- Danaher

- GE Healthcare

- Illumina

- Merck

- Nautilus Biotechnology

- Oxford Nanopore Technologies

- Promega

- QIAGEN

- Revvity, Inc.

- Seer

- Shimadzu

- SomaLogic

- Thermo Fisher Scientific

- Waters Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating adoption of personalized medicine

- 4.2.2 Surge in proteomics?specific funding

- 4.2.3 Breakthroughs in high-throughput MS platforms

- 4.2.4 Expansion of biopharma proteomics spending

- 4.2.5 AI-enabled proteogenomic decision tools

- 4.2.6 Field-deployable microfluidic sample-prep kits

- 4.3 Market Restraints

- 4.3.1 High capital cost of instruments

- 4.3.2 Bioinformatics talent shortage

- 4.3.3 Patent thickets on affinity reagents

- 4.3.4 Cyber-security risks in cloud multi-omics

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Component

- 5.1.1 Instruments

- 5.1.2 Reagents

- 5.1.3 Software and Services

- 5.2 By Technology

- 5.2.1 Mass Spectrometry

- 5.2.2 Spectroscopy

- 5.2.3 Chromatography

- 5.2.4 Next-Generation Sequencing

- 5.2.5 Protein Microarrays

- 5.2.6 Microfluidics

- 5.2.7 X-ray Crystallography

- 5.2.8 Other Technologies

- 5.3 By Application

- 5.3.1 Drug Discovery & Development

- 5.3.2 Clinical Diagnostics

- 5.3.3 Biomarker Discovery

- 5.3.4 Precision and Personalized Medicine

- 5.3.5 Agricultural & Environmental Proteomics

- 5.3.6 Other Applications

- 5.4 By End-user

- 5.4.1 Pharmaceutical & Biotechnology Companies

- 5.4.2 Academic & Research Institutes

- 5.4.3 Contract Research Organizations

- 5.4.4 Other End-users

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Agilent Technologies Inc.

- 6.4.2 Alamar Biosciences, Inc.

- 6.4.3 Bioinformatics Solutions Inc.

- 6.4.4 Bio-Rad Laboratories Inc.

- 6.4.5 Bruker Corporation

- 6.4.6 Creative Proteomics

- 6.4.7 Danaher Corporation

- 6.4.8 GE Healthcare

- 6.4.9 Illumina Inc.

- 6.4.10 Merck KGaA

- 6.4.11 Nautilus Biotechnology

- 6.4.12 Oxford Nanopore Technologies

- 6.4.13 Promega Corporation

- 6.4.14 QIAGEN N.V.

- 6.4.15 Revvity, Inc.

- 6.4.16 Seer Inc.

- 6.4.17 Shimadzu Corporation

- 6.4.18 SomaLogic Inc.

- 6.4.19 Thermo Fisher Scientific Inc.

- 6.4.20 Waters Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessmen