|

시장보고서

상품코드

1836671

손목관절 전치환술 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Total Wrist Replacement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

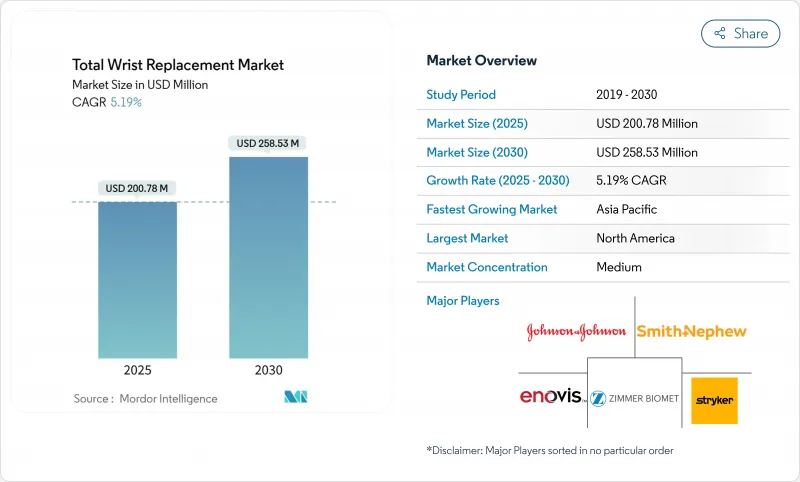

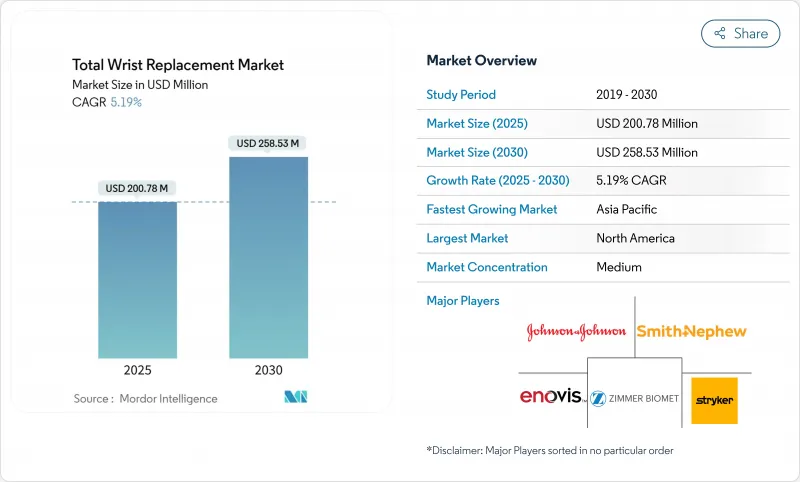

손목관절 전치환술 시장 규모는 2025년에 2억 78만 달러로 추정되고, 예측 기간(2025-2030년) CAGR 5.19%로 성장할 전망이며, 2030년에는 2억 5,853만 달러에 달할 것으로 예측되고 있습니다.

실험적 절차에서 일상적인 동작 유지 솔루션으로의 전환은 5년 생존율 90% 이상을 달성하는 4세대 임플란트를 반영한 것으로, 이 성능 수준은 외과의사의 폭넓은 채용을 촉진하는 동시에 융합 솔루션보다 기능 회복을 요구하는 환자 수요를 지원하고 있습니다. 주요 지급자의 일괄 지불 모델은 Medicare의 인공 관절 대체술의 에피소드 비용을 이미 20.8% 절감하고 있으며 외래 환자 경로에 유리한 비용을 시각화하고 외래수술센터(ASC)로 수술을 이행하도록 촉구합니다. 코발트 크롬 합금은 입증된 강도로 리드를 유지하지만, 외과의사가 금속 이온의 방출 위험을 최소화하기 위해 세라믹 구성 요소가 속도를 높이고 있습니다. 지역적으로는 북미가 수익의 기둥으로 계속되고 있지만, 중국, 일본, 인도에서 수술의 급속한 보급으로 아시아가 2030년까지 가장 급속히 확대하게 됩니다.

세계의 손목관절 전치환술 시장 동향 및 인사이트

류마티스 및 골관절염의 유병률 증가

류마티스 관절염은 미국에서 250만 명이 앓고 있으며, 손관절염은 일반 인구의 13.6%에서 발견되어 인공관절 치환술의 대상이 되는 임상 풀을 확대하고 있습니다. 인구 역학의 변화 및 앉아있는 노동 습관은 병태의 조기 발병을 초래하고 경제적으로 활동적인 젊은 환자의 치료 수요를 밀어 올리고 있습니다. 비교 연구는 관절 성형술이 합병증 프로파일이 약간 다르지만 관절 치환술보다 우수한 기능적 결과를 제공하는 것으로 확인되었으며 관절 성형술의 가치 제안이 강화되었습니다. 현재, 질병 개질성 항류마티스 요법은 관절의 완전성을 연장시키지만, 생존 기간이 길어짐에 따라, 평생에 걸쳐 관절의 움직임을 유지하기 위한 개입이 필요해지고 있습니다. 실제로 Universal Total Wrist 인공관절은 DASH(Disabilities of the Arm, Shoulder and Hand : 팔, 어깨, 손 장애) 점수를 29% 향상시켰고, 통증 점수를 66.3점에서 6.7점으로 감소시켰습니다.

4세대 모듈형 임플란트의 진보

4세대 시스템은 90%를 초과하는 4년 생존율을 실현하며, 1세대 장비에서 발견된 42%의 중기 결과를 능가합니다. 모듈식 트레이는 수술 중 외과의사가 컴포넌트의 크기를 조정할 수 있으므로 불일치 위험을 최소화하고 단계적 재치환을 용이하게 합니다. 예를 들어, Freedom 인공 관절은 8.7/10이라는 환자 만족도를 얻었지만 임플란트의 1/3에 X선 투과성이 보이며 연 1회 감시의 필요성을 강조하고 있습니다. 반구속 타원체 관절에 의한 강화된 운동학은 요골 수근 계면에 의해 균등하게 하중을 분산시킵니다. CoCrMo 합금과 Ti6Al4V 합금에 적용된 티타늄 질화물 코팅은 검출가능한 이온 방출을 실질적으로 제거하고 장기적인 생체적합성 우려에 부응합니다.

높은 수술비용 및 장비 비용과 제한된 상환금

미국에서는 손목관절 전치환술의 전국적 적용 결정이 아직 발표되지 않았기 때문에 외과의사는 사례별로 사전 승인을 받아야 합니다. 일부 민간 보험 회사는 류마티스의 적응 밖에서 실험적인 수술을 하고 환자의 처리 능력을 제한하는 제한적인 기준을 강제하고 있습니다. 인공 고관절이나 인공 슬관절에 비해 의료기기의 가격이 높아지는 것은 생산량이 적기 때문에 스케일 메리트가 적고, 규제 상의 장애물이 상품화 비용을 인상하고 있기 때문입니다. 일괄 지불 계약은 우수한 결과가 높은 컴포넌트를 정당화하지 않는 한 의료 제공업체를 임플란트 지출 감소로 향하게 합니다. 많은 신흥 시장에서는 국가 납부자가 틈새 시장의 손목 수술보다 더 많은 양의 정형외과 수술을 선호하기 때문에 상환에 대한 통합이 지연됩니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- 움직임 온존 절차에 대한 기호

- 외래 및 ASC 인공관절 치환술 확대

- 높은 재치환률 및 합병증률

부문 분석

손목의 전체 고정술은 2024년 매출의 65.17%를 차지했으며, 확실한 통증 통제와 예측 가능한 결합에 대한 외과의사의 신뢰를 보여줍니다. 이와는 대조적으로 인공관절 치환술은 CAGR 7.32%로 상승했는데, 이는 4세대 디바이스가 류마티스 코호트를 넘어 변형성 관절증이나 외상 후 적응증에도 내구성이 있음이 증명되어 후보층이 확대되었기 때문입니다. 3D 프린팅된 마이크로다공성 티타늄 보철물(3DMT-손목)은 통증을 66.3에서 6.7로 감소시키고 동시에 악력을 3배로 증가시켰습니다.

임상 메타 분석에 따르면 인공 관절 치환술의 합병증은 19%이며 류마티스 증례에서 고정술의 17%와 거의 유사합니다. Re-motion 시스템에 의해 달성된 97%의 7년 생존율은 그 진보를 강조하는 반면, 환자의 1/3은 여전히 2차 개입에 직면하고 있습니다. 인공지능에 의한 지침은 스크류의 궤적과 컴포넌트의 얼라인먼트를 밀리미터 레벨의 정밀도로 제공하여 재현성을 높이고 있습니다. 그 증거로 인공관절 치환술의 손목관절 전치환술 시장 규모는 2030년까지 다른 어떤 기술 분야보다 급속히 확대될 전망입니다.

지역별 분석

북미는 평균 에피소드 비용을 삭감하고 복잡한 손목 임플란트의 안정적인 상환을 실현하는 CJR 등 메디케어의 이니셔티브에 힘입어 2024년 매출 39.81%로 선두를 유지했습니다. 또한 FDA 510(k)의 명확화로 인해 임플란트 업그레이드 장애물이 낮아졌습니다. ASC의 확대는 지불자의 압력에 힘입어 환자의 안전 지표를 낮추지 않고 서비스 부위의 전환을 가속화하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)로 가장 빠른 9.39%를 기록합니다. 중국의 수술 건수가 많고 현지 제조 능력에 따라 국산 임플란트는 수입 임플란트보다 우위에 서서 가격 성능비가 극적으로 단축됩니다. 아시아태평양 손목 협회를 통한 지식 공유와 다국적 동료와의 교류로 수술 모범 사례가 급속히 확산되고 있습니다. 일본과 인도는 국민 보험 확대와 민간 병원 네트워크 덕분에 지역 수술 건수를 더욱 늘리고 있습니다.

유럽은 완만하고 꾸준한 성장을 이루고 있습니다. 이 시장은 생존율과 합병증의 지표를 벤치마킹하는 엄격한 레지스트리 피드백 루프에 따라 체계적인 채택으로 이익을 얻고 있습니다. 2024년 Enovis사의 LimaCorporate사의 8억 유로 인수 완료로 3D 프린팅 전문 지식이 각 대륙의 포트폴리오에 추가되어 트래비큘러 티타늄 디자인의 채용이 촉진되었습니다. 국경을 넘어서는 연구 컨소시엄은 범 EU 의료기기 지침과 결합되어 환자의 안전 의무를 지키면서 선진 임플란트를 위한 통합된 길을 제공하고 있다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 류마티스 및 골관절염의 유병률 상승

- 제4세대 모듈식 임플란트의 진보

- 관절 가동역 유지 수술에 대한 기호

- 외래 및 ASC 인공관절 치환술 확대

- 3D 프린터에 의한 환자 전용 기기 출현

- 성과에 보답하는 일괄 지불 모델

- 시장 성장 억제요인

- 높은 수술 비용과 장치 비용 및 한정된 상환금

- 높은 재치환율 및 합병증률

- 기기 철거 후의 규제 상 주의

- 신규 바이오머티리얼의 장기적 근거 부족

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액(달러)

- 기술별

- 손목 전치환술(TWR)

- 손목 전치환술(TWF)

- 재료별

- 코발트 크롬 합금

- 티타늄 합금

- 스테인레스 스틸

- 세라믹 베이스 부품

- 폴리머 부품

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 정형외과 전문 클리닉

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Acumed LLC

- Small Bone Innovations Inc.

- Zimmer Biomet Holdings Inc.

- Integra LifeSciences Holdings Corp.

- DePuy Synthes(Johnson & Johnson)

- Stryker Corporation

- Enovis(DJO Global)

- Medartis AG

- Skeletal Dynamics LLC

- Anika Therapeutics Inc.

- CONMED Corporation

- Extremity Medical LLC

- Wright Medical Group NV

- Smith & Nephew plc

- Orthofix Medical Inc.

- KeriMedical SA

- Avanta Orthopaedics

- MatOrtho Limited

- Signature Orthopaedics

- Stanmore Implants

- Biotechni SAS

- LimaCorporate SpA

제7장 시장 기회 및 전망

AJY 25.10.27The Total Wrist Replacement Market size is estimated at USD 200.78 million in 2025, and is expected to reach USD 258.53 million by 2030, at a CAGR of 5.19% during the forecast period (2025-2030).

The transition from experimental procedures to routine motion-preserving solutions reflects fourth-generation implants that achieve more than 90% five-year survivorship, a performance level that encourages wider surgeon adoption while supporting patient demand for functional recovery over fusion solutions. Bundled payment models across major payers have already trimmed Medicare joint-replacement episode costs by 20.8%, creating cost visibility that favors outpatient pathways and drives procedure migration to ambulatory surgical centers. Material science also propels differentiation: cobalt-chromium alloys keep the lead through proven strength, yet ceramic components gain pace as surgeons look to minimize metal-ion release risks. Geographically, North America remains the revenue anchor, but rapid procedure uptake in China, Japan, and India positions Asia for the fastest expansion through 2030.

Global Total Wrist Replacement Market Trends and Insights

Rising Prevalence of Rheumatoid & Osteoarthritis

Rheumatoid arthritis affects 2.5 million individuals in the United States, and wrist arthritis is present in 13.6% of the general population, expanding the clinical pool eligible for arthroplasty. Shifting demographics and sedentary work habits bring the earlier onset of pathology that pushes treatment demand among younger, economically active patients. Comparative studies confirm that arthroplasty delivers better functional results than arthrodesis in rheumatoid cohorts despite slightly different complication profiles, strengthening the procedure's value proposition. Disease-modifying antirheumatic therapies now prolong joint integrity, yet prolonged survival raises the lifetime need for motion-preserving interventions. In practice, the Universal Total Wrist prosthesis improved Disabilities of the Arm, Shoulder and Hand (DASH) scores by 29% while cutting pain scores from 66.3 to 6.7, an outcome that resonates with patient-reported priorities.

Advancements in 4th-Generation Modular Implants

Fourth-generation systems provide four-year survival rates above 90%, dwarfing the 42% mid-term results seen in first-generation devices. Modular trays let surgeons tailor component sizes intraoperatively, minimizing malalignment risk and enabling easier staged revisions. The Freedom prosthesis, for instance, receives patient satisfaction scores of 8.7/10, but radiographic lucency in one-third of implants underlines the need for annual surveillance. Enhanced kinematics via semi-constrained ellipsoidal joints distribute load more evenly across the radiocarpal interface. Titanium-nitride coatings on CoCrMo and Ti6Al4V alloys virtually eliminate detectable ion release, responding to long-term biocompatibility concerns

High Procedure & Device Cost / Limited Reimbursement

U.S. payers have yet to publish national coverage determinations for total wrist arthroplasty, obliging surgeons to secure prior authorization case by case. Several private insurers label the operation experimental outside rheumatoid indications, enforcing restrictive criteria that limit patient throughput. Device prices remain elevated relative to hip and knee counterparts because smaller volumes offer fewer economies of scale, while regulatory hurdles raise commercialization costs. Bundled payment contracts push providers toward lower implant expenditures unless superior outcomes justify premium components. In many emerging markets, state payers favor high-volume orthopedic interventions over niche wrist procedures, delaying reimbursement inclusion.

Other drivers and restraints analyzed in the detailed report include:

- Preference for Motion-Preserving Procedures

- Expansion of Outpatient/ASC Arthroplasty

- High Revision & Complication Rates

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Total Wrist Fusion represented 65.17% revenue in 2024, illustrating surgeon trust in reliable pain control and predictable union. In contrast, arthroplasty rises at a 7.32% CAGR as fourth-generation devices prove durable beyond the rheumatoid cohort and into osteoarthritis as well as post-traumatic indications, enlarging the candidate base. The 3D-printed microporous titanium prosthesis (3DMT-Wrist) lowered pain from 66.3 to 6.7 while tripling grip strength, reinforcing momentum behind motion-preserving platforms.

Clinical meta-analyses place arthroplasty complications at 19%, nearly matching the 17% rate seen in fusion among rheumatoid cases, eroding historical perceptions of high failure risk. Seven-year survival of 97% achieved by the Re-motion system underscores progress, though one-third of recipients still face secondary interventions. Artificial-intelligence guidance now offers millimeter-level accuracy on screw trajectory and component alignment, enhancing reproducibility. As evidence solidifies, the total wrist replacement market size for arthroplasty is set to expand faster than any other technology segment through 2030.

The Total Wrist Replacement Market is Segmented by Technology (Total Wrist Replacement, Total Wrist Fusion), Material (Cobalt-Chromium Alloys, Titanium Alloys, Stainless Steel, and More), End User (Hospitals, Ambulatory Surgical Centers, Specialty Orthopedic Clinics), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintains leadership with 39.81% revenue in 2024, supported by Medicare initiatives such as CJR that reduce average episode costs and create stable reimbursement for complex wrist implants. Consolidated centers of excellence draw volume nationally, while FDA 510(k) clarity lowers the hurdle for incremental implant upgrades. ASC expansion, driven by payer pressure, accelerates site-of-service conversions without diminishing patient safety metrics.

Asia-Pacific records the fastest 9.39% CAGR through 2030. China's high procedure volume, together with local manufacturing capability, now positions domestic implants ahead of imported counterparts, dramatically tightening price-performance ratios. Knowledge-sharing through the Asia Pacific Wrist Association plus multinational fellowship exchanges quickly diffuse surgical best practices. Japan and India further elevate regional numbers thanks to national insurance expansion and private-sector hospital networks.

Europe posts moderate, steady growth. The market benefits from methodical adoption following rigorous registry feedback loops that benchmark survivorship and complication metrics. The completion of Enovis's EUR 800 million purchase of LimaCorporate in 2024 brought additional 3D-printed expertise into continental portfolios, supporting take-up of trabecular titanium designs. Cross-border research consortia, combined with pan-EU medical-device directives, provide an integrated pathway for advanced implants while preserving patient safety obligations.

- Acumed

- Small Bone Innovations Inc.

- Zimmer Biomet

- Integra LifeSciences Holdings Corp.

- Johnson & Johnson

- Stryker

- Enovis

- Medartis

- Skeletal Dynamics LLC

- Anika Therapeutics

- Conmed

- Extremity Medical LLC

- Wright Medical Group

- Smiths Group

- Orthofix

- KeriMedical SA

- Avanta Orthopaedics

- MatOrtho Limited

- Signature Orthopaedics

- Stanmore Implants

- Biotechni SAS

- LimaCorporate S.p.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Rheumatoid & Osteoarthritis

- 4.2.2 Advancements in 4th-Generation Modular Implants

- 4.2.3 Preference for Motion-Preserving Procedures

- 4.2.4 Expansion of Outpatient/ASC Arthroplasty

- 4.2.5 Emergence of 3-D-Printed Patient-Specific Devices

- 4.2.6 Bundled-Payment Models Rewarding Outcomes

- 4.3 Market Restraints

- 4.3.1 High Procedure & Device Cost / Limited Reimbursement

- 4.3.2 High Revision & Complication Rates

- 4.3.3 Regulatory Caution After Device Withdrawals

- 4.3.4 Sparse Long-Term Evidence for Novel Biomaterials

- 4.4 Technological Outlook

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Total Wrist Replacement (TWR)

- 5.1.2 Total Wrist Fusion (TWF)

- 5.2 By Material

- 5.2.1 Cobalt-Chromium Alloys

- 5.2.2 Titanium Alloys

- 5.2.3 Stainless Steel

- 5.2.4 Ceramic-based Components

- 5.2.5 Polymer Components

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Orthopedic Clinics

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Acumed LLC

- 6.3.2 Small Bone Innovations Inc.

- 6.3.3 Zimmer Biomet Holdings Inc.

- 6.3.4 Integra LifeSciences Holdings Corp.

- 6.3.5 DePuy Synthes (Johnson & Johnson)

- 6.3.6 Stryker Corporation

- 6.3.7 Enovis (DJO Global)

- 6.3.8 Medartis AG

- 6.3.9 Skeletal Dynamics LLC

- 6.3.10 Anika Therapeutics Inc.

- 6.3.11 CONMED Corporation

- 6.3.12 Extremity Medical LLC

- 6.3.13 Wright Medical Group NV

- 6.3.14 Smith & Nephew plc

- 6.3.15 Orthofix Medical Inc.

- 6.3.16 KeriMedical SA

- 6.3.17 Avanta Orthopaedics

- 6.3.18 MatOrtho Limited

- 6.3.19 Signature Orthopaedics

- 6.3.20 Stanmore Implants

- 6.3.21 Biotechni SAS

- 6.3.22 LimaCorporate S.p.A.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment