|

시장보고서

상품코드

1836684

순환종양세포(CTC) 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Circulating Tumor Cells (CTC) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

순환종양세포(CTC) 시장은 2025년에 128억 5,000만 달러로 추정되고, 2025-2030년 CAGR 14.56%로 성장할 전망이며, 2030년에는 253억 6,000만 달러에 이를 전망입니다.

암 전문의가 침습적인 조직 생검에서 종양의 불균일성을 파악하고, 내성 패턴을 추적하며, 신속한 치료 변경을 이끄는 실시간 리퀴드 바이옵시 툴로 이행함에 따라 수요가 높아지고 있습니다. 생존율을 저하시키지 않으면서 높은 세포 포획 수율을 보장하는 마이크로플루이딕스 플랫폼이 기세를 늘리고 인공지능 영상 분석이 보다 신속한 해석과 정밀도 향상을 촉진합니다. 아시아태평양은 암 이환율 상승, 공공 검진 프로그램, 벤처 캐피탈의 자금 조달에 의해 기술 도입 사이클이 단축되기 때문에 가장 강한 상승 경향을 보이고 있습니다. 전략 리더는 CTC 분석이 동반진단제로 통합되어 장기 시약 수요를 창출하고 병원 네트워크 전체에서 순환종양세포(CTC) 시장을 고정화하도록 제약 스폰서와의 제휴를 지지합니다.

세계의 순환종양세포(CTC) 시장 동향 및 인사이트

암 유병률 증가

암 이환율은 2050년까지 76.6%, 사망률은 89.7% 상승할 것으로 예측되며, 사망률 대 이환율의 비율이 2.5배나 되는 개발도상 지역에서의 부담이 가장 커집니다. 미국에서는 2025년에 204만 명이 새롭게 발병한 것으로 추정되고, 61만 8,120명이 사망할 것으로 예측되고 있습니다. 이 추세는 정기적인 영상 진단보다 조기에 경고를 내리고 치료 효과를 신속하게 추적할 수 있는 CTC 검사의 채택을 촉진합니다. 병원과 외래 센터는 이러한 검사를 정기적인 후속 일정에 통합하여 순환종양세포(CTC) 시장 전반의 경상 수익을 높이고 있습니다.

정밀의료 및 동반자 진단에 대한 수요 증가

FDA는 60개가 넘는 동반진단제를 허가하고 있으며, 대부분은 리퀴드 바이옵시 마커를 포함하고 있습니다. UnitedHealthcare는 현재 조직 채취가 불가능한 경우 CTC 검사에 보험을 적용하고 있습니다. 온전한 세포는 각 치료 주기에서 치료 선택의 지침이 되는 표현형과 유전자형의 특징을 밝히기 위해 임상가는 평가하고 있으며 순환종양세포(CTC) 시장에서 플랫폼의 관련성을 강화하고 있습니다.

CTC 장비 및 소모품의 높은 비용

자동화 플랫폼의 설비 투자액은 25-50만 달러로, 시약 팩은 1 검정당 1,000 달러를 넘는 경우가 많습니다. 이러한 비용은 많은 공립 병원에서 예산 한도를 초과하므로 도입이 지연됩니다. 벤더는 임대 계약 및 시약 임대 모델에서 스티커 충격에 대항하고 있지만 경제적 장애물은 여전히 남아 있으며 순환종양세포(CTC) 시장에서 단기적인 흡수의 짐이 되고 있습니다.

보고서에서 분석된 기타 촉진요인 및 억제요인

- CTC 분리 및 검출에 있어서의 기술적 개선 확대

- 벤처캐피탈 및 정부 자금

- 기술적 복잡성 및 표준화의 부족

부문 분석

검출 및 농축 시스템은 2024년 순환종양세포(CTC) 시장 수익의 59.2%를 창출했습니다. 이 플랫폼은 수십억 개의 혈액 세포에서 희귀 종양 세포를 분리하기 때문에 모든 워크 플로우의 백본을 형성합니다. 검출 기술의 순환종양세포(CTC) 시장 규모는 마이크로플루이딕스칩 설계가 보다 높은 생존율로 온전한 세포를 포착하기 때문에 꾸준히 상승할 전망입니다. 새로운 레이저 유도 전방 이동 정밀 여과는 생존율 81.3%에서 88%의 포착률을 달성하고 단일 세포 시퀀싱 연구를 지원합니다.

해석 및 특성 분석 부문은 2030년까지 연평균 복합 성장률(CAGR) 16.96%로 가장 급성장이 전망됩니다. 단일 셀 멀티오믹스의 진보는 개별 CTC에서 DNA, RNA, 단백질의 동시 프로파일링을 가능하게 하고, 조직 생검에서는 간과되기 쉬운 내성 촉진 인자를 밝혀줍니다. AI의 이미지 분류 기능은 소요 시간을 단축하고, 수동으로 검토 오류를 줄이며, 지역 검사실이 고급 분석에 액세스할 수 있도록 합니다. 이러한 기능을 결합하면 순환종양세포(CTC) 시장에서 임상 가치 제안을 깊게 하고 프리미엄 가격을 유지할 수 있습니다.

키트 및 시약은 2024년 순환종양세포(CTC) 시장 수익의 63.54%를 차지했습니다. 이는 모든 검사에 단일 사용 항체 칵테일, 자기 비드, 염색 염료가 필요하기 때문입니다. 제조업체 각사는 상피간엽전환 마커를 타겟으로 한 시약 번들을 전개하여 전이성 질환에서의 유용성을 확대하고 있습니다.

소프트웨어 및 서비스는 2030년까지 연평균 복합 성장률(CAGR)이 15.84%로 가장 빠르게 상승할 것으로 예측됩니다. 클라우드 플랫폼은 안전한 이미지 라이브러리, 머신러닝 모델 및 자동 보고서 대시보드를 호스팅합니다. 학술 그룹은 주석이 달린 세포 이미지를 공유하여 알고리즘을 향상시키고 낮은 신호 샘플에서의 민감도를 향상시킵니다. 구독 애널리틱스는 순환종양세포(CTC) 시장에서 새로운 수익층을 창출하여 고객의 포위를 강화합니다.

지역 분석

북미는 2024년 순환종양세포(CTC) 시장 수익의 44.28%를 차지했습니다. 이 지역은 정교한 종양 센터, 견고한 지불자 프레임 워크 및 광범위한 조사 자금으로부터 이익을 얻고 있습니다. FDA는 동반진단 약물 목록을 지속적으로 확대하고 병원에서 채용을 촉구하고 있습니다. 2025년에 미국에서 새롭게 200만 명의 암 환자가 발생할 것으로 추정되고, 암 이환율의 상승은 안정된 검사량을 보증하고 있습니다. 캐나다에서는 영상 진단 비용을 상쇄하기 위해 액체 생체의 상환을 시험적으로 수행하는 주 프로그램이 있으며 유사한 동향을 보여줍니다.

유럽은 2위입니다. 유럽 리퀴드 바이옵시 학회와 같은 설문조사 네트워크는 독일, 프랑스, 영국 전역에서 프로토콜의 표준화와 숙련도 시험을 조정하고 있습니다. 이들 국가에서는 관민의 컨소시엄을 조직하고, 방사선 데이터와 함께 CTC 수를 평가하며, 반응 기준을 개량하고 있습니다. 동유럽의 보건부는 종양과를 근대화하고 턴키 CTC 분석기의 수입이 증가하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 16.06%로 가장 빠르게 성장할 전망입니다. 중국은 국가자본과 벤처 자본을 마이크로플루이딕스 제조로 향하고 국내 병원 플랫폼 비용을 낮추고 있습니다. 홍콩성 대학교의 마이크로플루이딕스 시스템은 이미 50개 병원에 널리 퍼져 있으며 더 많은 지역 개발을 촉진하고 있습니다. 일본과 한국은 국립암센터에 연속 원심 칩을 도입하고 인도의 민간 연구소는 재대여 모델에 투자하여 접근을 확대하고 있습니다. 정부의 스크리닝 의무화와 인구 규모는 순환종양세포(CTC) 시장 전체의 성장 가능성을 높이고 있습니다.

중동 및 아프리카, 남미는 새로운 비즈니스 기회입니다. 사우디아라비아와 아랍에미리트(UAE)은 국가 보건 전략의 일환으로 CTC 스위트를 갖춘 암 전문 기관을 건설하고 있습니다. 브라질은 상파울루와 리오데자네이루의 주요 암 전문 병원에 리퀴드 바이옵시 모듈을 추가했습니다. 국제 원조 프로그램은 소형 CTC 분석 장비와 교육 워크숍을 번들로 진단의 공정성을 향상시키고 장기적인 확장을 위한 기반을 구축했습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 암의 유병률 증가

- 정밀의료 및 동반자 진단에 대한 수요 증가

- CTC 분리 및 검출의 기술적 향상

- 암 진단에 대한 벤처 캐피탈 및 정부 자금 확대

- AI 대응 마이크로플루이딕스 칩 및 싱글 셀 멀티 오믹스 시퀀싱

- 시장 성장 억제요인

- CTC 장치 및 소모품의 고비용

- 기술적 복잡성 및 표준화의 부족

- ctDNA 및 기타 리퀴드 바이옵시 분석물에 의한 경쟁 위협

- 신흥 시장에서의 인식 및 숙련 노동력 부족

- 밸류체인 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모 및 성장 예측 : 금액

- 기술별

- CTC 농축법

- 긍정적인 풍부

- 네거티브 인리치먼트

- 사이즈 베이스 분리

- 밀도 기반 분리

- 면역 자기 분리

- 마이크로플루이딕스 칩 기반

- 기타 농축법

- CTC 검출법

- 면역 세포 화학 기술

- 분자(RNA) 기반 기술

- 이미징 기반 기술

- PCR 기반 기술

- SERS 기반 기술

- 기타 검출법

- CTC 분석 및 특성 분석

- 단일 셀 시퀀싱

- 단백질 발현 분석

- 후성적 프로파일링

- CTC 농축법

- 제품별

- 키트 및 시약

- 기기 및 장치

- 채혈관

- 소프트웨어 및 서비스

- 검체별

- 혈액

- 골수

- 기타 체액(수액, 소변)

- 용도별

- 임상

- 조기 암 스크리닝

- 예후 예측 바이오마커

- 치료 모니터링 및 최소 잔존 병변

- 연구

- 의약품 개발 및 동반자 진단

- 암 줄기세포 및 EMT 연구

- 기타 용도

- 임상

- 최종 사용자별

- 병원 및 클리닉

- 진단 실험실

- 연구 및 학술기관

- 바이오 제약 회사

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- ACROBiosystems

- Advanced Cell Diagnostics, Inc.

- ANGLE plc(Parsortix)

- Biolidics Limited

- Bio-Techne

- BioView

- Cell Microsystems(Fluxion Biosciences, Inc.)

- CellCarta

- Creatv MicroTech, Inc.

- Exact Sciences Corporation

- LungLIfe AI, Inc.

- Menarini Silicon Biosystems

- Miltenyi Biotec

- NeoGenomics Laboratories

- Oncocyte Corporation

- Precision Medicine Group, LLC(ApoCell, Inc.)

- QIAGEN

- RareCyte, Inc.

- Sysmex Corporation(Sysmex Inostics GmbH)

- Thermo Fisher Scientific Inc.

- Yishan Biotechnology Co., Ltd.(Surexam)

제7장 시장 기회 및 전망

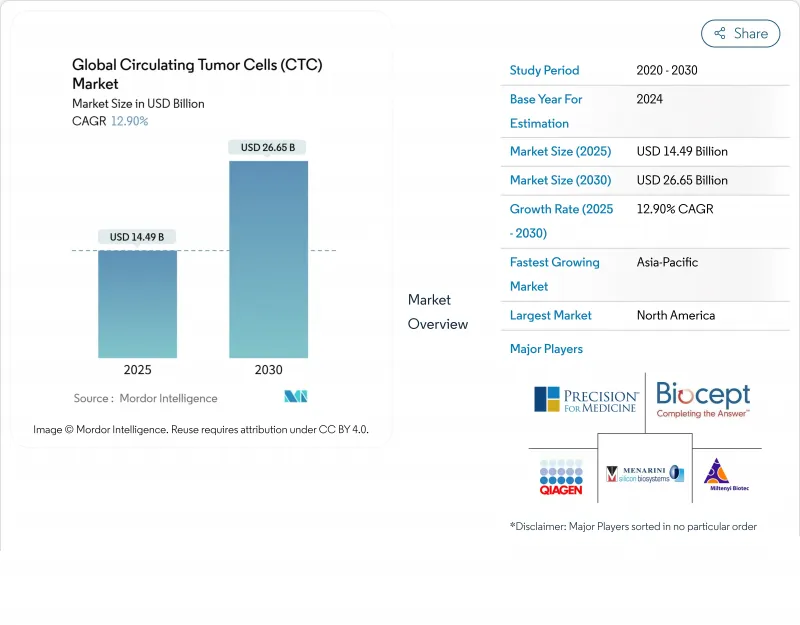

AJY 25.10.27The circulating tumor cells market stands at USD 12.85 billion in 2025 and is on track to reach USD 25.36 billion by 2030, supported by a 14.56% CAGR across 2025-2030.

Demand rises as oncologists shift from invasive tissue biopsies to real-time liquid biopsy tools that capture tumor heterogeneity, trace resistance patterns, and guide rapid therapy changes. Momentum builds around microfluidic platforms that secure higher cell-capture yields without compromising viability, while artificial-intelligence image analysis drives faster interpretation and better accuracy. Asia Pacific registers the strongest uptrend because rising cancer incidence, public screening programs, and venture capital funding shorten technology adoption cycles. Strategy leaders favor alliances with pharmaceutical sponsors so that CTC assays become embedded companion diagnostics, creating long-term reagent demand and locking in the circulating tumor cells market across hospital networks.

Global Circulating Tumor Cells (CTC) Market Trends and Insights

Increasing Prevalence of Cancer

Cancer incidence is projected to climb 76.6% and deaths 89.7% by 2050, with the burden most acute in developing regions where mortality-to-incidence ratios can be 2.5 times higher. The United States anticipates 2.04 million new cases and 618,120 deaths in 2025. This trend fuels adoption of CTC tests that deliver early alerts and track therapeutic efficacy more quickly than periodic imaging. Hospitals and outpatient centers integrate these assays into routine follow-up schedules, boosting recurring revenues across the circulating tumor cells market.

Rising Demand for Precision Medicine and Companion Diagnostics

The FDA lists more than 60 cleared companion diagnostics, many of which incorporate liquid biopsy markers. UnitedHealthcare now reimburses CTC tests when tissue sampling is not feasible. Clinicians value intact cells because they reveal phenotypic and genotypic traits that guide therapy selection at each treatment cycle, reinforcing platform relevance in the circulating tumor cells market.

High Cost of CTC Instruments and Consumables

Capital investments for automated platforms range between USD 250,000 and USD 500,000 and reagent packs often exceed USD 1,000 per assay. These expenses exceed budget ceilings in many public hospitals, delaying adoption. Vendors combat sticker shock with leasing contracts and reagent-rental models, yet the economic hurdle persists and weighs on near-term uptake in the circulating tumor cells market.

Other drivers and restraints analyzed in the detailed report include:

- Technological Improvements in CTC Isolation and Detection

- Expanding Venture Capital and Government Funding

- Technical Complexity and Lack of Standardization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Detection and enrichment systems generated 59.2% of circulating tumor cells market revenue in 2024. These platforms form the backbone of every workflow because they separate rare tumor cells from billions of blood cells. The circulating tumor cells market size for detection technologies is poised to rise steadily as microfluidic chip designs capture intact cells with higher viability. Novel laser-induced forward-transfer microfiltration reaches 88% capture with 81.3% viability, supporting single-cell sequencing studies.

The analysis/characterization segment grows the fastest at a 16.96% CAGR to 2030. Advances in single-cell multi-omics allow simultaneous DNA, RNA, and protein profiling in individual CTCs revealing drivers of resistance that tissue biopsies may overlook. AI image classifiers shorten turnaround times and reduce manual review errors, making advanced analytics accessible to community labs. Together these capabilities deepen the clinical value proposition and sustain premium pricing inside the circulating tumor cells market.

Kits and reagents held 63.54% of circulating tumor cells market revenue in 2024 because every test requires single-use antibody cocktails, magnetic beads, and staining dyes. Manufacturers roll out reagent bundles targeting epithelial-mesenchymal transition markers which expands utility across metastatic disease.

Software and services rise the quickest at a 15.84% CAGR through 2030. Cloud platforms host secure image libraries, machine-learning models, and automated reporting dashboards. Academic groups share annotated cell images to refine algorithms which improves sensitivity in low-signal samples. Subscription analytics create fresh revenue layers and reinforce customer lock-in within the circulating tumor cells market.

The Circulating Tumor Cells (CTC) Market Report is Segmented by Technology (CTC Enrichment Methods, CTC Analysis/Characterization), Product (Kits and Reagents, Instruments and Devices, Blood Collection Tubes, Software and Services), Specimen (Blood, Bone Marrow, and More), Application (Clinical, Research, and More), End User (Hospitals and Clinics, Diagnostic Laboratories, Research & Academic Institutes, and More), and Geography.

Geography Analysis

North America commanded 44.28% of circulating tumor cells market revenue in 2024. The region benefits from sophisticated oncology centers, robust payer frameworks, and wide research funding. The FDA continually enlarges its companion diagnostic list which inspires hospital adoption. Rising cancer incidence, projected at two million new US cases in 2025, ensures consistent test volume. Canada shows parallel trends with provincial programs piloting liquid biopsy reimbursement to offset imaging costs.

Europe ranks second. Research networks like the European Liquid Biopsy Society coordinate protocol standardization and proficiency testing across Germany, France, and the United Kingdom. These countries host public-private consortia that evaluate CTC counts alongside radiology data to refine response criteria. Eastern European health ministries modernize oncology departments and increasingly import turnkey CTC analyzers which lifts regional revenues within the circulating tumor cells market.

Asia Pacific is the fastest climber, locked on a 16.06% CAGR to 2030. China directs state and venture capital toward microfluidic manufacturing which lowers platform cost for domestic hospitals. The City University of Hong Kong microfluidics system has already spread to fifty hospitals and inspires further provincial rollouts. Japan and South Korea incorporate continuous centrifugal chips in national cancer centers, while India's private labs invest in reagent-rental models to expand access. Government screening mandates and population size amplify growth potential across the circulating tumor cells market.

The Middle East and Africa along with South America represent emerging opportunities. Saudi Arabia and the United Arab Emirates build specialist cancer institutes equipped with CTC suites as part of national health strategies. Brazil adds liquid biopsy modules to leading oncology hospitals in Sao Paulo and Rio de Janeiro. International aid programs bundle compact CTC analyzers with training workshops to improve diagnostic equity and lay the foundation for longer-term expansion.

- Acro Biosystems

- Advanced Cell Diagnostics, Inc.

- ANGLE plc (Parsortix)

- Biolidics Limited

- Bio-Techne

- BioView

- Cell Microsystems (Fluxion Biosciences, Inc.)

- CellCarta

- Creatv MicroTech, Inc.

- Exact Sciences

- LungLIfe AI, Inc.

- Menarini

- Miltenyi Biotec

- NeoGenomics Laboratories

- Oncocyte Corporation

- Precision Medicine Group, LLC (ApoCell, Inc.)

- QIAGEN

- RareCyte, Inc.

- Sysmex Corporation (Sysmex Inostics GmbH)

- Thermo Fisher Scientific

- Yishan Biotechnology Co., Ltd. (Surexam)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Prevalence of Cancer

- 4.2.2 Rising Demand for Precision Medicine and Companion Diagnostics

- 4.2.3 Technological Improvements in CTC Isolation and Detection

- 4.2.4 Expanding Venture Capital and Government Funding for Oncology Diagnostics

- 4.2.5 AI-Enabled Microfluidic Chips and Single-Cell Multi-Omics Sequencing

- 4.3 Market Restraints

- 4.3.1 High Cost of CTC Instruments and Consumables

- 4.3.2 Technical Complexity and Lack of Standardization

- 4.3.3 Competitive Threat from ctDNA and Other Liquid Biopsy Analytes

- 4.3.4 Limited Awareness and Skilled Workforce in Emerging Markets

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Technology

- 5.1.1 CTC Enrichment Methods

- 5.1.1.1 Positive Enrichment

- 5.1.1.2 Negative Enrichment

- 5.1.1.3 Size-Based Isolation

- 5.1.1.4 Density-Based Separation

- 5.1.1.5 Immunomagnetic Separation

- 5.1.1.6 Microfluidic Chip-Based

- 5.1.1.7 Other Enrichment Methods

- 5.1.2 CTC Detection Methods

- 5.1.2.1 Immunocytochemical Technology

- 5.1.2.2 Molecular (RNA)-Based Technology

- 5.1.2.3 Imaging-Based Technology

- 5.1.2.4 PCR-Based Technology

- 5.1.2.5 SERS-Based Technology

- 5.1.2.6 Other Detection Methods

- 5.1.3 CTC Analysis/Characterization

- 5.1.3.1 Single-Cell Sequencing

- 5.1.3.2 Protein Expression Analysis

- 5.1.3.3 Epigenetic Profiling

- 5.1.1 CTC Enrichment Methods

- 5.2 By Product

- 5.2.1 Kits & Reagents

- 5.2.2 Instruments and Devices

- 5.2.3 Blood Collection Tubes

- 5.2.4 Software and Services

- 5.3 By Specimen

- 5.3.1 Blood

- 5.3.2 Bone Marrow

- 5.3.3 Other Body Fluids (CSF, Urine)

- 5.4 By Application

- 5.4.1 Clinical

- 5.4.1.1 Early Cancer Screening

- 5.4.1.2 Prognostic and Predictive Biomarkers

- 5.4.1.3 Therapy Monitoring and Minimal Residual Disease

- 5.4.2 Research

- 5.4.2.1 Drug Development and Companion Diagnostics

- 5.4.2.2 Cancer Stem Cell and EMT Studies

- 5.4.3 Other Applications

- 5.4.1 Clinical

- 5.5 By End User

- 5.5.1 Hospitals and Clinics

- 5.5.2 Diagnostic Laboratories

- 5.5.3 Research and Academic Institutes

- 5.5.4 Biopharmaceutical Companies

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 ACROBiosystems

- 6.4.2 Advanced Cell Diagnostics, Inc.

- 6.4.3 ANGLE plc (Parsortix)

- 6.4.4 Biolidics Limited

- 6.4.5 Bio-Techne

- 6.4.6 BioView

- 6.4.7 Cell Microsystems (Fluxion Biosciences, Inc.)

- 6.4.8 CellCarta

- 6.4.9 Creatv MicroTech, Inc.

- 6.4.10 Exact Sciences Corporation

- 6.4.11 LungLIfe AI, Inc.

- 6.4.12 Menarini Silicon Biosystems

- 6.4.13 Miltenyi Biotec

- 6.4.14 NeoGenomics Laboratories

- 6.4.15 Oncocyte Corporation

- 6.4.16 Precision Medicine Group, LLC (ApoCell, Inc.)

- 6.4.17 QIAGEN

- 6.4.18 RareCyte, Inc.

- 6.4.19 Sysmex Corporation (Sysmex Inostics GmbH)

- 6.4.20 Thermo Fisher Scientific Inc.

- 6.4.21 Yishan Biotechnology Co., Ltd. (Surexam)

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment