|

시장보고서

상품코드

1842417

재조합 DNA 기술 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Recombinant DNA (rDNA) Technology - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

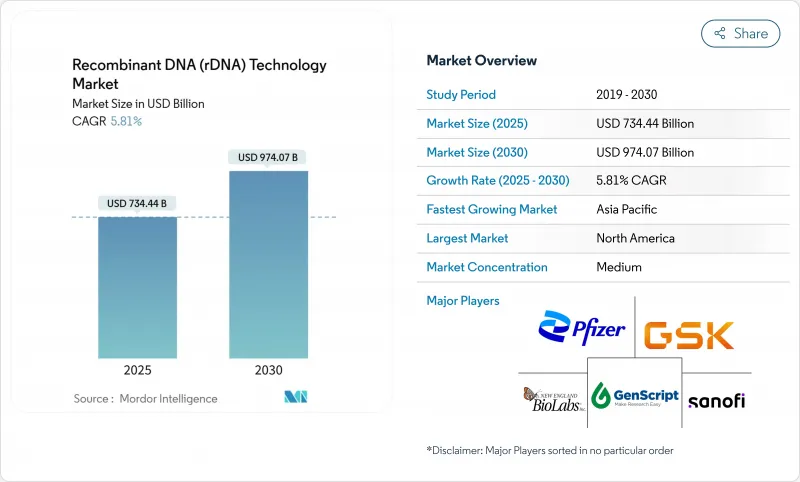

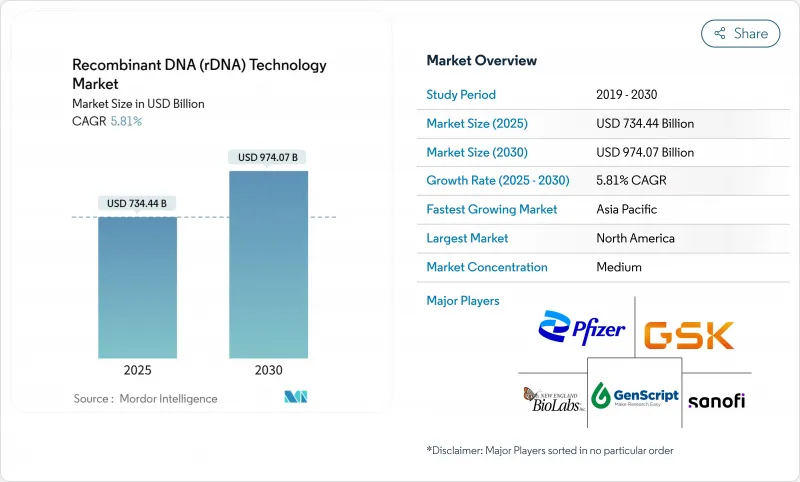

재조합 DNA 기술 시장은 2025년에 7,344억 4,000만 달러에 이르고, CAGR 5.81%를 나타내 2030년에는 9,740억 7,000만 달러에 달할 것으로 예상됩니다.

재조합 단백질 치료제에 대한 수요, CRISPR 비용의 가속도 저하, AI를 활용한 단백질 설계의 주류화에 의해 업계 경제가 계속 재구축되고 소규모 혁신자의 진입 장벽이 저하되는 한편, 생산 거점을 근대화하는 기존 기업은 보상됩니다. 단일 청소년 바이오리액터 및 플라스미드 마이크로팩토리의 가격 하락으로 개발자는 비용이 많이 드는 라인을 전환하지 않고도 치료와 농업 프로젝트 사이를 오가며 식품, 사료 및 환경 서비스로 포트폴리오를 확대하고 있습니다. 북미는 여전히 자금조달과 초기 단계 임상시험을 지지하고 있지만, 아시아태평양은 보다 빠른 속도로 생산 능력을 도입하고 있으며, 역사적인 기술 격차를 줄이고 세계 라이센시에 대한 지정학적 위험을 줄이는 현지 공급망을 육성하고 있습니다. 제약 대기업, 농업 대기업, 유전자 치료 전용 CDMO가 같은 벡터 원료와 규제의 대역폭을 둘러싸고 경쟁하기 때문에 경쟁이 격화되고 있습니다.

세계의 재조합 DNA 기술 시장 동향과 인사이트

CRISPR-Cas의 비용 곡선은 계속 하강

뉴클레아제 편집 키트에 대한 접근의 확대, 보다 저렴한 가이드 RNA 합성, 벡터 수율 증가로 인해 CRISPR 요법의 완전한 로딩 비용이 급격히 감소하고 있습니다. 겸상 적혈구증에서 CASGEVY의 임상적 성공은 환자 1인당 300만 달러에 가까운 초기 가격에도 이 치료법의 효능을 입증했습니다. 알데브론은 이후 개별화된 CRISPR의 생산 기간을 6개월로 단축하여 공급망이 성숙함에 따라 사이클 타임 향상이 현실적임을 입증했습니다. 2024년 미국에서 과거 최다 14건의 심사 지정이 이루어진 것은 규제 당국이 자신감을 높이고 개발 리스크의 프리미어가 축소되고 있음을 나타냅니다. 비용이 낮아지는 경향이 있기 때문에 개발자는 초희소성 질환의 대상에서 일반적인 질병으로 축발을 옮기고 있으며, 재조합 DNA 기술 시장의 대응 가능한 풀이 확대되고 있습니다.

재조합 단백질 의약품에 대한 바이오파머 수요

노보 노르디스크는 당뇨병과 비만 치료에 대한 근본적인 수요를 뒷받침하기 위해 주사용 재조합 단백질에 특화된 노스캐롤라이나주 신거점에 41억 달러를 기록했습니다. 엘라이 릴리의 위스콘신에 대한 30억 달러의 투자와 암젠의 2025년 1분기 바이오시밀러 매출 35% 증가한 7억 달러는 수요가 아니라 공급이 현재 병목임을 시사합니다. 연속 흐름 바이오리액터와 모듈식 일회용라인은 최소 효율 규모를 낮추고 중소 바이오테크놀러지 기업이 주요 제약회사의 지원 없이 표적 단백질을 상업화할 수 있게 하고, 재조합 DNA 기술 시장에의 경쟁 진입을 확대하고 있습니다.

진화하는 세계의 유전자 편집 규제

세분화된 감독을 통해 개발자는 여러 신청서 양식, 병행 임상 프로토콜, 다양한 시판 후 조사 의무에 대응해야 합니다. FDA의 CoGenT Global 파일럿 버전은 무결성을 요구하지만 유럽의 위험 평가 모델은 미국의 이익 위험 가중치와는 여전히 다릅니다. 중국은 유전자 치료 규칙을 개정하고 있으며, 국내 기업으로의 길을 앞당기는 한편 외국의 라이선스 홀더에는 불확실성을 가져오고 있습니다. 미국에서는 15년간의 추적조사가 의무화되어 소규모 개발자의 자금력을 늘리고, 자금력 있는 기존 기업의 힘을 강화하고 있습니다. 전반적으로, 규제의 괴리는 제품의 상시를 지연시키고, 컴플라이언스 비용을 상승시키고, 재조합 DNA 기술 시장의 단기적인 성장을 억제하고 있습니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 신흥 시장에 있어서의 유전자 재조합 작물 작부 면적의 확대

- AI 주도의 데노보 단백질 설계 플랫폼

- 제조의 복잡성과 CAPEX

부문 분석

의료용 의약품은 수십년에 걸친 공정 최적화와 확립된 상환 채널의 혜택을 받는 성숙한 치료용 단백질에 지지되어 2024년 매출 전체의 65.35%를 차지했습니다. 치료제는 GLP-1이나 암 영역의 파이프라인이 확대되어 바이오시밀러 의약품의 진입이 레거시 독점을 깎는 가운데도 기세를 유지하고 있습니다. COVID-19에서 mRNA 플랫폼이 검증된 후, 백신은 새로운 생명을 얻었습니다. 암 영역의 백신 시험은 현재 같은 지질 나노입자 섀시를 활용하여 전임상 예산을 삭감하고 있습니다. 헬스케어 이외에서는 가뭄 내성을 높이는 GM작물이나 석유화학 중간체의 대체가 되는 특수화학제품을 배경으로 비의약품이 CAGR 12.25%를 나타낼 전망입니다. 산업용 효소는 현재 저온에서 섬유 제품을 세척하고 에너지를 절약하며 효소 라이센서에 정기적인 충성도를 제공합니다.

스페셜리티 케미컬은 재조합 경로를 이용하여 발효조에서 계면활성제와 향료 전구체를 생산합니다. 환경 복구 생물은 유막과 플라스틱 파편을 소화하고 합성 생물학의 신흥 기업을 위한 완전히 새로운 서비스 분야를 시작합니다. 이러한 시장의 다양화는 재조합 DNA 기술 시장의 폭을 넓혀 블록버스터 의약품의 라이프사이클에 대한 의존도를 줄이고 경제주기 전반에 걸쳐 안정적인 현금 흐름을 지원합니다.

발현 시스템은 인간 치료제, 동물 백신 및 산업용 효소에 필수적임을 반영하여 2024년 재조합 DNA 기술 시장 점유율의 64.53%를 차지했습니다. 포유류 세포 숙주는 복잡한 항체 만들기에 필수적인 인간과 유사한 글리코실화를 하기 때문에 가격이 비쌉니다. 박테리아 균주와 효모 균주는 인슐린과 효소 생산의 주력 균주이며, 신속한 배가 시간과 낮은 배지 비용으로 지원됩니다. 클로닝 벡터는 CAGR 9.85%를 나타내며, 고품질의 플라스미드와 바이러스 백본을 필요로 하는 유전자 치료 시험의 급증에 추진되고 있습니다.

단일 사용 플라스미드 마이크로팩토리는 현재 표준 실험실 실적 내에 들어가게 되며, 병원은 동정적인 이용 사례를 위해 개별화된 벡터를 만들 수 있습니다. 아데노 관련 벡터와 렌티바이러스 벡터는 배치당 20만 달러의 가격으로 거래되며 전문 CDMO에 유리한 마이크로부문을 생성합니다. 분산 제조의 보급은 특히 소량의 희귀질환 파이프라인에서 두드러지며, 국소 제조는 콜드체인의 지연을 피하고 세관의 병목 현상을 완화시킵니다.

지역별 분석

북미는 2024년 매출의 37.82%를 차지했으며 왕성한 벤처 자금, 유리한 상환, 획기적 치료제의 심사 사이클을 단축하는 FDA의 틀에 지지되고 있습니다. 미국의 바이오 의약품 제조업체는 세제 우대 조치와 숙련된 졸업생을 산업계로 보내는 대학과 연구소 네트워크의 혜택을 받고 있습니다. 캐나다의 유전자 치료 인큐베이터에 대한 투자는 특히 바이러스 벡터의 연구와 개발에서 지역의 다양성을 증가시키고 있습니다. 재조합 DNA 기술 시장에서는 현재, 노스캐롤라이나주, 매사추세츠주, 캘리포니아주가 시설 증설에 매칭 그랜트를 제공하는 등 시장 경쟁은 주 차원에서 격화되고 있습니다.

아시아태평양의 2030년까지의 CAGR은 11.81%를 나타내, 강하 시장과 탄력성 있는 공급 체인을 확보하는 동남아시아와의 제휴를 향한 중국의 전략적 변화에 지지되고 있습니다. 일본 정부는 지속가능한 화학물질을 위한 합성 생물학을 목표로 하는 생명공학 자극 프로그램을 부활시키고, 한국의 재벌 그룹은 생물제제의 수출수입을 획득하기 위해 CDMO에 공동투자하고 있습니다. 인도에서는 바이오테크놀러지 규제청의 개혁에 의해 유전자 편집 작물의 신속한 인가가 약속되어 종자 생산의 허브로서의 지위가 강화되고 있습니다. 이러한 움직임과 함께, 구미 시장과의 역사적인 생산 격차가 축소되어, 유전자 재조합 입력의 현지에서의 이용 가능성이 높아지고 있습니다.

유럽은 특히 유전자 변형 식품의 경우 기술 혁신과 소비자 회의심 사이에 균형을 맞추고 있습니다. 곧 발표될 EU 의약품 전략은 첨단 치료법의 집중적 승인의 합리화를 목표로 하고 있지만, 작물의 승인은 여전히 회원국의 옵트아웃에 직면하고 있습니다. 아일랜드, 독일, 스위스의 계약 제조업자는 이러한 분열을 이용하여 세계 고객에게 규모가 큰 바이오리액터를 제공함으로써 치료법 스폰서가 수출 전용 생산을 우선하여 현지 규제 문제를 피할 수 있도록 합니다. 중동 및 아프리카는 아직 막 시작되었지만 정책적인 기세가 있습니다. 남미의 콩과 옥수수 지역은 유전자 변형 형질전환을 위한 비옥한 토양을 제공하지만, 거시경제의 불안정성은 해외로부터의 직접 투자에 물을 줄 수도 있습니다. 이러한 다양한 궤적은 재조합 DNA 기술 시장이 지리적으로 여러 개가 되고, 집중 위험을 줄이고, 국경을 넘은 협력을 가능하게 하는 것을 보증하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- CRISPR-Cas의 비용 곡선은 계속 하락

- 재조합 단백질 의약품에 대한 바이오파마 수요

- 엠즈에 있어서의 유전자 재조합 작물의 제작 면적 확대

- AI에 의한 탈노보 단백질 설계 플랫폼

- 분산형 일회용 플라스미드 DNA 마이크로 팩토리

- 시장 성장 억제요인

- 진화하는 세계의 유전자 편집 규제

- 제조의 복잡성과 CAPEX

- 의약품 등급 벡터 원료 부족

- 유전자 편집 식품에 대한 소비자의 반발

- Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측(금액, 달러)

- 제품별

- 의료

- 치료제

- 인간 단백질

- 백신

- 비의료

- 바이오기술 작물

- 특수 화학물질

- 기타 비의료 제품

- 의료

- 구성 요소별

- 발현 시스템

- 클로닝 벡터

- 용도별

- 식품 및 농업

- 건강 및 질병

- 환경

- 기타 용도

- 최종 사용자별

- 생명공학 및 제약회사

- 학술 및 정부 기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Amgen Inc.

- Eli Lilly & Co.

- F. Hoffmann-La Roche Ltd.(Genentech)

- GenScript

- Horizon Discovery

- Merck KGaA

- New England Biolabs

- Novartis AG

- Novo Nordisk A/S

- Pfizer Inc.

- Sanofi

- Syngene International

- Thermo Fisher Scientific

- Biogen

- Bayer CropScience(Monsanto)

- Illumina

- Lonza Group

- Agilent Technologies

- Aldevron

- Johnson & Johnson

- GSK plc

제7장 시장 기회와 전망

KTH 25.10.28The recombinant DNA technology market reached USD 734.44 billion in 2025 and is projected to climb to USD 974.07 billion by 2030, reflecting a 5.81% CAGR.

Demand for recombinant protein therapeutics, accelerating CRISPR cost declines, and the mainstreaming of AI-enabled protein design continue to re-shape industry economics, lowering entry barriers for smaller innovators while rewarding established firms that modernize production footprints. Falling prices for single-use bioreactors and plasmid micro-factories now let developers pivot between therapeutic and agricultural projects without costly line changeovers, encouraging portfolio expansion into food, feed, and environmental services. North America still anchors financing and early-stage trials, but Asia-Pacific is installing capacity at a faster pace, narrowing historical skill gaps and fostering local supply chains that reduce geopolitical risk for global licensees. Competitive intensity is mounting as pharmaceutical leaders, agricultural majors, and purpose-built gene-therapy CDMOs all vie for the same vector raw materials and regulatory bandwidth.

Global Recombinant DNA (rDNA) Technology Market Trends and Insights

CRISPR-Cas Cost Curve Keeps Falling

Widening access to nuclease-editing kits, cheaper guide-RNA synthesis, and rising vector yields have pushed the fully loaded cost of CRISPR therapies down sharply. CASGEVY's clinical success in sickle cell disease validated the modality, even at an initial price tag near USD 3 million per patient. Aldevron then cut personalized CRISPR manufacturing time to six months, proving cycle-time gains are realistic as supply chains mature. A record 14 US review designations in 2024 signaled that regulators are gaining confidence, shrinking development risk premia. As costs trend lower, developers are pivoting from ultra-rare disease targets toward prevalent disorders, enlarging the recom¬binant DNA technology market addressable pool.

Biopharma Demand for Recombinant Protein Drugs

Novo Nordisk earmarked USD 4.1 billion for a new North Carolina site focused on injectable recombinant proteins, underscoring persistent demand in diabetes and obesity care. Eli Lilly's USD 3 billion Wisconsin investment and Amgen's 35% Q1 2025 biosimilar revenue jump to USD 700 million suggest supply, not demand, is the current bottleneck. Continuous-flow bioreactors and modular single-use lines are lowering minimum efficient scale, letting smaller biotechs commercialize targeted proteins without big-pharma backing, thereby broadening competitive participation in the recombinant DNA technology market.

Evolving Global Gene-Editing Regulations

Fragmented oversight forces developers to navigate multiple dossier formats, parallel clinical protocols, and divergent post-marketing surveillance mandates. The FDA's CoGenT Global pilot seeks alignment, yet Europe's risk-assessment model still differs from US benefit-risk weighting. China is revising its gene-therapy rules, creating uncertainty for foreign license holders even as it speeds pathways for domestic firms. Fifteen-year follow-up requirements in the US stretch the financial stamina of small developers, consolidating power among cash-rich incumbents. Collectively, regulatory divergence slows product launches and raises compliance costs, tempering near-term growth for the recombinant DNA technology market.

Other drivers and restraints analyzed in the detailed report include:

- GM-Crop Acreage Expansion in Emerging Markets

- AI-Driven De-Novo Protein Design Platforms

- Manufacturing Complexity & CAPEX

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Medical products contributed 65.35% of overall revenue in 2024, anchored by mature therapeutic proteins that benefit from decades of process optimization and well-established reimbursement channels. The therapeutic agents subset keeps momentum through expanding GLP-1 and oncology pipelines, even as biosimilar entrants chip away at legacy monopolies. Vaccines gained new life after COVID-19 validated mRNA platforms; oncology vaccine trials now leverage the same lipid-nanoparticle chassis, cutting preclinical budgets. Outside healthcare, non-medical products are rising at a 12.25% CAGR on the back of GM crops that boost drought tolerance and specialty chemicals that replace petrochemical intermediates. Industrial enzymes now clean textiles at lower temperatures, saving energy and creating recurring royalties for enzyme licensors, an illustration of revenue resilience that cushions cyclicality in drug sales.

Specialty chemicals harness recombinant pathways to produce surfactants and fragrance precursors in fermenters, yielding lower emissions relative to petro-routes and aligning with corporate net-zero pledges. Environmental remediation organisms digest oil slicks and plastic debris, launching entirely new service niches for synthetic-biology startups. This diversification broadens the recombinant DNA technology market, reduces dependence on blockbuster drug lifecycles, and supports steady cash flows across economic cycles.

Expression systems accounted for a 64.53% slice of recombinant DNA technology market share in 2024, reflecting their indispensability across human therapeutics, animal vaccines, and industrial enzymes. Mammalian cell hosts command premium pricing because they perform human-like glycosylation, a must for complex antibodies. Bacterial and yeast lines remain the workhorses for insulin and enzyme production, favored for rapid doubling times and lower media costs. Cloning vectors, growing at 9.85% CAGR, are propelled by surging gene-therapy trials that require high-grade plasmids and viral backbones.

Single-use plasmid micro-factories now fit within standard laboratory footprints, letting hospitals craft personalized vectors for compassionate-use cases. Adeno-associated and lentiviral vectors fetch prices up to USD 200,000 per batch, creating lucrative micro-segments for specialized CDMOs. The spread of distributed manufacturing is especially pronounced in low-volume rare-disease pipelines, where localized production avoids cold-chain delays and alleviates customs bottlenecks.

The Recombinant DNA Technology Market Report is Segmented by Product (Medical [Therapeutic Agents, and More] and Non-Medical), Component (Expression System and Cloning Vector), Application (Food and Agriculture, Health and Disease, and More), End User (Biotech & Pharma Companies, Academic & Govt Institutes, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 37.82% of revenue in 2024, supported by robust venture funding, favorable reimbursement, and FDA frameworks that shorten review cycles for breakthrough therapies. US biomanufacturers benefit from tax incentives and university-laboratory networks that funnel skilled graduates into industry. Canada's investments in gene-therapy incubators add regional diversity, particularly in viral-vector R&D. The recombinant DNA technology market now sees strong state-level competition for capacity, with North Carolina, Massachusetts, and California offering matching grants for facility build-outs.

Asia-Pacific logged the fastest CAGR at 11.81% to 2030, underpinned by China's strategic shift toward Southeast Asian partnerships that secure downstream markets and resilient supply chains. Japan's government has revived biotech stimulus programs, targeting synthetic biology for sustainable chemicals, while South Korea's Chaebol groups co-invest in CDMOs to capture biologics export revenue. India's reform of its Biotechnology Regulatory Authority promises faster clearance for gene-edited crops, strengthening its position as a seed-production hub. Together, these moves are narrowing the historical production gap with Western markets and boosting local availability of recombinant inputs.

Europe balances innovation with consumer skepticism, particularly for GMO foods. The forthcoming EU Pharmaceutical Strategy aims to streamline centralized approvals for advanced therapies, yet crop approvals still face member-state opt-outs. Contract manufacturers in Ireland, Germany, and Switzerland capitalize on this split by offering scale bioreactors for global clients, letting therapy sponsors sidestep local regulatory snags in favor of export-only production. The Middle East and Africa are at a nascent stage but show policy momentum: Saudi Arabia has budgeted sovereign-fund capital for genomics centers, and Ghana's GM cowpea clearance signals a pragmatic stance on food security. South America's soy and corn belts provide fertile ground for GM traits, though macroeconomic volatility can dampen foreign direct investment. These diverse trajectories ensure the recombinant DNA technology market remains geographically plural, reducing concentration risk and enabling cross-border collaboration.

- Amgen

- Eli Lilly and Company

- F. Hoffmann-La Roche Ltd. (Genentech)

- Genscript

- Horizon Discovery

- Merck

- New England Biolabs

- Novartis

- Novo Nordisk

- Pfizer

- Sanofi

- Syngene International

- Thermo Fisher Scientific

- Biogen

- Bayer CropScience (Monsanto)

- Illumina

- Lonza Group

- Agilent Technologies

- Aldevron

- Johnson & Johnson

- GlaxoSmithKline

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 CRISPR-Cas Cost Curve Keeps Falling

- 4.2.2 Biopharma Demand For Recombinant Protein Drugs

- 4.2.3 GM-Crop Acreage Expansion In Ems

- 4.2.4 AI-Driven De-Novo Protein Design Platforms

- 4.2.5 Distributed, Single-Use Plasmid DNA Micro-Factories

- 4.3 Market Restraints

- 4.3.1 Evolving Global Gene-Editing Regulations

- 4.3.2 Manufacturing Complexity & CAPEX

- 4.3.3 Pharmaceutical-Grade Vector Raw-Material Shortages

- 4.3.4 Consumer Push-Back On Gene-Edited Foods

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Medical

- 5.1.1.1 Therapeutic Agents

- 5.1.1.2 Human Proteins

- 5.1.1.3 Vaccines

- 5.1.2 Non-medical

- 5.1.2.1 Biotech Crops

- 5.1.2.2 Specialty Chemicals

- 5.1.2.3 Other Non-medical Products

- 5.1.1 Medical

- 5.2 By Component

- 5.2.1 Expression Systems

- 5.2.2 Cloning Vectors

- 5.3 By Application

- 5.3.1 Food & Agriculture

- 5.3.2 Health & Disease

- 5.3.3 Environment

- 5.3.4 Other Applications

- 5.4 By End User

- 5.4.1 Biotech & Pharma Companies

- 5.4.2 Academic & Govt Institutes

- 5.4.3 Other End Users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Amgen Inc.

- 6.3.2 Eli Lilly & Co.

- 6.3.3 F. Hoffmann-La Roche Ltd. (Genentech)

- 6.3.4 GenScript

- 6.3.5 Horizon Discovery

- 6.3.6 Merck KGaA

- 6.3.7 New England Biolabs

- 6.3.8 Novartis AG

- 6.3.9 Novo Nordisk A/S

- 6.3.10 Pfizer Inc.

- 6.3.11 Sanofi

- 6.3.12 Syngene International

- 6.3.13 Thermo Fisher Scientific

- 6.3.14 Biogen

- 6.3.15 Bayer CropScience (Monsanto)

- 6.3.16 Illumina

- 6.3.17 Lonza Group

- 6.3.18 Agilent Technologies

- 6.3.19 Aldevron

- 6.3.20 Johnson & Johnson

- 6.3.21 GSK plc

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment