|

시장보고서

상품코드

1842432

섭취형 센서 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Ingestible Sensors - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

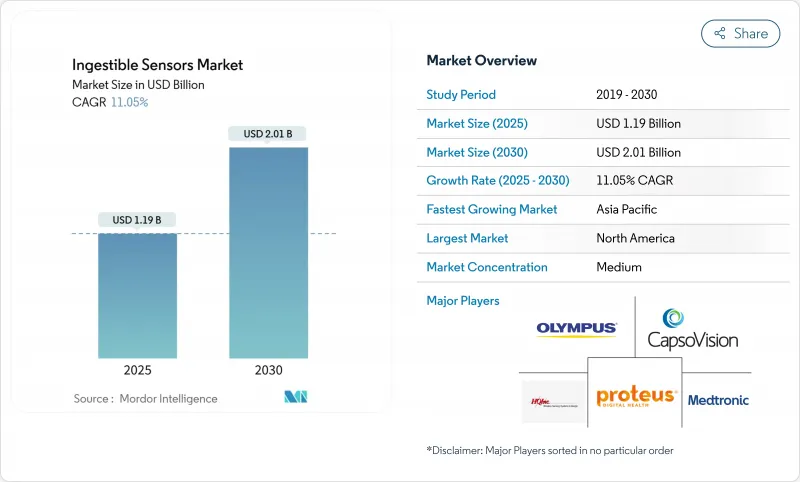

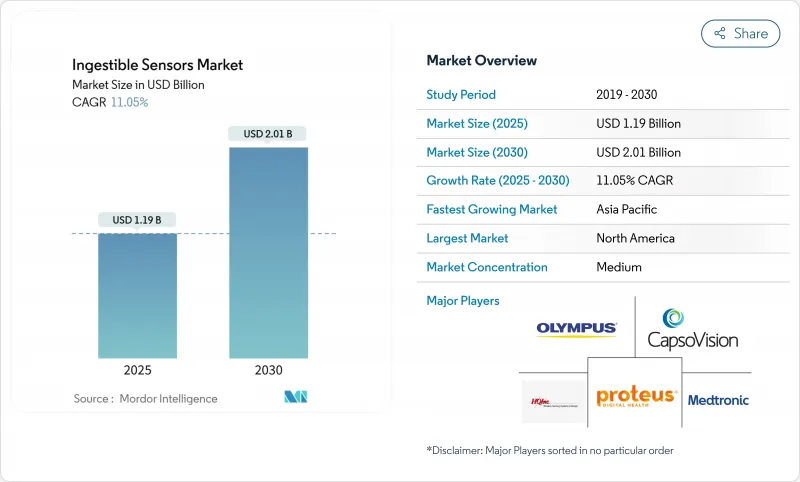

섭취형 센서 시장 규모는 2025년 11억 9,000만 달러에 이르며, CAGR 11.05%를 나타내 2030년에는 20억 1,000만 달러로 상승할 것으로 예측됩니다.

강한 기세는 소형화 전자의 진보, 센싱 모달리티의 확대, 헬스케어 부문이 예방적인 데이터 주도형 케어에 축발을 옮기고 있는 것에 기인하고 있습니다. 인공지능과 캡슐이 생성하는 데이터의 통합으로, 한때 침습적인 진단이 필요했던 소화기 질환의 실시간 모니터링 옵션이 확산되고 있습니다. 디지털 정제의 규제 클리어런스는 시장 진입 장벽을 줄이고, 가치 기반 상환의 보급은 북미와 유럽에서 수요를 견인하고 있습니다. 바이오센싱 신흥기업에 대한 벤처자금 제공은 2024년 기록적인 수준에 이르렀으며, 전력효율과 멀티파라미터 센싱을 목표로 하는 신규 진입기업을 뒷받침하고 있습니다. 그럼에도 불구하고 배터리용량 제한과 사이버 보안 강화가 제품 투입 속도를 늦추고 있습니다.

세계의 섭취형 센서 시장 동향과 인사이트

OECD 국가에서 디지털 정제의 상환 확대

OECD 회원국의 주요 의료 시스템에서 보험 상환을 확대하면 섭취 가능한 모니터링 솔루션의 예측 가능한 수익원이 강화되고 있습니다. 지불자는 만성 질환 환자가 치료를 계속함으로써 얻은 장기적인 비용 절감과 보험 적용을 연결하고 처방전에 디지털 정제를 표준 옵션으로 통합하도록 촉구합니다 (ema.europa.eu). 유럽의 임상시험에서는 어드히어런스 센서가 유효한 바이오마커로 인증되었으며 더욱 보급이 가속화되고 있습니다. 병원은 현재 캡슐 기반 복약 준수 지표를 성과 기반 계약에 통합하고 있으며 초기 기술 채용자에게 머무르지 않는 수요를 지원합니다. 그 결과 섭취형 센서 시장은 2자리 성장을 유지할 전망입니다.

북미에서 제약 회사 주도의 복약 준수 플랫폼 추진

제약 회사는 실제 세계의 증거를 수집하고, 가격 설정을 보호하고, 특허 기간을 연장하기 위해 기존의 의약품에 섭취 가능한 태그를 포함합니다. 에빌리파이 마이사이트에 의해 열린 FDA의 길은 의약품과 디바이스의 조합을 정당화하고 타사가 비슷한 프로그램에 많은 투자를할 것을 촉구했습니다. 디지털 섭취 데이터는 차별화된 라벨링을 지원하고, 상당한 상환을 요구하며, 연간 1,000억-3,000억 달러의 비어드히어런스의 부담을 상쇄합니다. 이러한 산업의 움직임은 초기 단계의 센서 공급업체를 지원하는 상업적 최종 시장을 견고하게 하고 주기적인 자금 조달의 변동에도 불구하고 섭취형 센서 시장을 유지합니다.

FDA 사이버 장비 지침이 데이터 보안 장애물 조성

2024년에 더 엄격해진 사이버 보안 규칙에 따라 섭취형 센서는 생태계 전체에 걸쳐 다층 암호화와 실시간 위협 모니터링을 통합해야 합니다(irp.nih.gov). 이러한 표준을 충족하기 위해서는 전력 소비가 급박하고 검증주기가 장기화됩니다. 소규모 혁신자는 설계 동결 기간의 장기화와 인증 비용 상승에 직면하고 경쟁 우위는 기존 기업에 기울입니다. 이러한 대책은 환자 데이터의 무결성을 향상시키지만, 시장 진입을 일시적으로 감속시킬 수 있어 단기적인 섭취형 센서 시장의 성장 예측에 물을 끼치게 됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 소형화 ASIC의 진보에 의한 캡슐의 전력 수요의 저하

- EU에서의 체내 원격 측정 모듈의 CE 마크 급증

- 캡슐 배터리 수명 제한으로 인한 다중 파라미터 감지 제약

부문 분석

온도 센서는 2024년 섭취형 센서 시장의 42%를 차지했으며, 유효한 정밀도와 저전력 수요로 그 지위를 획득했습니다(sciencedirect.com). 스포츠 의학, 군사 준비, 주술기 의료는 열 스트레스를 피하고 체온 동향을 모니터링하기 위해 이러한 캡슐에 의존합니다. 체온 장치의 섭취형 센서 시장 규모는 훈련 블록에서 지속적인 체온 모니터링을 의무화하는 스포츠 리그의 프로토콜을 배경으로 꾸준히 확대될 것으로 예측됩니다. 이미지 캡슐은 기초가 작음에도 불구하고 소형화된 광학계와 캡슐 내시경 검사에 대한 상환 확대로 혜택을 받으며 2030년까지 연평균 복합 성장률(CAGR) 13.8%를 나타내 급성장합니다.

화상 대응 기기는 출혈, 폴립, 클론 병변을 비침습적으로 검출하기 때문에 진정제나 내시경 합병증의 회피를 요구하는 소화기내과의를 끌어들인다. 메드트로닉의 PillCam Genius SB는 수만 장의 점막 사진을 촬영하면서 인공지능을 이용한 이미지 분류로 의사의 독서 시간을 단축할 수 있음을 입증합니다 (news.medtronic.com). PressureCap과 같은 최근 프로토타입은 캡슐의 직경을 부풀리지 않고 여러 변형 게이지를 통합합니다 (cell.com). 3유형의 센서를 모두 내장한 크로스 모달리티 디자인은 배터리의 기술 혁신에 의해 전력 제약이 완화되면, 프리미엄 가격으로의 판매가 가능하게 될지도 모릅니다.

2024년의 섭취형 센서 시장 수익의 86%는 의료시설이 차지했고, 복약 준수 감사, 출혈 국재화, 염증성 장 질환 평가에 캡슐이 사용되었습니다. 임상 가이드라인이 내시경 검사량을 보다 침습적인 캡슐 경로로 이동시키기 때문에 병원 배치와 관련된 섭취형 센서 시장 규모는 계속 확대될 것으로 예측됩니다. FDA가 항정신병제과 항바이러스제으로 허가한 복약 준수 모듈은 99%에 가까운 복약 컴플라이언스율을 나타내며, 밸류베이스 계약에 있어서의 지불자의 채용을 뒷받침하고 있습니다.

엘리트 스포츠 팀과 군사 조직은 그 수가 적은 CAGR 14.2%를 나타내 가장 급성장하는 고객 기반을 형성하고 있습니다. 올림픽과 같은 행사에서 지구계 선수가 착용하는 보온 캡슐은 참가자를 노작성 열사병으로부터 보호하고 수분 보급 요법을 최적화합니다. 웨어러블 심박 스트랩 및 클라우드 분석과 통합하여 종합적인 교육 대시보드를 만들고 고성능 코칭 직원을 매료시킵니다. 시간이 지남에 따라 소비자 피트니스 프로그램이 간이 버전을 채택하게 되어 섭취형 센서 시장은 프로 집단 이외에도 확대될 가능성이 있습니다.

지역 분석

북미는 2024년 섭취형 센서 시장 수익의 40%를 차지하며 디지털 정제에 대한 지불자의 상환, 강력한 벤처 자금, 지지적인 FDA 데노보 패스웨이 (accessdata.fda.gov)에 지지되었습니다. 병원 시스템은 고액의 재입원을 억제하기 위해 어드히어런스 캡슐을 도입하고, 제약 회사는 처방전 배치를 협상하기 위해 실제 세계 섭취 데이터를 활용합니다. 현지 학술센터는 차세대 센싱 모달리티를 검증하는 조기실현가능성 시험을 실시했습니다.

아시아태평양은 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 14.5%를 나타낼 것으로 예측되며, 이는 세계에서 가장 빠릅니다. 일본은 고령화가 진행되고 중국은 소화기 질환의 부담이 크기 때문에 대응 가능한 기반이 형성됩니다. 국내 제조업체는 지역 구매력에 맞추어 비용을 최적화한 캡슐을 도입하고, 국가의 디지털 건강 전략은 원격 모니터링 채택을 촉진합니다. 한국과 같은 시장에서는 정부 보험이 캡슐 내시경의 상환을 검토하기 시작하고 있으며 수요를 더욱 자극하고 있습니다.

유럽은 혁신적인 원격 측정 캡슐의 조기 입수를 가능하게 하는 CE 마크 제도를 활용하여 섭취형 센서 시장에서 주목할만한 점유율을 유지하고 있습니다. 공공 부문의 프로그램은 예방 의료를 중시하고 비 침습적 진단과 일치합니다. 독일과 북유럽에서는 벤처기업에 대한 자금 지원이 증가하여 자기발전형 센서와 생분해성 하우징을 추구하는 신흥기업을 지원하고 있습니다. 걸프 협력 회의와 브라질 민간 병원은 특히 프리미엄 케어 패키지의 캡슐 내시경 검사를 신속하게 채용하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- OECD 전체에서 디지털 알약의 상환 확대

- 북미의 제약 기업 주도의 복약 준수 플랫폼의 추진

- ASIC의 소형화가 진행되어, 캡슐의 전력 수요가 저하

- EU에서의 체내 원격 측정 모듈의 CE 마크 취득 급증

- APAC의 대규모 소화기 질환 환자 수가 수요를 견인

- 바이오센싱 신흥기업에 대한 벤처 투자(2023-2024년에 과거 최고를 기록)

- 시장 성장 억제요인

- FDA의 사이버 디바이스 가이던스에 의한 데이터 보안의 장애

- 캡슐의 전지 수명의 제한에 의한 멀티 파라미터·센싱의 제약

- 지불자에게 있어서의 아웃컴 베네핏에 관한 임상 근거는 거리

- 신흥국에 있어서의 1회 한정의 높은 처치 비용

- 가치/공급망 분석

- 규제 전망

- 기술적 전망

- 특허 정세 분석

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측(금액)

- 구성 요소별

- 센서

- 웨어러블 패치/데이터 레코더

- 소프트웨어 및 분석 플랫폼

- 센서 유형별

- 온도 센서

- 압력 센서

- pH 센서

- 이미지 센서

- 기능별

- 이미징

- 모니터링 및 준수

- 약물 전달 트리거

- 업계별

- 의료 및 헬스케어

- 스포츠 및 피트니스

- 업계별

- 최종 사용자별

- 병원 및 ASC

- 재택 헬스케어

- 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 기타 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Medtronic PLC(Given Imaging)

- Proteus Digital Health, Inc.

- CapsoVision, Inc.

- IntroMedic Co., Ltd.

- Jinshan Science and Technology

- Olympus Corporation

- HQ, Inc.

- MC10, Inc.

- etectRx, Inc.

- Otsuka Holdings Co., Ltd.

- Atmo Biosciences

- STMicroelectronics

- Philips Healthcare

- Check-Cap Ltd.

- PENTAX Medical

- RF Wireless Systems

- Karl Storz SE and Co. KG

- Boston Scientific Corporation

- CapsuleTech(a Lantronix company)

- Dassiet BioTelemetry

제7장 시장 기회와 전망

KTH 25.10.28The ingestible sensors market size reached USD 1.19 billion in 2025 and is forecast to climb to USD 2.01 billion by 2030, reflecting an 11.05% CAGR.

Strong momentum stems from advances in miniaturized electronics, expanded sensing modalities, and the healthcare sector's pivot toward preventive, data-driven care. Integration of artificial intelligence with capsule-generated data is broadening real-time monitoring options for gastrointestinal disorders that once required invasive diagnostics. Regulatory clearances for digital pills are reducing market-entry barriers, while the spread of value-based reimbursement is pulling demand forward in North America and Europe. Venture funding for biosensing start-ups hit record levels in 2024, encouraging new entrants that target power efficiency and multi-parameter sensing. Nonetheless, battery capacity limits and heightened cybersecurity mandates are moderating the pace of product launches.

Global Ingestible Sensors Market Trends and Insights

Reimbursement Expansion for Digital Pills across OECD

Broader reimbursement in major OECD health systems is reinforcing predictable revenue streams for ingestible monitoring solutions. Payers link coverage to the long-term cost savings that accrue when chronic-disease patients adhere to therapy, prompting formularies to incorporate digital pills as standard options [ema.europa.eu]. Qualification of adherence sensors as valid biomarkers in European clinical trials further accelerates uptake. Hospitals now embed capsule-based adherence metrics in outcome-based contracts, anchoring demand that goes beyond early technology adopters. The resulting pull-through is expected to keep the ingestible sensors market on its double-digit growth path.

Pharma-led Push for Dose Adherence Platforms in North America

Pharmaceutical firms are embedding ingestible tags into legacy drugs to collect real-world evidence, defend pricing, and extend patent life. The FDA pathway opened by Abilify MyCite legitimized drug-device combinations, prompting others to invest heavily in similar programs. Digital ingestion data support differentiated labelling, which commands premium reimbursements and offsets the USD 100-300 billion annual burden of non-adherence. These industry moves solidify a commercial end-market that anchors early-stage sensor suppliers, sustaining the ingestible sensors market despite cyclical funding swings.

FDA Cyber-device Guidance Creating Data-Security Hurdles

Stricter 2024 cybersecurity rules obligate ingestible sensors to embed multi-layer encryption and real-time threat monitoring across their entire ecosystem [irp.nih.gov]. Meeting these standards strains power budgets and prolongs verification cycles. Smaller innovators face longer design-freeze periods and higher certification costs, tilting competitive advantage toward established firms. While the measures improve patient data integrity, they can momentarily decelerate market arrivals, dampening near-term ingestible sensors market growth projections.

Other drivers and restraints analyzed in the detailed report include:

- Miniaturized ASIC Advances Lowering Capsule Power Demand

- CE-mark Surge for In-body Telemetry Modules in EU

- Limited Capsule Battery Life Restricts Multi-Parameter Sensing.

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Temperature sensors contributed 42% of the ingestible sensors market in 2024, a position earned through validated accuracy and low power demand [sciencedirect.com]. Sports medicine, military readiness, and perioperative care rely on these capsules to avert heat stress and monitor core temperature trends. The ingestible sensors market size for temperature devices is projected to expand steadily on the back of sports league protocols that mandate continuous thermal monitoring during training blocks. Imaging capsules, despite a smaller base, are set to grow fastest at 13.8% CAGR through 2030, benefitting from miniaturized optics and expanding reimbursement for capsule endoscopy.

Image-enabled devices elevate non-invasive detection of bleeding, polyps, and Crohn's lesions, thus attracting gastroenterologists who seek to avoid sedation and endoscopic complications. Medtronic's PillCam Genius SB demonstrates how AI-assisted image sorting can reduce physician reading time while capturing tens of thousands of mucosal pictures [news.medtronic.com]. Pressure and pH modules address motility disorders and acid reflux; recent prototypes such as PressureCap integrate multiple strain gauges without inflating capsule diameter [cell.com]. Cross-modality designs that embed all three sensor types may unlock premium pricing once battery innovations alleviate power constraints.

Healthcare facilities accounted for 86% of the ingestible sensors market revenue in 2024, using capsules for medication adherence audits, bleeding localization, and inflammatory bowel disease assessment. The ingestible sensors market size tied to hospital deployment is forecast to keep growing as clinical guidelines shift endoscopy volumes toward less invasive capsule pathways. Adherence modules, cleared by the FDA for antipsychotics and antivirals, show compliance rates approaching 99%, supporting payer adoption in value-based contracts.

Elite sports teams and military organizations, though a smaller slice, form the fastest-growing customer base at a 14.2% CAGR. Thermal capsules worn by endurance athletes during events like the Olympics safeguard participants from exertional heat stroke and optimize hydration regimens. Integration with wearable heart-rate straps and cloud analytics produces a holistic training dashboard, enticing high-performance coaching staffs. Over time, consumer fitness programs may adopt simplified versions, extending the ingestible sensors market beyond professional cohorts.

Ingestible Sensors Market Segmented by Component (Sensors, Wearable Patch / Data Recorder and More), Sensor Type (Temperature Sensor, Pressure Sensor and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 40% of ingestible sensors market revenue in 2024, underpinned by payer reimbursement for digital pills, strong venture funding, and a supportive FDA De Novo pathway [accessdata.fda.gov]. Hospital systems deploy adherence capsules to curb costly readmissions, while pharmaceutical companies leverage real-world ingestion data to negotiate formulary placements. Regional academic centers also run early-feasibility trials that validate next-generation sensing modalities.

Asia-Pacific is forecast to chart a 14.5% CAGR from 2025 to 2030, the fastest worldwide. Japan's aging population and China's large burden of gastrointestinal disorders create a sizable addressable base. Domestic manufacturers introduce cost-optimized capsules that align with regional purchasing power, while national digital-health strategies encourage remote monitoring adoption. Government insurance in markets such as South Korea has begun considering capsule endoscopy reimbursement, further stimulating demand.

Europe retains a notable share of the ingestible sensors market, leveraging its CE-mark system, which grants earlier access to innovative telemetry capsules. Public-sector programs emphasize preventive care, aligning with non-invasive diagnostics. Increased venture funding in Germany and the Nordics supports start-ups pursuing self-powered sensors and biodegradable housings. Meanwhile, Middle East and Africa and South America together represent a small but rising opportunity; private hospitals in the Gulf Cooperation Council and Brazil are early adopters, especially for capsule endoscopy in premium care packages.

- Medtronic PLC (Given Imaging)

- Proteus Digital Health, Inc.

- CapsoVision, Inc.

- IntroMedic Co., Ltd.

- Jinshan Science and Technology

- Olympus Corporation

- HQ, Inc.

- MC10, Inc.

- etectRx, Inc.

- Otsuka Holdings Co., Ltd.

- Atmo Biosciences

- STMicroelectronics

- Philips Healthcare

- Check-Cap Ltd.

- PENTAX Medical

- RF Wireless Systems

- Karl Storz SE and Co. KG

- Boston Scientific Corporation

- CapsuleTech (a Lantronix company)

- Dassiet BioTelemetry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Reimbursement Expansion for Digital Pills across OECD

- 4.2.2 Pharma-led Push for Dose Adherence Platforms in North America

- 4.2.3 Miniaturised ASIC Advances Lowering Capsule Power Demand

- 4.2.4 CE-mark Surge for In-body Telemetry Modules in EU

- 4.2.5 Large GI Disorder Patient Pools in APAC Driving Demand

- 4.2.6 Venture Investments in Biosensing Start-ups (2023-24 record high)

- 4.3 Market Restraints

- 4.3.1 FDA Cyber-device Guidance Creating Data-Security Hurdles

- 4.3.2 Limited Capsule Battery Life Restricts Multi-parameter Sensing

- 4.3.3 Mixed Clinical Evidence on Outcome Benefits for Payors

- 4.3.4 High One-time Procedure Costs in Emerging Countries

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Patent Landscape Analysis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Sensors

- 5.1.2 Wearable Patch / Data Recorder

- 5.1.3 Software and Analytics Platform

- 5.2 By Sensor Type

- 5.2.1 Temperature Sensor

- 5.2.2 Pressure Sensor

- 5.2.3 pH Sensor

- 5.2.4 Image Sensor

- 5.3 By Function

- 5.3.1 Imaging

- 5.3.2 Monitoring / Adherence

- 5.3.3 Drug Delivery Trigger

- 5.4 By Industry Vertical

- 5.4.1 Healthcare / Medical

- 5.4.2 Sport and Fitness

- 5.4.3 Other Verticals

- 5.5 By End-user

- 5.5.1 Hospitals and ASCs

- 5.5.2 Home Healthcare

- 5.5.3 Research Institutes

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Medtronic PLC (Given Imaging)

- 6.4.2 Proteus Digital Health, Inc.

- 6.4.3 CapsoVision, Inc.

- 6.4.4 IntroMedic Co., Ltd.

- 6.4.5 Jinshan Science and Technology

- 6.4.6 Olympus Corporation

- 6.4.7 HQ, Inc.

- 6.4.8 MC10, Inc.

- 6.4.9 etectRx, Inc.

- 6.4.10 Otsuka Holdings Co., Ltd.

- 6.4.11 Atmo Biosciences

- 6.4.12 STMicroelectronics

- 6.4.13 Philips Healthcare

- 6.4.14 Check-Cap Ltd.

- 6.4.15 PENTAX Medical

- 6.4.16 RF Wireless Systems

- 6.4.17 Karl Storz SE and Co. KG

- 6.4.18 Boston Scientific Corporation

- 6.4.19 CapsuleTech (a Lantronix company)

- 6.4.20 Dassiet BioTelemetry

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment