|

시장보고서

상품코드

1842442

통풍 치료제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Gout Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

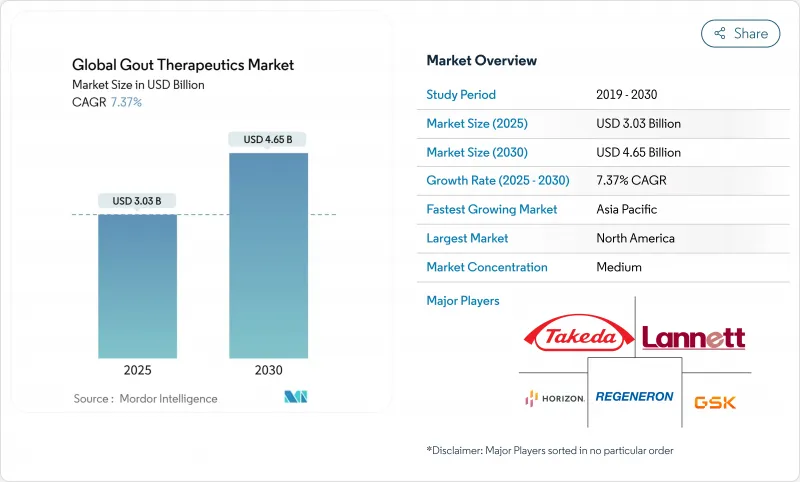

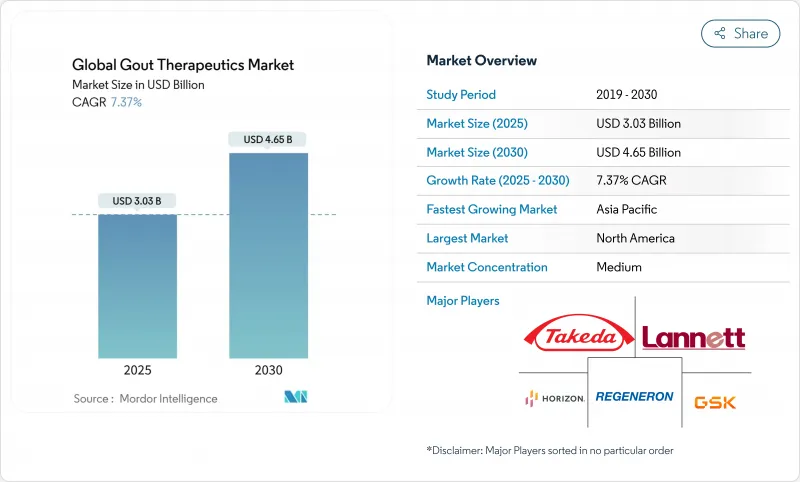

통풍 치료제 시장은 2024년에 30억 3,000만 달러를 창출했고 2030년에는 46억 5,000만 달러에 달할 것으로 예측되며, 2025-2030년의 CAGR은 7.37%를 나타낼 전망입니다.

고령화, 대사 증후군, 비만과 관련된 질병 유병률 증가가 치료 대상 환자를 계속 확대하는 반면, 약리 유전체 검사 및 실시간 혈청 측정 웨어러블과 같은 정밀 접근법은 진단률과 치료율을 끌어올리고 있습니다. 다수의 고속 트럭 지정 및 생물학적 제제의 승인 사이클 가속화 등 규제 촉매가 신규 약제 시장 투입까지의 시간을 단축하고 있으며, 각 회사는 이러한 경로를 이용하여 적응 확대 및 차세대 URAT1 억제제의 상시를 진행하고 있습니다. Febuxostat를 둘러싼 공급망의 혼란과 NSAID의 안전성에 대한 우려의 장기화로 인해 특히 심혈관 위험이 높은 코호트에서는 처방자의 선호도가 대체 메커니즘으로 바뀌고 있습니다. 이러한 배경 속에서 통풍 치료제 시장은 적극적인 혈청 요산 수치 조절이 비용이 많이 드는 합병증을 회피한다는 지불 측 인식 증가로 혜택을 받고 있으며, 병용 요법, 생물학적 제제, 동반자 진단제의 보험 적용을 뒷받침하고 있습니다.

세계의 통풍 치료제 시장 동향과 인사이트

고령화와 비만으로 통풍 유병률 상승

세계의 통풍 환자 수는 2024년에는 5,300만명을 넘어, 1990년부터의 연령 표준화율로 22.4% 급증해, 이 동향은 55세 이상의 남성에서 가장 현저하고, 유병률은 10만명당 2,500명을 넘었습니다. 고소득국가의 고령화는 도시화가 진행되는 아시아태평양경제의 비만 증가와 함께 장기간 요산강하요법의 대상자를 확대하고 있습니다. 태평양 제도 지역사회에서는 급속한 식생활 서유럽화로 유전적인 고요산혈증이 나타나지만, 이 패턴은 신흥 시장에서도 재현될 것으로 예측됩니다. 통풍 치료제 시장은 기존의 건강 관리 시스템과 신흥 건강 관리 시스템 모두에서 지속적인 수요 증가가 꾸준한 확대를 지원합니다.

요산치 저하 가이드라인의 표적 치료에의 채용

혈청 요산 값 6mg/dL 미만을 권장하는 서양 류마티스 학회의 지침에 따라 통풍 관리는 에피소드 플레어 컨트롤에서 사전 활성 질환 변형으로 재구성되었습니다. 목표치를 달성하는 것으로 심혈관 이벤트가 경감된다는 근거가 나타나기 때문에 의료 보험 회사는 혈청 요산치의 연속 검사, 병용 요법, 전문의의 진찰에 대해서 점점 보험 상환을 실시하게 되고 있습니다. 현재 미국의 통풍 환자의 28.9%만 요산 강하 요법을 받고 있지만, 디지털 어드히어런스 툴이나 약사 주도의 프로그램이 확대됨에 따라 컴플라이언스의 향상이 기대되고 있습니다. 가이드라인 준수율 향상은 환자 1인당 평균 치료 기간을 밀어 올려 통풍 치료제 시장 확대에 직결합니다.

Febuxostat 및 NSAID 장기 사용에 대한 박스형 경고 안전 문제

2023년 2월, FDA는 페부크소스타트와 심혈관계 사망률의 연관성을 나타내는 박스 경고를 발행하였으며, 페부크소스타트의 사용은 알로프리놀 불내증 환자로 제한되었습니다. 다케다 약품이 2025년 1월에 유로릭 브랜드에서 철수하기로 결정한 것은 상업적 영향을 강조하는 것입니다. 유사한 심혈관계 및 신장의 위험 프로파일은 NSAID의 장기 투여를 제한하기 때문에 처방자는 URAT1 억제제 및 생물학적 제제와 같은 비용은 높지만 안전한 메커니즘을 선택하게 됩니다.

보고서에서 분석된 기타 성장 촉진요인 및 억제요인

- 생물학적 제형 및 차세대 URAT1 승인(예 : AR882, SEL-212)

- 난치성 통풍 치료에 대한 FDA의 고속 트랙 프로그램

- 만성 투여 및 플레어 패러독스로 인한 어드히어런스 감소

부문 분석

크산틴 옥시다아제 억제제는 저렴한 제네릭 의약품인 알로프리놀과 브랜드에 충실한 페부크소스타트 사용자의 힘으로 2024년 통풍 치료제 시장 점유율의 46.34%를 획득했습니다. 이 부문은 여전히 확대되었지만 CAGR 4%를 나타내 URAT1 억제제에 뒤처졌으며 8.12%가 통풍 치료제 시장 규모를 재정의하고 있습니다. 임상 데이터는 ABCG2 다형성이 50% 이상인 환자에서 알로프리놀 반응을 둔화시키는 경우에도 URAT1 억제는 효능을 유지하는 것으로 나타났습니다. 이러한 유전학적 인사이트는 정밀의료에 대한 지불자의 관심과 일치하며, 처방 위원회는 지금까지 크산틴 옥시다아제 저해를 우선해 온 단계적 치료 규칙을 재평가하는 방향에 있습니다.

파이프라인의 역동성은 혁신자에게 유리합니다. AR882와 dotinurad는 옥시프리놀 축적이 없는 1일 1회 경구 투여가 가능하며 신장에 안전한 프로파일과 약물-약물 상호작용이 적은 저분자 URAT1 억제제군의 필두입니다. 재조합 돌연변이 생물 제제는 토포피의 부담이 큰 만성 난치성 통풍에서 틈새 위치를 차지합니다. 페글로티카제의 매출은 암젠에 의한 호라이즌 세라퓨틱스 인수 전 전년 대비 33% 증가해 이 카테고리를 통합한 reuters.com. 한편, 카나키누맙과 같은 IL-1 억제제는 2023년 12월에 성인 통풍의 적응을 획득하고 요산 강하제를 보완하는 항염증 생물학적 제형의 확대를 나타냈습니다. 이러한 진화하는 부류는 유전적, 신장 및 심혈관 프로파일에 적합한 차별화된 옵션을 제공함으로써 통풍 치료제 시장을 계속 확대하고 있습니다.

지역 분석

북미는 생물학적 제제의 조기 도입, 폭넓은 보험 적용, 전문의의 보급으로 2024년 매출의 41.72%를 차지했습니다. Treat-to-target 가이드라인은 전문 학회로부터 강한 지지를 얻고 있으며, 지불자는 혈청 정밀도의 연속 검사를 환불하는 경우가 많기 때문에 환자 1인당 지출은 증가 경향이 있습니다. 이 지역의 이점은 연구 중 URAT1 억제제와 IL-1 생물학적 제제에 대한 접근을 촉진하는 활발한 임상시험 네트워크에 의해 강화되었습니다. 그럼에도 불구하고 박스 경고의 영향과 페부크소스타트의 판매 중단으로 처방전의 내용이 변경되어 처방자는 새로운 메커니즘으로의 이행을 강요하고 있습니다.

유럽은 국민 모두 보험제도와 엄격한 가격통제가 금리를 줄이고 안정적인 성장에 기여하고 있습니다. 바이오시밀러의 보급률은 높고, 의료기술평가기관은 확실한 실임상 데이터를 요구하기 때문에 신규 진입의약품의 보급이 늦어지고 있습니다. 그러나 인구동태의 고령화와 비만 증가가 수요를 뒷받침하고 있으며, 류마티스의 전문시설은 세계적으로 영향력 있는 가이드라인을 갱신하고 있습니다.

아시아태평양은 급속한 도시화로 대사 증후군의 유병률이 상승하여 CAGR이 가장 높은 9.34%를 나타내 성장을 지속하고 있습니다. 중국의 통풍 이환율은 보험 확대와 함께 상승하고 있으며 LG화학과 JW제약 등 현지 기업들이 경쟁력 있는 가격 설정과 맞춤형 유전자 스크리닝을 결합한 URAT1 프로그램을 시작하도록 촉구하고 있습니다. 태평양도량국에서는 유전적 소인에 의해 혈청요산치가 세계에서 가장 높아 공중위생 캠페인에 박차가 걸리고 있습니다. 원격 류머티즘과 e-pharmacy 플랫폼은 농촌 지역의 사람들에게 쉽게 접근할 수 있게 하고, 제품 도달 범위를 확대하고, 다양한 소득층에 걸친 통풍 치료제 시장을 강화합니다.

남미와 중동/아프리카는 현재의 점유율은 작지만, 제네릭 의약품이 보다 입수가 용이해지고, 정부가 비감염성 질환 관리에 투자하기 때문에 2자리대의 성장을 보여줍니다. 통풍 진단에 관한 1차 케어 의사를 육성하는 사하라 이남의 노력과 기증자 자금을 통한 스크리닝 프로그램은 미래의 수량 증가를 예감합니다. 제조의 현지화와 가격 연동 모델을 전개하는 다국적 기업은 이러한 헬스케어 생태계의 성숙에 따라 선행자 이익을 획득할 수 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 비만에 의한 통풍 유병률의 상승

- 요산치 저하 가이드라인의 표적 치료에의 채용

- 생물제제 및 차세대 URAT1의 승인(AR882, SEL-212 등)

- FDA에 의한 난치성 통풍 치료제의 조기 승인 프로그램

- 파마코유전체학와 웨어러블 sUA 모니터링이 개별화를 가능

- 신흥 시장에서의 원격 류마티스 치료와 전자 약국의 확대

- 시장 성장 억제요인

- Febuxostat와 NSAID의 장기 사용에 대한 안전 경고 문제

- 만성 투여와 플레어 패러독스에 의한 어드히어런스의 저하

- 브랜드 의약품의 철수에 의한 가격 저하와 R&D ROI의 저하

- 푸딩체를 많이 포함하는 식품 광고에 대한 규제상의 감시가 수요를 감퇴

- 공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 약제 클래스별

- 크산틴 산화효소 억제제

- 요산배설촉진제

- 재조합 요산분해효소

- 콜히친

- 비스테로이드성 항염증제

- 코르티코스테로이드

- 인터루킨-1 억제제

- 기타

- 투여 경로별

- 경구

- 주사

- 질환 유형별

- 급성 통풍

- 만성 난치성 통풍

- 토파스성 통풍

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- Horizon Therapeutics(Amgen)

- Takeda Pharmaceutical Co.

- AstraZeneca(Ardea Biosciences)

- Novartis AG

- UCB Pharma

- Sobi

- Pfizer Inc.

- Regeneron Pharmaceuticals

- Selecta Biosciences

- Arthrosi Therapeutics

- XORTX Therapeutics

- Mitsubishi Tanabe Pharma

- JW Pharmaceutical

- Atom Bioscience

- Protalix BioTherapeutics

- Teijin Pharma

- Sanofi

- Hanmi Pharmaceutical

- Horizon Biosciences(Verinurad)

- Boehringer Ingelheim

제7장 시장 기회와 전망

KTH 25.10.28The gout therapeutics market generated USD 3.03 billion in 2024 and is forecast to reach USD 4.65 billion by 2030, advancing at a 7.37% CAGR during 2025-2030.

Rising disease prevalence tied to aging populations, metabolic syndrome, and obesity continues to enlarge the treated patient pool, while precision approaches such as pharmacogenomic testing and real-time serum-urate wearables are lifting diagnosis and treatment rates. Regulatory catalysts-including multiple Fast Track designations and an accelerating approval cycle for biologics-shorten time-to-market for novel agents, and companies are using these pathways to expand indications or launch next-generation URAT1 inhibitors. Supply-chain disruptions around febuxostat and lingering NSAID safety concerns are reshaping prescriber preferences toward alternative mechanisms, especially in cardiovascular-risk cohorts. Against this backdrop, the gout therapeutics market is benefiting from growing payer recognition that aggressive serum-urate control averts costly complications, which is supporting coverage for combination therapy, biologics, and companion diagnostics.

Global Gout Therapeutics Market Trends and Insights

Rising prevalence of gout driven by aging & obesity

Global cases climbed to more than 53 million in 2024, a 22.4% jump in age-standardized rates since 1990, and the trend is most pronounced among men older than 55 where prevalence exceeds 2,500 per 100,000 individuals. Aging populations in high-income nations combine with escalating obesity in urbanizing Asia-Pacific economies, broadening the base eligible for long-term urate-lowering therapy. Pacific Island communities illustrate genetically driven hyperuricemia compounded by rapid dietary westernization, a pattern expected to replicate across emerging markets. Persistent demand growth underpins steady expansion of the gout therapeutics market in both established and nascent healthcare systems.

Treat-to-target adoption of urate-lowering guidelines

Guidance from European and US rheumatology societies recommending serum urate below 6 mg/dL has recast gout management from episodic flare control to proactive disease modification. Health insurers increasingly reimburse serial serum-urate testing, combination therapy, and specialist visits because evidence shows that achieving target levels mitigates cardiovascular events. Although only 28.9% of US gout patients receive urate-lowering therapy today, compliance is expected to rise as digital adherence tools and pharmacist-led programs scale. Wider guideline adherence boosts average treatment duration per patient, directly enlarging the gout therapeutics market.

Boxed-warning safety issues for febuxostat & long-term NSAID use

The February 2023 FDA boxed warning that links febuxostat to greater cardiovascular mortality restricted its use to allopurinol-intolerant patients, cutting addressable volume by 70-80% fda.gov. Takeda's decision to withdraw branded Uloric in January 2025 underscores the commercial fallout. Similar cardiovascular and renal risk profiles limit extended NSAID courses, prompting prescribers to favor costlier but safer mechanisms such as URAT1 inhibition or biologics, which elevates therapy costs and complicates formulary access.

Other drivers and restraints analyzed in the detailed report include:

- Biologics & next-gen URAT1 approvals (e.g., AR882, SEL-212)

- Fast-track FDA programs for refractory gout therapies

- Poor adherence owing to chronic dosing & flare paradox

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Xanthine oxidase inhibitors captured 46.34% of gout therapeutics market share in 2024 on the strength of inexpensive generic allopurinol and brand-loyal febuxostat users. The segment still expands, but its 4% CAGR lags behind URAT1 inhibitors, whose 8.12% rate is redefining the gout therapeutics market size for uricosurics. Clinical data show that URAT1 inhibition retains efficacy even when ABCG2 polymorphisms blunt allopurinol response in over 50% of patients. These genetic insights dovetail with payer interest in precision medicine, pushing formulary committees to re-evaluate step-therapy rules that historically favored xanthine oxidase inhibition.

Pipeline dynamism favors innovators. AR882 and dotinurad headline a cohort of small-molecule URAT1 agents designed for once-daily oral dosing without oxypurinol accumulation, offering renal-safe profiles and fewer drug-drug interactions. Recombinant uricase biologics hold their niche in chronic refractory gout where tophi burden is high; pegloticase revenues rose 33% year-on-year before Amgen's acquisition of Horizon Therapeutics consolidated the category reuters.com. Meanwhile, IL-1 inhibitors such as canakinumab earned an adult-flare indication in December 2023, signaling expansion of anti-inflammatory biologics that complement urate-lowering backbones. Collectively, these evolving classes continue to broaden the gout therapeutics market by offering differentiated options matched to genetic, renal, and cardiovascular profiles.

The Gout Therapeutics Market is Segmented by Drug Class (Xanthine Oxidase Inhibitors, Uricosurics, Recombinant Uricase and More), by Route of Administration (oral and Injection), Application (Acute Gout, Chronic Refractory Gout and More), and Geography (North America, Europe, Asia-Pacific and More). The Report Offers the Value (in USD Million) for the Above Segments.

Geography Analysis

North America generated 41.72% of 2024 revenue owing to early biologic adoption, broad insurance coverage, and widespread specialist availability. Treat-to-target guidelines enjoy strong professional-society endorsement, and payers often reimburse serial serum-urate tests, sustaining higher per-patient spending. The region's dominance is reinforced by active clinical-trial networks that accelerate access to investigational URAT1 inhibitors and IL-1 biologics. Nevertheless, boxed-warning fallout and febuxostat discontinuation are reshaping formularies and nudging prescribers toward emerging mechanisms.

Europe contributes steady growth as universal coverage and stringent price controls temper margins. Uptake of biosimilars is higher, and health-technology assessment bodies require robust real-world data, slowing diffusion of new entrants. Yet the continent's aging demographics and rising obesity sustain underlying demand, and centers of excellence in rheumatology produce influential guideline updates that ripple globally.

Asia-Pacific posts the highest 9.34% CAGR as rapid urbanization escalates metabolic syndrome prevalence. China's gout prevalence is climbing alongside insurance expansion, prompting local firms such as LG Chem and JW Pharmaceutical to launch URAT1 programs that combine competitive pricing with tailored genetic screening. Pacific Island nations display some of the world's highest serum-urate levels due to genetic predisposition, spurring public-health campaigns that could translate into pharmaceutical uptake once budget allocations rise. Tele-rheumatology and e-pharmacy platforms facilitate outreach to rural populations, amplifying product reach and strengthening the gout therapeutics market across diverse income strata.

South America and the Middle East/Africa together account for a smaller share today but exhibit double-digit unit growth as generics become more accessible and governments invest in non-communicable disease management. Sub-Saharan initiatives to train primary-care physicians in gout diagnosis, plus donor-funded screening programs, foreshadow future volume gains. Multinationals that localize manufacturing or deploy tiered-pricing models can capture early-mover advantages as these healthcare ecosystems mature.

- Horizon Therapeutics (Amgen)

- Takeda Pharmaceutical Co.

- AstraZeneca (Ardea Biosciences)

- Novartis

- UCB

- Sobi

- Pfizer

- Regeneron Pharmaceuticals

- Selecta Biosciences

- Arthrosi Therapeutics

- XORTX Therapeutics

- Mitsubishi Tanabe Pharma

- JW Pharmaceutical

- Atom Bioscience

- Protalix BioTherapeutics

- Teijin Pharma

- Sanofi

- Hanmi Pharmaceutical

- Horizon Biosciences (Verinurad)

- Boehringer Ingelheim

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of gout driven by aging & obesity

- 4.2.2 Treat-to-target adoption of urate-lowering guidelines

- 4.2.3 Biologics & next-gen URAT1 approvals (e.g., AR882, SEL-212)

- 4.2.4 Fast-track FDA programs for refractory gout therapies

- 4.2.5 Pharmacogenomics & wearable sUA monitoring enable personalization

- 4.2.6 Tele-rheumatology & e-pharmacy expansion in emerging markets

- 4.3 Market Restraints

- 4.3.1 Boxed-warning safety issues for febuxostat & long-term NSAID use

- 4.3.2 Poor adherence owing to chronic dosing & flare paradox

- 4.3.3 Branded-drug withdrawals causing price erosion & lower R&D ROI

- 4.3.4 Regulatory scrutiny on purine-rich food advertising dampening demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Drug Class (Value)

- 5.1.1 Xanthine Oxidase Inhibitors

- 5.1.2 Uricosurics

- 5.1.3 Recombinant Uricase

- 5.1.4 Colchicine

- 5.1.5 NSAIDs

- 5.1.6 Corticosteroids

- 5.1.7 IL-1 Inhibitors

- 5.1.8 Others

- 5.2 By Route of Administration (Value)

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.3 By Disease Type (Value)

- 5.3.1 Acute Gout

- 5.3.2 Chronic Refractory Gout

- 5.3.3 Tophaceous Gout

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Horizon Therapeutics (Amgen)

- 6.4.2 Takeda Pharmaceutical Co.

- 6.4.3 AstraZeneca (Ardea Biosciences)

- 6.4.4 Novartis AG

- 6.4.5 UCB Pharma

- 6.4.6 Sobi

- 6.4.7 Pfizer Inc.

- 6.4.8 Regeneron Pharmaceuticals

- 6.4.9 Selecta Biosciences

- 6.4.10 Arthrosi Therapeutics

- 6.4.11 XORTX Therapeutics

- 6.4.12 Mitsubishi Tanabe Pharma

- 6.4.13 JW Pharmaceutical

- 6.4.14 Atom Bioscience

- 6.4.15 Protalix BioTherapeutics

- 6.4.16 Teijin Pharma

- 6.4.17 Sanofi

- 6.4.18 Hanmi Pharmaceutical

- 6.4.19 Horizon Biosciences (Verinurad)

- 6.4.20 Boehringer Ingelheim

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment