|

시장보고서

상품코드

1842448

얼굴용 주사제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Facial Injectables - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

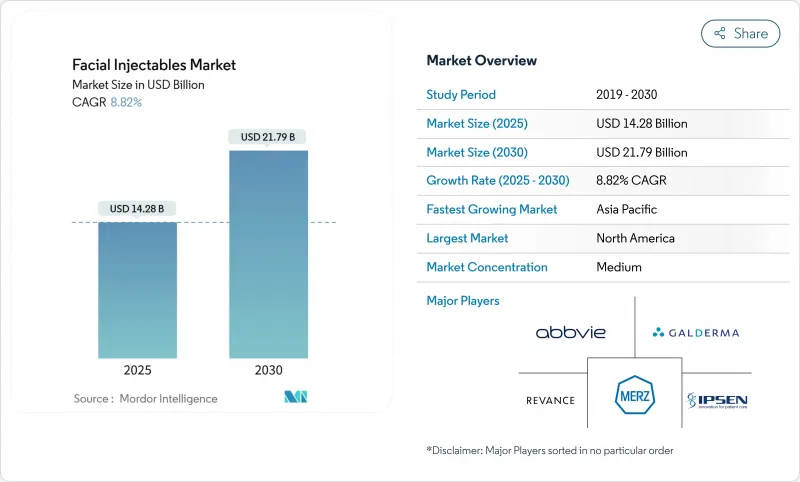

얼굴용 주사제 시장은 2025년에 142억 8,000만 달러로 평가되며, 2030년에는 217억 9,000만 달러에 이르고, CAGR 8.82%를 나타낼 것으로 예측됩니다.

낮은 침습 미용에 대한 소비자 수요가 증가하고 제품 과학이 더 오래 지속되고 편안한 결과를 가져올 수 있도록 진화하고 있기 때문에 성장은 안정적입니다. 청소년층에서의 예방적 신경조절제의 사용, 폴리뉴클레오티드 등의 재생 주사제의 출현, 환자 1인당 지출을 늘리는 정기 구매 프로그램의 통합 등이 대응 가능한 기반을 확대하고 있습니다. 북미는 여전히 가장 큰 수익원이지만, 아시아태평양은 의료 관광과 중간층 증가를 배경으로 모든 지역을 능가하고 있습니다. 경쟁 격화는 기존 리더가 파이프라인 자산을 획득하고 소규모 진출기업이 얼굴용 주사제 시장에서 가장 급성장하고 있는 2개의 코호트인 Z세대와 남성 환자를 타겟으로 차별화된 가격 설정과 마케팅을 추구하고 있기 때문입니다.

세계의 얼굴용 주사제 시장 동향과 인사이트

소셜 미디어 주도의 아기 보톡스 동향

시장의 기세는 미묘한 예방 효과를 요구하는 Z 세대 소비자에게 호소하는 소량의 신경 조절제 주사에 의해 지원됩니다. TikTok과 Instagram의 인플루언서 게시물은 조기 개입에 대한 편견을 없애고 20-29세 환자의 시술 건수는 2019년부터 2022년 사이에 71% 증가했습니다. 브랜드는 현재 청소년을 대상으로 메시징 앱과 로열티 앱을 조정하여 얼굴용 주사제 시장에서 이 부문의 평생 가치를 확대하고 있습니다.

국경을 넘은 미용 투어리즘이 시술량 촉진

연간 1,000만 명의 환자가 미용 치료를 위해 여행하고 있는 것으로 추정되며, 그 60%가 주사를 선택하고 있습니다. 코스트 메리트, 외과의사의 평판, 합리화된 비자 정책에 의해 한국, 멕시코, 두바이는 교통량이 많은 허브가 되고 있습니다. 이 나라의 클리닉은 다국어 애프터 케어 프로그램을 연마하고 주입제와 보조 치료를 결합하여 얼굴용 주사제 시장에 안정적인 수요를 유입시키고 있습니다.

브랜드 신뢰를 해치는 위조 필러의 만연

2024년에 FDA가 보톡스의 위조 로트에 대해 경고를 발행했고, 그 후 CDC가 권고를 함으로써 소비자의 관심이 높아지고 있습니다. 특정 시장에서공급량의 추정 10%는 규제되지 않기 때문에 얼굴용 주사제 시장에서 활동하는 브랜드에 있어서 컴플라이언스 코스트를 인상하는 보다 엄격한 직렬화와 임상의 교육 프로그램에 박차가 걸리고 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

- 장시간 작용형 리도카인 HA 필러에 의한 환자 처리 능력의 향상

- 보툴리눔툭신(보톡스) 제제의 새로운 적응증이 승인

- 주사자 라이선스 규칙의 엄격화로 공급자 용량이 제한됨

부문 분석

보툴리눔툭신(보톡스)는 2024년 매출의 56.10%를 차지하며 높은 반복률과 여러 미용·치료 적응으로 얼굴용 주사제 시장을 지원했습니다. 그래블러 라인, 까마귀 발자국, 새로운 적응 외 사용 등 의사가 익숙한 광범위한 임상 데이터에 뒷받침되어 그 보급은 계속 견조합니다. 제조업체 각사는 차세대 혈청형이나 투여 간격의 연장이나 투여 개시까지의 시간을 단축하는 적응 확대에 의해 점유율을 지키고 있습니다.

히알루론산 필러는 10.23%의 연평균 복합 성장률(CAGR)을 나타내 발전하고 있으며, 이는 제품 중 가장 빠릅니다. 트리히알루론산 가교와 리도카인 봉입에 의해 내구성이 12-18개월로 연장되어 환자의 쾌적성이 향상되고 있습니다. 콜라겐, 칼슘 하이드 록실 아파타이트, 폴리 L 락트산은 목표 볼륨 회복을위한 틈새 역할을 유지하고 지방 이식과 PMMA는 영구적인 결과를 추구하는 환자를 수용하고 얼굴 주입 산업의 상황에 깊이를 부여합니다.

여성은 2024년 시술의 80.76%를 차지하며, 이는 역사적인 채용 기간의 길이와 사회적 수용의 높이를 뒷받침했습니다. 예방 치료 메시징과 독감 마케팅은 클리닉에 대한 안정적인 방문을 지원합니다.

남성 시술 건수는 매년 10.04% 증가하고 있습니다. 수요의 중심은 남성적인 특징을 유지하기 위한 미묘한 이마의 완화와 턱 라인의 세련이며, 종종 미용적인 변화보다는 '개인적인 그루밍'으로 판매되고 있습니다. 클리닉은 남성에게 특화된 시간과 마케팅을 제공하고 얼굴용 주사제 시장의 부족한 부분을 획득하려고 합니다.

지역 분석

북미는 2024년에 38.75%의 매출 점유율을 차지하며, 8,800개 이상의 메디컬 스파와 특정 치료 용도에 대한 광범위한 보험 적용을 받았습니다. 이 지역의 8.45% 성장 페이스는 경기의 역풍과 위조품에 대한 규제 당국의 감시에 의해 완만해지고 있지만, 제품 혁신과 새로운 적응증이 시술 파이프라인을 건전하게 유지하고 있습니다.

아시아태평양은 2030년까지 10.89%의 두 자릿수 성장을 이룰 것으로 예측됩니다. 가처분 소득 증가, 미용에 대한 대중 문화의 관심, 한국과 태국의 성숙한 의료 관광 생태계는 지역 및 해외 고객을 끌어들이고 있습니다. LG화학과 같은 현지 기업들은 품질에 타협하지 않고 얼굴용 주사제 시장 규모를 확대하는 경쟁력 있는 가격의 충전제를 제조하고 있습니다.

유럽의 CAGR은 8.81%를 나타내 세련된 환자 의식과 범 EU 교육 네트워크의 결속에 의한 혜택을 받고 있습니다. 영국에서 제안한 라이선스 규칙은 임상 기준을 높이고 환자의 신뢰를 강화할 확률이 높고 얼굴용 주사제 시장의 확대를 지속합니다. 중동 및 아프리카는 CAGR 8.67%를 나타내 두바이의 고급 화장품 허브로 자리매김하고 사우디아라비아와 남아프리카의 도시 부유층의 인구 증가에 추진되고 있습니다. 남미는 브라질의 미용문화와 교정시술에 대한 보험상환 확대로 주사제에 대한 접근이 확대되고 CAGR은 9.23%를 나타낼 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 소셜 미디어에 뒷받침된 Z세대 소비자의 '베이비 보톡스' 동향

- 국경을 넘은 미용 투어리즘에 의한 시술량 증가

- 장시간 작용형 리도카인 강화 HA 필러에 의한 환자 처리 능력의 향상

- 보툴리눔툭신(보톡스) 제제의 새로운 적응이 승인

- 구독 기반 메드 스파 프로그램이 반복 소비를 촉진

- 재생 폴리뉴클레오티드 주사제의 대두에 의한 제품 구성의 확대

- 시장 성장 억제요인

- 브랜드의 신뢰를 해치는 위조 필러의 만연

- 공급자의 용량을 제한하는 주사기 라이선스 규제 강화

- 경제적 역풍에 의한 화장품에의 지출 억제

- HA 원료 공급의 제약에 의한 생산의 중단

- 공급망 분석

- 기술적 전망

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자/소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 유형별

- 보툴리눔툭신(보톡스)

- 히알루론산

- 콜라겐

- 칼슘 하이드록시아파타이트

- 폴리 L 락틱산

- 폴리메틸메타크릴레이트(PMMA)

- 지방 주입

- 기타 필러

- 성별

- 여성

- 남성

- 용도별

- 얼굴 주름 교정

- 입술 확대

- 안면 리프팅

- 여드름 흉터 치료

- 지방위축증 치료

- 기타 용도

- 최종 사용자별

- 병원 및 외래 수술 센터(ASC)

- 클리닉 및 미용 센터

- 메드스파 및 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- AbbVie Inc.(Allergan Aesthetics)

- Anika Therapeutics Inc.

- BioPlus Co. Ltd.

- Bloomage Biotechnology Corp. Ltd.

- EG Bio Co. Ltd.

- Evolus Inc.

- Galderma SA

- Huons Global Co. Ltd.

- IBSA Institut Biochimique SA

- Ipsen SA

- LG Chem Ltd.

- Medytox Inc.

- Merz Pharma GmbH & Co. KGaA

- PharmaResearch Products Co. Ltd.

- Revance Therapeutics Inc.

- Samyang Biopharm USA Inc.

- Sinclair France SAS

- Sinclair Pharma Ltd.

- Teoxane Laboratories SA

- Tiger Aesthetics Medical, LLC

제7장 시장 기회와 전망

KTH 25.10.28The facial injectables market is valued at USD 14.28 billion in 2025 and is forecast to reach USD 21.79 billion by 2030, advancing at an 8.82% CAGR.

Growth remains steady as consumer demand for minimally invasive aesthetics rises and product science evolves to deliver longer-lasting, more comfortable results. Preventative neuromodulator use among younger adults, the emergence of regenerative injectables such as polynucleotides, and the integration of subscription programs that lift per-patient spend are expanding the addressable base. North America continues to generate the largest revenue pool, yet Asia-Pacific is outpacing all regions on the back of medical tourism and a growing middle class. Competitive intensity is climbing as established leaders acquire pipeline assets and smaller entrants pursue differentiated pricing and marketing aimed at Gen Z and male patients-the two fastest growing cohorts in the facial injectables market.

Global Facial Injectables Market Trends and Insights

Social-media-driven Baby Botox trend

Market momentum is buoyed by smaller-dose neuromodulator injections that appeal to Gen Z consumers seeking subtle, preventative results. Influencer posts on TikTok and Instagram have removed stigma around early intervention, and procedural volume among patients aged 20-29 rose 71% between 2019 and 2022. Brands now tailor messaging and loyalty apps to younger budgets, extending the lifetime value of this segment inside the facial injectables market.

Cross-border aesthetic tourism boosting procedure volumes

An estimated 10 million patients travel annually for cosmetic care, with 60% opting for injectables. Cost advantages, surgeon reputation, and streamlined visa policies make South Korea, Mexico, and Dubai high-traffic hubs. Clinics in these destinations refine multilingual after-care programs and bundle injectables with adjunct treatments, channeling a steady inflow of demand into the facial injectables market.

Proliferation of counterfeit fillers undermining brand trust

FDA alerts in 2024 on falsified Botox lots and subsequent CDC advisories have heightened consumer concern. An estimated 10% of supply in certain markets is unregulated, which spurs stricter serialization and clinician education programs that raise compliance costs for brands active in the facial injectables market.

Other drivers and restraints analyzed in the detailed report include:

- Long-acting lidocaine HA fillers improving patient throughput

- New indications approved for botulinum toxin products

- Tightening injector-licensing rules limiting provider capacity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Botulinum toxin contributed 56.10% of 2024 revenue, anchoring the facial injectables market with high repeat rates and multiple cosmetic and therapeutic indications. Uptake remains strong across glabellar lines, crow's-feet and emerging off-label uses, supported by physician familiarity and broad clinical data. Manufacturers defend share through next-generation serotypes and on-label expansions that extend dosing intervals or speed onset.

Hyaluronic acid fillers are advancing at a 10.23% CAGR, the fastest among products. Tri-hyal cross-linking and lidocaine inclusion lengthen durability to 12-18 months and elevate patient comfort. Collagen, calcium hydroxylapatite and poly-L-lactic acid maintain niche roles for targeted volume restoration, while fat transfer and PMMA serve patients seeking permanent outcomes, contributing depth to the facial injectables industry landscape.

Women accounted for 80.76% of 2024 procedures, underscoring longer historical adoption and higher social acceptance. Preventative treatment messaging and influencer marketing sustain steady clinic footfall.

Male procedure volume is rising 10.04% annually. Demand centers on subtle forehead relaxation and jawline refinement that preserve masculine features, often marketed as "personal grooming" rather than cosmetic change. Clinics are offering male-focused hours and marketing to capture this unmet slice of the facial injectables market.

The Facial Injectables Market Report is Segmented by Product Type (Botulinum Toxin, Hyaluronic Acid, and More), Gender (Male and Female), Application (Facial Line Correction, Lip Augmentation, and More), End-User (Hospitals & Ambulatory Surgical Centers, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held a 38.75% revenue share in 2024, underpinned by 8,800+ medical spas and broad insurance coverage for certain therapeutic uses. The region's 8.45% growth pace is moderated by economic headwinds and regulatory scrutiny of counterfeit products, yet product innovation and new indications keep procedure pipelines healthy.

Asia-Pacific is projected to reach double-digit 10.89% growth through 2030. Rising disposable income, pop culture focus on beauty and mature medical tourism ecosystems in South Korea and Thailand attract both regional and international clients. Local firms like LG Chem scale competitively priced fillers that grow the facial injectables market size without compromising quality.

Europe delivers an 8.81% CAGR, benefiting from sophisticated patient awareness and cohesive pan-EU training networks. Proposed UK licensing rules are likely to lift clinical standards and reinforce patient trust, sustaining expansion in the facial injectables market. The Middle East and Africa record 8.67% CAGR, propelled by Dubai's positioning as a luxury cosmetic hub and growing urban affluent populations in Saudi Arabia and South Africa. South America advances 9.23% as Brazil's culture of aesthetics and expanding insurance reimbursement for corrective procedures broaden access to injectables.

- Abbvie

- Anika Therapeutics

- BioPlus

- Bloomage Biotechnology Corp. Ltd.

- EG Bio Co. Ltd.

- Evolus Inc.

- Galderma

- Huons Global Co. Ltd.

- IBSA Institut Biochimique SA

- Ipsen

- LG Chem

- Medytox

- Merz Pharma

- PharmaResearch Products Co. Ltd.

- Revance Therapeutics

- Samyang Biopharm USA Inc.

- Sinclair France SAS

- Sinclair Pharma Ltd.

- Teoxane Laboratories SA

- Tiger Aesthetics Medical, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Social-media-fueled "Baby Botox" trend among Gen Z consumers

- 4.2.2 Cross-border aesthetic tourism boosting procedure volumes

- 4.2.3 Long-acting lidocaine-enhanced HA fillers improving patient throughput

- 4.2.4 New indications approved for botulinum toxin products

- 4.2.5 Subscription-based MedSpa programs driving repeat spend

- 4.2.6 Rise of regenerative polynucleotide injectables expanding product mix

- 4.3 Market Restraints

- 4.3.1 Proliferation of counterfeit fillers undermining brand trust

- 4.3.2 Tightening injector-licensing rules limiting provider capacity

- 4.3.3 Economic headwinds reducing discretionary cosmetic spend

- 4.3.4 HA raw-material supply constraints disrupting production

- 4.4 Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Botulinum Toxin

- 5.1.2 Hyaluronic Acid

- 5.1.3 Collagen

- 5.1.4 Calcium Hydroxylapatite

- 5.1.5 Poly-L-lactic Acid

- 5.1.6 Polymethyl-methacrylate (PMMA)

- 5.1.7 Fat Injection

- 5.1.8 Other Fillers

- 5.2 By Gender

- 5.2.1 Female

- 5.2.2 Male

- 5.3 By Application

- 5.3.1 Facial Line Correction

- 5.3.2 Lip Augmentation

- 5.3.3 Face-Lift

- 5.3.4 Acne Scar Treatment

- 5.3.5 Lipoatrophy Treatment

- 5.3.6 Other Applications

- 5.4 By End-User

- 5.4.1 Hospitals & Ambulatory Surgical Centers

- 5.4.2 Clinics & Aesthetic Centers

- 5.4.3 MedSpas & Others

- 5.5 By Geography (Value)

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AbbVie Inc. (Allergan Aesthetics)

- 6.4.2 Anika Therapeutics Inc.

- 6.4.3 BioPlus Co. Ltd.

- 6.4.4 Bloomage Biotechnology Corp. Ltd.

- 6.4.5 EG Bio Co. Ltd.

- 6.4.6 Evolus Inc.

- 6.4.7 Galderma SA

- 6.4.8 Huons Global Co. Ltd.

- 6.4.9 IBSA Institut Biochimique SA

- 6.4.10 Ipsen SA

- 6.4.11 LG Chem Ltd.

- 6.4.12 Medytox Inc.

- 6.4.13 Merz Pharma GmbH & Co. KGaA

- 6.4.14 PharmaResearch Products Co. Ltd.

- 6.4.15 Revance Therapeutics Inc.

- 6.4.16 Samyang Biopharm USA Inc.

- 6.4.17 Sinclair France SAS

- 6.4.18 Sinclair Pharma Ltd.

- 6.4.19 Teoxane Laboratories SA

- 6.4.20 Tiger Aesthetics Medical, LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment