|

시장보고서

상품코드

1842472

치과용 시멘트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Dental Cement - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

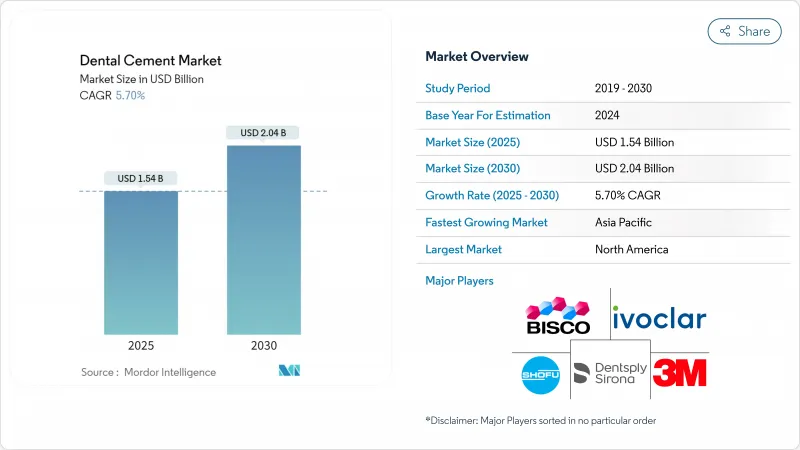

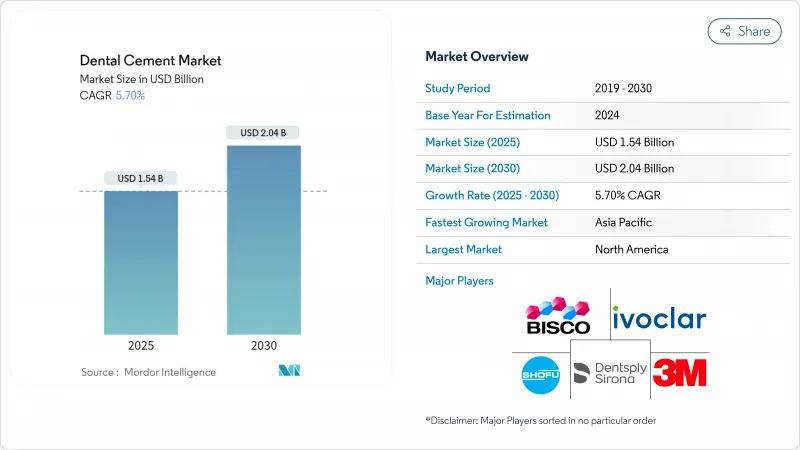

치과용 시멘트 시장 규모는 2025년 15억 4,000만 달러에 이르고, 2030년에는 CAGR 5.70%를 나타내 20억 4,000만 달러로 확대될 것으로 예측됩니다.

이 기세는 인구통계학적 압력, 처치 건수 증가, 긴 수명과 심미성을 향상시키는 생물활성 제제와 나노하이브리드 제제의 기술진보의 합류로부터 발생하고 있습니다. 유럽 연합(EU)의 수은 아말감 금지령(2025년 1월 발효)은 불소 서방형 무수은 시멘트에 대한 급속한 대체를 일으키며, 다른 지역에서도 유사한 법률이 보급되고 있습니다. CAD/CAM 및 3D 프린터를 통한 디지털 워크플로우는 첨단 시멘트 시스템의 적응증을 지속적으로 확대하고 인공지능은 재료 선택과 임베디드 프로토콜을 개선하고 있습니다. 특수 모노머와 희토류 필러공급 체인 마찰이 역풍이 되고 있지만, 다양한 조달처와 유효한 규제 서류를 가진 제조업체는 프리미엄 부문에서 가격 결정력을 유지하고 있습니다.

세계의 치과용 시멘트 시장 동향과 인사이트

우식과 무치악증 증가

치료되지 않은 우식은 2024년에 약 35억 명의 사람들에게 영향을 미치며 치과용 시멘트 시장을 지원하는 지속적인 임상 작업량을 확립했습니다. 인구 역학의 노화는 무치악증을 증가시키고 고강도 영구 시멘트에 의존하는 내구성이 있는 보철 솔루션에 대한 수요를 높이고 있습니다. 세계 경제적 부담(직접 비용으로 3,870억 달러, 간접 비용으로 3,230억 달러)은 재치료 사이클을 최소화하는 시멘트의 필요성을 강화하고 있습니다. 생물활성, 불소 서방형, 간소화된 워크플로우를 입증하는 제조업체는 치과용 시멘트 시장에서 비용에 민감한 의료 제공업체들 사이에서의 채용을 강화하고 있습니다.

치열 교정·보철 처치 건수 증가

조사에 의하면, 젊은 성인의 20.6%가 얼라이너 치료를 희망하고 있어, 세라믹 브래킷이나 클리어 얼라이너 어태치먼트에 적합한 시멘트에 대한 수요가 높아지고 있습니다. CAD/CAM과 3D 프린팅이 의자 시간을 단축하고 심미성을 향상시키기 위해 지르코니아, 리튬 디실리케이트, 폴리머 침투 세라믹에 접착하는 시멘트에 대한 요구가 높아지고 있습니다. 로봇 공학과 인공지능을 치과 보철학에 통합하면 접착 강도와 마지널 무결성의 성능 기준을 높일 수 있습니다. 이러한 요인은 치과용 시멘트 시장의 장기적인 수요 동향을 강화합니다.

소규모 치과 진료소의 높은 가격 감도

독립 클리닉의 95%가 2024년 공급 비용 상승을 보고했으며 위생사 임금은 2018년부터 2023년 사이에 26.6% 상승하여 금리를 침식했습니다. 이 치과 진료소는 비싼 생체 활성 시멘트를 저가의 대체품으로 대체하는 경우가 많으며 가격 탄력성이있는 지역에서의 보급이 늦어지고 있습니다. 보험 상환의 상한은 조달의 절충을 악화시키고 클리닉이 시멘트 시스템을 선택할 때 총 치료비를 평가하도록 촉구하고 있습니다. 신흥 시장에서는 이러한 역학이 선진배합의 수량 성장을 제한하고 치과용 시멘트 시장 전체의 확대를 억제하고 있습니다.

분석되는 기타 성장 촉진요인 및 억제요인

- 심미/미용치과의 성장

- 수은 프리, 불소 서방형 수복물에의 규제 강화

- ISO 4049 및 FDA 510(k)의 엄격한 성능 검증

부문 분석

2024년 치과용 시멘트 시장 점유율의 72.34%는 영구재가 차지했으며 크라운, 브리지, 임플란트 수리에 있어 전체 수익을 지원했습니다. 액티바 바이오액티브와 같은 강화된 생체활성 제제는 불화물, 칼슘, 인산염 이온을 방출하고 재석회화를 촉진하여 2차 충치 위험을 줄입니다. 유니버설 셀프 어드히티브 화학은 별도의 프라이머를 사용할 필요가 없으므로 임상 워크플로를 간소화하고 대량 진료를 위한 의자 시간을 단축합니다.

임시 착용 시멘트는 수익이 작은 것, 다단계 임플란트 사례 및 복잡한 재활이 증가함에 따라 CAGR 6.34%를 나타낼 전망입니다. 게다가 최종 임베디드 전의 교합 확인에 가착 수복물을 사용하는 당일 CAD/CAM 워크플로우의 대두도 수요를 뒷받침하고 있습니다. 오이게놀이 없는 레진 강화 잠간 시멘트의 기술 혁신은 회수성을 손상시키지 않고 안정성을 향상시켜 치과용 시멘트 시장에서 환자의 사용감과 클리닉의 효율을 높여줍니다.

지역 분석

2024년 치과용 시멘트 시장 점유율은 북미가 39.42%로 최고였으며, 선진적인 치과 인프라, 높은 보험 보급률, 디지털 치과의 보급에 지지되었습니다. 치과 서비스 기관의 확대로 조달 프로토콜이 표준화되어 고급 바이오 액티브 시스템의 보급이 가속화되고 있습니다. FDA의 510(k) 패스웨이에 의한 규제의 명확화는 특히 만능 접착제와 듀얼 큐어 제품의 조기상시를 촉진하고 있습니다.

아시아태평양의 CAGR은 가장 빠른 7.23%를 나타내 중류 계급의 인구 증가와 의식 향상 캠페인에 힘쓰고 있습니다. 인도에는 약 65,000 개의 치과 진료소가 있으며 17억 달러의 치과 생태계가 구축되어 성능과 저렴한 균형을 유지하는 수리 재료에 대한 수요가 증가하고 있습니다. 중국의 급속한 도시화는 수리 처치의 건수를 증가시키고 일본과 한국은 선진재료의 혁신과 노인의료 보험 지원을 통해 공헌하고 있습니다. 그럼에도 불구하고 치과용 시멘트 시장에서는 치과 진료소가 프리미엄 기능과 예산 제약을 비교 검토하기 때문에 가격에 민감한 치과 진료소가 단계적인 포트폴리오 전략을 결정하고 있습니다.

유럽에서는 2025년 1월 수은 아말감 금지령을 받아 수은을 포함하지 않는 불소 서방형 시멘트로의 전환이 가속화되고 있습니다. 독일, 프랑스, 영국은 보철 교육 프로그램이 충실하며 심미 치료를 선호하는 소비자가 많기 때문에 수요 선진을 끊고 있습니다. ISO106 치과 표준에 따른 규제 조화는 제품 품질 기준을 인상하고 생체적합성과 장기 임상 데이터를 문서화한 제조업체를 우월합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 우식과 무치악증의 유병률 상승

- 치열 교정·보철 처치 증가

- 심미치과의 성장

- 수은 프리, 불소 서방형 수복물에의 규제 강화(과소보고)

- 생체활성 및 나노하이브리드 시멘트 기술의 급속한 대두(과소보고)

- 시장 성장 억제요인

- 소규모 치과 진료소의 가격 감도 높이

- 엄격한 ISO 4049와 FDA 510(k)의 성능 검증

- 특수 모노머와 희토류 필러공급 체인 경직(과소보고)

- 오이게놀과 Bis-GMA의 폐기에 관한 환경조사(과소보고)

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 유형별

- 영구적

- 임시적

- 소재별

- 산화아연 유제놀

- 인산아연

- 폴리카르복실레이트

- 글래스 아이오노머

- 수지 베이스

- 기타

- 용도별

- 치수 보호

- 접착 및 본딩

- 수복물

- 수술용 드레싱

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M

- Dentsply Sirona

- Danaher(Envista-Kerr)

- Ivoclar Vivadent

- GC Corporation

- SHOFU Dental

- Coltene Holding

- Kuraray Noritake Dental

- BISCO

- Medental International

- VOCO GmbH

- Tokuyama Dental

- Ultradent Products

- Septodont

- SDI Limited

- Pulpdent

- DenMat Holdings

- DMG Chem-Pharma

- FGM Dental

- Kuraray America

제7장 시장 기회와 전망

KTH 25.10.28The dental cement market size reached USD 1.54 billion in 2025 and is forecast to expand to USD 2.04 billion by 2030 at a 5.70% CAGR, underscoring consistent demand for restorative materials that comply with tightening global regulations environment.

Momentum stems from a confluence of demographic pressures, rising procedural volumes, and technological progress in bio-active and nano-hybrid formulations that improve longevity and aesthetics. The European Union's mercury amalgam ban, effective January 2025, has triggered rapid substitution toward fluoride-releasing, mercury-free cements and similar legislation is proliferating in other regions. Digital workflows in CAD/CAM and 3-D printing continue to widen the indications for advanced cement systems, while artificial intelligence is refining material selection and placement protocols. Supply-chain friction in specialty monomers and rare-earth fillers poses a headwind, yet manufacturers with diversified sourcing and validated regulatory dossiers maintain pricing power in premium segments.

Global Dental Cement Market Trends and Insights

Rising Prevalence of Dental Caries and Edentulism

Untreated dental caries affected nearly 3.5 billion people in 2024, establishing a persistent clinical workload that sustains the dental cement market. Aging demographics elevate edentulism rates and heighten demand for durable prosthodontic solutions that rely on high-strength permanent cements. The global economic burden-USD 387 billion in direct costs and USD 323 billion in indirect costs-reinforces the need for cements that minimize retreatment cycles. Manufacturers that demonstrate bio-activity, fluoride release, and simplified workflows strengthen adoption among cost-sensitive providers within the dental cement market.

Increasing Orthodontic & Prosthodontic Procedure Volumes

Surveys indicate 20.6% of young adults intend to pursue aligner therapy, intensifying demand for cements compatible with ceramic brackets and clear-aligner attachments. Prosthodontics is scaling as CAD/CAM and 3-D printing shorten chair time and elevate aesthetics, driving need for cements that bond to zirconia, lithium-disilicate, and polymer-infiltrated ceramics. Integration of robotics and AI in prosthodontics raises performance benchmarks for bond strength and marginal integrity. These factors reinforce long-term demand trajectories in the dental cement market.

High Price Sensitivity Among Small Dental Clinics

Ninety-five percent of independent practices reported higher supply costs in 2024, while hygienist wages increased 26.6% between 2018 and 2023, eroding margins. These clinics often substitute premium bio-active cements with lower-cost alternatives, slowing penetration in price-elastic regions. Insurance reimbursement ceilings exacerbate procurement trade-offs, prompting practices to evaluate total cost of care when selecting cement systems. In emerging markets, the dynamic limits volume growth for advanced formulations, moderating overall expansion in the dental cement market.

Other drivers and restraints analyzed in the detailed report include:

- Growth of Cosmetic / Aesthetic Dentistry

- Regulatory Push Toward Mercury-Free, Fluoride-Releasing Restoratives

- Stringent ISO 4049 & FDA 510(k) Performance Validations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Permanent products held 72.34% of the dental cement market share in 2024, anchoring overall revenue due to their role in definitive crowns, bridges, and implant restorations. Enhanced bio-active formulations such as ACTIVA BioACTIVE release fluoride, calcium, and phosphate ions, promoting remineralization and mitigating secondary caries risk. Universal self-adhesive chemistries simplify clinical workflows by eliminating separate primers, reducing chair time for high-volume practices.

Temporary cements, although smaller in revenue, are forecast to expand at a 6.34% CAGR as multi-stage implant cases and complex rehabilitations proliferate. Demand is further buoyed by the rise of same-day CAD/CAM workflows that use temporary restorations for occlusal verification before final placement. Innovations in eugenol-free, resin-reinforced temporary cements improve stability without compromising retrievability, enhancing patient experience and clinic efficiency within the dental cement market.

The Dental Cement Market Report Segments the Industry Into by Product Type (Temporary and Permanent ), by Material Type (Glass Ionomer, Zinc Oxide Eugenol, Zinc Phosphate and More), by Application (Pulpal Protection, Luting & Bonding and More), by End User (Hospitals, Dental Clinics, Other End Users), and Geography (North America, Europe, Asia-Pacific and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 39.42% of the dental cement market share in 2024, underpinned by advanced dental infrastructure, high insurance penetration, and widespread adoption of digital dentistry. Expansion of dental service organizations is standardizing procurement protocols and accelerating uptake of premium bio-active systems. Regulatory clarity provided by FDA 510(k) pathways, despite added stringency, encourages early commercial launches, particularly for universal adhesive and dual-cure products.

Asia-Pacific delivers the fastest 7.23% CAGR, propelled by growing middle-class populations and heightened awareness campaigns. India hosts roughly 65,000 dental clinics and a USD 1.7 billion dental ecosystem, fuelling demand for restorative materials that balance performance with affordability. China's rapid urbanization raises restorative procedure volumes, while Japan and South Korea contribute through advanced materials innovation and insurance support for geriatric care. Nonetheless, price sensitivity dictates tiered portfolio strategies as clinics weigh premium features against budget constraints in the dental cement market.

Europe confronts immediate material transition challenges following the January 2025 mercury amalgam ban, instigating accelerated adoption of mercury-free, fluoride-releasing cements environment. Germany, France, and the United Kingdom spearhead demand given robust prosthodontic training programs and consumer preference for aesthetic treatments. Regulatory harmonization via ISO 106 dentistry standards elevates product quality thresholds, favoring manufacturers with documented biocompatibility and long-term clinical data.

- 3M

- Dentsply Sirona

- Danaher (Envista - Kerr)

- Ivoclar Vivadent

- GC Corporation

- SHOFU Dental

- Coltene Holding

- Kuraray Noritake Dental

- BISCO

- Medental International

- VOCO

- Tokuyama Dental

- Ultradent Products

- Septodont

- SDI

- Pulpdent

- DenMat Holdings

- DMG Chem-Pharma

- FGM Dental

- Kuraray America

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of dental caries and edentulism

- 4.2.2 Increasing orthodontic & prosthodontic procedure volumes

- 4.2.3 Growth of cosmetic / aesthetic dentistry

- 4.2.4 Regulatory push toward mercury-free, fluoride-releasing restoratives (under-reported)

- 4.2.5 Rapid emergence of bio-active & nano-hybrid cement technologies (under-reported)

- 4.3 Market Restraints

- 4.3.1 High price sensitivity among small dental clinics

- 4.3.2 Stringent ISO 4049 & FDA 510(k) performance validations

- 4.3.3 Supply-chain crunch in specialty monomers & rare-earth fillers (under-reported)

- 4.3.4 Environmental scrutiny on eugenol & Bis-GMA disposal (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Type

- 5.1.1 Permanent

- 5.1.2 Temporary

- 5.2 By Material

- 5.2.1 Zinc-Oxide Eugenol

- 5.2.2 Zinc Phosphate

- 5.2.3 Polycarboxylate

- 5.2.4 Glass Ionomer

- 5.2.5 Resin-Based

- 5.2.6 Others

- 5.3 By Application

- 5.3.1 Pulpal Protection

- 5.3.2 Luting & Bonding

- 5.3.3 Restorations

- 5.3.4 Surgical Dressing

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 3M

- 6.3.2 Dentsply Sirona

- 6.3.3 Danaher (Envista - Kerr)

- 6.3.4 Ivoclar Vivadent

- 6.3.5 GC Corporation

- 6.3.6 SHOFU Dental

- 6.3.7 Coltene Holding

- 6.3.8 Kuraray Noritake Dental

- 6.3.9 BISCO

- 6.3.10 Medental International

- 6.3.11 VOCO GmbH

- 6.3.12 Tokuyama Dental

- 6.3.13 Ultradent Products

- 6.3.14 Septodont

- 6.3.15 SDI Limited

- 6.3.16 Pulpdent

- 6.3.17 DenMat Holdings

- 6.3.18 DMG Chem-Pharma

- 6.3.19 FGM Dental

- 6.3.20 Kuraray America

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment