|

시장보고서

상품코드

1842573

자궁경 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Hysteroscope - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

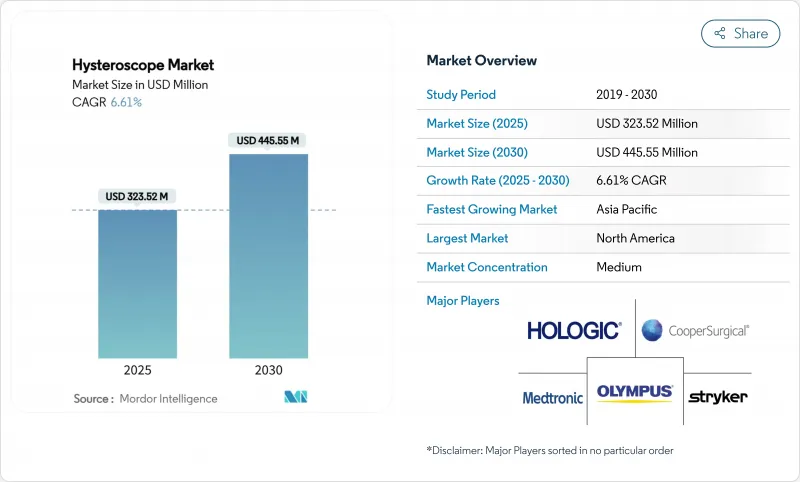

세계의 자궁경 시장은 2025년에 3억 2,352만 달러로 추정되고, 2030년에는 4억 4,555만 달러에 이를 것으로 예측됩니다.

저침습 부인과 수술의 보급, 사무실 기반 케어에 대한 지불자의 지원 확대, 고급 광학 시스템과 엄격한 감염 제어 프로토콜을 융합시킨 급속한 제품 혁신이 성장을 뒷받침하고 있습니다. 단일 사용 장치 플랫폼, 클라우드 연결 이미지 처리, 인공지능(AI) 의사결정 지원은 워크플로를 재구성하고 총 수술 비용을 낮추고 있습니다. 병원은 여전히 조달량을 지원하고 있지만, 진료 보상 규칙이 외래 환자를 우월하기 때문에 현재는 독립적인 부인과 클리닉이 선택적 치료의 점유율을 확대하고 있습니다. 경성 자궁경은 복잡한 수술실에서 여전히 선택되는 플랫폼이지만, 일회용 제품은 특히 재처리 능력이 제한된 경우 치료 증가의 원동력이 되고 있습니다. 선도적인 제조업체가 차별화된 기술과 지역 비계를 확보하기 위해 인수를 추구하기 때문에 경쟁의 치열성이 커지고 있습니다.

세계의 자궁경 시장 동향 및 인사이트

저침습 부인과 수술에 대한 수요 증가

현재 임상의는 자궁을 온존하고 회복을 단축하며 합병증을 억제하는 절개를 수반하지 않는 선택을 선호하고 있습니다. 전문적인 데이터에 따르면, 질식 자연 개방 경관 내시경 자궁 절제술은 복강경 수술과 비교하여 직장 복귀의 중앙값을 3개월에서 2개월로 단축할 수 있습니다. 메이요 클리닉은 자궁경하수술은 복부 절개를 피하고 입원 기간을 단축할 수 있기 때문에 자궁내 병변의 제일 선택이라고 합니다. 고밀도 초점 초음파와 고주파 소작술을 포함한 새로운 기술은 자궁 선근증과 자궁 근종의 새로운 치료 분야를 개척하고 있습니다. 로봇 관절, AI를 활용한 타겟팅, 강화된 시각화로 정확도가 더욱 향상되고, 자궁경 수술은 기존의 개복 수술과 복강경 수술을 대체하는 옵션으로 점유율을 획득하고 있습니다.

감염 관리를 위한 일회용 자궁경의 신속한 채용

내시경 재처리 실패에 대한 모니터링 강화는 시설에 재사용 가능한 기구의 위험 이익 방정식을 재평가하도록 촉구합니다. FDA(미국 식품의약국)의 안전성 정보는 특히 재처리 검증이 비용적으로 어려운 소량의 센터에서는 오염의 위험성을 강조하고 있습니다. ACOG는 결정적인 비용 효율성 조사가 없다고 지적했지만 표면 결함이나 부적절한 오염 제거가 고장률을 높일 것이라고 경고합니다. Minerva Surgical과 같은 제조업체는 재사용 가능한 범위에 필적하는 광학 시스템을 제공하면서 재처리 단계를 제거하는 완전 일회용 플랫폼에서 지원합니다. 미래에 메디케어의 지불 조정이 처치당 소모품 비용 증가를 다루면 외래 채용 곡선이 빠르게 급경사가 될 수 있습니다.

재사용형 자궁경에 의한 감염 위험

복잡한 장비의 모양은 무균 처리 팀을 괴롭히고 제조업체의 지침과 시설 자원의 불일치는 재처리 오류를 유발합니다. ANSI/AAMI ST108의 수질 가이드라인은 인프라스트럭처의 비용을 상승시키고 오염 사건에 대한 소송에 대한 공포가 관리자를 일회용 옵션으로 향하게 합니다. NYU Langone Health는 전문 부문 횡단 팀을 배치하여 결함을 줄였으나 자원 부담이 크고 단가가 높음에도 불구하고 소규모 시설이 일회용 범위를 채택하는 이유를 돋보이게 합니다.

부문 분석

경성 스코프는 2024년 매출의 45.35%를 차지했으며, 복잡한 자궁내 수술에서 입증된 광학적 투명성 및 조작성을 반영합니다. 경성 플랫폼의 자궁경 시장 규모는 2024년에 1억 4,700만 달러에 이르렀으며, 3차 센터 내에서 높은 자본 이용률에 의해 지원되고 있습니다. 대조적으로 일회용 스코프는 CAGR 15.25%로 가장 높은 성장 궤도를 기록하고 재처리 능력이 제한되어 배상 책임 보험료가 상승하고 있는 곳에서 급속한 견인력을 얻고 있습니다. 사무실 환경에서 환자에게 더 편안하고 사례 간의 소요 시간이 단축됨에 따라 일회용은 처리량 지향 클리닉에게 매력적입니다.

재사용 가능한 이미지 처리 장치와 일회용 외장을 결합한 하이브리드 솔루션은 기존 제품의 경계를 모호하게 만들고 비용과 감염 제어 목표의 균형을 맞추어 채택을 가속화할 수 있습니다. 2024년 5월에 FDA의 인가를 받은 메디트리나의 2세대 플랫폼은 경량의 인체공학과 4K의 시각화를 융합시킨 혁신적인 기술로, 경성 포맷과 연성 포맷 사이의 성능 격차를 줄일 수 있습니다. 유연한 범위는 여전히 틈새 시장이며 해부학적으로 어려운 사례와 환자의 허용 범위가 최우선적인 경우에 의해 지원되지만 획득 비용이 높고 절차의 적응 범위가 좁기 때문에 점유율이 느립니다.

진단용 자궁경은 2024년 총 수술 횟수의 62.53%를 차지했으며, 이는 자궁의 첫 번째 선택 검사에서의 보편적인 역할을 반영합니다. 진단 범위는 직경이 작고 워크플로우가 간소화되어 외래에서의 무마취 평가에 이상적인 것으로 임상의가 지지하고 있습니다. CAGR 9.85%로 확대하는 외과 수술은 1회의 진찰로 폴립 절제, 자궁근종 절제, 절제를 가능하게 하는 조직 제거 시스템이나 에너지 장치로부터 혜택을 받습니다. 2025년 코호트 연구의 증거에 따르면 콜드나이프 자궁경하 자궁내막 박리술+호르몬 요법은 심한 자궁내 유착에서 94.07%의 성공률을 달성하고 과거 표준을 능가하고 있습니다.

병원과 고도 외래 센터는 복잡한 수술 워크플로우를 간소화하는 통합 이미지 스택 및 AI 지원 지침에 투자합니다. 이러한 업그레이드는 자본 예산을 증가시키지만 진단과 치료를 결합한 세션이 전체적인 에피소드 오브 케어 비용을 삭감하기 때문에 상환 가능성도 높입니다. 시뮬레이션 훈련과 텔레멘터링으로 외과의사의 숙련도가 향상됨에 따라 선진국과 신흥국 모두에서 수술 하위 부문에서 2자리수의 수술 확대가 유지될 것으로 예측됩니다.

지역 분석

북미는 2024년에 37.63%의 점유율로 선두를 이끌었고, 선진적인 지불자 모델, 광범위한 서브스페셜리티 트레이닝, AI 강화 시각화 시스템의 급속한 보급에 힘입었습니다. 미국은 압도적인 수술 건수를 유지하고, 캐나다는 공적 자금에 의한 헬스케어 제도 하에서 유사한 기술을 채용하고 있습니다. 멕시코에서는 민간 병원 부문의 성장 및 의료 관광의 노력이 저침습 치료를 요구하는 지역의 환자를 끌어들이고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 9.91%로 예측되어 가장 급성장하고 있는 지역입니다. 가처분 소득 증가, 보험 적용 범위 확대, 높은 부인과 질환 부담이 수요를 지원합니다. 체계적인 2025년 분석에서는 특히 남아시아 전역에서 자궁경부암과 자궁체암이 지속적으로 증가하여 검진과 수술의 필요성이 높아질 것으로 예측되고 있습니다. 중국과 일본은 국내 장비 생산에 많은 투자를 하고 공급망을 단축하며 현지 설치를 지원하는 한편 인도의 새로운 판매 규약은 규제의 성숙을 부각시키고 세계 공급업체 시장 진입을 가속시킬 것입니다.

유럽은 세계 제조 기준에 영향을 미치는 엄격한 안전 및 환경 규제에서 안정적인 성장을 유지하고 있습니다. 라이프사이클의 투명화를 추진하는 이 지역은 재활용 가능한 컴포넌트를 중심으로 한 설계 혁신을 촉진하고 있습니다. 한편, 중동 및 아프리카와 라틴아메리카에서는 도시의 사립 병원이나 불임 치료 센터가 중심이 되어 서서히 도입이 진행되고 있지만, 노동력 부족과 불균등한 진료 보수가 보급을 늦추고 있습니다. 교육의 공동 실시와 클라우드를 이용한 원격 지도에 의해 예측 기간 중 능력 격차는 축소될 것으로 보입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 자궁질환 및 이상 발생률 증가

- 저침습 부인과 수술에 대한 수요 증가

- 광학 기술 및 소형화 기술의 진보

- 감염 관리를 위한 단회 사용 자궁경의 급속한 채용

- 오피스 기반의 자궁경 검사로의 시프트에 의한 총 치료비 저하

- AI 지원 이미지 및 클라우드 분석의 통합

- 시장 성장 억제요인

- 재사용 가능한 자궁경에 의한 감염 위험

- 신흥 시장에서 훈련된 자궁경의 부족

- 일회용 디바이스에 대한 지속가능성 우려

- 모르셀레이션 및 체액 관리에 관한 규제의 정사

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 경성 자궁경

- 연성 자궁경

- 일회용 자궁경

- 모달리티별

- 진단용

- 수술용

- 컴포넌트별

- 스코프 샤프트 및 광학계

- 카메라 헤드 및 이미징 시스템

- 광원

- 분주 매체 및 펌프

- 액세서리 및 소모품

- 용도별

- 폴립 절제술

- 자궁근종 핵출술

- 자궁내막 소작술

- 불임 평가 및 치료

- 유착절제술 및 격벽절제술

- 기타

- 최종 사용자별

- 병원

- 외래수술센터(ASC)

- 부인과 클리닉

- 불임치료센터

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- B. Braun SE

- Boston Scientific Corp.

- CooperSurgical Inc.

- Gynesonics

- Hologic Inc.

- Karl Storz SE & Co. KG

- LiNA Medical

- MedGyn Products Inc.

- Medtronic plc

- Olympus Corporation

- Richard Wolf GmbH

- Smith & Nephew plc

- Sopro-Comeg(Acteon)

- Stryker Corp.

- XION Medical

- Cook Medical

- Optomic Espana

- EndoChoice Holdings

- Omnitech Systems

- Alltion(Wuzhou)

- Shenzhen Shen Da Medical

제7장 시장 기회 및 전망

AJY 25.10.29The global hysteroscope market is valued at USD 323.52 million in 2025 and is forecast to reach USD 445.55 million by 2030, translating into a 6.61% CAGR over the period.

Growth is propelled by broader uptake of minimally invasive gynecologic surgery, widening payer support for office-based care, and rapid product innovation that blends advanced optics with rigorous infection-control protocols. Single-use device platforms, cloud-connected imaging, and artificial-intelligence (AI) decision support are reshaping workflows and lowering total procedural costs, giving early adopters measurable clinical and financial advantages. Hospitals still anchor procurement volumes, yet independent gynecology clinics now capture a rising share of elective procedures as reimbursement rules reward outpatient settings. Rigid hysteroscopes remain the platform of choice inside complex surgical theaters, but disposable offerings are driving incremental procedure growth, especially where reprocessing capacity is limited. Competitive intensity is increasing as leading manufacturers pursue acquisitions to secure differentiated technologies and regional footholds.

Global Hysteroscope Market Trends and Insights

Growing Demand for Minimally Invasive Gynecologic Surgery

Clinicians now favor uterine-preserving, incision-free options that shorten recovery and limit complications. Prospective data show vaginal natural orifice transluminal endoscopic hysterectomy can cut median return-to-work from 3 months to 2 months compared with laparoscopy, a finding that resonates with payers evaluating value-based reimbursement. The Mayo Clinic cites hysteroscopic approaches as a first-line solution for intrauterine pathologies because they avoid abdominal incisions and reduce hospital stay. Emerging techniques, including high-intensity focused ultrasound and radiofrequency ablation, are opening new therapy segments for adenomyosis and fibroids. Robotic articulation, AI-enabled targeting, and enhanced visualization further improve precision, positioning operative hysteroscopy to capture share from traditional open or laparoscopic alternatives.

Rapid Adoption of Single-Use Hysteroscopes for Infection Control

Heightened scrutiny of endoscope reprocessing failures is prompting facilities to reevaluate the risk-benefit equation of reusable devices. FDA safety communications underscore contamination hazards, especially in low-volume centers where reprocessing validation is cost-prohibitive. ACOG notes the absence of definitive cost-effectiveness research but warns that surface defects and improper decontamination raise failure rates. Manufacturers such as Minerva Surgical have responded with fully disposable platforms that remove the reprocessing step while offering optics comparable to reusable scopes. If future Medicare payment adjustments cover higher per-procedure consumable costs, adoption curves could steepen quickly across ambulatory sites.

Infection Risk from Reusable Hysteroscopes

Complex device geometries challenge sterile-processing teams, and misalignment between manufacturer instructions and facility resources drives reprocessing errors. ANSI/AAMI ST108 water-quality guidelines raise infrastructure costs, while litigation fear over contamination events pushes administrators toward disposable options. NYU Langone Health reduced defects by deploying dedicated cross-functional teams, yet the resource burden is substantial, underscoring why smaller sites embrace single-use scopes despite higher unit costs.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Optics & Miniaturization

- Integration of AI-Guided Imaging & Cloud Analytics

- Sustainability Concerns Around Disposable Devices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Rigid scopes held 45.35% of 2024 revenue, reflecting proven optical clarity and maneuverability during complex intrauterine surgery. The hysteroscope market size for rigid platforms reached USD 147.0 million in 2024, supported by high capital utilization rates inside tertiary centers. In contrast, single-use scopes recorded the highest growth trajectory at 15.25% CAGR, gaining rapid traction where reprocessing capacity is limited and liability insurance premiums are rising. Greater comfort for patients in office settings, coupled with reduced turnaround time between cases, makes disposables attractive for throughput-oriented clinics.

Hybrid solutions that combine a reusable imaging unit with disposable sheaths blur traditional product boundaries and may accelerate adoption by balancing cost and infection-control goals. Meditrina's second-generation platform, cleared by FDA in May 2024, highlights innovation that marries lightweight ergonomics with 4K visualization, narrowing the perceived performance gap between rigid and flexible formats. Flexible scopes remain niche, favored in anatomically difficult cases or where patient tolerance is paramount, yet higher acquisition costs and narrower procedure indications keep share growth moderate.

Diagnostic hysteroscopy represented 62.53% of total 2024 procedures, reflecting its universal role in first-line uterine assessment. Clinicians favor diagnostic scopes for their smaller diameter and simplified workflow, making them ideal for outpatient evaluation without anesthesia. Operative procedures, expanding at 9.85% CAGR, benefit from tissue-removal systems and energy devices that allow polypectomy, myomectomy, and ablation during a single encounter. Evidence from a 2025 cohort study shows cold-knife hysteroscopic separation plus hormonal therapy achieved a 94.07% success rate in severe intrauterine adhesion, outperforming historical standards.

Hospitals and advanced ambulatory centers are investing in integrated imaging stacks and AI-enabled guidance that streamline complex operative workflows. These upgrades increase capital budgets but also elevate reimbursement potential because combined diagnostic-therapeutic sessions reduce overall episode-of-care costs. Growing surgeon proficiency, aided by simulation training and telementoring, is expected to sustain double-digit procedure expansion in operative subsegments across both developed and emerging geographies.

The Hysteroscope Market Report is Segmented by Product (Rigid Hysteroscopes and More), Modality (Diagnostic and Operative), Component (Scope Shaft & Optics, Light Source, and More), Application (Polypectomy, Myomectomy, Endometrial Ablation, and More), End User (Hospitals, Ambulatory Surgical Services, and More) and Geography (North America, Europe, Asia Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 37.63% share in 2024, buoyed by advanced payer models, extensive sub-specialty training, and rapid uptake of AI-enhanced visualization systems. The United States maintains dominant procedure volume, while Canada adopts similar technologies under its publicly funded healthcare scheme. Mexico's growing private hospital sector and medical tourism initiatives attract regional patients seeking minimally invasive care.

Asia-Pacific is the fastest-growing territory at a projected 9.91% CAGR to 2030. Rising disposable income, expanded insurance coverage, and high gynecological disease burden underpin demand. A systematic 2025 analysis forecasts persistent growth in cervical and uterine cancers, particularly across South Asia, intensifying screening and operative requirements. China and Japan invest heavily in domestic device production, shortening supply chains and supporting local installations, whereas India's new marketing code underscores regulatory maturation that should accelerate market entry for global suppliers.

Europe maintains stable growth amid stringent safety and environmental regulations that influence global manufacturing standards. The region's push toward life-cycle transparency encourages design innovation around recyclable components. Meanwhile, Middle East & Africa and Latin America see incremental adoption led by private hospitals and fertility centers in urban hubs, though workforce shortages and uneven reimbursement slow broader penetration. Targeted training collaborations and cloud-enabled remote mentoring are expected to narrow the capability gap over the forecast horizon.

- B. Braun

- Boston Scientific

- The Cooper Companies

- Gynesonics

- Hologic

- Karl Storz

- LiNA Medical

- MedGyn Products

- Medtronic

- Olympus

- Richard Wolf

- Smiths Group

- Sopro-Comeg (Acteon)

- Stryker

- XION Medical

- Cook Group

- Optomic Espana

- EndoChoice Holdings

- Omnitech Systems

- Alltion (Wuzhou)

- Shenzhen Shen Da Medical

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increase In Incidence Of Uterine Diseases & Abnormalities

- 4.2.2 Growing Demand For Minimally-Invasive Gynecologic Surgery

- 4.2.3 Technological Advances In Optics & Miniaturization

- 4.2.4 Rapid Adoption Of Single-Use Hysteroscopes For Infection Control

- 4.2.5 Shift Toward Office-Based Hysteroscopy Lowering Total Cost Of Care

- 4.2.6 Integration Of AI-Guided Imaging & Cloud Analytics

- 4.3 Market Restraints

- 4.3.1 Infection Risk From Re-Usable Hysteroscopes

- 4.3.2 Shortage Of Trained Hysteroscopists In Emerging Markets

- 4.3.3 Sustainability Concerns Around Disposable Devices

- 4.3.4 Regulatory Scrutiny Of Morcellation & Fluid-Management Events

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Rigid Hysteroscopes

- 5.1.2 Flexible Hysteroscopes

- 5.1.3 Single-use / Disposable Hysteroscopes

- 5.2 By Modality

- 5.2.1 Diagnostic

- 5.2.2 Operative

- 5.3 By Component

- 5.3.1 Scope Shaft & Optics

- 5.3.2 Camera Head / Imaging System

- 5.3.3 Light Source

- 5.3.4 Distension Media & Pumps

- 5.3.5 Accessories & Consumables

- 5.4 By Application

- 5.4.1 Polypectomy

- 5.4.2 Myomectomy

- 5.4.3 Endometrial Ablation

- 5.4.4 Infertility Assessment & Treatment

- 5.4.5 Adhesiolysis / Septum Resection

- 5.4.6 Others

- 5.5 By End User

- 5.5.1 Hospitals

- 5.5.2 Ambulatory Surgical Centers

- 5.5.3 Office-based Gynecology Clinics

- 5.5.4 Fertility Centers

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 B. Braun SE

- 6.3.2 Boston Scientific Corp.

- 6.3.3 CooperSurgical Inc.

- 6.3.4 Gynesonics

- 6.3.5 Hologic Inc.

- 6.3.6 Karl Storz SE & Co. KG

- 6.3.7 LiNA Medical

- 6.3.8 MedGyn Products Inc.

- 6.3.9 Medtronic plc

- 6.3.10 Olympus Corporation

- 6.3.11 Richard Wolf GmbH

- 6.3.12 Smith & Nephew plc

- 6.3.13 Sopro-Comeg (Acteon)

- 6.3.14 Stryker Corp.

- 6.3.15 XION Medical

- 6.3.16 Cook Medical

- 6.3.17 Optomic Espana

- 6.3.18 EndoChoice Holdings

- 6.3.19 Omnitech Systems

- 6.3.20 Alltion (Wuzhou)

- 6.3.21 Shenzhen Shen Da Medical

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment