|

시장보고서

상품코드

1842589

항응고제 역전제 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Anticoagulant Reversal Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

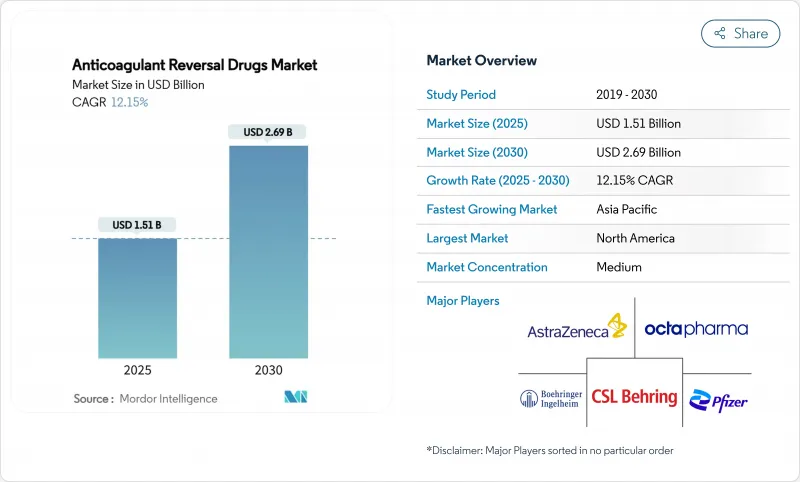

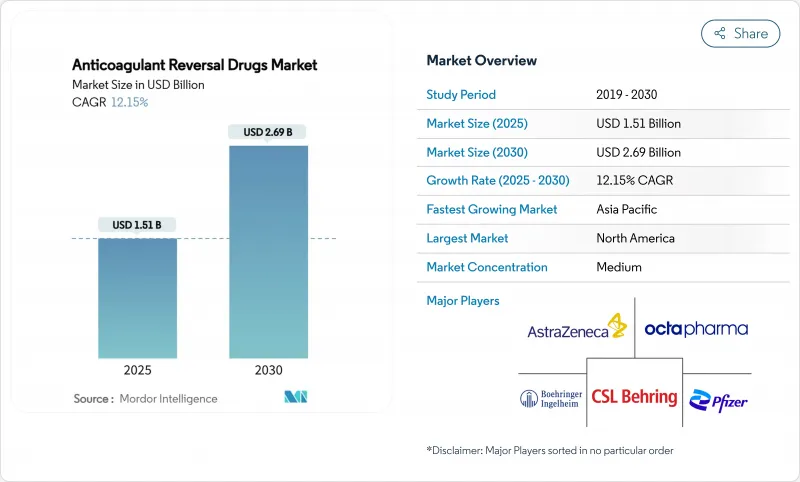

항응고제 역전제 시장 규모는 2025년에 15억 1,000만 달러에 이르고, 2030년에는 26억 9,000만 달러에 달할 것으로 예측되며, CAGR은 12.15%를 나타낼 전망입니다.

성장 배경은 직접 경구 항응고제(DOAC) 채택 확대, 노인 인구 증가, 신규 역전제 시장 출시 시간을 단축하는 규제 당국의 승인을 가속화하는 것입니다. 병원은 DOAC 우선 프로토콜을 확대하고 있으며, 그 결과 신속하고 특이한 역전 솔루션에 대한 수요가 증가하고 있습니다. AI를 활용한 응고 진단의 이용이 증가하고 출혈의 검출이 향상되어 조기 개입으로 이어지는 한편, 혈장 채취의 온쇼어화에 의해 프로트롬빈 농축 제제(PCC)공급 회복력이 강화되고 있습니다. 노바티스가 리버록사반에 비해 출혈을 67% 감소시키는 XI인자 억제제 아베라시맙을 확보함으로써 경쟁 시장의 경쟁이 격화되고 항응고제 역전제 시장의 추가 재위치를 가능하게 하는 차세대 약물로의 변화를 시사하고 있습니다.

세계의 항응고제 역전제 시장 동향과 인사이트

인구 고령화와 혈액 질환 유병률 상승

평균 수명이 증가함에 따라 심방세동의 유병률은 80세 이상으로 9%에 달하고, 항응고제에 대한 만성 노출이 증가하고, 항응고제의 역치료 요구가 높아지고 있습니다. 병원은 현재 노인 특유의 항응고 요법 패스웨이를 도입하고 있으며, 다양한 요법을 반복하는 경우가 많은 노인 환자에게 여러 항응고 요법의 선택을 보장하고 있습니다. 이러한 인구 역학의 변화는 DOAC와 관련된 출혈에 대한 광역 스펙트럼 PCC와 표적 약물을 모두 재고하는 전략적 가치를 높입니다.

미국 FDA/EMA 신속 승인

규제 당국은 전통적인 일정보다 언멧 긴급성을 선호합니다. andexanet alfa는 조기 승인으로 전진했고, MK-2060은 2025년 Fast Track의 지위를 획득하여 일반 개발 기간을 8-12년에서 약 5-7년으로 단축했습니다. 유럽 의약청은 현재 구명을 위한 역전 치료제에 대한 대체 엔드포인트와 실제 임상에서의 증거를 인정하고 있으며, 견고한 데이터 패키지를 가진 기업은 조기 진입의 우위를 획득할 수 있습니다.

신약의 고비용

안덱사넷 알파의 치료비는 1회당 25,000-5만 달러로, PCC에 비해 10-25배의 비싸기 때문에 보험사는 사전 승인의 장애물을 부과하고, 신흥 시장의 병원은 사용을 제한하고 있습니다. 경제모델에서는 ICU 재원일수 단축에 의한 순절약에 대해서는 아직 논의가 있으며, 항제Xa인자 역전제의 유효성이 증명되었음에도 불구하고 채용이 늦어지고 있습니다.

부문 분석

프로트롬빈 복합체 농축 제제는 2024년에 항응고제 역전제 시장 점유율의 39.35%를 차지해 최대 매출을 창출했습니다. 병원은 와파린과 적응 외 DOAC의 긴급 사태에 대응할 수 있는 PCC의 범용성을 높이 평가하고 있으며, 항응고제 역전제 시장에서 안정적인 기준선을 확립하고 있습니다.

2030년까지 연평균 복합 성장률(CAGR)은 14.25%를 나타내며, 가장 급성장하고 있는 것은 안덱사넷 알파 등의 유전자 변형 디코이 단백질입니다. 인자 Xa 억제제를 정확하게 중화하기 때문에 높은 비용이지만 특정 DOAC 역전제의 현대 표준 약물로 자리 잡고 있습니다. 아벨라시맙이 후기 임상시험을 종료하면, 단일클론항체도 유사한 궤적을 따라갈 수 있고, 항응고제 역전제 시장 경쟁 구도를 재조합할 수 있습니다.

생명을 위협하는 출혈은 2024년 항응고제 역전제 시장 규모의 47.53%를 차지했습니다. 이는 두개내 출혈, 위장관 출혈, 외상과 관련된 출혈에 신속한 해독제 접근이 필수적이기 때문입니다. 뇌졸중 센터와 외상 네트워크에서 긴급 의료 담당자는 발병 시간이 짧고 지혈 효과가 입증된 약물을 우선적으로 사용하기 때문에 견조한 이용이 계속되고 있습니다.

선택적 수술의 CAGR은 13.85%로 가장 높지만, 이는 항응고제의 계속이 출혈 위험을 높이는 심장과 신경계의 수술을 계획할 때 예방적 역류 방지가 널리 채용되고 있음을 반영하고 있습니다. 주술기 관리의 프로토콜화는 예측 가능한 수요를 증가시켜, 예정된 치료에 적합한 장시간 작용형 제제의 탐구를 제조업체에 촉구해, 항응고제 역전제 시장에 두께를 가져오고 있습니다.

지역 분석

북미는 2024년 세계 매출의 41.82%를 차지하며 특정 역전제를 지지하는 FDA 지도 프로토콜과 고가격 제품에 대한 강력한 상환에 힘입었습니다. 레벨 1 외상 시스템과 종합적인 뇌졸중 네트워크가 안정적인 소비를 유지하는 반면, 캐나다 보건부가 2024년 온덱시아를 승인함으로써 대륙에 대한 접근이 확대되었습니다.

아시아태평양의 CAGR은 14.51%를 나타내 모든 지역을 초과할 것으로 예측됩니다. 일본의 온덱시아 승인, 중국과 인도의 DOAC 사용량 증가, 도시화 경제권의 심혈관 질환 유병률은 항응고제 역전제 시장을 확대하는 힘이 되고 있습니다. 한국과 같은 국가 데이터베이스는 대출혈의 발생을 강조하고 해독제의 입수를 정책적으로 의무화합니다.

유럽은 EMA 지도와 성숙한 혈장 공급망이 PCC 생산을 지원하고 안정을 유지하고 있습니다. 독일, 영국, 프랑스는 비용 효과적인 지표를 채택하여 제조업체에게 임상적 증거와 경제적 가치 제안을 결합하도록 촉구합니다. 중동 및 아프리카는 현재 차세대 약제의 보급을 제한하고 있는 가격면의 제약에 의해 완화되고 있는 것, 제3차 의료의 생산 능력 증가에 따라, 화이트 스페이스의 가능성을 나타내고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화와 혈액 질환 증가

- 가속하는 미국 FDA/EMA의 패스트트랙 승인

- 병원에 있어서의 DOAC 우선 프로토콜의 채용이 역전제 수요를 촉진

- 조기 역전 개입을 가능하게 하는 AI를 활용한 응고 진단

- 혈장 유래 PCC공급 공급망 국내 생산 전환

- 시장 성장 억제요인

- 신약의 고비용

- 혈전 색전 위험과 블랙박스 경고

- POC(Point-of-Care) 응고 디바이스와의 경쟁에 의한 약제 요구의 저하

- Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 약제 클래스별

- 프로트롬빈 복합체 농축액

- 응고 인자

- 단일클론항체

- 재조합 미끼 단백질

- 피트나디온

- 기타 클래스

- 적응증별

- 생명을 위협하는 출혈

- 응급 수술

- 선택적 수술

- 투여 경로별

- 정맥 내 볼루스/수액

- 피하

- 최종 사용자별

- 병원 약국

- 응급실/외상센터

- 일반 약국

- 외래 수술 센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Alexion Pharmaceuticals Inc.

- CSL Behring

- Pfizer Inc.

- AstraZeneca

- Octapharma AG

- Boehringer Ingelheim

- Fresenius Kabi

- Bausch Health

- Amneal Pharmaceuticals

- Ferring Pharmaceuticals

- Baxter International

- Johnson & Johnson(Ethicon)

- Perosphere Pharma

- Nichi-Iko Pharma

- Grifols SA

- Sanquin Blood Supply Foundation

- Octava Pharma USA(Balfaxar)

제7장 시장 기회와 전망

KTH 25.10.29The anticoagulant reversal drugs market size reached USD 1.51 billion in 2025 and is forecast to attain USD 2.69 billion by 2030, advancing at a 12.15% CAGR.

Growth stems from greater adoption of direct oral anticoagulants (DOACs), an expanding elderly population, and faster regulatory approvals that shorten time-to-market for new reversal agents. Hospitals are widening DOAC-first protocols, which in turn heighten demand for rapid, specific reversal solutions. Rising use of AI-driven coagulation diagnostics is improving bleed detection and guiding earlier intervention, while on-shored plasma collection strengthens prothrombin complex concentrate (PCC) supply resilience. Competitive momentum intensified after Novartis secured abelacimab, a Factor XI inhibitor linked to 67% bleeding reduction compared with rivaroxaban, signalling a shift toward next-generation agents that could further reposition the anticoagulant reversal drugs market.

Global Anticoagulant Reversal Drugs Market Trends and Insights

Aging Population & Rising Prevalence of Blood-Borne Disorders

Growing life expectancy pushes atrial fibrillation prevalence to 9% among those over 80 years, increasing chronic exposure to anticoagulants and heightening reversal needs. Hospitals now embed geriatric-specific anticoagulation pathways that guarantee availability of multiple reversal options for elderly patients who often cycle through varied regimens. This demographic shift elevates the strategic value of stocking both broad-spectrum PCCs and targeted agents for DOAC-associated bleeds.

Accelerated US FDA/EMA Fast-Track Approvals

Regulators prioritize unmet urgency over traditional timelines; andexanet alfa advanced under accelerated approval, while MK-2060 gained Fast Track status in 2025, cutting typical development windows from 8-12 years to roughly 5-7 years. The European Medicines Agency now accepts surrogate endpoints and real-world evidence for life-saving reversal therapies, allowing firms with robust data packages to capture early-mover advantage.

High Cost of Novel Agents

Andexanet alfa costs USD 25,000-50,000 per treatment, a 10-25 fold premium over PCCs, prompting insurers to impose prior-authorization hurdles and emerging-market hospitals to restrict use. Economic models still debate net savings relative to reduced ICU stays, slowing adoption despite proven anti-Factor Xa reversal efficacy.

Other drivers and restraints analyzed in the detailed report include:

- Hospital Adoption of DOAC-First Protocols Driving Demand for Reversal Agents

- AI-Driven Coagulation Diagnostics Enabling Earlier Reversal Intervention

- Thrombo-Embolic Risk & Black-Box Warnings

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Prothrombin complex concentrates generated the largest revenue in 2024, holding 39.35% of anticoagulant reversal drugs market share, buoyed by decades of clinical familiarity and recent approval of Balfaxar that ensures diversified domestic supply. Hospitals value PCC versatility across warfarin and certain off-label DOAC emergencies, cementing a stable baseline within the anticoagulant reversal drugs market.

Recombinant decoy proteins such as andexanet alfa headline the fastest-growing cohort with a projected 14.25% CAGR through 2030. Their precise neutralization of Factor Xa inhibitors positions them as the contemporary standard for specific DOAC reversal, albeit at a high cost. Monoclonal antibodies could follow a similar trajectory once abelacimab concludes late-stage trials, potentially reshaping competitive hierarchies inside the anticoagulant reversal drugs market.

Life-threatening hemorrhage accounted for 47.53% of the anticoagulant reversal drugs market size in 2024, as rapid antidote access remains vital for intracranial, gastrointestinal, and trauma-related bleeds. Emergency clinicians prioritize agents with short onset and proven hemostatic efficacy, sustaining robust utilization across stroke centers and trauma networks.

Elective surgery posts the highest 13.85% CAGR, reflecting wider adoption of prophylactic reversal in planned cardiac or neurological procedures where anticoagulant continuation elevates bleed risk. Protocolized peri-operative management increases predictable demand and encourages manufacturers to explore longer-acting formulations suitable for scheduled care, thereby adding depth to the anticoagulant reversal drugs market.

The Anticoagulant Reversal Drugs Market Report is Segmented by Drug Class (Prothrombin Complex Concentrates, Coagulation Factors, Phytonadione, and More), Indication (Life-Threatening Bleeding, and More), Route of Administration (Intravenous Bolus/Infusion, and Sub-Cutaneous), End User (Hospital Pharmacies, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 41.82% of global revenue in 2024, supported by FDA-guided protocols that favor specific reversal agents and strong reimbursement for premium-priced products. Level 1 trauma systems and comprehensive stroke networks uphold steady consumption, while Health Canada's 2024 clearance of Ondexxya widened continental access.

Asia-Pacific is projected to outpace all regions at 14.51% CAGR. Japan's approval of Ondexxya, rising DOAC usage in China and India, and cardiovascular disease prevalence across urbanizing economies are converging forces expanding the anticoagulant reversal drugs market. National databases such as South Korea's highlight major bleeding incidence that reinforces policy mandates for antidote availability.

Europe remains stable with coordinated EMA guidance and mature plasma supply chains backing PCC production. Germany, the United Kingdom, and France adopt cost-effectiveness metrics, compelling manufacturers to pair clinical evidence with economic value propositions. Middle East & Africa trail but represent white-space potential as tertiary-care capacity grows, albeit tempered by pricing constraints that currently limit widespread penetration of next-generation agents.

- Alexion Pharmaceuticals Inc.

- CSL Behring

- Pfizer

- AstraZeneca

- Octapharma

- Boehringer Ingelheim

- Fresenius

- Bausch Health

- Amneal Pharmaceuticals

- Ferring Pharmaceuticals

- Baxter

- Johnson & Johnson

- Perosphere Pharma

- Nichi-Iko Pharma

- Grifols

- Sanquin Blood Supply Foundation

- Octava Pharma USA (Balfaxar)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging Population & Rising Prevalence Of Blood-Borne Disorders

- 4.2.2 Accelerated US FDA/EMA Fast-Track Approvals

- 4.2.3 Hospital Adoption Of DOAC-First Protocols Driving Demand For Reversal Agents

- 4.2.4 AI-Driven Coagulation Diagnostics Enabling Earlier Reversal Intervention

- 4.2.5 Supply-Chain On-Shoring Of Plasma-Derived Pccs

- 4.3 Market Restraints

- 4.3.1 High Cost Of Novel Agents

- 4.3.2 Thrombo-Embolic Risk & Black-Box Warnings

- 4.3.3 Competition From Point-Of-Care Coagulation Devices Reducing Drug Need

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Prothrombin Complex Concentrates

- 5.1.2 Coagulation Factors

- 5.1.3 Monoclonal Antibodies

- 5.1.4 Recombinant Decoy Proteins

- 5.1.5 Phytonadione

- 5.1.6 Other Classes

- 5.2 By Indication

- 5.2.1 Life-threatening Bleeding

- 5.2.2 Emergency Surgery

- 5.2.3 Elective Surgery

- 5.3 By Route of Administration

- 5.3.1 Intravenous Bolus/Infusion

- 5.3.2 Sub-cutaneous

- 5.4 By End User

- 5.4.1 Hospital Pharmacies

- 5.4.2 Emergency Departments/Trauma Centers

- 5.4.3 Retail Pharmacies

- 5.4.4 Ambulatory Surgery Centers

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alexion Pharmaceuticals Inc.

- 6.3.2 CSL Behring

- 6.3.3 Pfizer Inc.

- 6.3.4 AstraZeneca

- 6.3.5 Octapharma AG

- 6.3.6 Boehringer Ingelheim

- 6.3.7 Fresenius Kabi

- 6.3.8 Bausch Health

- 6.3.9 Amneal Pharmaceuticals

- 6.3.10 Ferring Pharmaceuticals

- 6.3.11 Baxter International

- 6.3.12 Johnson & Johnson (Ethicon)

- 6.3.13 Perosphere Pharma

- 6.3.14 Nichi-Iko Pharma

- 6.3.15 Grifols S.A.

- 6.3.16 Sanquin Blood Supply Foundation

- 6.3.17 Octava Pharma USA (Balfaxar)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment