|

시장보고서

상품코드

1842591

무균 샘플링 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Aseptic Sampling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

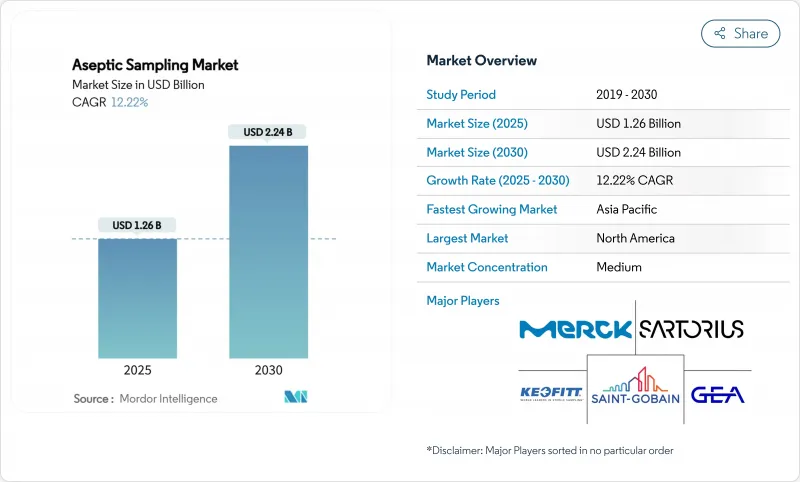

무균 샘플링 시장은 2025년에 12억 6,000만 달러, 2030년에는 22억 4,000만 달러에 달하며, CAGR 12.22%를 나타낼 전망입니다.

오염 없는 바이오프로세스에 대한 급속한 투자, 무균 규제 강화, 단일 사용 어셈블리의 광범위한 채택이 이러한 확대를 지원합니다. 제약 제조업체는 자동화된 장치를 인간 오류에 대한 신뢰할 수 있는 가드 레일로 간주하고 있는 반면, 세포 치료 및 유전자 치료 파이프라인은 개발 초기에 무균 관리를 강요하고 있습니다. 디지털 공정 분석 기술(PAT)은 현재 샘플링 하드웨어와 결합하여 수백만 달러 규모의 생물학적 제형 배치를 보호하는 실시간 품질 데이터를 제공합니다. 지역적으로는 북미 업체들이 성숙한 인프라와 FDA의 감독으로 리더십을 지키고 있지만, 아시아태평양 시설은 국가 우대 조치와 낮은 운영 비용을 배경으로 보다 빠르게 생산 능력을 강화하고 있습니다. 통합 솔루션 제공업체가 하드웨어, 분석 및 데이터 관리를 통합 플랫폼에 통합하고 검증 타임라인을 단축함에 따라 경쟁이 치열해지고 있습니다.

세계의 무균 샘플링 시장 동향과 인사이트

무균성 보증을 위한 엄격한 정부 규정

세계의 규제 당국은 현재 무균 제조에서의 샘플링 빈도와 추적성의 엄격화를 요구하고 있습니다. 개정된 FDA 지침은 첨단 치료 의약품에도 적용되며 문서화된 검증을 통해 일상적인 환경 모니터링을 의무화하고 있습니다. 동등한 EU GMP Annex 1의 개정은 지역 간의 기대를 일치시키고 제조업체가 종이 로그에서 전자 감사 추적 및 모든 개입을 기록하는 자동화 장비로 대체하도록 촉구합니다. 이 압력은 레거시 공장 업그레이드를 가속화하고 오염 위험을 최소화하기 위해 Greenfield 사이트에서 폐쇄, 단일 사용 경로를 규정합니다.

세포 및 유전자 치료 파이프라인의 신속한 스케일 업

자가 및 동종 요법의 상업화는 각 환자 배치가 교차 오염의 허용 범위를 0으로 만들기 때문에 무균 약점을 나타냅니다. 따라서 생산자는 CoC 문서화를 보장하고 다양한 바이러스 벡터 및 세포 유형을 지원하는 자동화된 폐쇄 샘플링을 지정합니다. 2030년까지 승인 예정인 치료법이 3,000개에 달함에 따라, 생산 능력 확장을 위해서는 긴 검증 주기 없이 다중 제품 생산 라인에 바로 적용 가능한 모듈식 스키드가 요구됩니다.

고분자 어셈블리에서 용출물 및 추출물의 위험

일회용 매니폴드는 유기산, 가소제 및 미량 금속을 방출할 수 있으며, 이들은 민감한 생물학적 제제를 불안정하게 하므로 철저한 화학적 프로파일링이 필요합니다. 기업은 종종 여러 온도와 용매로 몇 주간의 추출물 테스트를 실시하여 비용 증가와 제품 시행 일정 지연을 초래합니다. 세계적으로 통일된 시험 표준이 없는 것도 분석 작업의 부담을 늘리고 있습니다.

부문 분석

2024년 무균 샘플링 시장에서 수동 시스템은 72.35%의 점유율을 차지했습니다. 저자본 지출과 입증된 컴플라이언스 기록은 특히 인프라 변경이 가동 중지 시간을 초래하는 레거시 공장에서 광범위한 사용을 유지하고 있습니다. 그러나 자동화 모듈은 생산자가 운영자의 부담 완화와 데이터 무결성 강화를 목표로 하기 때문에 CAGR은 가장 빠른 18.25%를 나타낼 전망입니다. 자동화된 스키드는 제조 실행 시스템과 통합되어 모든 잡아를 기록하고 감사 검토를 위해 결과를 즉시 보관합니다. 이 기능에 의해 서류 작성의 피로가 경감되어 FDA 사찰시의 신뢰성이 높아집니다. 세포 치료에서 배치 값의 상승은 사람의 개입을 완전히 제거하는 솔루션에 대한 수요를 날카롭게 하고 무균 샘플링 시장에서 자동화에 대한 장기적인 기울기를 강화하고 있습니다.

수동 키트는 예산이 처리량을 능가하는 초기 연구 개발 또는 소량의 생물학적 제제와 같은 틈새 시장을 여전히 차지합니다. 공급업체는 현재 수동 트리거를 수락하면서 사용 간 멸균을 자동화하는 하이브리드 플랫폼을 배치하고 있습니다. 이 브리지 전략은 가격에 민감한 구매자가 기존 프로토콜을 버리지 않고 서서히 마이그레이션하는 데 도움이 됩니다. 예측기간 중 전자기록규격의 하모나이제이션이 진행되어 무균 샘플링 시장의 상업생산라인의 디폴트가 자동화 기기로 결정적으로 변화해 나갈 것으로 보입니다.

온라인 기기는 실시간 피드백으로 2024년 세계 수익의 46.53%를 차지했습니다. 이 장치는 밀폐 조건 하에서 연속적으로 마이크로 분취 량을 채취하여 pH와 영양분을 즉시 조정할 수 있습니다. CAGR이 13.85%를 나타내는 앳라인 장치는 완벽하게 통합된 온라인 루프와 같은 복잡한 엔지니어링을 필요로 하지 않으며 빈번한 분석을 원하는 운영자를 끌어들입니다. 앳라인 프로브는 용기에 인접하여 설치되기 때문에 튜브의 길이가 짧아져 센서의 교환이 신속하게 이루어집니다. 이것은 막힘의 위험을 줄이고 교정을 단순화합니다.

소형화할 수 없는 바이러스 클리어런스 분석과 같은 고급 분석에는 오프라인 잡기가 필수적입니다. 그러나 모든 오프라인 전송은 개방적 인 취급과 함께 턴 어라운드를 장기화하고 편차의 위험을 수반합니다. PAT 가이드라인과 실시간 릴리스 테스트가 성숙함에 따라 앳라인 장치는 오프라인 워크플로우에서 점진적으로 점유율을 빼앗아갈 것으로 보입니다. 표준화된 기계적 인터페이스와 일회용 유로는 현재 무균 샘플링 시장의 중견 공장에서의 채택을 강화하고 개조를 용이하게합니다.

지역 분석

북미는 2024년에 41.82%의 매출을 획득해 깊은 바이오 의약품 파이프라인, FDA 지침의 벤치마크, CDMO의 밀집에 의해 리드를 지켰습니다. 미국은 대부분의 상업 세포 치료 시설을 보유하고 있으며 PAT에 많은 투자를 하고 있습니다. 캐나다는 연방 정부의 보조금을 통해 바이오시밀러 의약품 생산 능력을 강화하고 멕시코는 비용 효율적인 노동력으로 제네릭 의약품 생산에 박차를 가하고 있습니다. 첨단 무균성을 요구하는 첫 번째 클래스의 생물학적 제형을 지원하는 벤처 캐피탈은 수요를 더욱 높입니다.

아시아태평양은 정부가 생산 능력을 조성하고 품질 향상을 강제하고 있기 때문에 CAGR이 13.61%를 나타낼 전망입니다. 한국의 SK Pharmteco는 폐쇄 샘플러를 갖춘 펩티드 합성 라인에 2억 6,000만 달러를 투입했습니다. 중국의 국산화 정책은 국내 공급의 안정을 추구하고 처음부터 일회용 샘플링을 표준화하는 새로운 생물 제제 공원에 박차를 가하고 있습니다. 인도는 비용에 민감한 공장이 수동 키트와 일회용 키트를 혼합하는 원료 강국임에 변함이 없습니다. 이러한 프로그램을 종합하면, 무균 샘플링 시장은 이 지역에 깊이 들어가 세계 벤더의 현지 제조 거점을 확립하게 됩니다.

유럽은 독일의 엔지니어링 클러스터와 프랑스 생물 제제의 확장에 힘입어 안정을 유지하고 있습니다. 브렉짓 후 영국 시설은 자동 샘플링 로거의 개수를 추진하고 갱신된 부속서 1에 맞춥니다. 지속가능성 규제는 금속과 플라스틱의 하이브리드 매니폴드를 검토하고 라이프사이클에 미치는 영향을 문서화하기 위해 제조업체에 압력을 가하고 있습니다. 이탈리아와 스페인의 백신 제조업체도 마찬가지로 유행 대책 보조금을 확보하기 위해 시설을 업그레이드하고 있습니다. 이러한 투자는 극적이지 않더라도 안정적인 성장을 가져오고이 지역을 무균 샘플링 시장의 혁신 허브로 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 무균성 보증을 위한 엄격한 정부 규제

- 세포 및 유전자 치료 파이프라인의 급속한 스케일 업

- 클로즈드 루프, 일회용 바이오프로세싱으로의 변화

- 인라인, 앳라인 PAT의 채용에 의한 배치 수율의 향상

- AI에 의한 오염 예측 플랫폼

- 시장 성장 억제요인

- 폴리머 어셈블리의 용출물·추출물 위험

- 자동 무균 샘플링 스키드가 높은 CAPEX

- 다용도 커넥터의 복잡한 밸리데이션

- Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 샘플링 유형별

- 수동 무균 샘플링

- 백

- 병

- 기타 용기

- 자동 무균 샘플링

- 수동 무균 샘플링

- 샘플링 기법별

- 온라인 샘플링

- 앳라인 샘플링

- 오프라인 샘플링

- 용도별

- 업스트림 공정

- 다운스트림 공정

- 최종 사용자별

- 생명공학 및 제약 제조업체

- 계약 연구 및 제조 기관

- 학술 및 연구 기관

- 구성 요소 재료별

- 일회용 어셈블리

- 재사용 가능(스테인레스 스틸 기반) 시스템

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Merck KGaA

- Sartorius AG

- Thermo Fisher Scientific

- Danaher Corp(Pall & Cytiva)

- Lonza Group

- Keofitt A/S

- Saint-Gobain Life Sciences

- GEA Group

- Gemu Group

- Qualitru Sampling Systems

- WL Gore & Associates

- Avantor(VWR)

- Repligen Corp

- Solventum Corporation

- Parker Hannifin(domnick hunter)

- Colder Products Company(CPC)

- Mettler-Toledo

- PendoTECH

- Bbi-Biotech GmbH

- Advanced Microdevices Pvt Ltd

제7장 시장 기회와 전망

KTH 25.10.29The aseptic sampling market stands at USD 1.26 billion in 2025 and is on track to reach USD 2.24 billion by 2030, advancing at a 12.22% CAGR.

Rapid investment in contamination-free bioprocessing, tighter sterility regulations, and wider adoption of single-use assemblies underpin this expansion. Pharmaceutical producers see automated devices as a reliable guardrail against human error, while growing cell and gene therapy pipelines force sterility controls earlier in development. Digital process analytical technology (PAT) now pairs with sampling hardware to deliver real-time quality data that protects multimillion-dollar biologic batches. Regionally, North American manufacturers defend leadership through mature infrastructure and FDA oversight, yet Asia-Pacific facilities add capacity faster on the back of state incentives and lower operating costs. Competition intensifies as integrated solution providers couple hardware, analytics, and data management into unified platforms that shorten validation timelines.

Global Aseptic Sampling Market Trends and Insights

Stringent Government Regulations For Sterility Assurance

Global regulators now require tighter sampling frequency and traceability in aseptic production. The revised FDA guidance extends to advanced therapy medicinal products and mandates routine environmental monitoring with documented validation. Equivalent EU GMP Annex 1 revisions align expectations across regions, prompting manufacturers to replace paper logs with electronic audit trails and automated devices that record every intervention. This pressure accelerates upgrades in legacy plants and prescribes closed, single-use pathways in greenfield sites to minimize contamination risks.

Rapid Scale-Up Of Cell & Gene Therapy Pipelines

Commercialization of autologous and allogeneic therapies exposes sterility weak points, as each patient batch carries zero tolerance for cross-contamination. Producers therefore specify automated, closed sampling that secures chain-of-custody documentation and supports diverse viral vectors and cell types. As approvals approach 3,000 therapies by 2030, capacity build-outs demand modular skids that drop into multiproduct suites without lengthy validation cycles.

Leachables & Extractables Risk In Polymeric Assemblies

Disposable manifolds can release organic acids, plasticizers, or trace metals that destabilize sensitive biologics, requiring exhaustive chemical profiling. Firms often run multi-week extractables studies at several temperatures and solvents, adding cost and delaying product launch schedules. The absence of harmonized global test standards also multiplies analytical workloads.

Other drivers and restraints analyzed in the detailed report include:

- Shift Toward Closed-Loop, Single-Use Bioprocessing

- In-Line, At-Line PAT Adoption Improving Batch Yields

- High CAPEX Of Automated Aseptic Sampling Skids

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Manual systems commanded a 72.35% share of the aseptic sampling market in 2024. Their low capital outlay and proven compliance records maintain widespread usage, especially in legacy plants where infrastructure changes invite downtime. However, automated modules exhibit the fastest 18.25% CAGR as producers target lower operator exposure and stronger data integrity. Automated skids integrate with manufacturing execution systems to log every grab and immediately archive results for audit review. That capability relieves documentation fatigue and elevates confidence during FDA inspections. Rising batch values in cellular therapies sharpen demand for solutions that remove human interventions entirely, reinforcing the long-term tilt toward automation in the aseptic sampling market.

Manual kits still occupy niches such as early R&D or low-volume biologics where budget trumps throughput. Vendors now position hybrid platforms that accept manual triggers yet automate sterilization between uses. This bridge strategy helps price-sensitive buyers migrate gradually without scrapping existing protocols. Over the forecast window, wider harmonization of electronic records standards is set to catalyze a decisive inflection toward automated devices as the default for commercial production lines within the aseptic sampling market.

On-line instruments represented 46.53% of global revenue in 2024 due to their real-time feedback. They continuously pull micro-aliquots under closed conditions, enabling immediate pH or nutrient adjustments. At-line devices, posting the brisk 13.85% CAGR, attract operators who want frequent analytics without the engineering complexity of fully integrated on-line loops. At-line probes station adjacent to the vessel, keep tubing lengths short, and permit rapid sensor swaps. This reduces risk of clogging and simplifies calibrations.

Off-line grabs persist for advanced analytics such as viral clearance assays that cannot be miniaturized. Yet every off-line transfer involves open handling, elongates turnaround, and risks deviations. As PAT guidelines and real-time release testing mature, at-line units will likely siphon incremental share from off-line workflows. Standardized mechanical interfaces and disposable flow paths now make retrofits easier, bolstering adoption across mid-tier plants in the aseptic sampling market.

The Aseptic Sampling Market Report is Segmented by Type of Sampling (Manual Aseptic Sampling and Automated Aseptic Sampling), Sampling Technique (On-Line Sampling and More), Application (Upstream Process and Downstream Process), End-User (Biotechnology and Pharmaceutical Manufacturers and More), Component Material (Single-Use Assemblies and Reusable Systems), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 41.82% revenue in 2024 and defends its lead through deep biopharmaceutical pipelines, benchmarking FDA guidance, and a density of CDMOs. The United States hosts most commercial cell therapy facilities and invests heavily in PAT. Canada builds biosimilar capacity under targeted federal grants, while Mexico's cost-effective labor spurs generic drug output. Demand rises further due to venture capital backing first-in-class biologics that demand heightened sterility.

Asia-Pacific records the strongest 13.61% CAGR as governments subsidize capacity and enforce quality uplift. South Korea's SK Pharmteco placed USD 260 million into peptide synthesis lines equipped with closed samplers. China's localization policies call for domestic supply security, fueling new biologics parks that standardize single-use sampling from the outset. India remains a powerhouse for active pharmaceutical ingredients, where cost-sensitive plants mix manual and disposable kits. Collectively, these programs push the aseptic sampling market deeper into the region and establish local manufacturing bases for global vendors.

Europe remains stable, anchored by Germany's engineering clusters and France's biologics expansions. Post-Brexit United Kingdom facilities align with updated Annex 1, driving retrofits of automated sampling loggers. Sustainability regulations pressure producers to explore hybrid metal-plastic manifolds and to document lifecycle impacts. Italian and Spanish vaccine manufacturers similarly upgrade equipment to secure pandemic preparedness grants. These investments deliver steady, if less dramatic, growth that keeps the region an innovation hub for the aseptic sampling market.

- Merck

- Sartorius

- Thermo Fisher Scientific

- Danaher Corp (Pall & Cytiva)

- Lonza Group

- Keofitt

- Saint-Gobain Life Sciences

- GEA Group

- Gemu Group

- Qualitru Sampling Systems

- W. L. Gore & Associates

- Avantor (VWR)

- Repligen Corp

- Solventum Corporation

- Parker Hannifin (domnick hunter)

- Colder Products Company (CPC)

- Mettler-Toledo

- PendoTECH

- Bbi-Biotech GmbH

- Advanced Microdevices Pvt Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent Government Regulations For Sterility Assurance

- 4.2.2 Rapid Scale-Up Of Cell & Gene Therapy Pipelines

- 4.2.3 Shift Toward Closed-Loop, Single-Use Bioprocessing

- 4.2.4 In-Line, At-Line PAT Adoption Improving Batch Yields

- 4.2.5 AI-Driven Contamination Prediction Platforms

- 4.3 Market Restraints

- 4.3.1 Leachables & Extractables Risk In Polymeric Assemblies

- 4.3.2 High CAPEX Of Automated Aseptic Sampling Skids

- 4.3.3 Complex Validation For Multi-Use Connectors

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Type of Sampling

- 5.1.1 Manual Aseptic Sampling

- 5.1.1.1 Bags

- 5.1.1.2 Bottles

- 5.1.1.3 Other Containers

- 5.1.2 Automated Aseptic Sampling

- 5.1.1 Manual Aseptic Sampling

- 5.2 By Sampling Technique

- 5.2.1 On-line Sampling

- 5.2.2 At-line Sampling

- 5.2.3 Off-line Sampling

- 5.3 By Application

- 5.3.1 Upstream Process

- 5.3.2 Downstream Process

- 5.4 By End-User

- 5.4.1 Biotechnology & Pharmaceutical Manufacturers

- 5.4.2 Contract Research & Manufacturing Organizations

- 5.4.3 Academic & Research Institutes

- 5.5 By Component Material

- 5.5.1 Single-Use Assemblies

- 5.5.2 Reusable (Stainless-Steel-Based) Systems

- 5.6 Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 Middle East and Africa

- 5.6.4.1 GCC

- 5.6.4.2 South Africa

- 5.6.4.3 Rest of Middle East and Africa

- 5.6.5 South America

- 5.6.5.1 Brazil

- 5.6.5.2 Argentina

- 5.6.5.3 Rest of South America

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Merck KGaA

- 6.3.2 Sartorius AG

- 6.3.3 Thermo Fisher Scientific

- 6.3.4 Danaher Corp (Pall & Cytiva)

- 6.3.5 Lonza Group

- 6.3.6 Keofitt A/S

- 6.3.7 Saint-Gobain Life Sciences

- 6.3.8 GEA Group

- 6.3.9 Gemu Group

- 6.3.10 Qualitru Sampling Systems

- 6.3.11 W. L. Gore & Associates

- 6.3.12 Avantor (VWR)

- 6.3.13 Repligen Corp

- 6.3.14 Solventum Corporation

- 6.3.15 Parker Hannifin (domnick hunter)

- 6.3.16 Colder Products Company (CPC)

- 6.3.17 Mettler-Toledo

- 6.3.18 PendoTECH

- 6.3.19 Bbi-Biotech GmbH

- 6.3.20 Advanced Microdevices Pvt Ltd

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment