|

시장보고서

상품코드

1842603

치과용 주사기 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2025-2030년)Dental Syringes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

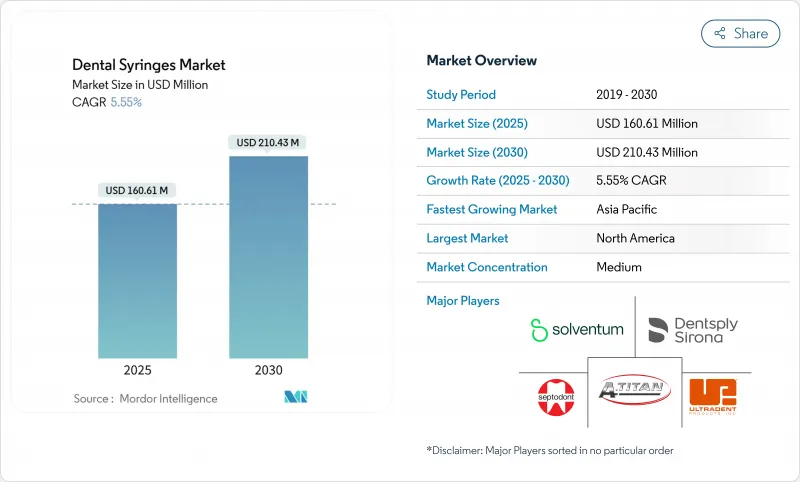

치과용 주사기 시장은 2025년에 1억 6,061만 달러가 되고, 2030년에는 2억 1,043만 달러에 이를 것으로 예측되며, CAGR은 5.55%를 나타낼 전망입니다.

이 성장은 감염 관리 요건의 강화, 보철 치료가 필요한 노인 인구 증가, 컴퓨터 제어의 국소 마취제 공급 시스템의 꾸준한 보급을 반영합니다. 최근 세계적인 보건 보건 사건 이후 의식이 높아짐에 따라 치과의사는 CDC 멸균 규칙 준수를 단순화하는 단일 사용 및 RFID 추적 장치로 전환하고 있습니다. 보험사도 수요에 영향을 주고 있습니다. 2024년에는 미국 성인의 65%가 치과보험에 가입했으며, 91%가 치과검진을 필수 예방케어로 간주했습니다. 공급면에서는 EU의 포장 및 포장 폐기물 규제에 대응하기 위해 제조업체는 생분해성 플라스틱과 경량 금속을 중심으로 제품을 재설계하고 있습니다. 2025년 4월에 도입된 관세와 불안정한 스테인레스 스틸 공급망은 치과 진료소에 조달 대상을 다변화하고 그룹 구매를 가속화합니다.

세계의 치과용 주사기 시장 동향과 인사이트

고령화로 보철업무 확대

60세 이상의 성인은 이미 10억 명에 달했으며 2030년에는 14억 명을 돌파할 전망입니다. 이 연령층을 차지하는 보철 치료는 정확한 마취제의 투여가 요구되기 때문에 클리닉은 컴퓨터 제어의 국소 마취 장치 등 첨단 치과용 주사기 시장의 솔루션을 도입하는 경향이 있습니다. 말레이시아에서는 25-54세의 성인이 최대 환자 그룹을 형성하고 의자 용량을 더욱 압박하고 있습니다. 치과보험사는 구강과 전신건강과의 관련성을 강조하고, 예방적인 진찰을 촉진하고, 고급 주사기 수요를 강화하고 있습니다. 그 결과, 진료소에서는 사용자가 피로하지 않고 복수회의 주사를 실시할 수 있는 인간공학에 근거한 설계가 선호되고 있습니다. 풀 아치 수리가 증가함에 따라 높은 배럴 투명도와 제어 된 흡입력을 특징으로하는 주사기 디자인이 표준이되고 있습니다.

우식과 치주병 증가

세계 2억 8,000만 명 이상의 노인들이 치료되지 않은 우식과 치주병에 직면해 있습니다. 업데이트된 CDC 가이드라인에서 카트리지 주사기는 환자와 환자 사이에서 멸균되어야 하며, 주사 바늘과 마취제 카트리지는 단일 사용으로 유지되어야 한다고 규정되어 있습니다. 신흥경제국에서는 당분이 많은 식사나 한정된 예방조치에 의해 압식의 발생이 빨라지고 있어 비용효과가 뛰어나고 적합성이 높은 주사기가 요구되고 있습니다. 텔레덴티스트리는 젊은 성인의 조기 진단을 가능하게 하고, 국소 마취를 필요로 하는 저침습 수리 기회가 증가하고 있습니다. Curodont Repair Fluoride Plus와 같은 제품에 의해 제공되는 드릴을 사용하지 않는 충치 수리와 같은 초기 단계의 개입은 의자 시간을 단축하지만 복잡한 경우는 안전한 침착을 확인하는 흡입 장치에 따라 계속됩니다.

저소득 지역에서 숙련된 치과 의사의 부족

많은 신흥국에서는 인구 1만 명당 치과 의사 수가 1명 미만입니다. WHO는 지리적, 경제적 장벽이 노인의 적시 치료를 방해한다고 지적합니다. 제한된 교육 능력으로 인해 흡입 및 유량 설정에 대한 지침이 필요한 고급 컴퓨터 제어 장비의 도입이 지연됩니다. 각국 정부는 이동 진료소에 자금을 제공함으로써 대응하고 있지만, 기본적인 기구에의 지출에 중점을 두고 있습니다. 한편, 주사기 제조업체는 치과용 주사기 업계에서 가혹한 재처리를 견디고 적은 운영 예산에 부합하는 단순화된 금속 형식을 공급하고 있습니다.

부문 분석

재사용 가능한 장비는 확립된 오토클레이브 인프라의 혜택을 받아 2024년 58.91%의 매출을 유지했습니다. 같은 해, 일회용 기구는 급속하게 성장하여 일회용 치과용 주사기 시장 규모는 CAGR 6.61%를 나타낼 전망입니다. 1일 주사 횟수가 30회를 넘는 환자를 안고 있는 진료소에서는 멸균기의 병목이 지적되고 있어, 턴어라운드 타임을 단축할 수 있는 색으로 구분된 일회용 배럴이 선호되고 있습니다.

EU 프레임워크는 2030년까지 재활용 가능한 포장을 의무화하고 있기 때문에 공급업체는 퇴비화 가능성 목표를 충족하는 PLA 및 PHA 배럴의 출시를 촉구하고 있습니다. 주요 그룹 기업은 다년간 계약을 체결하고 가격을 안정시키고 공급을 보장합니다. 자본 예산으로 고급 세정 소독기를 충당하고 인건비 제약보다 단가 절감을 우선하는 경우 여전히 재사용 가능한 것이 주류입니다. 하이브리드 전략이 대두되고 있으며, 금속 흡입 핸들과 일회용 주사 바늘과 카트리지를 조합하여 사용하는 클리닉이 안전과 지속가능성의 균형을 이루고 있습니다.

흡입식 모델은 주입 전에 혈관내가 아닌 것을 확인할 수 있기 때문에 2024년 치과용 주사기 시장 점유율의 62.21%를 획득했습니다. 비흡입식 디자인은 일상적인 조성물이나 예방조치 시에 보다 단순한 취급을 요구하는 젊은 개업의에게 호소하고 있습니다.

디지털 CCLAD 플랫폼에는 압력 센서가 내장되어있어 수동으로 흡입하지 않고 조직의 차이를 확인할 수 있습니다. 얇은 게이지 바늘과 결합하여 이러한 시스템은 거의 무통의 침윤을 실현하고 선택적인 미용 치료에서 환자의 수용을 넓히고 있습니다. LED 기반의 Nuralyte와 같은 바늘이 없는 장비는 추가적인 파괴를 약속하지만, 적응은 여전히 얕은 치료에 한정되어 있으며, 채용은 향후 FDA 승인에 달려 있습니다. 기존의 흡입 주사기는 현재 진화하는 치과용 주사기 시장 내에서 관련성을 유지하기 위해 실리콘 코팅과 플런저 마찰 감소를 통합하고 있습니다.

지역 분석

북미는 2024년 매출의 43.43%를 차지하며 엄격한 CDC 프로토콜과 광범위한 보험 적용이 프리미엄 장비의 보급을 지원했습니다. 컴퓨터 제어 시스템은 대규모 그룹 진료소에서 일반적이며 성인의 91%가 치과 진찰을 연 1회의 건강 진단과 동일시하고 있는 것이 처치 건수를 뒷받침하고 있습니다. 2025년 4월에 관세가 도입되어 장비 비용이 상승해 판매자는 멕시코와 베트남에 공급원을 분산하여 카탈로그 폭을 넓혔습니다. 3M에서 분리된 독립적인 Solventum은 매출액이 1.8% 감소했음에도 불구하고 2024년 1분기 치과용 솔루션 매출액이 3억 3,500만 달러를 기록하여 이 지역의 치과용 주사기 시장의 탄력성을 보였습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 6.56%를 나타내 가장 빠르게 성장하고 있는 지역입니다. 말레이시아는 그 동향을 나타내고 있으며, 2027년까지 28억 달러의 치과 서비스 부문이 민간 진료소에서 70%의 점유율을 차지할 것으로 예상됩니다. 중간 소득층의 소득 증가는 정확한 국소 마취에 의존하는 심미 치과 교정과 임플란트 치료 수요를 밀어 올리고 있습니다. 덴탈 투어리즘은 호텔 스타일의 복구 스위트와 EU 호환 감염 프로토콜을 융합하고 있으며, 시설에서는 바코드가 달린 껍질 파우치에 포장 된 일회용 흡입 주사기를 선호합니다. 국내 제조업체는 비용 효율적인 폴리스티렌 배럴을 공급하는 반면 수입업체는 고급 CCLAD 유닛을 판매하고 치과용 주사기 시장에 계층적인 기회를 창출하고 있습니다.

유럽은 서큘러 이코노미의 의제가 소재 선택을 재구축하는 동안 일관된 성장을 유지하고 있습니다. EU 포장 및 포장 폐기물 규정은 2030년까지 재활용 가능한 부품의 재설계를 생산자에게 의무화하고 있습니다. 독일에서는 임상용 바이오플라스틱의 지자체 회수가 시험적으로 개시되어, 신속하게 시장에 진입한 기업이 브랜드 면에서 우위에 서 있습니다. 프랑스와 스칸디나비아의 클리닉은 탄소 중립 수복물을 홍보하고 PLA와 PHA의 주사기 바디를 지원합니다. 동유럽은 저렴한 풀 아치 임플란트를 요구하는 인바운드 치과 관광객들로부터 기세를 얻고 있으며, 미드레인지 흡입장치의 매출을 견인하고 있습니다. 중동 및 아프리카는 의료 관광과 호화로운 접객를 결합한 GCC 국가를 중심으로 수요 가속을 기록하고 있습니다. 남미에서는 브라질과 아르헨티나가 현지 플라스틱 생산을 활용하여 치과용 주사기 시장공급망을 안정화시켜 점진적인 성장을 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고령화에 의한 보철 작업량의 확대

- 우식과 치주병의 유병률 상승

- 감염 관리를 위한 일회용 안전 주사기로의 급속한 이동

- APAC 및 CEE에서 치과 관광의 성장

- 의자 사이드에서 디지털 마취 제공이 프리미엄 주사기 수요를 뒷받침

- 고소득 클리닉에 있어서의 RFID 대응 기기 트래킹의 의무화

- 시장 성장 억제요인

- 저소득 지역에서의 숙련 치과 의사의 부족

- 전자 주사기 및 스마트 주사기의 초기 비용

- 일회용 플라스틱에 대한 규제 강화에 의한 컴플라이언스 비용의 상승

- 의료용 스테인레스 공급 불안정

- 규제 상황

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 용도별

- 재사용 가능한 치과용 주사기

- 일회용 치과용 주사기

- 제품 유형별

- 흡입식

- 비흡입식

- 재료별

- 금속

- 플라스틱

- 최종 사용자별

- 치과 병원 및 클리닉

- 치과 기공소

- 기타

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Solventum

- Dentsply Sirona

- Septodont

- Vista Dental Products

- Integra LifeSciences

- A. Titan Instrument Inc.

- Ultradent Products

- Power Dental USA

- Accesia

- Anthogyr SAS

- Carl Martin GmbH

- Asa Dental SpA

- Faro SpA

- Diadent Group International

- Milestone Scientific

- Orsing AB

- Kulzer GmbH

- Henry Schein Inc.

- Coricama S.r.l

- Tillid Dental

제7장 시장 기회와 전망

KTH 25.10.29The dental syringes market stood at USD 160.61 million in 2025 and is forecast to reach USD 210.43 million by 2030, progressing at a 5.55% CAGR.

Growth reflects tighter infection-control requirements, a wider older-adult population needing prosthodontic care, and the steady roll-out of computer-controlled local anesthetic delivery systems. Heightened awareness after recent global health events has moved dentists toward single-use devices and RFID-tracked instruments that simplify compliance with CDC sterilization rules. Insurers are also influencing demand: 65% of U.S. adults held dental coverage in 2024 and 91% now view dental check-ups as essential preventive care. On the supply side, manufacturers are redesigning products around biodegradable plastics and lightweight metals to meet the upcoming EU Packaging and Packaging Waste Regulation. Tariffs introduced in April 2025 and volatile stainless-steel supply chains are prompting practices to diversify sourcing and accelerate group purchasing.

Global Dental Syringes Market Trends and Insights

Ageing Population Expanding Prosthodontic Workload

Adults aged 60 and older already number 1.0 billion and will pass 1.4 billion by 2030. Prosthodontic interventions that dominate this cohort demand precise anesthetic delivery, pushing clinics to adopt advanced dental syringes market solutions such as computer-controlled local anesthetic devices . In Malaysia, adults aged 25-54 form the largest patient group, further straining chair capacity. Dental insurers highlight the link between oral and systemic health, driving preventive visits and reinforcing demand for premium syringes. Practices consequently prefer ergonomic designs that perform multiple injections without user fatigue. As full-arch restorations rise, syringe designs featuring high barrel clarity and controlled aspiration are becoming standard .

Rising Prevalence of Caries & Periodontal Disease

More than 280 million older adults face untreated caries or gum disease worldwide. Updated CDC guidelines stipulate that cartridge syringes must be sterilized between patients and that needles as well as anesthetic cartridges remain single use . Emerging economies report faster disease incidence due to sugary diets and limited prophylaxis, opening space for cost-effective yet compliant syringes. Teledentistry is enabling earlier diagnosis among younger adults, creating more occasions for minimally invasive restorations that still need local anesthesia. Early-stage interventions such as drill-free cavity repair delivered by products like Curodont Repair Fluoride Plus lower chair time, but complex cases continue to rely on aspirating devices that confirm safe deposition.

Shortage of Skilled Dentists in Low-Income Regions

Many emerging economies record fewer than one dentist per 10,000 residents. The WHO notes that geographic and economic barriers keep older adults from timely care. Limited training capacity delays the uptake of advanced computer-controlled devices that require instruction on aspiration and flow-rate settings. Governments respond by funding mobile clinics but focus spending on basic instruments. In turn, syringe makers supply simplified metallic formats that tolerate rugged reprocessing and align with thin operating budgets inside the dental syringes industry.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Shift to Single-Use Safety Syringes for Infection Control

- Growth in Dental Tourism Across APAC & CEE

- Up-Front Cost of Electronic & Smart Syringes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reusable devices retained 58.91% revenue in 2024, benefiting from well-established autoclave infrastructures. In the same year disposables grew swiftly as the dental syringes market size for single-use formats recorded a 6.61% CAGR, reflecting heightened infection control vigilance. Practices with patient loads exceeding 30 daily injections cite sterilizer bottlenecks, thus preferring color-coded disposable barrels that cut turnaround time.

Disposable adoption faces environmental scrutiny; the EU framework compels recyclable packaging by 2030, prompting suppliers to launch PLA and PHA barrels that meet compostability targets. Large group practices lock in multi-year contracts to stabilize pricing and guarantee supply. Reusables still dominate where capital budgets cover advanced washer-disinfectors and where unit cost savings outweigh staffing constraints. Hybrid strategies emerge, with clinics using metallic aspirating handles paired with single-use needles and cartridges to balance safety and sustainability.

Aspirating models captured 62.21% of dental syringes market share in 2024 because they allow clinicians to verify they are not in a blood vessel before injecting. Non-aspirating designs appeal to younger practitioners seeking simpler handling during routine composites and prophylaxis.

Digital CCLAD platforms incorporate pressure sensors that can identify tissue differences without manual aspiration. When paired with narrow-gauge needles, these systems deliver near-painless infiltration which is expanding patient acceptance in elective cosmetic work. Needle-free devices such as LED-based Nuralyte promise further disruption; however, indications remain limited to shallow treatments and adoption hinges on upcoming FDA clearance. Traditional aspirating syringes now integrate silicone coating and reduced plunger friction to maintain relevance within an evolving dental syringes market.

The Dental Syringes Market is Segmented by Usability (Reusable Dental Syringes, and More), Product Type (Aspirating and Non-Aspirating), Material (Metallic and Plastic), End-User (Dental Hospitals & Clinics, Dental Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 43.43% of 2024 revenue as stringent CDC protocols and widespread insurance coverage sustained premium device uptake. Computer-controlled systems are common in large group practices, and 91% of adults equate dental visits with annual physicals which underpins procedure volumes. Tariffs imposed in April 2025 raise equipment costs so distributors diversify toward Mexico and Vietnam sources to maintain catalog breadth. Solventum, spun off from 3M, posted USD 335 million in Q1-2024 dental solutions sales in spite of a 1.8% revenue dip, demonstrating resilience in the regional dental syringes market.

Asia-Pacific is the fastest-growing territory with a 6.56% CAGR to 2030. Malaysia illustrates the trend: a USD 2.8 billion dental services sector by 2027 with private clinics holding 70% share. Rising middle-class incomes boost demand for cosmetic orthodontics and implantology, both reliant on accurate local anesthesia. Dental tourism blends hotel-style recovery suites with EU-compliant infection protocols, leading facilities to favor single-use aspirating syringes packaged in bar-coded peel pouches. Domestic manufacturers supply cost-efficient polystyrene barrels while importers market premium CCLAD units, creating tiered opportunities inside the dental syringes market.

Europe maintains consistent growth as the circular-economy agenda reshapes material selection. The EU Packaging and Packaging Waste Regulation forces producers to redesign components for recyclability by 2030. Germany pilots municipal collection of clinical-grade bioplastics, giving early movers brand advantage. Clinics in France and Scandinavia advertise carbon-neutral restorations which in turn favor PLA or PHA syringe bodies. Eastern Europe gains momentum from inbound dental tourists seeking affordable full-arch implants, driving mid-range aspirating device sales. The Middle East and Africa record accelerating demand, especially in GCC countries that pair medical tourism with luxury hospitality. South America exhibits incremental gains, with Brazil and Argentina leveraging local plastics production to stabilize supply chains within the dental syringes market.

- Solventum

- Dentsply Sirona

- Septodont

- Vista Dental Products

- Integra LifeSciences

- A. Titan Instrument

- Ultradent Products

- Power Dental USA

- Accesia

- Anthogyr

- Carl Martin

- Asa Dental

- Faro

- DiaDent

- Milestone Scientific

- Orsing AB

- Kulzer

- Henry Schein

- Coricama S.r.l

- Tillid Dental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing population expanding prosthodontic workload

- 4.2.2 Rising prevalence of caries & periodontal disease

- 4.2.3 Rapid shift to single-use safety syringes for infection control

- 4.2.4 Growth in dental tourism across APAC & CEE

- 4.2.5 Chair-side digital anesthesia delivery boosting premium syringe demand

- 4.2.6 RFID-enabled instrument-tracking mandates in high-income clinics

- 4.3 Market Restraints

- 4.3.1 Shortage of skilled dentists in low-income regions

- 4.3.2 Up-front cost of electronic & smart syringes

- 4.3.3 Regulatory crack-down on single-use plastics raising compliance cost

- 4.3.4 Volatile supply of medical-grade stainless steel

- 4.4 Regulatory Landscape

- 4.5 Porters Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Usability

- 5.1.1 Reusable Dental Syringes

- 5.1.2 Disposable Dental Syringes

- 5.2 By Product Type

- 5.2.1 Aspirating

- 5.2.2 Non-aspirating

- 5.3 By Material

- 5.3.1 Metallic

- 5.3.2 Plastic

- 5.4 By End-User

- 5.4.1 Dental Hospitals & Clinics

- 5.4.2 Dental Laboratories

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, Recent Developments)

- 6.3.1 Solventum

- 6.3.2 Dentsply Sirona

- 6.3.3 Septodont

- 6.3.4 Vista Dental Products

- 6.3.5 Integra LifeSciences

- 6.3.6 A. Titan Instrument Inc.

- 6.3.7 Ultradent Products

- 6.3.8 Power Dental USA

- 6.3.9 Accesia

- 6.3.10 Anthogyr SAS

- 6.3.11 Carl Martin GmbH

- 6.3.12 Asa Dental SpA

- 6.3.13 Faro SpA

- 6.3.14 Diadent Group International

- 6.3.15 Milestone Scientific

- 6.3.16 Orsing AB

- 6.3.17 Kulzer GmbH

- 6.3.18 Henry Schein Inc.

- 6.3.19 Coricama S.r.l

- 6.3.20 Tillid Dental

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment