|

시장보고서

상품코드

1842606

세포주 개발 : 시장 점유율 분석, 산업 동향, 통계, 성장 동향 예측(2025-2030년)Global Cell Line Development - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

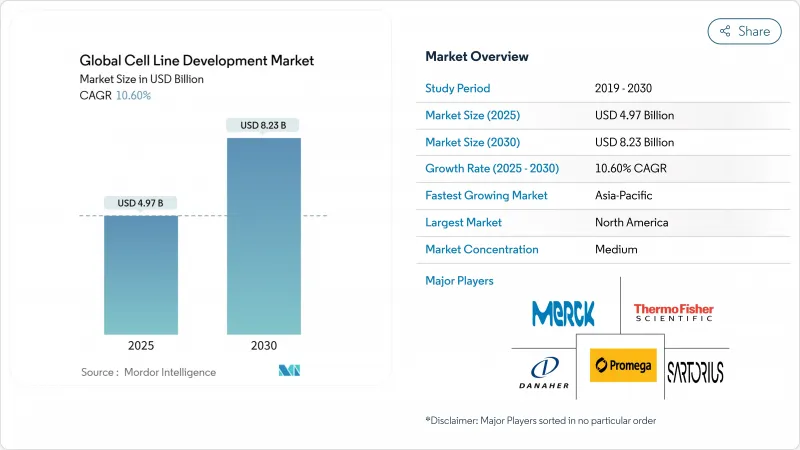

세포주 개발 시장은 2025년에 49억 7,000만 달러에 이르고, 2030년에는 82억 3,000만 달러로 확대될 것으로 예측됩니다.

복잡한 단백질, 단클론 항체 및 유전자 치료는 모두 상업적 규모의 생산을 위해 고도로 조작된 세포주를 필요로 하기 때문입니다. 지속적인 바이오프로세스에 대한 자본 지출 증가, 아웃소싱으로의 전환 가속, AI 유도형 최적화 플랫폼의 등장으로 개발 사이클은 이미 6-9개월에서 3-4개월로 단축되고 있으며, 선행 기업은 눈에 띄는 경쟁 우위를 획득하고 있습니다. 리스크 기반 바이러스 안전성 평가를 뒷받침하는 규제 개혁은 컴플라이언스 비용과 품질 인센티브를 모두 생성하며, 지정학적 긴장은 단일 국가공급 리스크에 대한 노출을 줄이는 지역 제조 클러스터를 촉진합니다. 이러한 구조적 힘을 종합하면 세포주 개발 시장이 생물학적 제제의 다음 파동을 초래하는 데 핵심적인 역할을 수행하는 것이 강화됩니다.

세계의 세포주 개발 시장 동향과 인사이트

증가하는 바이오 의약품 수요

단일클론항체는 이미 생물학적 제형의 파이프라인을 지배하고 있으며, 자가면역질환이나 희소질환에 대한 적응확대가 세포주 생산성을 압박하고 있습니다. 200개가 넘는 항체 치료제가 승인되었으며, 1,400개가 넘는 후보가 현재 개발 중이기 때문에 스폰서는 임상 프로그램의 초기 단계부터 견고하고 생산적인 세포주를 확보할 필요가 있습니다. 그러므로 세포주 개발 시장은 전체 프로젝트의 타임라인과 상업적 실행 가능성을 크게 좌우하는 전략적 병목 역할을 합니다. 이중특이적 항체와 항체 약물 복합체의 개발량이 증가함에 따라 균형 잡힌 사슬의 발현이 가능한 엔지니어링 세포주가 필요하며, 특수한 개발 서비스에 대한 비싼 가격 설정이 추진되고 있습니다. 어느 지역에서도 저분자보다 고분자 쪽이 우선적으로 투자하게 되어 첨단 세포 배양 시스템에 대한 장기적인 수요가 높아지고 있습니다.

단일클론항체 파이프라인 확대

2020년 이후의 이중특이적 항체의 임상 승인은 세포 공학 워크플로우의 복잡성을 두배로 하는 듀얼 타겟 포맷으로의 변화를 부각시켰습니다. 제약사는 엔드 투 엔드 항체 약물 복합체의 생산 능력을 확보하기 위해 아스트라 제네카의 15억 달러의 싱가포르 사이트와 같은 전용 시설에 계속 자금을 공급하고 있습니다. 각 신규 항체 포맷에는 독자적인 폴딩이나 글리코실화의 요구가 있기 때문에 스폰서는 장기 공급 계약이 가능한 독자적인 세포 플랫폼을 점점 선호하게 되고 있습니다. 이러한 역학은 특히 턴키 엔지니어링 및 다운스트림 분석을 제공하는 서비스 제공업체들에게 세포주 개발 시장에서 경쟁을 격화시키고 있습니다.

엄격한 규정 준수

바이러스 안전성에 대한 FDA의 Q5A(R2) 지침은 업데이트되어 새로운 세포 기질에 대해 최대 1년간의 추가 시험이 되는 특성 시험의 연장을 요구하고 있습니다. 사내에 규제에 관한 전문지식이 없는 기업은 높은 컨설팅료를 부담하여야 하며, 제출서류가 진화하는 기준에 못 미치는 경우에는 되돌아갈 가능성도 있습니다. 유럽에서는 다른 지역에서는 요구되지 않는 추가적인 모험적 약물 스크리닝이 요구되기 때문에 지역마다 다른 기대가 세계 상시의 순서를 복잡하게 합니다. 이러한 압력은 세포주 개발 시장에서 활동하기 위한 고정비를 증가시키고 중소기업의 철수와 통합을 초래하며 수직 통합된 선도적인 공급자로 협상력을 옮길 수 있습니다.

부문 분석

시약·배지는 2024년 매출액의 44.12%를 차지했는데, 이는 생산 로트마다 대량의 배지, 사료, 완충액을 소비하기 때문입니다. 이 부문의 예측 CAGR은 10.94%를 나타내 자본 설비보다 많습니다. 이는 새로운 치료법이 승인될 때마다 소모품의 정기 주문이 증가하고 세포주 개발 시장 전반에 걸쳐 예측 가능한 수요가 확보되기 때문입니다. 공급업체는 오염 위험을 줄이면서 배치 일관성을 향상시키는 화학적으로 정의된 무혈청 제형을 선호하며, AI 대응 설계 도구는 피크 역가를 높이기 위해 영양 블렌드를 최적화합니다. 생물반응기 및 자동화된 세포 처리 시스템을 커버하는 장비는 세포 밀도가 증가함에 따라 영양 고갈과 폐기물의 축적을 피하기 위해 정확한 공정 제어가 필요하기 때문에 여전히 매우 중요합니다. 세포 뱅킹, 분석 검사, 바이러스 클리어런스 시험 등의 부수 서비스는 규제 당국의 감시 강화의 혜택을 받아 롱테일 카테고리로 성장하고 있습니다.

시약 카테고리는 바이오 리액터가 장시간 관류 운전 중에 지속적으로 공급 성분을 흡입하기 때문에 구독과 같은 구매 패턴에서 더 많은 이익을 얻고 있습니다. 현재 전문 공급업체는 독특한 대사 실적를 보여주는 CRISPR 변형된 세포주에 맞는 모듈식 배지 키트를 판매하고 있습니다. 공정 강화가 진행됨에 따라 고순도 원료에 대한 수요가 증가하고 아미노산과 비타민 생산을 수직 통합하려는 공급업체가 나타날 것으로 보입니다. 이러한 동향을 종합하면 세포주 개발 시장에서 소모품의 경쟁적 중요성이 강화되어 배지의 혁신과 시설 전체의 생산량과의 연결이 강해집니다.

2024년 세포주 개발 시장 점유율의 75.04%는 포유동물주가 차지했고, 그 CAGR은 11.35%를 나타내 인간과 유사한 번역후 수식을 선호하는 경향이 지속되고 있음을 뒷받침하고 있습니다. 차이니즈 햄스터 난소 세포는 여전히 단일클론항체의 골드 표준인 반면, 주요 당쇄 변형 유전자를 제거하는 CRISPR 녹아웃은 면역원성을 감소시키고 보다 균질한 당쇄를 제공합니다. 현탁 증식에 최적화된 인간 배아 신장(HEK293) 균주는 유전자 치료를 위한 아데노-관련 바이러스 벡터 생산의 대부분을 지원하고 있으며, 현재 바이러스 응용의 세포주 개발 시장 규모에 중요한 수익을 제공합니다. 효모와 곤충 균주를 포함한 비 포유류 시스템은 복잡한 글리코 실화가 필요없는 틈새 효소와 백신 응용을 지원합니다.

높은 처리량의 마이크로플루이딕스 스크리닝의 진보는 기존의 한계 희석 캠페인에서 몇 주를 줄여 포유류의 최고 생산 클론을 신속하게 분리할 수 있습니다. 새로운 유전체 불안정성 센서는 염색체 이상을 실시간으로 추적하여 불안정한 클론의 조기 도태를 가능하게 합니다. 박테리아와 효모 시스템은 전반적인 성장이 포유류보다 느리지만 단순한 단백질 산물에서 여전히 우수합니다. 이러한 기술 믹스를 통해, 세포주 개발 시장은 특정 분자 요구 사항과 가장 비용 효율적인 세포 섀시를 맞출 수있는 다양한 도구 상자를 유지합니다.

지역 분석

북미는 엘라이 릴리의 인디애나 복합시설(90억 달러)과 노보 노르디스크 노스캐롤라이나 확장(41억 달러) 등 대규모 투자에 힘입어 2024년 매출액 점유율은 40.23%를 유지했습니다. 이 지역은 확립된 규제의 전문 지식과 강력한 벤처 캐피탈로부터 혜택을 받고 있지만, 공급 연속성을 복잡하게 하는 원료 부족과 수출 규제의 불확실성에 직면하고 있습니다. 캐나다의 옴니아 바이오(OmniaBio)사는 AI를 활용한 세포 치료 허브를 건설 중이며 제조 비용을 절반으로 줄이도록 설계되었습니다. 멕시코는 국내 비용 구조를 부담하지 않고 미국과의 근접성을 요구하는 기업의 니어 쇼어링에 대한 관심을 모으고 있습니다. 이러한 역학을 종합하면 북미의 세포주 개발 시장은 혁신적이고 자본 집약적이어야 합니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 11.23%를 나타낼 것으로 예상되고, 2024년에는 싱가포르만으로 30억 달러 이상의 바이오 제조가 위탁되었습니다. 아스트라제네카의 15억 달러의 ADC 공장과 BioNTech의 독일 국외 최초의 시설은 이 지역이 프리미엄 바이오 제조 목적지로 부상하고 있음을 보여줍니다. 중국과 인도는 비용면에서의 우위성과 큰 내수를 유지하고 있지만, 미국 BIOSECURE법의 제안에 의해 인도의 CDMO, 한국의 생물제제 클러스터, ASEAN 회원국으로의 다양화가 가속화되고 있습니다. 일본과 호주는 각각 고정밀 분석과 RNA 치료제 플랫폼을 통해 생태계를 보완합니다. 이러한 움직임은 세포주 개발 시장의 중심을 아시아태평양으로 옮기는 동시에 지정학적 위험을 줄이는 다극 공급 네트워크를 형성합니다.

유럽은 독일, 스위스, 아일랜드의 확립된 의약 회랑에 힘입어 꾸준하지만 완만한 확대가 계속되고 있습니다. 선진치료에 대한 정부의 우대조치와 국경을 넘은 규제의 하모나이제이션이 경쟁력을 유지하고 있지만, 에너지 비용과 임금 인플레이션이 아시아에 비해 이폭을 좁히고 있습니다. 중동 및 아프리카는 전략적 진입을 도모하고 있으며, 사우디아라비아의 국가 생명 공학 전략은 2040년까지 세계 리더십을 목표로 하고 있으며, UAE는 지역 물류 기지로서의 지위를 확립하고 있습니다. 브라질을 필두로 하는 남미는 내수와 바이오시밀러라는 새로운 비즈니스 기회를 개척하고 있지만, 벤처기업의 자금조달이 한정되어 있어 급속한 생산능력 증강에는 한계가 있습니다. 전반적으로 세포주 개발 시장이 지역 수요에 부합하고 공급망의 위험을 줄이는 다양한 제조 허브에 의존하는 균형 잡힌 세계 발자국이 떠오릅니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 바이오의약품 수요 증가

- 단일클론항체 파이프라인의 확대

- 특허 절벽 후의 바이오시밀러 생산의 급증

- 상용 바이오프로세싱·인프라의 CAPEX 경쟁

- AI에 의한 세포주 최적화 플랫폼

- 중동, 아프리카와 ASEAN의 지역 바이오 CDMO 클러스터의 상승

- 시장 성장 억제요인

- 엄격한 규제 준수

- 긴 세포주 안정화 스케줄

- cGMP 등급 원재료 공급망 부족

- CHO/HEK 세포주의 지정학적 수출 규제 위험

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 제품별

- 시약 및 배지

- 기기

- 기타 제품

- 원천별

- 포유류 세포주

- 비포유류 세포주

- 용도별

- 재조합 단백질 발현

- 하이브리도마 기술

- 백신 생산

- 신약 개발 및 스크리닝

- 유전자 및 세포 치료제 제조

- 기타 용도

- 최종 사용자별

- 바이오제약 및 제약 기업

- 계약 개발 및 제조 기관(CDMO)

- 학술 및 연구 기관

- 기타 최종 사용자

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- American Type Culture Collection(ATCC)

- Sartorius AG

- Danaher Corporation(Cytiva)

- Merck KGaA(MilliporeSigma)

- Thermo Fisher Scientific

- WuXi Biologics

- Corning Incorporated

- Selexis SA(JSR Life Sciences)

- Promega Corporation

- Fujifilm Diosynth Biotechnologies

- Lonza Group

- GE HealthCare(Cell Culture)

- Samsung Biologics

- AGC Biologics

- Horizon Discovery(PerkinElmer)

- Charles River Laboratories

- KBI Biopharma

- BioReliance(Merck)

- GenScript Biotech

- Evotec SE

제7장 시장 기회와 전망

KTH 25.10.29The cell line development market reached USD 4.97 billion in 2025 and is forecast to expand to USD 8.23 billion by 2030, reflecting a 10.60% CAGR through the period.

Expanding demand for biologics, which accounted for more than 40% of 2024 drug approvals, anchors this growth as complex proteins, monoclonal antibodies, and gene therapies all require highly engineered cell lines for commercial-scale production. Heightened capital expenditure on continuous bioprocessing, an accelerating shift toward outsourcing, and the advent of AI-guided optimization platforms have already shortened development cycles from 6-9 months to 3-4 months, giving first movers a tangible competitive edge. Regulatory reforms that favor risk-based viral safety evaluations create both compliance costs and quality incentives, while geopolitical tensions encourage regional manufacturing clusters that reduce exposure to single-country supply risks. Taken together, these structural forces reinforce the central role that the cell line development market will play in delivering the next wave of biologics.

Global Cell Line Development Market Trends and Insights

Growing Biopharmaceutical Demand

Monoclonal antibodies already dominate biologic pipelines, and their growth into autoimmune and rare disease indications sustains pressure on cell line productivity. Over 200 antibody therapeutics are approved, with nearly 1,400 candidates in active development, forcing sponsors to secure robust, high-yielding cell lines early in clinical programs. The cell line development market therefore functions as a strategic bottleneck that largely dictates overall project timelines and commercial viability. Rising volumes of bispecific antibodies and antibody-drug conjugates require engineered cell lines capable of balanced chain expression, driving premium pricing for specialized development services. Across every major geography, large molecules now receive preferential investment over small molecules, cementing long-term demand for sophisticated cell culture systems.

Expansion of Monoclonal Antibody Pipelines

Clinical approvals of bispecific antibodies since 2020 highlight the shift toward dual-target formats, which double the complexity of cell engineering workflows. Pharmaceutical majors continue to finance dedicated facilities, such as AstraZeneca's USD 1.5 billion Singapore site, to secure end-to-end antibody-drug conjugate production capacity. As each novel antibody format carries unique folding and glycosylation needs, sponsors increasingly favor proprietary cell platforms that can be locked into long-term supply agreements. Those dynamics intensify the competitive race within the cell line development market, particularly for service providers that offer turnkey engineering plus downstream analytics.

Stringent Regulatory Compliance

The FDA's updated Q5A(R2) guidance on viral safety requires extended characterization studies, adding up to one year of additional testing for new cell substrates. Companies lacking in-house regulatory expertise must absorb higher consulting fees and possible rework if submissions fall short of evolving standards. Divergent regional expectations complicate global launch sequencing, as Europe often requests supplementary adventitious-agent screens not demanded elsewhere. These pressures raise the fixed costs of operating in the cell line development market and may lead smaller firms to exit or consolidate, shifting bargaining power toward large, vertically integrated providers.

Other drivers and restraints analyzed in the detailed report include:

- CAPEX Race for Continuous Bioprocessing Infrastructure

- AI-Guided Cell-Line Optimisation Platforms

- Shortage of cGMP-Grade Raw-Material Supply Chains

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Reagents and media represented 44.12% of 2024 revenue, as every production lot consumes large volumes of culture medium, feed, and buffer. The segment's 10.94% forecast CAGR exceeds that of capital equipment because each new therapy approval scales recurring consumable orders, ensuring predictable demand within the broader cell line development market. Suppliers prioritize chemically defined and serum-free formulations that improve batch consistency while reducing contamination risks, and AI-enabled design tools optimize nutrient blends to lift peak titers. Equipment, which covers bioreactors and automated cell-handling systems, remains crucial because rising cell densities require precise process control to avoid nutrient depletion and waste accumulation. Ancillary services, such as cell banking, analytical testing, and viral clearance studies, round out a growing long-tail category that benefits from heightened regulatory scrutiny.

The reagents category further benefits from subscription-like purchasing patterns, as bioreactors continuously draw feed components during extended perfusion runs. Specialized vendors now market modular media kits tailored to CRISPR-engineered cell lines that exhibit unique metabolic footprints. As process intensification expands, demand for high-purity raw materials will escalate, encouraging suppliers to vertically integrate amino-acid and vitamin production. Collectively, these trends consolidate the competitive importance of consumables within the cell line development market, tightening linkages between media innovation and overall facility output.

Mammalian lines controlled 75.04% of cell line development market share in 2024, and their 11.35% CAGR underscores sustained preference for human-like post-translational modifications. Chinese hamster ovary cells remain the gold standard for monoclonal antibodies, while CRISPR knockouts that delete key glycosylation genes deliver more homogeneous glycoforms with reduced immunogenicity. Human embryonic kidney (HEK293) lines, optimized for suspension growth, underpin most adeno-associated viral vector production for gene therapies and now contribute meaningful revenue to the cell line development market size for viral applications. Non-mammalian systems, including yeast and insect lines, address niche enzyme and vaccine applications where complex glycosylation is unnecessary.

Advances in high-throughput microfluidic screening enable the rapid isolation of top-producing mammalian clones, cutting weeks from traditional limiting dilution campaigns. Novel genomic instability sensors track chromosomal aberrations in real time, allowing early culling of unstable clones. Bacterial and yeast systems still excel for simple protein products, although their overall growth lags mammalian gains. That technology mix ensures that the cell line development market maintains a diverse toolbox capable of matching specific molecular requirements with the most cost-effective cellular chassis.

The Cell Line Development Market Report Segments the Industry Into by Product (Reagent & Media, Equipment, Other Products), by Source (Mammalian Cell Line, Non-Mammalian Cell Line), by Application (Recombinant Protein Expression, Hybridomas Technology, and More. ), by End User (Biotech & Pharma Companies, Cdmos, and More. ), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America maintained 40.23% revenue share in 2024, buoyed by large-scale investments such as Eli Lilly's USD 9 billion Indiana complex and Novo Nordisk's USD 4.1 billion North Carolina expansion. The region benefits from entrenched regulatory expertise and robust venture capital, yet faces raw-material shortages and export-control uncertainties that complicate supply continuity. Canada's OmniaBio is building an AI-enabled cell therapy hub designed to halve production costs, signaling regional commitment to advanced manufacturing. Mexico attracts near-shoring interest as companies seek proximity to the United States without incurring domestic cost structures. Collectively, these dynamics ensure that the cell line development market in North America remains both innovative and capital intensive.

Asia-Pacific records the fastest 11.23% CAGR through 2030, fueled by more than USD 3 billion of 2024 biomanufacturing commitments in Singapore alone. AstraZeneca's USD 1.5 billion ADC plant and BioNTech's first ex-Germany facility exemplify the region's rise as a premium biomanufacturing destination. China and India retain cost advantages and large internal demand, yet the U.S. BIOSECURE Act proposal accelerates diversification toward Indian CDMOs, South Korean biologics clusters, and ASEAN member states. Japan and Australia complement the ecosystem through high-precision analytics and RNA therapeutics platforms, respectively. These moves collectively shift the gravitational center of the cell line development market toward Asia-Pacific while creating multipolar supply networks that mitigate geopolitical risks.

Europe experiences steady but slower expansion, supported by established pharmaceutical corridors in Germany, Switzerland, and Ireland. Government incentives for advanced therapies and cross-border regulatory harmonization preserve competitiveness, although energy costs and wage inflation narrow margins relative to Asia. The Middle East and Africa pursue strategic entry, with Saudi Arabia's National Biotechnology Strategy targeting global leadership by 2040 and the UAE positioning itself as a regional logistics node. South America, led by Brazil, taps domestic demand and emerging biosimilar opportunities, yet limited venture funding constrains rapid capacity build-out. Altogether, a rebalanced global footprint emerges in which the cell line development market relies on diverse manufacturing hubs to match local demand and de-risk supply chains.

- American Type Culture Collection

- Sartorius

- Danaher

- Merck KGaA (MilliporeSigma)

- Thermo Fisher Scientific

- Wuxi Biologics

- Corning

- Selexis SA (JSR Life Sciences)

- Promega

- FUJIFILM

- Lonza Group

- GE HealthCare (Cell Culture)

- Samsung Group

- AGC Biologics

- Horizon Discovery (PerkinElmer)

- Charles River

- KBI Biopharma

- BioReliance (Merck)

- GenScript Biotech

- Evotec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Biopharmaceutical Demand

- 4.2.2 Expansion of Monoclonal Antibody Pipelines

- 4.2.3 Surge in Biosimilar Production Post-patent Cliff

- 4.2.4 CAPEX Race for Continuous Bioprocessing Infrastructure

- 4.2.5 AI-guided Cell-line Optimisation Platforms

- 4.2.6 Rise of Regional Bio-CDMO Clusters in MENA & ASEAN

- 4.3 Market Restraints

- 4.3.1 Stringent Regulatory Compliance

- 4.3.2 Lengthy Cell-line Stability Timelines

- 4.3.3 Shortage of cGMP-grade Raw-material Supply Chains

- 4.3.4 Geopolitical Export-control Risks for CHO/HEK Cell Lines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Million)

- 5.1 By Product

- 5.1.1 Reagents & Media

- 5.1.2 Equipment

- 5.1.3 Other Products

- 5.2 By Source

- 5.2.1 Mammalian Cell Line

- 5.2.2 Non-mammalian Cell Line

- 5.3 By Application

- 5.3.1 Recombinant Protein Expression

- 5.3.2 Hybridoma Technology

- 5.3.3 Vaccine Production

- 5.3.4 Drug Discovery & Screening

- 5.3.5 Gene & Cell Therapy Manufacturing

- 5.3.6 Other Applications

- 5.4 By End User

- 5.4.1 Biopharma & Pharma Companies

- 5.4.2 Contract Development & Manufacturing Organisations (CDMOs)

- 5.4.3 Academic & Research Institutes

- 5.4.4 Other End-users

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles

- 6.3.1 American Type Culture Collection (ATCC)

- 6.3.2 Sartorius AG

- 6.3.3 Danaher Corporation (Cytiva)

- 6.3.4 Merck KGaA (MilliporeSigma)

- 6.3.5 Thermo Fisher Scientific

- 6.3.6 WuXi Biologics

- 6.3.7 Corning Incorporated

- 6.3.8 Selexis SA (JSR Life Sciences)

- 6.3.9 Promega Corporation

- 6.3.10 Fujifilm Diosynth Biotechnologies

- 6.3.11 Lonza Group

- 6.3.12 GE HealthCare (Cell Culture)

- 6.3.13 Samsung Biologics

- 6.3.14 AGC Biologics

- 6.3.15 Horizon Discovery (PerkinElmer)

- 6.3.16 Charles River Laboratories

- 6.3.17 KBI Biopharma

- 6.3.18 BioReliance (Merck)

- 6.3.19 GenScript Biotech

- 6.3.20 Evotec SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment