|

시장보고서

상품코드

1842609

두개 임플란트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Cranial Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

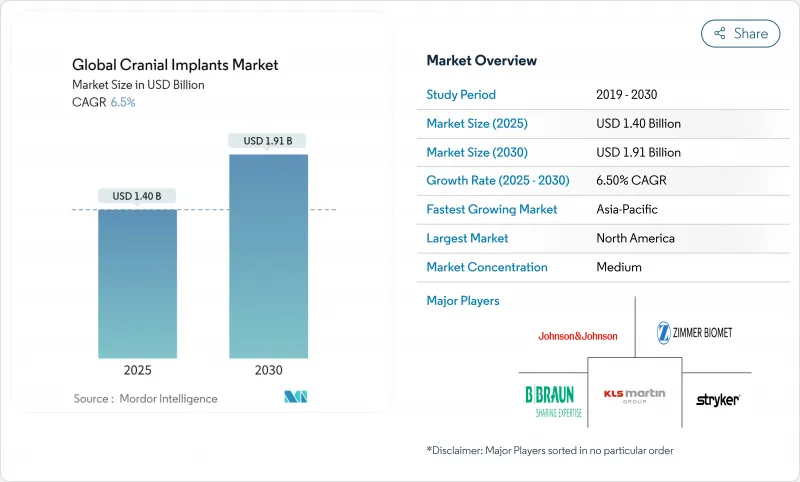

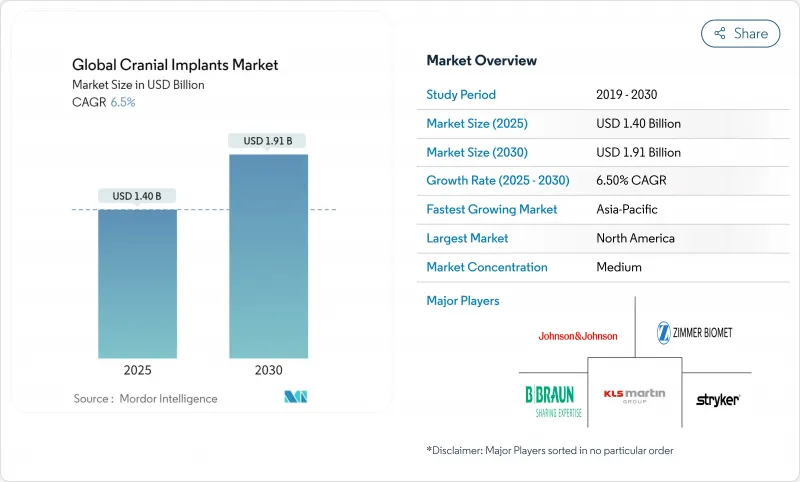

두개 임플란트 시장은 2025년에 14억 달러에 이르고, 2030년에는 CAGR 6.5%를 나타내 19억 1,000만 달러로 확대될 것으로 예측됩니다.

왕성한 수요는 외상성 뇌 손상의 꾸준한 증가, 신흥 국가의 신경 수술 능력 확대, 3 차원 환자별 제조로의 결정적인 변화로 인해 발생합니다. 병원이 주요 고객 기반이라는 점은 변함이 없지만, 지급자가 성과가 높은 시설을 보상하기 때문에 전문 뇌신경 수술센터가 급속히 확대되고 있습니다. 티타늄은 수십년에 걸친 임상 증명을 위해 우위를 유지하고 있지만, 외과의사가 아티팩트가 없는 이미지를 우선시함에 따라 PEEK와 같은 고분자 대체 재료가 지지를 모으고 있습니다. 기존의 가공은 여전히 대량 생산 요구를 충족하지만, 3D 프린터 솔루션은 수술 시간과 재수술 위험을 줄이기 때문에 복잡한 경우에 승리를 거두고 있습니다. 지역별로는 북미가 매출을 이끌고 있지만, 아시아태평양은 인프라 정비와 규제의 현대화에 의해 디바이스의 승인 사이클이 단축되어 급성장하고 있습니다.

세계의 두개 임플란트 시장 동향과 인사이트

두개 외상과 신경 외과 수술의 발생률 상승

세계에서는 매년 약 6,900만 건의 외상성 뇌손상이 발생하고 있으며, 중증례에서는 두개성형술에 의한 재건이 필요하게 되는 경우가 많습니다. 인구 고령화, 자동차 밀도 상승, 조직화된 스포츠가 임상적 부담을 높이고 있습니다. 국방부의 신경보호에 관한 연구는 군의가 전장 부상에 대해 신뢰성 있는 합성판을 필요로 하기 때문에 수요를 더욱 증대시키고 있습니다. 병원 수준에서는 신경 외상 전문센터가 복잡한 사례를 집계하고 있기 때문에 대량 공급업체에게 예측 가능한 조달주기가 형성됩니다. 외상 발생률은 경기 사이클과의 상관성이 낮기 때문에 두개 임플란트 시장은 제조업체와 의료 시스템에 의한 장기적인 계획을 지원하는 수비 건강 관리의 지위를 누리고 있습니다.

환자 전용 임플란트를 위한 3D 프린팅 진행

Additive Manufacturing은 획일적인 수술에서 맞춤형 재건으로 변모합니다. 2024년 3D 시스템즈의 PEEK 두개판의 FDA 승인은 폴리머 적층 성형 임플란트의 규제 실행 가능성을 입증했습니다. 외과의사는 현재 CT 데이터를 즉시 인쇄할 수 있는 파일로 변환하는 클라우드 기반 설계 도구에 몇 분 안에 액세스할 수 있어 수술 시간과 마취 노출을 줄일 수 있습니다. 병원은 재원일수의 단축과 환자 만족도의 향상을 이유로 보험사와의 협상력을 높이고 있습니다. 한편, 밀링 가공에서는 불가능한 격자 형상의 인필이나 두께 가변의 벽이 일상적인 것이 되어 경량화와 생체역학적 스트레스 경로의 최적화를 실현합니다. 인공지능과 자체 제조 프린터를 결합한 공급업체는 경쟁적 해자를 넓히고 있지만, 기존의 기계 공장은 상품화 위험에 직면 해 있습니다.

신흥국에서 뇌신경 외과 인프라 확대

중국의 헬스케어 개혁에서는 2030년까지 1조 4,000억 달러를 Tier2 도시의 외상 허브를 포함한 새로운 시설로 채울 것으로 예상됩니다. 인도의 국가 의료기기 정책은 연간 15% 성장을 목표로 임플란트의 현지 생산을 위한 합작 사업을 장려하고 있습니다. 수술 중 이미지가 시중 병원에도 보급되어 외과의사가 경력 초기에 고급 두개 성형술을 채용하게 됩니다. 동남아시아에서는 민간의료보험이 점차 확대되고 비용 장벽이 더욱 완화되고 두개 임플란트 시장은 대도시 중심부 이외에도 퍼지고 있습니다.

부문 분석

티타늄은 2024년에 두개 임플란트 시장 점유율의 52.76%를 차지했으며, 임상적 수용이 정착되어 있음을 뒷받침했습니다. 이 부문은 외과 의사가 익숙하고 기계적 강도 대 중량비가 양호하다는 장점이 있습니다. 그러나 PEEK는 가장 급속히 확대되고 있는 재료이며 방사선과 의사가 그 이미지의 선명도를 선호하기 때문에 CAGR 7.35%를 나타낼 전망입니다. 수익 측면에서 두개 임플란트 시장 규모에서 차지하는 PEEK의 비율은 FDA가 승인한 환자별 솔루션에 힘입어 2030년까지 꾸준히 확대될 것으로 예측됩니다.

PEEK 쉘에 티타늄 메쉬를 내장하는 하이브리드 구조는 방사선 투과성을 유지하면서 응력 차폐를 완화하고 완전 폴리머 임플란트를 경원하는 외과의에게 중간 경로를 제공합니다. PMMA는 단가가 싸기 때문에 저자원 환경에서는 틈새 시장을 유지하는 반면, 재흡수성 폴리머는 임플란트 후에도 두개골의 성장이 계속되는 소아 사례에서 관심을 끌고 있습니다. 첨단 표면 텍스처링 기술과 플라즈마 코팅 기술은 모든 재료에서 뼈 형성을 개선하고, 성능 차이를 모호하게 하며, 두개 임플란트 시장에서 경쟁을 강화할 수 있습니다.

지역 분석

북미는 2024년 매출의 41.23%를 차지하며, 메디케어의 적용과 하이엔드 화상처리 시스템의 설치 베이스가 이를 지원했습니다. 메이요 클리닉과 존스 홉킨스 등의 학술 거점은 혁신의 인큐베이터로서도 기능하고 있으며, 두개 성형술에서 증강현실 내비게이션의 조기 채용을 가속화하고 있습니다. 그럼에도 불구하고 지불자의 압력이 높아짐에 따라 목록 가격 인플레이션이 억제되고 공급업체는 재수술률의 감소를 입증함으로써 비용이 많이 드는 수수료 설정을 정당화해야 할 필요가 없습니다.

아시아태평양은 CAGR 8.75%를 나타내 가장 급성장하는 지역으로 중국과 인도에서 수십억 달러 규모의 공적 병원 건설이 뒷받침되고 있습니다. 합리화된 기기 승인 경로와 현지 생산에 대한 우대 조치로 다국적 기업과 국내 진출기업 모두 시장 투입까지의 시간이 단축됩니다. 일본과 한국은 수술용 로봇의 보급을 선도하고 임플란트의 정확한 적합과 합병증 발생률의 저하라는 호순환을 촉진하고 있습니다. 가구소득의 상승과 민간보험의 이용가능 범위의 확대로 선택적 두개성형술이 보다 가까워지고, 두개 임플란트 시장의 기세가 지속되고 있습니다.

유럽은 의료기기 규제가 컴플라이언스 비용을 인상하고 있기 때문에 꾸준하지만 성장은 둔화하고 있습니다. 독일과 프랑스는 증거 기반 조달을 선도하고 판매자에게 장기적인 결과 데이터를 제출하도록 의무화하고 있습니다. 의료기록의 디지털화가 진행되고 있는 북유럽 국가들은 단일 지불제도로 국가 규모에서 실제 가치를 평가할 수 있기 때문에 환자 고유의 임플란트를 신속하게 채용하고 있습니다. 중동 및 걸프 국가에서는 의료 관광 프로그램이 고급 임플란트 수요를 지원합니다. 이러한 지역적 차이를 종합하면 두개 임플란트 시장에서 활약하는 기업에게는 각 지역에 맞는 시장 전략이 요구됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 머리부상과 신경외과 수술 증가

- 환자 전용 임플란트를 위한 3D 프린팅의 진보

- 티타늄제 및 PEEK제 임플란트의 뛰어난 임상 성적

- 신흥국의 신경 외과 인프라 확대

- 증강현실을 이용한 임플란트의 위치결정 지원(과소보고)

- 군용 신경보호의 연구개발이 바이오세라믹의 채용을 뒷받침(과소보고)

- 시장 성장 억제요인

- 특주 임플란트의 고비용과 한정된 상환액

- 임플란트 제거로 이어지는 수술 후 감염

- 생체 흡수성 비계 재료에 관한 규제의 모호함(과소보고)

- 의료급 PEEK 수지공급 체인 리스크(과소보고)

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 진입자의 위협

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 재료별

- 티타늄

- 폴리에테르에테르케톤(PEEK)

- 폴리메틸메타크릴레이트(PMMA)

- 하이드록시아파타이트

- 기타 재료

- 기술별

- 3D 프린팅 임플란트

- CAD/CAM 밀링 임플란트

- 기존 가공 임플란트

- 최종 사용자별

- 병원

- 전문 신경외과 센터

- 외래 수술 센터(ASC)

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Stryker Corporation

- Zimmer Biomet Holdings Inc.

- DePuy Synthes(Johnson & Johnson)

- Integra LifeSciences Holdings

- Medtronic plc

- KLS Martin Group

- Xilloc Medical BV

- OssDsign AB

- Renishaw plc

- B. Braun(Aesculap)

- Anatomics Pty Ltd

- Tecomet Inc.

- Synimed

- OsteoMed(An Acumed Company)

- Evonik Industries AG

- CranioTech Inc.

- ADEOR medical AG

제7장 시장 기회와 전망

KTH 25.10.29The cranial implants market stands at USD 1.40 billion in 2025 and is projected to expand to USD 1.91 billion by 2030, advancing at a 6.5% CAGR.

Robust demand stems from a steady rise in traumatic brain injuries, broader neurosurgical capacity in emerging economies, and a decisive shift toward 3-dimensional patient-specific manufacturing. Hospitals remain the anchor customer base, yet specialty neurosurgery centers are scaling rapidly as payers reward high-outcome facilities. Titanium retains primacy because of decades of clinical proof, but polymeric alternatives such as PEEK gain traction as surgeons prioritize artifact-free imaging. Technology adoption also pivots: conventional machining still fills high-volume needs, yet 3-D printed solutions are winning complex cases because they reduce operative time and revision risk. Regionally, North America leads revenue, while Asia-Pacific generates the fastest growth on the back of infrastructure build-outs and regulatory modernization that shorten device-approval cycles.

Global Cranial Implants Market Trends and Insights

Rising Incidence of Cranial Trauma & Neurosurgical Procedures

Worldwide, roughly 69 million traumatic brain injuries occur each year, and severe cases often necessitate cranioplasty reconstruction. Aging populations, higher motor-vehicle density, and organized sports elevate the clinical burden. Defense research into neuro-protection further amplifies demand as military surgeons require dependable synthetic plates for battlefield injuries. At the hospital level, dedicated neuro-trauma centers consolidate complex cases, creating predictable procurement cycles for high-volume suppliers. Because trauma incidence is weakly correlated with economic cycles, the cranial implants market enjoys defensive-healthcare status that supports long-term planning by manufacturers and health systems alike.

Advancements in 3-D Printing for Patient-Specific Implants

Additive manufacturing transforms a one-size-fits-all procedure into tailored reconstruction. The 2024 FDA clearance of 3D Systems' PEEK cranial plate proved the regulatory viability of polymeric additive implants. Surgeons now access cloud-based design tools that convert CT data into a ready-to-print file in minutes, trimming operating time and anesthesia exposure. Hospitals gain negotiating leverage with insurers by citing shorter length of stay and higher patient-satisfaction indices. Meanwhile, lattice infills and variable-thickness walls impossible in milling become routine, lowering weight and optimizing biomechanical stress paths. Suppliers that combine artificial intelligence with in-house printers are building widening competitive moats while legacy machine shops face commoditization risk.

Expanding Neurosurgical Infrastructure in Emerging Economies

China's healthcare reform earmarks USD 1.4 trillion through 2030 for new facilities, including trauma hubs in tier-2 cities National Health Commission of China. India's National Medical Devices Policy targets 15% annual growth and encourages joint ventures for localized implant production Government of India. As intraoperative imaging reaches community hospitals, surgeons adopt advanced cranioplasty techniques earlier in their careers. Gradual expansion of private health insurance in Southeast Asia further softens cost barriers, broadening the cranial implants market beyond major metropolitan centers.

Other drivers and restraints analyzed in the detailed report include:

- Superior Clinical Outcomes of Titanium & PEEK Implants

- High Cost & Limited Reimbursement for Customized Implants

- Post-Operative Infection Leading to Implant Removal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Titanium held 52.76% of cranial implants market share in 2024, underscoring its entrenched clinical acceptance. The segment benefits from abundant surgeon familiarity and favorable mechanical strength-to-weight ratios. PEEK, however, is the fastest-expanding material, advancing at a 7.35% CAGR as radiologists favor its imaging clarity. In revenue terms, PEEK's portion of the cranial implants market size is forecast to widen steadily through 2030, propelled by FDA-cleared patient-specific solutions.

Hybrid constructs that embed titanium meshes inside PEEK shells mitigate stress shielding while preserving radiolucency, offering a middle path for surgeons wary of fully polymer implants. PMMA retains a niche in low-resource settings because of low unit cost, while resorbable polymers gather interest for pediatric cases where skull growth continues post-implantation. Advanced surface texturing and plasma coating technologies are improving bone ingrowth across all materials, potentially blurring performance gaps and intensifying competition within the cranial implants market.

The Cranial Implants Market Report is Segmented by Material (Titanium, Polyether-Ether-Ketone (PEEK) and More), by Technology (3-D Printed Implants, CAD/CAM-Milled Implants and More), by End-User (Hospitals, Specialty Neurosurgery Centers and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Report Offers the Value (in USD) for the Above Segments.

Geography Analysis

North America generated 41.23% of 2024 revenue, anchored by Medicare coverage and an installed base of high-end imaging systems. Academic hubs such as Mayo Clinic and Johns Hopkins also function as innovation incubators, accelerating early adoption of augmented-reality navigation during cranioplasty procedures. Nevertheless, mounting payer pressure keeps list-price inflation in check, compelling suppliers to justify premium tariffs with demonstrable reductions in revision rates.

Asia-Pacific is the fastest-growing region at an 8.75% CAGR, propelled by multibillion-dollar public-hospital buildouts in China and India. Streamlined device-approval pathways and incentives for local production shorten time to market for both multinationals and domestic entrants. Japan and South Korea lead surgical robotics penetration, fostering a virtuous cycle of precise implant fit and lower complication rates. Rising household incomes and broader private-insurance availability make elective cranioplasty more accessible, sustaining momentum in the cranial implants market.

Europe exhibits steady but slower growth as the Medical Device Regulation raises compliance costs. Germany and France spearhead evidence-based procurement, obliging sellers to produce longitudinal outcome data. Nordic countries, which have digitized health records extensively, adopt patient-specific implants quickly because their single-payer systems can evaluate real-world value at national scale. In the Middle East and Gulf states, medical-tourism programs underpin premium implant demand, while African markets remain nascent but benefit from international trauma-care initiatives. Collectively, these regional nuances demand tailored go-to-market strategies from companies active in the cranial implants market.

- Stryker

- Zimmer Biomet

- Johnson & Johnson

- Integra LifeSciences Holdings

- Medtronic

- KLS Martin Group

- Xilloc Medical B.V.

- OssDsign AB

- Renishaw plc

- B. Braun (Aesculap)

- Anatomics

- Tecomet Inc.

- Synimed

- OsteoMed (An Acumed Company)

- Evonik Industries

- CranioTech Inc.

- ADEOR medical AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of cranial trauma & neurosurgical procedures

- 4.2.2 Advancements in 3-D printing for patient-specific implants

- 4.2.3 Superior clinical outcomes of titanium & PEEK implants

- 4.2.4 Expanding neurosurgical infrastructure in emerging economies

- 4.2.5 Augmented-reality assisted implant positioning (under-reported)

- 4.2.6 Military neuro-protection R&D boosting bioceramic adoption (under-reported)

- 4.3 Market Restraints

- 4.3.1 High cost & limited reimbursement for customized implants

- 4.3.2 Post-operative infection leading to implant removal

- 4.3.3 Regulatory ambiguity for bio-resorbable scaffold materials (under-reported)

- 4.3.4 Supply-chain risk for medical-grade PEEK resin (under-reported)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Material (Value, USD Million)

- 5.1.1 Titanium

- 5.1.2 Polyether-ether-ketone (PEEK)

- 5.1.3 Polymethyl-methacrylate (PMMA)

- 5.1.4 Hydroxy-apatite

- 5.1.5 Other Materials

- 5.2 By Technology (Value, USD Million)

- 5.2.1 3-D Printed Implants

- 5.2.2 CAD/CAM-Milled Implants

- 5.2.3 Conventional Machined Implants

- 5.3 By End User (Value, USD Million)

- 5.3.1 Hospitals

- 5.3.2 Specialty Neurosurgery Centers

- 5.3.3 Ambulatory Surgical Centers

- 5.4 By Geography (Value, USD Million)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Stryker Corporation

- 6.3.2 Zimmer Biomet Holdings Inc.

- 6.3.3 DePuy Synthes (Johnson & Johnson)

- 6.3.4 Integra LifeSciences Holdings

- 6.3.5 Medtronic plc

- 6.3.6 KLS Martin Group

- 6.3.7 Xilloc Medical B.V.

- 6.3.8 OssDsign AB

- 6.3.9 Renishaw plc

- 6.3.10 B. Braun (Aesculap)

- 6.3.11 Anatomics Pty Ltd

- 6.3.12 Tecomet Inc.

- 6.3.13 Synimed

- 6.3.14 OsteoMed (An Acumed Company)

- 6.3.15 Evonik Industries AG

- 6.3.16 CranioTech Inc.

- 6.3.17 ADEOR medical AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment