|

시장보고서

상품코드

1842610

혈액 가온기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Blood Warmer Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

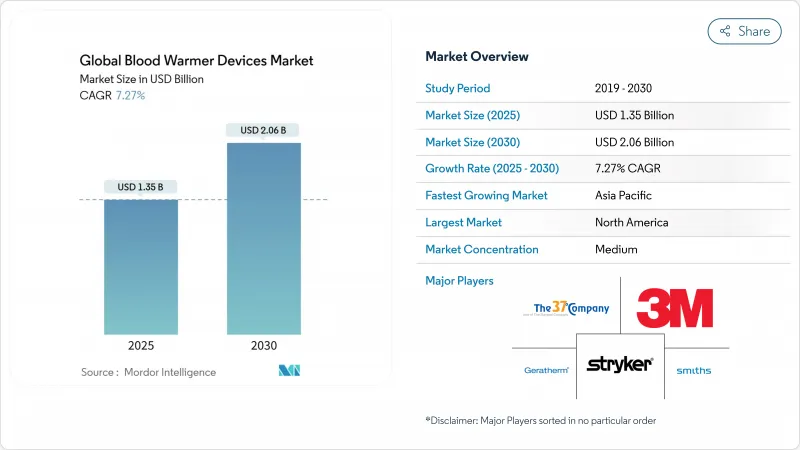

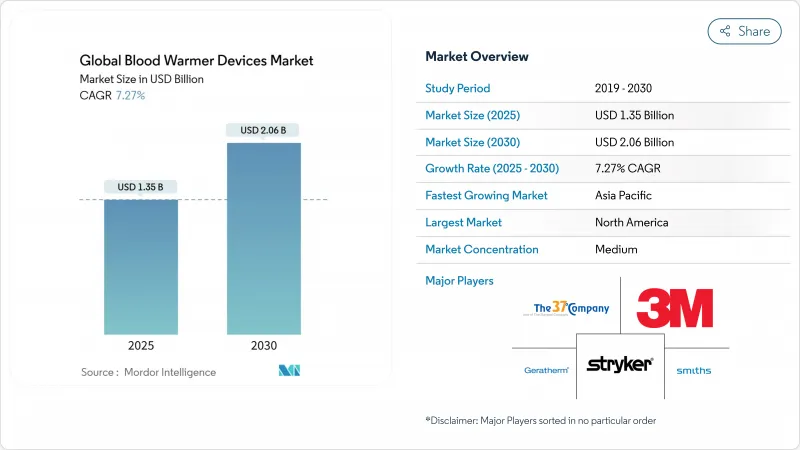

혈액 가온기 시장은 2025년에 13억 5,000만 달러, 2030년에는 20억 6,000만 달러에 달하며, CAGR 7.27%를 나타낼 전망입니다.

이 기세는 외과 수술과 외상 환자의 항온화 추진, 외상 처치 건수 증가, 휴대형 시스템의 급속한 군사적 보급에 의한 것입니다. 2025년 3월에 수술기 등록 간호사 협회(Association of PeriOperative Registered Nurses)가 발표한 지속적 가온의 의무화는 병원의 컴플라이언스에 대한 대처를 강화하고 의료기기공급망의 회복력에 관한 최근의 FDA 지침은 제품의 중단 없는 가용성에 초점을 맞춥니다. 제조업체 각사는 통합 IoT 로깅, 배터리 수명 연장, 전장 사양의 견고화 등의 기능으로 대응해, 방위 및 응급 의료 서비스(EMS)의 바이어로부터 새로운 계약을 획득하고 있습니다.

세계의 혈액 가온기 시장 동향과 인사이트

외상·구급 수술 건수 증가

교통사고, 고령화, 분쟁지역의 장기화 등으로 세계의 외상환자 수는 증가의 길을 따라가고 있습니다. 미국의 합동 외상 시스템에서 자동 혈액 온난화 물류가 표준으로 실행되면 전장에서 사망이 44% 감소했습니다. 응급실 연구에 따르면 병원 전 수혈 프로그램은 연간 90만 명의 미국 환자에게 혜택을 줄 수 있으며 저체온증과 관련된 사망을 피하는 신뢰할 수 있는 가온기의 필요성을 강조합니다. 대량 수혈 프로토콜에 가온 요건이 포함되어 혈액 가온기 시장은 병원의 외상 케어 예산의 중심적인 존재가 되고 있습니다.

엄격한 수술기 상온 치료 지침

갱신된 AORN 가이드라인은 도입 전부터 회복까지 지속적인 가온을 의무화하고 있으며, 이에 따르지 않는 시설은 법적 책임을 질 수 있습니다. 2024년 3월에 발표된 FDA의 테스트 프로토콜은 온열 효과 평가를 표준화하고 자동 셧오프와 -0.1℃의 정확도를 가진 시스템 조달을 가속화합니다. 임상적 증거에 의하면, 미수정의 주술기 저체온증은 합병증 발생률을 9% 상승시켜, 급성 신장해를 14% 증가시키는 것으로 되어, 병원이 최첨단의 기기를 도입하는 동기부여가 되고 있습니다.

용혈 및 단백질 변성의 위험

46℃를 초과하면 적혈구가 파열되고 단백질은 2시간 노출 후 43℃에서 변성되기 시작합니다. 조사된 백혈구를 60℃로 따뜻하게 한 유닛을 사용한 시험에서는 급격한 칼륨 방출이 기록되어 신생아의 심정지 위험이 상승했습니다. 장비 제조업체는 현재 트리플 센서, 자동 바이패스, 즉각적인 셧오프를 포함하고 있으며, 이들은 비용 및 검증 장애물을 높이지만 환자의 안전에 필수적입니다.

부문 분석

정맥내 인라인 시스템은 2024년 매출의 40.65%를 차지하며 혈액 가온기 시장이 원활한 통합과 엄격한 온도 관리를 선호한다는 것을 보여주었습니다. 3M Ranger 245와 같은 장치는 45초 내에 세트 포인트에 도달하고 37°C와 41°C 사이의 동시 주입을 관리하므로 수술실 및 외상실 프로토콜에 이상적입니다. 서피스 워머는 절대적인 매출에서는 틈새이지만, 구급차나 항공기 내에서 전개 가능한 유연한 랩 패드를 중시하는 구급대원에 의해 밀려, CAGR은 8.23%를 나타내 성장을 지속하고 있습니다.

임상적 증거는 인라인 모델이 왜 주류인지를 뒷받침합니다. 비교 시험에서는 47℃에서 1시간 가온한 신선혈에는 세포 손상이 보이지 않았지만, 침지조에서는 보다 큰 편차가 보였습니다. Sarstedt사의 SAHARA-III와 같은 캐비닛형 장치는 물 침지 없이 대량 처리를 필요로 하는 혈액은행에서 여전히 이용되고 있지만, 성장은 POC(Point-of-Care)에 사용하기에 적합한 보다 작고 민첩한 장치로 이행하고 있습니다.

지역 분석

북미는 2024년 매출의 45.23%를 차지했고, 이는 성숙한 상환, FDA의 엄격한 감독, 23개 주에서 이미 온보드에서 혈액을 운반하고 있는 자금 풍부한 EMS 네트워크를 반영하고 있습니다. 2025년부터 2026년까지 메디케어 결제 갱신은 정상 체온 준수와 관련된 품질 인센티브를 높여 새로운 병원 업그레이드를 촉진합니다. 사망률을 44% 감소시킨 자동 전장 외상 시스템과 같은 국방부의 기술 혁신은 민간 의료에도 파급되어 업스트림 수요를 지지하고 있습니다.

유럽에서는 의료기기 규제의 조화와 집중치료학회 가이드라인이 온도관리기준을 강화하여 균형 잡힌 확대를 보이고 있습니다. 독일, 프랑스, 영국의 주요 센터에서 채택된 외상성 뇌 손상의 표적 온도 관리에 대한 컨센서스는 지역의 지정학적 긴장에 가장자리를 둔 공급망 마찰에도 불구하고 안정적인 조달 흐름을 보장합니다.

아시아태평양은 중국, 인도, 동남아시아에서 엄청난 외상 사례와 정부 인프라 계획에 힘입어 10.23%로 가장 빠른 복합 성장을 달성했습니다. 벤처기업에 의한 자금조달이 감소하고, 현지 신흥기업이 뻗어나가는 한편, 자연재해에 대응한 후 전장 레벨의 기기를 국가가 조달하는 것으로, 채용 곡선은 급경사를 유지하고 있습니다. 가격에 민감한 공립 병원에서는 보다 저가의 휴대용 유닛을 시험하는 케이스가 늘어나고 있어 정확도를 떨어뜨리지 않고 제품 라인 업을 충실시킬 수 있는 제조업체에, 새로운 길이 열리고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 외상 및 긴급 수술 건수 증가

- 엄격한 주술기 정상체온 가이드라인

- 군 및 응급 의료에 있어서의 휴대형 배터리식 카이로의 채용

- 컴플라이언스를 위한 IoT 온도 로깅 통합

- AI에 의한 실시간 관류 모니터링(언더 더 레이더)

- 대량의 가온을 필요로 하는 줄기세포·아페레시스 요법의 성장(언더 더 레이더)

- 시장 성장 억제요인

- 생리적 온도 이상에서의 용혈과 단백질 변성의 위험

- LMIC 병원의 자본 비용 감도

- 브랜드 간 호환성이 없는 일회용 세트(언더 더 레이더)

- 발열체 희토류공급 체인 취약성(언더 더 레이더)

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 진입자의 위협

- 공급자의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 유형별

- 정맥 내 라인

- 표면/대류식 유체

- 인클로저 캐비닛 워머

- 모달리티별

- 휴대용

- 고정식

- 용도별

- 수술 및 수술 전후 관리

- 중환자 치료(ICU/ER)

- 혈액은행 및 채혈센터

- 군 및 응급의료 서비스(EMS) 사용

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- 3M Company

- Stryker Corporation(벨몬트)

- ICU Medical Inc.(Smiths Medical)

- Barkey GmbH & Co. KG

- Belmont Medical Technologies

- Fresenius SE & Co. KGaA

- GE HealthCare Technologies Inc.

- Gentherm Medical

- Vyaire Medical Inc.

- Princeton Medical Scientific Inc.

- Emit Corporation

- The 37Company BV

- SOMATEX Medical Technologies GmbH

- Keewell Medical Technology Co. Ltd.

- Qingdao Flux Medical

- ThermoGenesis Holdings Inc.

- Sarstedt AG & Co. KG

- Smiths Group plc

- Inspiration Healthcare Group plc

- Enthermics Medical Systems

제7장 시장 기회와 전망

KTH 25.10.29The blood warmer devices market stands at USD 1.35 billion in 2025 and is set to reach USD 2.06 billion by 2030, advancing at a 7.27% CAGR.

Strong momentum comes from the push to keep surgical and trauma patients normothermic, escalating trauma procedure volumes, and rapid military uptake of portable systems. Continuous-warming mandates issued by the Association of periOperative Registered Nurses in March 2025 have heightened hospital compliance efforts, while recent FDA guidance on medical-device supply-chain resilience has sharpened focus on uninterrupted product availability. Manufacturers respond with integrated IoT logging, battery life extensions, and battlefield-grade ruggedisation-features that win new contracts from defense and emergency-medical service (EMS) buyers.

Global Blood Warmer Devices Market Trends and Insights

Rising Trauma & Emergency Surgery Volumes

Global trauma caseloads keep climbing, driven by road accidents, ageing populations and prolonged conflict zones. The U.S. Joint Trauma System recorded a 44% drop in battlefield deaths once automated blood-warming logistics became standard practice health.mil. Emergency-department studies show prehospital transfusion programs could benefit as many as 900,000 U.S. patients annually, underscoring the need for reliable warmers that avert hypothermia-related mortality. Mass-transfusion protocols now embed warming requirements, making the blood warmer devices market central to hospital trauma-care budgets.

Stringent Peri-operative Normothermia Guidelines

Updated AORN guidelines mandate continuous warming from pre-induction through recovery, threatening legal exposure for facilities that fail to comply. Complementary FDA test-protocols released in March 2024 standardise thermal-effect evaluation, accelerating procurement of systems with automatic shut-off and +-0.1 °C accuracy. Clinical evidence ties uncorrected peri-operative hypothermia to 9% higher complication rates and a 14% lift in acute kidney injury, further motivating hospitals to deploy state-of-the-art devices.

Risk of Hemolysis & Protein Denaturation

Temperatures exceeding 46 °C cause measurable red-cell rupture, while proteins begin denaturing at 43 °C after two-hour exposure. Trials on irradiated leukoreduced units warmed to 60 °C recorded sharp potassium release, elevating cardiac-arrest risk in neonates. Device makers now integrate triple sensors, automatic bypass and instant shut-off, which add cost and raise validation hurdles but are essential for patient safety.

Other drivers and restraints analyzed in the detailed report include:

- Adoption of Portable Warmers in Military & EMS

- Integration of IoT Temperature Logging for Compliance

- Capital-Cost Sensitivity in LMIC Hospitals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intravenous in-line systems controlled 40.65% of 2024 revenue, demonstrating the blood warmer devices market preference for seamless integration and tight temperature control. Units such as 3M's Ranger 245 reach set-point in 45 seconds and manage concurrent infusions between 37 °C and 41 °C, making them the workhorse for operating-theatre and trauma-bay protocols. Surface warmers, although niche in absolute sales, register an 8.23% CAGR, propelled by EMS crews that value flexible wrapping pads deployable inside ambulances or aircraft.

Clinical evidence underlines why in-line models dominate. Comparative trials show fresh blood warmed at 47 °C for one hour displayed no cell damage, whereas immersion baths showed higher variability. Cabinet units such as Sarstedt's SAHARA-III still serve blood banks needing large-volume processing without water immersion, yet growth pivots to smaller, agile devices for point-of-care use.

The Blood Warmer Devices Market is Segmented by Product Type (Intravenous In-Line, Surface/Convective Fluid and More), by Modality (Portable and Stationary), by Application (Surgery & Peri-Operative Care, Critical Care (ICU/ER) and More) and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led with 45.23% of 2024 revenue, reflecting mature reimbursement, stringent FDA oversight and a well-funded EMS network that already fields blood on board in 23 states. Medicare payment updates for 2025-2026 increase quality incentives tied to normothermia compliance, driving new hospital upgrades federalregister.gov. Pentagon innovations such as the Automated Battlefield Trauma System, which delivered a 44% mortality reduction, spill over into civilian care and sustain upstream demand.

Europe shows balanced expansion as harmonised Medical Device Regulation and intensive-care society guidelines reinforce thermal-management standards. Consensus on targeted temperature control for traumatic brain injury, adopted by leading centres in Germany, France and the United Kingdom, secures a steady cadence of procurement despite supply-chain frictions triggered by regional geopolitical tensions

Asia-Pacific delivers the fastest compound growth at 10.23%, propelled by massive trauma caseloads and government infrastructure programmes in China, India and Southeast Asia. While venture funding dips curtailed some local start-ups, state procurement of battlefield-grade equipment after natural-disaster responses keeps the adoption curve steep. Price-sensitive public hospitals increasingly trial lower-cost portable units, opening new avenues for manufacturers that can tier offerings without diluting accuracy.

- 3M

- Stryker Corporation (Belmont)

- ICU Medical

- Barkey

- Belmont Medical Technologies

- Fresenius

- GE HealthCare Technologies Inc.

- Gentherm Medical

- Vyaire Medical

- Princeton Medical Scientific Inc.

- Emit Corporation

- The 37Company B.V.

- SOMATEX Medical Technologies GmbH

- Keewell Medical Technology Co. Ltd.

- Qingdao Flux Medical

- ThermoGenesis Holdings Inc.

- Sarstedt

- Smiths Group

- Inspiration Healthcare Group plc

- Enthermics Medical Systems

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising trauma & emergency surgery volumes

- 4.2.2 Stringent peri-operative normothermia guidelines

- 4.2.3 Adoption of portable, battery-operated warmers in military & EMS

- 4.2.4 Integration of IoT temperature logging for compliance

- 4.2.5 AI-assisted real-time perfusion monitoring (under-the-radar)

- 4.2.6 Stem-cell & apheresis therapy growth needing large-volume warming (under-the-radar)

- 4.3 Market Restraints

- 4.3.1 Risk of hemolysis & protein denaturation at supra-physiologic temps

- 4.3.2 Capital cost sensitivity in LMIC hospitals

- 4.3.3 Disposable set incompatibility across brands (under-the-radar)

- 4.3.4 Supply-chain fragility for heating elements rare-earths (under-the-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 by Product Type (Value)

- 5.1.1 Intravenous In-Line

- 5.1.2 Surface/Convective Fluid

- 5.1.3 Enclosure Cabinet Warmers

- 5.2 by Modality (Value)

- 5.2.1 Portable

- 5.2.2 Stationary

- 5.3 by Application (Value)

- 5.3.1 Surgery & Peri-operative Care

- 5.3.2 Critical Care (ICU/ER)

- 5.3.3 Blood Banks & Apheresis Centers

- 5.3.4 Military & EMS Use

- 5.4 Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 3M Company

- 6.3.2 Stryker Corporation (Belmont)

- 6.3.3 ICU Medical Inc. (Smiths Medical)

- 6.3.4 Barkey GmbH & Co. KG

- 6.3.5 Belmont Medical Technologies

- 6.3.6 Fresenius SE & Co. KGaA

- 6.3.7 GE HealthCare Technologies Inc.

- 6.3.8 Gentherm Medical

- 6.3.9 Vyaire Medical Inc.

- 6.3.10 Princeton Medical Scientific Inc.

- 6.3.11 Emit Corporation

- 6.3.12 The 37Company B.V.

- 6.3.13 SOMATEX Medical Technologies GmbH

- 6.3.14 Keewell Medical Technology Co. Ltd.

- 6.3.15 Qingdao Flux Medical

- 6.3.16 ThermoGenesis Holdings Inc.

- 6.3.17 Sarstedt AG & Co. KG

- 6.3.18 Smiths Group plc

- 6.3.19 Inspiration Healthcare Group plc

- 6.3.20 Enthermics Medical Systems

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment