|

시장보고서

상품코드

1842616

마이크로서지컬 기구 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Microsurgical Instruments - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

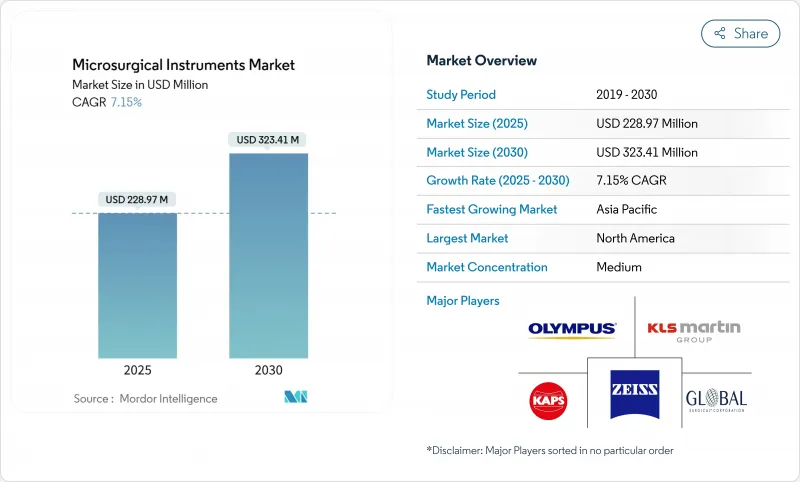

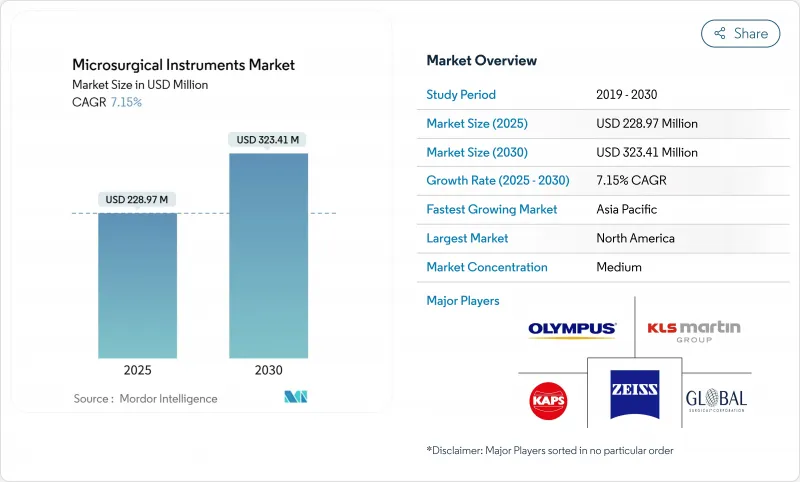

세계의 마이크로서지컬 기구 시장은 2025년 2억 2,897만 달러로 평가되고, 2030년에는 3억 2,341만 달러로 확대될 것으로 예측됩니다.

정밀 기반 수술 절차의 보급, 4K/3D 디지털 현미경의 급속한 통합, 만성 질환 관련 개입 건수 증가가 고도로 전문화된 기구 수요를 계속 확대하고 있습니다. 병원과 교육센터는 AI 대응 수술용 현미경으로 설비기기의 갱신을 계속하고 외래 수술 센터는 복잡한 사례를 외래로 이행하기 위해 컴팩트하고 워크플로우 중시의 세트에 경주하고 있습니다. 경쟁이 심한 분야에서는 인체공학적 설계, 생체흡수성 미세봉합재료, 음성제어 시각화 유닛 등 제품차별화를 위한 연구개발비가 계획적으로 투입되고 있습니다. 하지만 제조업체는 엄격한 Class III 승인 경로를 철회해야 하기 때문에 혁신 추세를 지속하려면 규제 당국과의 조기 협력 및 의료 제공업체와의 위험 분담이 필수적입니다.

세계의 마이크로서지컬 기구 시장 동향과 인사이트

전통적인 수술에 대한 마이크로서지컬의 이점

밀리미터 이하의 정밀도가 합병증 발생률의 감소와 회복의 속도로 이어진다는 임상 증거가 제시되어 있으며, 마이크로서지컬 기구 시장은 지속적인 보급이 기대되고 있습니다. ETcath 로봇 플랫폼은 0.1mm의 정확도로 병변을 확인하고 수동 한계를 넘어 자본 구매의 경제적 근거를 강화하고 있습니다. 플루트와 같은 멀티태스킹 장비는 3대의 장비를 1대로 대체할 수 있어 설치 시간과 수술실의 혼잡을 줄일 수 있습니다. 병원은 이러한 성과를 활용하여 유리한 진료 보상을 협상함으로써 교체 사이클을 가속화하고 있습니다. 전문 클리닉은 표준 기술에서는 재현이 어려운 기능적·미학적 결과를 개선하기 위해 마이크로 서저리에 의한 재건을 적용하고 있습니다. 보험사가 가치 기반 지표로 상환을 하는 동안 유해 사건의 감소를 증명하는 기기 벤더는 신규 입찰 시에 우위를 차지할 수 있습니다.

수술 건수 증가와 만성 질환 이환율

인구의 고령화와 세계적인 당뇨병 이환율은 수술 건수 증가를 뒷받침해, 마이크로서지컬 기구 시장의 다년간에 걸친 성장을 확실히 하고 있습니다. 2060년까지 33조 4,000억 달러에 달하는 중국의 의료비 전망은 3차 의료 센터 전체에서 대규모 장비 풀을 시사하고 있습니다. 당뇨병성 망막증이 망막 마이크로서젤리의 높은 기본 수준을 견인하는 한편, 관상동맥 우회와 종양 절제술은 레거시 도구로는 실현할 수 없는 신경을 온존하는 정밀도가 요구됩니다. 아시아의 각국 정부는 안과용 및 심장혈관용 기기에 조달예산을 할당해 매력적인 일괄구입 기회를 창출하고 있습니다. 구미 시스템은 성숙하다고는 해도, 재수술이나 평균 수명의 연장에 의해 성장을 계속하고 있습니다. 기기 제조업체는 현미경, 집게, 생체 흡수성 봉합사를 번들한 스타터 키트를 조정하는 것으로, 중견 시설에서의 도입 마찰을 줄임으로써 대응하고 있습니다.

고급 마이크로서지컬 시스템의 고비용

프리미엄 로봇 현미경의 정가는 100만 달러를 넘어, 유지관리 계약이나 멸균 소모품은 10년간의 소유 비용을 배증시킵니다. 신흥 시장 병원은 제한된 자본을 필요로 하는 필수적인 영상 진단과 ICU 침대에 휘두르고, 마이크로 서저리 업그레이드는 늘어나고 있습니다. 또, 북미의 소규모 지역 병원에서는 풀 장비의 스위트에 손을 내기 전에, 대수의 임계치를 검토해, 대신에 한정된 기능 밖에 없는 개장 끝난 유닛을 선택합니다. 벤더는 사용량에 따른 종량제 리스, 이익 분배 모델, 코어 광학계로 시작하여 나중에 로봇 암을 추가하는 모듈식 구축 등으로 스티커 쇼크에 대항하고 있습니다. 의료의 질 목표에 연동된 정부 조달 보조금은 설비 투자의 장벽을 부분적으로 상쇄하지만, 보다 저비용의 수동 세트와 동등하게 되기 위해서는 추가의 사이클이 필요할지도 모릅니다.

부문 분석

수술용 현미경은 4K 시각화, 증강현실 오버레이, AI 가이드가 있는 자동 초점의 지속적인 투입에 힘입어 2024년에는 29.52%의 압도적인 현미경 시장 점유율을 유지했습니다. 이 부문은 2025년에 마이크로서지컬 기구 시장 규모의 6,700만 달러를 획득하며, 신경외과 의사와 안과 의사가 로봇 호환 광학 제품군을 채택함에 따라 꾸준히 확대될 것으로 보입니다. 또한 이비인후과 의사와 성형 외과 의사가 하이브리드 수술실 내에서 현미경을 공유함으로써 이용률과 교환 빈도가 높아집니다.

생체 흡수성 폴리머가 이물질 반응을 억제하는 마이크로 봉합사는 CAGR 9.25%를 나타내 특히 신경 이식이나 혈관 문합의 경우에 견디는 기세입니다. 마이크로 포셉과 마이크로니들 홀더는 티타늄으로 만들어진 햅틱 기능을 강화한 그립으로 6시간에 걸쳐 재건 수술 중 손의 피로를 줄여줍니다. 게다가, 마이크로 시저스와 마이크로 혈관 클램프는 1,000회의 멸균 사이클 후에도 예리함을 유지하는 다이아몬드 라이크 코팅이 적용되며, 특수 리트랙터는 소아 마이크로서지컬의 좁은 해부학적 통로에 대응합니다. 이러한 진보는 소모품, 서비스 계약 및 소프트웨어 업그레이드의 경상적인 수익원을 강화하고 공급업체에게 기구 카테고리 간의 균형 잡힌 성장을 가져옵니다.

지역 분석

북미는 2024년 매출의 38.82%를 차지했으며 OR의 디지털화 정착과 고액의 시각화 플랫폼을 커버하는 유리한 상환에 지지되었습니다. 클리블랜드 클리닉의 광학 기기 제조업체와의 제휴와 같은 지역 교육 제휴는 증강현실 지침을 시험적으로 실시하여 관련 병원 전체의 조달 경로에 직접 반영합니다. ASC는 현재 힘줄 수복의 60% 이상을 실시하고 있으며 소형 현미경과 일회용 봉합사 카트리지의 교체 수요를 확보하고 있습니다. 마이크로서지컬 기구 시장은 재입원률 저하로 비싼 기기비용을 상쇄하는 보너스 지불이 확보되는 가치 기반 계약으로 가격 결정력을 유지하고 있습니다.

유럽은 독일, 프랑스, 북유럽 국가에서의 도입이 호조로, 여전히 2위의 구매자 시장입니다. 이 지역에서는 엄격한 외과의 자격증과 라이프사이클 비용을 우선시하는 집중 입찰 프레임워크가 공급업체에게 보증 기간 연장 및 예보 보전 패키지를 제공하도록 촉구하고 있습니다. EU MDR 준수 비용은 신규 진입 장벽을 높이고 간접적으로 기존 기업의 점유율을 보호하고 있습니다. 그러나 남유럽 국가에서는 긴축 재정에 의한 제약이 남아 있기 때문에 성장률은 한 자리 대 중반으로 억제되고 있습니다. 그러나 폴란드와 체코 공화국에서는 민간 병원 네트워크가 확대되고 있으며 독일의 기준을 모방하여 톱 클래스 현미경을 구입하는 경우가 많기 때문에 그 영향은 일부 상쇄됩니다.

아시아태평양의 CAGR은 9.62%를 나타내 가장 높으며 중국과 인도의 급속한 헬스케어 인프라 확대가 뒷받침되고 있습니다. 중국의 Healthy China 2030 청사진과 인도의 Ayushman Bharat 보험 체계와 같은 정부 이니셔티브로 대응 가능한 환자층이 확대되고 있습니다. 중국의 제3종 의료 특구에서는 현지 장비 조립에 세제 우대 조치가 적용되므로 외자계 브랜드는 리드 타임을 단축하여 지방 입찰을 획득할 수 있습니다. 중산계급의 기대가 높아지고, 백내장 수술이나 굴절 교정 수술의 보급이 가속화되어 안과 기기의 수입이 촉진됩니다. 종종 귀국 자녀의 기술자를 보유한 현지 신흥기업은 제3차 병원과 협력하여 비용효과가 높은 현미경을 공동 개발하고 경쟁압력을 가하는 동시에 전반적인 보급률을 높이고 있습니다. 일본과 한국은 성숙하고 있지만 고령화가 진행되고 있기 때문에 1세대 디지털 스코프에서 로봇 대응 기종으로의 교체가 진행되고, 지역의 출하 대수는 유지되고 있습니다.

남미는 상파울루와 리오데자네이루의 기간병원의 설비 갱신을 실시하는 브라질의 관민 파트너십이 주역이 되어 안정적이지만 완만한 성장을 이루고 있습니다. 환율 변동으로 인해 입찰이 지연될 수 있으므로 공급업체는 판매 주문을 보장하기 위해 현지 현실 자금 조달을 고려해야 합니다. 중동 및 아프리카에서는 특히 걸프 협력 회의 회원국에서 최첨단 마이크로서지컬 도구가 필요한 새로운 이식 센터와 종양 센터가 주권자의 건강 비전에 자금을 제공합니다. 사하라 이남의 아프리카에서는 NGO가 지원하는 백내장 캠프가 휴대용 현미경의 일시적인 수요를 낳고 있으며, 상설 안과 의료 센터가 설립되면 미래의 업셀 기초가 정돈됩니다. 어떠한 지역에서도 마이크로서지컬 기구 시장은 모범 사례를 보급하고 자국에서의 조달 희망 목록에 영향을 미치는 국경을 넘는 외과의사 휄로우십에서 이익을 얻고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 기존 수술에 대한 마이크로 서저리의 우위성

- 수술 건수와 만성 질환 이환율 증가

- 디지털 현미경과 로봇의 기술 진보

- 낮은 침습 수술에 대한 수요 증가

- 마이크로 기기의 업그레이드를 가속하는 4K/3D OR 통합

- 생체 흡수성 마이크로 봉합사의 출현

- 시장 성장 억제요인

- 고급 마이크로서지컬 시스템의 고비용

- 엄격한 기기 승인 패스웨이(클래스 III)

- 신흥 시장에서 훈련된 마이크로 서저리의 부족

- 로봇·플랫폼으로의 예산 변화에 의한 수동 세트의 공식

- Five Forces 분석

- 신규 진입자의 위협

- 구매자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품별

- 마이크로 봉합사

- 마이크로 포셉

- 수술용 현미경

- 마이크로 가위

- 마이크로 바늘 집게

- 마이크로 혈관 클램프

- 기타 기기

- 마이크로서지컬 유형별

- 정형외과

- 안과

- 성형 및 재건

- 이비인후과

- 신경외과

- 부인과 및 비뇨기과

- 기타 유형

- 최종 사용자별

- 병원

- 외래 수술 센터(ASC)

- 전문 클리닉

- 학술 및 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- ZEISS International

- Olympus Corporation

- B. Braun Melsungen AG(Aesculap)

- Haag-Streit Surgical

- Karl Kaps GmbH

- Global Surgical Corporation

- KLS Martin Group

- Microsurgery Instruments Inc.

- Beaver-Visitec International(BVI)

- Stille AB

- Alcon Inc.

- Stryker Corporation

- Integra LifeSciences

- Danaher Corporation

- Scanlan International

- Baxter International

- Johnson & Johnson

- Teleflex Medical

- Medtronic plc

- Karl Storz SE

제7장 시장 기회와 전망

KTH 25.10.29The global microsurgical instruments market was valued at USD 228.97 million in 2025 and is forecast to advance to USD 323.41 million by 2030, reflecting a robust 7.15% CAGR over the period.

Escalating uptake of precision-based surgical techniques, rapid integration of 4K/3D digital microscopy, and rising volumes of chronic-disease-related interventions continue to expand demand for highly specialized instruments. Hospitals and teaching centers continue to refresh capital equipment fleets with AI-enabled operating microscopes, while ambulatory surgical centers lean on compact, workflow-oriented sets to migrate complex cases to outpatient settings. The competitive field shows purposeful R&D spending on ergonomic designs, bio-resorbable micro-suture materials, and voice-controlled visualization units to differentiate offerings. Manufacturers must, however, maneuver through stringent Class III approval pathways, making early engagement with regulators and risk-sharing partnerships with providers vital to sustaining innovation momentum.

Global Microsurgical Instruments Market Trends and Insights

Microsurgery Advantage Over Conventional Surgery

Clinical evidence shows sub-millimeter accuracy translating into lower complication rates and faster recovery, positioning the microsurgical instruments market for sustained adoption. The ETcath robotic platform identifies lesions with 0.1 mm precision, surpassing manual limits and reinforcing the economic rationale for capital purchases. Multitasking devices such as "the flute," which replaces three instruments in one, reduce setup time and operating-room congestion. Hospitals leverage these outcome gains to negotiate favorable reimbursements, thereby accelerating replacement cycles. Specialty clinics apply microsurgical reconstruction to improve functional and aesthetic results that standard techniques struggle to replicate. As insurers reimburse for value-based metrics, instrument vendors that document reduction in adverse events enjoy an edge when new tenders are issued.

Rising Surgical Volumes & Chronic Disease Incidence

Population aging and the global diabetes burden underpin climbing procedure counts, ensuring multiyear velocity for the microsurgical instruments market. China's health expenditure outlook of USD 33.4 trillion by 2060 signals large equipment pools across tertiary centers. Diabetic retinopathy drives a high baseline of retinal microsurgery, while coronary artery bypass and tumor resections require nerve-sparing precision that legacy tools cannot deliver. Governments in Asia allocate procurement budgets for ophthalmic and cardiovascular suites, creating attractive bulk-purchase opportunities. Western systems, although mature, still see growth from revision surgeries and longer life expectancy. Device makers respond by tailoring starter kits that bundle microscopes, forceps, and bio-resorbable sutures to lower adoption friction in mid-tier facilities.

High Cost of Advanced Microsurgical Systems

Premium robotic microscopes command list prices exceeding USD 1 million, while maintenance contracts and sterile consumables can double ten-year ownership cost. Emerging-market hospitals divert limited capital toward essential imaging or ICU beds, leaving microsurgical upgrades on deferred wish lists. Smaller North American community facilities also weigh volume thresholds before committing to full suites, opting instead for refurbished units that offer limited functionality. Vendors counteract sticker shock with pay-per-use leasing, profit-sharing models, and modular build-outs that start with core optics then add robotic arms later. Government procurement grants tied to quality-of-care targets partially offset capex barriers, yet parity with lower-cost manual sets may take additional cycles.

Other drivers and restraints analyzed in the detailed report include:

- Technological Advances in Digital Microscopes & Robotics

- Growing Demand for Minimally-Invasive Procedures

- Stringent Device-Approval Pathways (Class III)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Operating Microscopes retained a commanding 29.52% microsurgical instruments market share in 2024, underpinned by continuous infusion of 4K visualization, augmented-reality overlays, and AI-guided autofocus. The segment captured USD 67 million of the microsurgical instruments market size in 2025 and is charted to expand steadily as neurosurgeons and ophthalmologists adopt robotics-ready optics suites. Segment expansion also rides on multi-disciplinary use; ENT and plastic surgeons leverage shared microscopes within hybrid theatres, boosting utilization rates and replacement frequency.

Micro Sutures, bolstered by bio-resorbable polymers that curb foreign-body reactions, are set to outpace through their 9.25% CAGR, particularly in nerve grafting and vascular anastomosis cases. Micro Forceps and Micro Needle Holders benefit from titanium construction and haptic-enhanced grips, alleviating hand fatigue during six-hour reconstructive sessions. Rounding out portfolios, Micro Scissors and Micro Vessel Clamps evolve with diamond-like coatings that preserve sharpness after 1,000 sterilization cycles, while specialty retractors address narrow anatomical corridors in pediatric microsurgery. Collectively, these advancements reinforce recurring revenue streams from consumables, service contracts, and software upgrades, providing vendors with balanced growth across instrument categories.

The Microsurgical Instruments Market Report is Segmented by Product (Micro Sutures, Micro Forceps, Operating Microscopes, Micro Scissors, Micro Needle Holders, and More), Microsurgery Type (Orthopedic, Ophthalmic, ENT, Neurological, and More), End-User (Hospitals, Ambulatory Surgical Centers and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 38.82% of 2024 revenue, supported by entrenched OR digitization and favorable reimbursement that covers high-ticket visualization platforms. Regional teaching alliances, such as Cleveland Clinic's collaboration with optics manufacturers, pilot augmented-reality guidance that feeds directly into procurement pathways across affiliated hospitals. Site-of-service migration continues unabated; ASCs now execute more than 60% of rotator cuff repairs, ensuring replacement demand for compact microscopes and single-use suture cartridges. The microsurgical instruments market maintains pricing power here due to value-based contracting, where lower readmission rates secure bonus payments that offset premium device costs.

Europe remains the second-largest buyer pool, with strong adoption in Germany, France, and the Nordics. The region leans on rigorous surgeon credentialing and centralized tender frameworks that prioritize lifecycle cost, pushing vendors to extend warranty periods and offer predictive maintenance packages. EU MDR compliance expenses elevate barriers for new entrants, indirectly protecting incumbent share. Growth, however, is more tempered at mid-single-digit rates as austerity constraints linger in Southern Europe. That drag is partially offset by expanding private hospital networks in Poland and the Czech Republic, which often emulate German standards and thus purchase top-tier microscopes.

Asia-Pacific posts the highest CAGR at 9.62%, buoyed by rapid healthcare infrastructure expansion in China and India. Government initiatives such as China's Healthy China 2030 blueprint and India's Ayushman Bharat insurance scheme enlarge addressable patient pools. Chinese class-III medical zones grant tax incentives for local device assembly, enabling foreign brands to shorten lead times and capture provincial tenders. Rising middle-class expectations accelerate penetrative depth in cataract and refractive surgery, bolstering ophthalmic instrument imports. Local start-ups, often staffed by returnee engineers, collaborate with tertiary hospitals to co-develop cost-effective microscopes, injecting competitive pressure yet broadening overall adoption. Japan and South Korea, mature but aging societies, drive replacement sales as facilities swap first-generation digital scopes for robotics-ready variants, preserving regional unit shipment volume.

South America delivers steady but moderate growth, dominated by Brazil's public-private partnerships that renew capital equipment across flagship hospitals in Sao Paulo and Rio de Janeiro. Currency volatility occasionally delays tenders, urging vendors to consider financing denominated in local reais to secure orders. Middle East & Africa represent nascent opportunity pockets, particularly in Gulf Cooperation Council states where sovereign health visions fund new transplant and oncology centers requiring state-of-the-art microsurgical tools. In Sub-Saharan Africa, NGO-supported cataract camps create episodic demand for portable microscopes, setting the groundwork for future up-selling once permanent eye-care centers are established. Across all geographies, the microsurgical instruments market benefits from cross-border surgeon fellowships that disseminate best practices and subsequently influence procurement wish lists in home countries.

- Carl Zeiss

- Olympus

- B. Braun Melsungen AG (Aesculap)

- HAAG-Streit

- Karl Kaps

- Global Surgical

- KLS Martin Group

- Microsurgery Instruments Inc.

- Beaver-Visitec International (BVI)

- Stille

- Alcon

- Stryker

- Integra LifeSciences

- Danaher

- Scanlan International

- Baxter

- Johnson & Johnson

- Teleflex Medical

- Medtronic

- Karl Storz SE

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Microsurgery Advantage Over Conventional Surgery

- 4.2.2 Rising Surgical Volumes & Chronic Disease Incidence

- 4.2.3 Technological Advances In Digital Microscopes & Robotics

- 4.2.4 Growing Demand For Minimally-Invasive Procedures

- 4.2.5 4K/3-D OR Integration Accelerating Micro-Instrument Upgrades

- 4.2.6 Emergence Of Bio-Resorbable Micro-Sutures

- 4.3 Market Restraints

- 4.3.1 High Cost Of Advanced Microsurgical Systems

- 4.3.2 Stringent Device-Approval Pathways (Class III)

- 4.3.3 Shortage Of Trained Microsurgeons In Emerging Markets

- 4.3.4 Budget Shift Toward Robotic Platforms Cannibalising Manual Sets

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Micro Sutures

- 5.1.2 Micro Forceps

- 5.1.3 Operating Microscopes

- 5.1.4 Micro Scissors

- 5.1.5 Micro Needle Holders

- 5.1.6 Micro Vessel Clamps

- 5.1.7 Other Instruments

- 5.2 By Microsurgery Type

- 5.2.1 Orthopedic

- 5.2.2 Ophthalmic

- 5.2.3 Plastic & Reconstructive

- 5.2.4 ENT

- 5.2.5 Neurological

- 5.2.6 Gynecological & Urological

- 5.2.7 Other Types

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Ambulatory Surgical Centers

- 5.3.3 Specialty Clinics

- 5.3.4 Academic & Research Institutes

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 ZEISS International

- 6.3.2 Olympus Corporation

- 6.3.3 B. Braun Melsungen AG (Aesculap)

- 6.3.4 Haag-Streit Surgical

- 6.3.5 Karl Kaps GmbH

- 6.3.6 Global Surgical Corporation

- 6.3.7 KLS Martin Group

- 6.3.8 Microsurgery Instruments Inc.

- 6.3.9 Beaver-Visitec International (BVI)

- 6.3.10 Stille AB

- 6.3.11 Alcon Inc.

- 6.3.12 Stryker Corporation

- 6.3.13 Integra LifeSciences

- 6.3.14 Danaher Corporation

- 6.3.15 Scanlan International

- 6.3.16 Baxter International

- 6.3.17 Johnson & Johnson

- 6.3.18 Teleflex Medical

- 6.3.19 Medtronic plc

- 6.3.20 Karl Storz SE

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment