|

시장보고서

상품코드

1842650

바이러스 클리어런스 서비스 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Viral Clearance Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

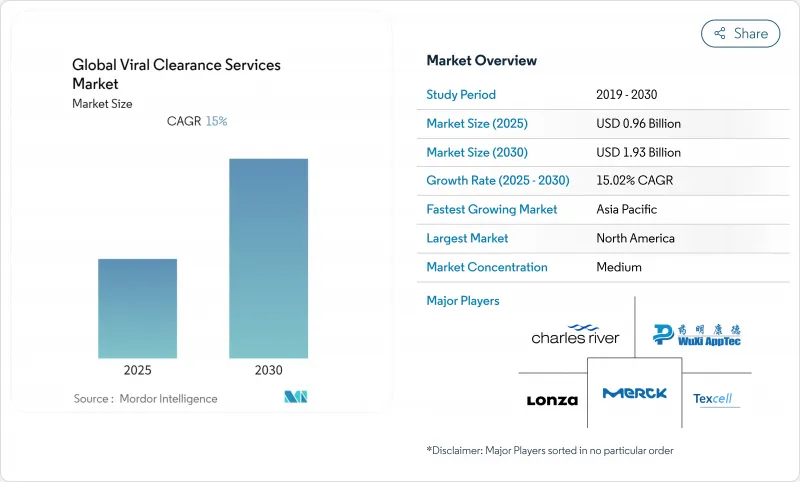

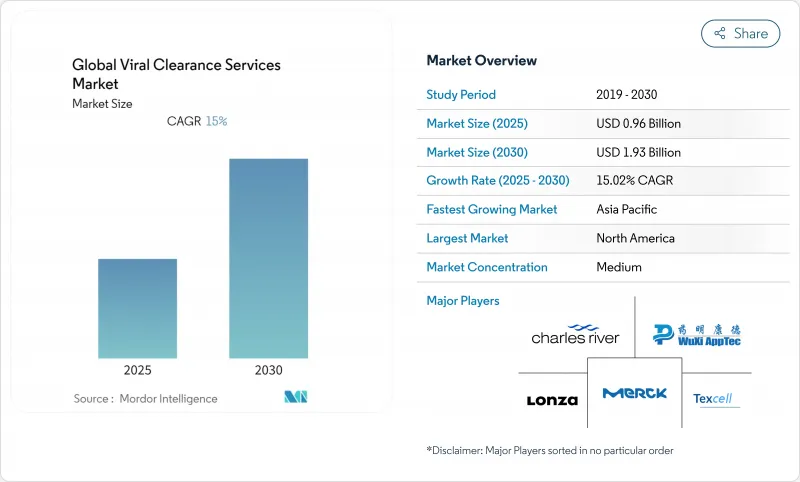

바이러스 클리어런스 서비스 시장 규모는 2025년에 9억 6,000만 달러가 되고, CAGR 15.02%를 나타내, 2030년에는 19억 3,000만 달러에 달할 것으로 예측됩니다.

이 배증의 궤도는 생물제제, 백신, 세포 및 유전자 치료 등의 선진 의료에서의 바이러스 안전성 밸리데이션 수요의 급증을 반영하고 있습니다. 미국 식품의약국(FDA)의 Q5A(R2) 업데이트에 의해 장려된 플랫폼 기반 검증은 연구 일정을 단축하고 바이러스 클리어런스를 컴플라이언스 체크박스에서 보다 신속한 제품 시장을 위한 전략적 인에이블러로 바꿨습니다. 아데노 관련 바이러스(AAV) 및 렌티바이러스 벡터 파이프라인의 급속한 확대는 맞춤형 프로토콜의 필요성을 더욱 확대하고, 전문가의 개발 및 제조 위탁 기관(CDMO)으로의 아웃소싱은 생산 능력 확대를 가속화하고 있습니다.

주요 성장 촉매는 고분자 제조의 세계 르네상스, 주요 시장 전반의 규제 프레임 워크의 조화, 연속 바이오프로세스의 꾸준한 산업화를 포함합니다. 전통적인 장비 공급업체가 서비스에 진출하고 전문 수탁 연구 기관(CRO)이 제조 자산을 구매하여 엔드 투 엔드 서비스를 제공하게 되었기 때문에 경쟁 역학이 재구성되고 있습니다. 견조한 전망과는 반대로 비용 집약적인 멀티바이러스 연구, 숙련된 바이오 세이프티 요원의 부족, 신규 모달리티에 대한 단편적인 지침이 역풍이 되고 있습니다.

세계의 바이러스 클리어런스 서비스 시장 동향과 인사이트

고분자 제조에서 바이러스 안전성 검증 수요 증가

고분자 의약품 제조에서 바이러스 클리어런스는 공정 설계의 업스트림로 이동합니다. FDA 지침은 현재 플랫폼 접근법을 평가하여 제조업체가 안전성을 유지하면서 단일클론항체 프로그램 전체에서 클리어런스 데이터를 재사용할 수 있도록 하고 있습니다. 연속 바이오프로세싱 라인은 인라인 바이러스 필터를 통합하여 실시간 보증을 제공하고 수율을 향상시키고 재밸리데이션 비용을 절감합니다. 이러한 통합 능력을 가진 기업은 제품을 더 빨리 상시하고 규제 당국의 문의를 제한함으로써 바이러스 클리어런스 능력을 명확한 경쟁 우위로 바꾸고 있습니다. 장비의 혁신자는 처리량을 손상시키지 않고 제품의 품질을 보호하는 높은 플럭스 필터를 지원합니다.

세계적으로 확대되는 생물 제제 및 바이오시밀러 의약품 파이프라인

700개가 넘는 유전자 치료제와 수백 개의 바이오시밀러가 개발 중이며, 신규 진입에는 각각 엄격한 클리어런스가 필요합니다. 국제 의약품 평가 조화위원회(ICH)의 노력은 요구 사항을 표준화하고 단일 검증 패키지로 여러 대륙에서 신청할 수있게했습니다. 따라서 서비스 제공업체는 개발 예산의 더 큰 부분을 차지합니다. 예를 들어, 유로핀스 사이언티픽사는 대규모 위탁 시험의 회복을 보고하고 바이러스 안전 업무에 추가 능력을 할당했습니다.

다중 바이러스 검증 테스트의 높은 비용과 복잡성

종합적인 연구는 종종 3-5 유형의 모델 바이러스를 사용하며 각각은 여러 단계에서 테스트됩니다. 총 조사 비용은 50만 달러에서 200만 달러로, 소규모 바이오테크놀러지 기업의 예산을 압박해 자원이 부족한 지역의 혁신자의 발판이 되고 있습니다. 시약 공급 체인은 취약하고 자격을 갖춘 시드 스톡 리드 타임이 깁니다. 서비스 제공업체는 비감염성 대리인과 규제 당국이 현재 받아들이고 있는 데이터가 풍부한 플랫폼 검증을 채택하여 비용에 대응하고 있습니다.

부문 분석

바이러스 제거법은 2024년 바이러스 클리어런스 서비스 시장 규모의 60.78%를 차지하고 바이오프로세스의 안전성을 지원하는 기간기술인 것으로 재확인되었습니다. 크로마토그래피, 심층 여과 및 바이러스 보유 막은 단일클론항체 및 재조합 단백질에서 예측 가능한 로그 감소 값을 제공합니다. 현재 연속적인 다운스트림 트레인은 이러한 단계를 홀드 타임을 최소화하면서 무균성을 유지하는 단일 사용 폐쇄 시스템에 통합하고 있습니다.

하이브리드 전략은 2030년까지 연평균 복합 성장률(CAGR) 17.04%를 나타내 서비스 포트폴리오를 재구성했습니다. 공급자는 의도적인 순서로 솔벤트/세제 불활성화, 낮은 pH 홀드, UV-C 조사 및 물리적 제거를 통합하여 엔벨로프화된 위협과 엔벨로프화되지 않은 위협을 모두 처리합니다. Asahi Kasei의 플라노바 FG1 필터는 높은 플럭스 막이 바이러스의 로그 감소 계수를 희생하지 않고 처리량을 가속화하는 방법을 보여줍니다. 하이브리드 프로토콜의 바이러스 클리어런스 서비스 시장 규모는 2025년 1억 4,000만 달러에서 2030년에는 3억 5,000만 달러로 확대될 것으로 예측되며, 멀티모달 탄력성에 대한 업계의 의욕을 뒷받침하고 있습니다.

2세대 하이브리드는 기존의 단계에 고압 처리와 나노여과를 거듭하여 견고한 파보바이러스에 대항합니다. 인공지능 가이드 설계 도구는 최적의 단계 조합을 제안하고 실험 횟수를 최대 30%까지 줄입니다. 이러한 혁신은 예측 가능성을 높이고 리스크 기반의 과학 주도의 검증 프레임워크를 목표로 하는 규제 당국의 움직임을 지원합니다. 연속 제조가 확산됨에 따라 하이브리드 모듈을 인라인으로 통합할 수 있는 공급업체는 배치 지향 경쟁사를 희생하여 점유율을 확대할 것으로 보입니다.

지역 분석

북미는 2024년에 바이러스 클리어런스 서비스 시장의 39.32%를 차지하며, 규제 당국의 주도, 벤처 자금 조달, 대규모 공장 확장의 세계적인 중심지였습니다. 후지필름의 12억 달러의 노스캐롤라이나 프로젝트는 2031년까지 바이오리액터의 생산량을 3배로 할 예정으로 통합 클리어런스 검증의 새로운 수요를 창출하고 있습니다. 자격을 갖춘 모델 바이러스의 견고한 공급 네트워크 외에도 FDA의 심사관에 가깝기 때문에이 지역의 전략적 중요성이 높아지고 있습니다. 북미의 바이러스 클리어런스 서비스 시장 규모는 2025년 3억 8,000만 달러에서 2030년에는 7억 4,000만 달러로 확대될 것으로 예측됩니다.

유럽은 유럽 의약품청의 종합적인 바이러스 안전 지침과 유럽 위원회의 2024년 생명공학 전략에 힘입어 큰 존재감을 보여주었습니다. 독일에 있는 9,000만 유로의 유전자 치료 허브와 슬로베니아에 있는 노바티스의 4,000만 유로의 벡터 시설은 지역의 능력을 확대하고 있습니다. 그러나 유럽의 여러 국가에 걸친 규제 상황과 인건비 상승으로 유럽의 CAGR은 한 자리에 머물렀고 점유율은 계속 커지고 있습니다.

아시아태평양은 CAGR 16.47%를 나타내 가장 빠르게 성장하고 있습니다. 중국의 자유무역지역 내에서의 세포 및 유전자 치료를 위한 외국인 소유권 제한 철폐의 결정과 일본의 SAKIGAKE 패스웨이의 신속화에 의해 승인까지의 기간이 단축되어 다국적 스폰서가 유치되었습니다. WuXi Biologics 및 다카라 바이오와 같은 지역 CDMO는 벡터 스위트 및 대용량 바이러스 여과 트레인에 투자합니다. 아시아태평양의 바이러스 클리어런스 서비스 시장 규모는 2025년 2억 1,000만 달러에서 2030년 4억 5,000만 달러로 급증할 것으로 예측되며, 구미의 확립된 거점과의 차이가 줄어듭니다. 인재 부족은 여전히 계속되고 있지만, 정부 보조금이나 대학과의 제휴에 의해 바이러스학의 인재 풀을 확대하는 것을 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 고분자 제조에 있어서의 바이러스 안전성 밸리데이션 수요 증가

- 세계의 생물제제 및 바이오시밀러 파이프라인 확대

- 특주 프로토콜을 필요로 하는 세포 및 유전자 치료 붐

- 전문 CRO/CDMO에 아웃소싱 급증

- 상용적인 바이오프로세스가 인라인 클리어런스 기술을 추진

- AI를 활용한 예측 밸리데이션 플랫폼이 시험 기간을 단축

- 시장 성장 억제요인

- 멀티바이러스 밸리데이션 시험의 고비용과 복잡성

- 숙련된 바이러스학 및 바이오 세이프티 인재의 부족

- 신규 모달리티(AAV 등)에 대한 세계 가이던스의 단편화

- 적격한 모델 바이러스와 참조 표준 공급망 공백

- 밸류체인 분석

- 기술적 전망

- Porter's Five Forces 분석

- 신규 진입자의 위협

- 구매자/소비자의 협상력

- 공급자의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 방법별

- 바이러스 제거

- 크로마토그래피

- 단백질 A 포집

- 이온 교환

- 친화성 및 혼합 모드

- 여과

- 나노 여과

- 심층 여과

- 막 흡착제

- 침전(PEG/에탄올)

- 바이러스 불활성화

- 용제/세제 처리

- 낮은 pH 배양

- UV-C 조사

- 가열/저온 살균

- 고압 처리

- 하이브리드 전략

- 바이러스 제거

- 용도별

- 재조합 단백질

- 단일클론 항체

- 조직 및 혈액 유래 제품

- 백신

- 유전자 및 세포 치료제

- 바이러스 벡터

- 기타 용도

- 최종 사용자별

- 주요 제약 회사

- 중소 바이오 테크놀로지

- 계약 개발 및 제조 기관(CDMO)

- 계약 연구 및 시험 기관(CRO)

- 학술 및 정부 연구 기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 경쟁 벤치마킹

- 시장 점유율 분석

- 기업 프로파일

- BioOutsource Ltd(Sartorius)

- Bioscience Laboratories

- BSL BioService

- Catalent Inc.

- Charles River Laboratories

- Clean Cells

- Creative Biolabs

- Cygnus Technologies

- Eurofins Scientific

- Fujifilm Diosynth Biotechnologies

- Lonza Group

- Merck KGaA

- Microbac Laboratories

- Pall Corporation(Cytiva)

- Sartorius AG

- SGS SA

- Texcell SA

- Vironova AB

- ViruSure GmbH

- WuXi AppTec

제7장 시장 기회와 전망

KTH 25.10.29The viral clearance services market size stood at USD 0.96 billion in 2025 and is expected to reach USD 1.93 billion by 2030, advancing at a 15.02% CAGR.

The doubling trajectory reflects surging demand for viral safety validation across biologics, vaccines, and advanced modalities such as cell and gene therapies. Platform-based validation encouraged by the United States Food and Drug Administration's (FDA) Q5A(R2) update has shortened study timelines, turning viral clearance from a compliance checkbox into a strategic enabler of faster product launches fda.gov. Rapid expansion of adeno-associated virus (AAV) and lentiviral vector pipelines has further magnified the need for bespoke protocols, while outsourcing to specialist contract development and manufacturing organizations (CDMOs) accelerates capacity growth.

Key growth catalysts include the global renaissance in large-molecule manufacturing, harmonized regulatory frameworks across major markets, and the steady industrialization of continuous bioprocessing. Competitive dynamics are reshaping as traditional equipment vendors extend into services and specialist contract research organizations (CROs) buy manufacturing assets to provide end-to-end offerings. Despite a robust outlook, cost-intensive multi-virus studies, shortages of skilled biosafety personnel, and fragmented guidance for novel modalities pose headwinds.

Global Viral Clearance Services Market Trends and Insights

Rising Demand for Viral Safety Validation in Large-Molecule Manufacturing

Large-molecule production has shifted viral clearance upstream into process design. FDA guidance now rewards platform approaches, letting manufacturers reuse clearance data across monoclonal antibody programs while preserving safety. Continuous bioprocessing lines incorporate in-line virus filters that provide real-time assurance, improving yields and lowering re-validation costs. Companies with such integrated capabilities launch products sooner and limit regulatory queries, turning viral clearance capacity into a clear competitive advantage. Equipment innovators have responded with high-flux filters that safeguard product quality without compromising throughput.

Expanding Biologics & Biosimilar Pipeline Worldwide

More than 700 gene therapies and hundreds of biosimilars are under development, and each new entrant needs rigorous clearance. International Council for Harmonisation (ICH) efforts have standardized requirements so that a single validation package can underpin submissions on multiple continents. Service providers therefore capture a larger slice of development budgets. Eurofins Scientific, for example, has reported a rebound in large contracted studies and allocated additional capacity to viral safety work.

High Cost & Complexity of Multi-Virus Validation Studies

Comprehensive studies often involve three to five model viruses, each tested across multiple process steps. The total research outlays range from USD 500,000 to USD 2 million, straining smaller biotech budgets and deterring innovators in resource-limited regions. Reagent supply chains are fragile, with long lead times for qualified seed stocks. Service providers are countering costs by adopting non-infectious surrogates and data-rich platform validations that regulators now accept.

Other drivers and restraints analyzed in the detailed report include:

- Cell & Gene Therapy Boom Requiring Bespoke Protocols

- Outsourcing Surge to Specialist CRO/CDMOs

- Shortage of Skilled Virology and Biosafety Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Viral removal methods captured 60.78% of the viral clearance services market size in 2024, reaffirming their status as the backbone of bioprocess safety. Chromatography, depth filtration, and virus-retentive membranes deliver predictable log-reduction values across monoclonal antibodies and recombinant proteins. Continuous downstream trains now weave these steps into single-use, closed systems that maintain sterility while minimizing hold times.

Hybrid strategies, though accounting for a smaller base, are growing at 17.04% CAGR through 2030 and are reshaping service portfolios. Providers integrate solvent/detergent inactivation, low-pH hold, and UV-C irradiation with physical removal in deliberate sequences that address both enveloped and non-enveloped threats. Asahi Kasei's Planova FG1 filter demonstrates how high-flux membranes accelerate throughput without sacrificing virus log-reduction factors. The viral clearance services market size for hybrid protocols is projected to expand from USD 140 million in 2025 to USD 350 million in 2030, underscoring industry appetite for multimodal resilience.

Second-generation hybrids layer high-pressure processing or nanofiltration onto legacy steps to combat robust parvoviruses. AI-guided design tools suggest optimal step combinations, reducing experimental runs by up to 30%. These innovations enhance predictability and support regulators' push toward risk-based, science-driven validation frameworks. As continuous manufacturing gains traction, providers able to integrate hybrid modules inline will gain share at the expense of batch-oriented competitors.

The Viral Clearance Services Market Report is Segmented by Method (Viral Removal [Chromatography and More], Viral Inactivation [Solvent/Detergent Treatment and More], and Hybrid Strategies), Application (Recombinant Proteins, Monoclonal Antibodies, and More), End-User (Large Pharma and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controlled 39.32% of the viral clearance services market in 2024 and remains the global nexus for regulatory leadership, venture funding, and large-scale plant expansions. Fujifilm's USD 1.2 billion North Carolina project will triple bioreactor output by 2031, creating new demand for integrated clearance validation. Robust supply networks for qualified model viruses, plus proximity to FDA reviewers, enhance the region's strategic importance. The viral clearance services market size in North America is expected to climb from USD 380 million in 2025 to USD 740 million in 2030.

Europe maintains a substantial presence underpinned by the European Medicines Agency's comprehensive viral safety guidance and the European Commission's 2024 biotechnology strategy. Roche's €90 million gene therapy hub in Germany and Novartis's €40 million vector facility in Slovenia expand regional capacity. Yet Europe's multi-country regulatory landscape and rising labor costs temper growth to single-digit CAGRs, keeping its share stable rather than expansionary.

Asia Pacific is the fastest mover, advancing at a 16.47% CAGR. China's decision to lift foreign ownership limits for cell and gene therapy within free-trade zones and Japan's expedited Sakigake pathway shorten approval windows and attract multinational sponsors. Regional CDMOs like WuXi Biologics and Takara Bio are investing in vector suites and high-capacity virus filtration trains. The viral clearance services market size in Asia Pacific is projected to leap from USD 210 million in 2025 to USD 450 million by 2030, closing the gap with established Western hubs. Talent shortages persist, yet government grants and university partnerships aim to broaden the virology talent pool.

- BioOutsource Ltd (Sartorius)

- BIOSCIENCE LABORATORIES

- BSL BioService

- Catalent

- Charles River

- Clean Cells

- Creative Biolabs

- Cygnus Technologies

- Eurofins

- FUJIFILM

- Lonza Group

- Merck

- Microbac Laboratories

- Pall Corporation (Cytiva)

- Sartorius

- SGS

- Texcell

- Vironova

- ViruSure GmbH

- WuXi App Tec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for viral safety validation in large-molecule manufacturing

- 4.2.2 Expanding biologics & biosimilar pipeline worldwide

- 4.2.3 Cell & gene therapy boom requiring bespoke protocols

- 4.2.4 Outsourcing surge to specialist CRO/CDMOs

- 4.2.5 Continuous bioprocessing drives in-line clearance technologies

- 4.2.6 AI-enabled predictive validation platforms shorten study timelines

- 4.3 Market Restraints

- 4.3.1 High cost & complexity of multi-virus validation studies

- 4.3.2 Shortage of skilled virology and biosafety workforce

- 4.3.3 Fragmented global guidance for novel modalities (e.g., AAV)

- 4.3.4 Supply-chain gaps in qualified model viruses & reference standards

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Method

- 5.1.1 Viral Removal

- 5.1.1.1 Chromatography

- 5.1.1.1.1 Protein A Capture

- 5.1.1.1.2 Ion-Exchange

- 5.1.1.1.3 Affinity & Mixed-Mode

- 5.1.1.2 Filtration

- 5.1.1.2.1 Nanofiltration

- 5.1.1.2.2 Depth Filtration

- 5.1.1.2.3 Membrane Adsorbers

- 5.1.1.3 Precipitation (PEG/Ethanol)

- 5.1.2 Viral Inactivation

- 5.1.2.1 Solvent/Detergent Treatment

- 5.1.2.2 Low-pH Incubation

- 5.1.2.3 UV-C Irradiation

- 5.1.2.4 Heat / Pasteurization

- 5.1.2.5 High-Pressure Processing

- 5.1.3 Hybrid Strategies

- 5.1.1 Viral Removal

- 5.2 By Application

- 5.2.1 Recombinant Proteins

- 5.2.2 Monoclonal Antibodies

- 5.2.3 Tissue & Blood-derived Products

- 5.2.4 Vaccines

- 5.2.5 Gene & Cell Therapies

- 5.2.6 Viral Vectors

- 5.2.7 Other Applications

- 5.3 By End-User

- 5.3.1 Large Pharma

- 5.3.2 Small & Mid-size Biotech

- 5.3.3 Contract Development & Manufacturing Organizations (CDMOs)

- 5.3.4 Contract Research & Testing Organizations (CROs)

- 5.3.5 Academic & Government Research Institutes

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East and Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East and Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Competitive Benchmarking

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 BioOutsource Ltd (Sartorius)

- 6.4.2 Bioscience Laboratories

- 6.4.3 BSL BioService

- 6.4.4 Catalent Inc.

- 6.4.5 Charles River Laboratories

- 6.4.6 Clean Cells

- 6.4.7 Creative Biolabs

- 6.4.8 Cygnus Technologies

- 6.4.9 Eurofins Scientific

- 6.4.10 Fujifilm Diosynth Biotechnologies

- 6.4.11 Lonza Group

- 6.4.12 Merck KGaA

- 6.4.13 Microbac Laboratories

- 6.4.14 Pall Corporation (Cytiva)

- 6.4.15 Sartorius AG

- 6.4.16 SGS SA

- 6.4.17 Texcell SA

- 6.4.18 Vironova AB

- 6.4.19 ViruSure GmbH

- 6.4.20 WuXi AppTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment