|

시장보고서

상품코드

1844468

체외 독성 시험 시장 : 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)In Vitro Toxicology Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

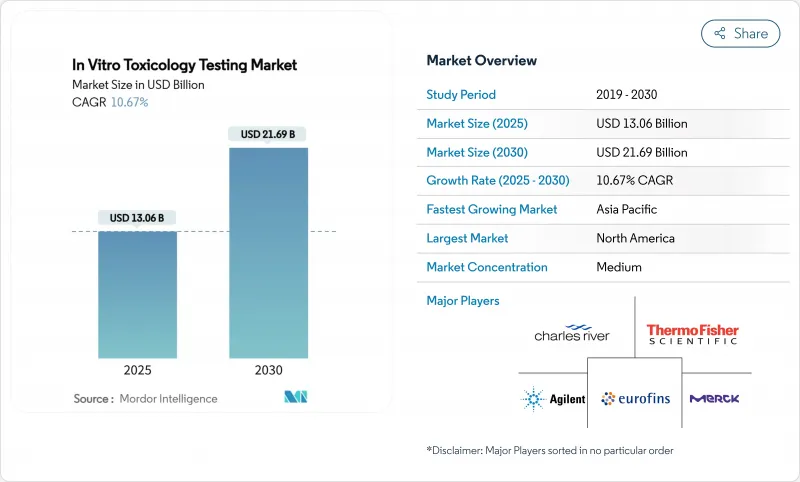

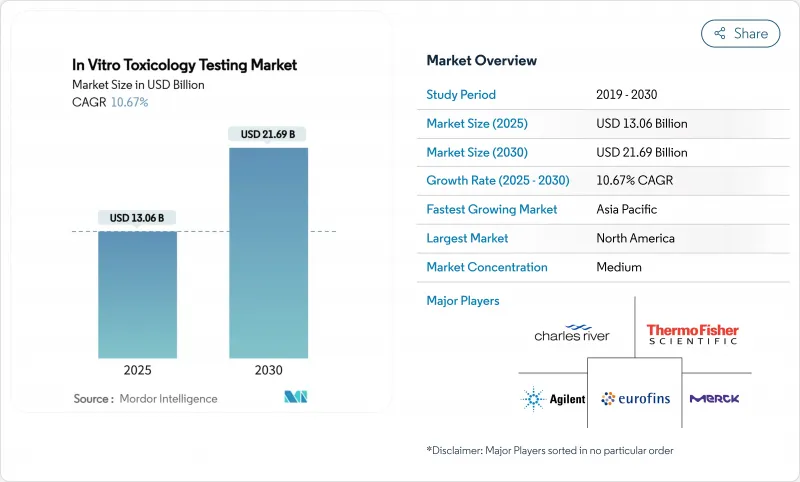

체외 독성 시험 시장 규모는 2025년에 130억 6,000만 달러, 예측기간(2025-2030년)의 CAGR은 10.67%를 나타낼 전망이며, 2030년에는 216억 9,000만 달러에 달할 것으로 예측됩니다.

이 속도는 동물실험을 억제하는 세계적인 규제를 충족시키면서 의약품, 화장품, 화학제품 전반에 걸쳐 사람의 건강을 지키는 데 이 분야가 중심적인 역할을 담당하고 있음을 뒷받침하고 있습니다. 안전 의무화 강화, FDA의 New Alternative Methods 프로그램, 동물 모델을 단계적으로 폐지해 가는 유럽의 로드맵이 수요에 박차를 가하고 있습니다. 3D 세포 배양, 장기 온칩 시스템, AI를 활용한 해석의 병행적인 진보는 예측 정밀도를 높이고, 연구 개발 비용을 삭감하고, 개발 업무 수탁 기관에 새로운 수익원을 가져오고 있습니다. 기술 변화는 독성 검출의 조기화, 후기 단계의 실패 감소, 혁신적인 치료제 시장 출시까지의 시간 단축을 약속하므로 투자자의 관심은 여전히 높습니다.

세계의 체외 독성 시험 시장 동향과 통찰

전임상 연구에서 동물 사용에 대한 반대

윤리적인 압력과 규제의 금지로 동물 실험을 대체하는 움직임이 계속되고 있습니다. Society of Toxicology는 유럽의 엄격한 화장품 지침과 FDA 현대화법 2.0이 비동물 실험을 합법화했다고 지적합니다. 기업이 이러한 규칙을 충족함에 따라 검증된 시험관내 분석에 대한 수요가 가속화되고 있습니다. 다국적기업은 현재 대체법을 세계 신청서류에 통합하여 지역간 통일된 워크플로우를 구축하고 있습니다. 이 추세는 또한 분석법의 검증을 가속화하기 위해 참조 데이터를 공유하는 관민 파트너십을 촉진합니다. 사회적 의식이 높아짐에 따라 잔인하지 않은 시험 서비스를 제공하는 기업이 투자자들에게 지지를 받게 됩니다.

체외 독성 분석의 현저한 진보

3D 오가노이드, 마이크로플루이딕스공학, 단일세포 분석의 획기적인 발전은 인간과 관련된 더 풍부한 데이터를 제공합니다. 미세 유체 폐 온칩 모델은 기존의 기액 계면 시험보다 높은 처리량으로 미립자 독성을 평가할 수 있습니다. 실시간 이미징과 AI를 결합하여 과학자는 노출 후 몇 시간 후에 미묘한 표현형의 변화를 포착할 수 있습니다. 이 도구는 설치류 모델에서 부족하기 쉬운 발달 신경 독성과 같은 복잡한 끝점에 대한 규제 의사 결정을 지원합니다. 프로토콜이 성숙함에 따라 CRO는 분석 번들과 통합하여 완전한 메커니즘 통찰력을 제공하여 프로젝트 당 수익을 높입니다.

자가면역 및 면역자극을 결정하기 위한 시험관내 모델의 무력

정교한 3D 조직조차도 완전한 면역의 복잡성이 부족합니다. AZoLifeSciences는 혈관이나 림프구의 구성 요소가 없는 유기체에서 사이토카인 폭풍을 예측하기가 어렵다고 강조합니다. 따라서 생물 제제 개발자는 생체 내 시험에서 분석을 보완합니다. 새로운 멀티 장기 온칩 시스템은 유망하지만, 재현성과 규제 당국의 검증이 여전히 과제이며, 보급을 늦추고 있습니다.

부문 분석

세포 배양은 성숙한 프로토콜과 광범위한 사용자로부터 지원되었으며 2024년 시험관 내 독성 시험 시장의 43.91%에서 가장 큰 점유율을 유지했습니다. 이 부문의 강점은 탐색 스크리닝, 효능 분석, 규제 당국 신청 등의 다양성에 있습니다. 세포 배양 응용 분야의 시험관 내 독성 시험 시장 규모는 CRISPR 편집 균주 및 AI 지원 이미징과 같은 향상된 기능을 통해 새로운 메커니즘 해명이 진행됨에 따라 2030년까지 80억 달러 이상을 유지할 것으로 예측됩니다. 새로운 3D 구조물은 인간 장기를 더욱 에뮬레이트하여 2차원 단층에서 흔히 볼 수 있는 위음성을 감소시킵니다.

전사체학, 단백질체학, 대사체학에 걸친 OMICS 접근법은 2030년까지 연평균 복합 성장률(CAGR)이 13.88%로 가장 빠른 것을 기록했습니다. 시퀀싱 비용의 급격한 감소와 단일세포 분석의 발전으로 제약, 생명 공학 및 아카데미아 간의 채택이 확산되고 있습니다. 멀티오믹스 층의 통합은 표현형 스크리닝을 보완하는 시스템 수준의 독성학적 시그니처를 제공하고 OMICS를 차세대 안전 파이프라인의 요점으로 자리매김합니다. 데이터 세트가 증가함에 따라, OMICS 지문을 기반으로 훈련된 머신러닝 모델은 구조적 활성 상관을 정밀화하고 신약의 초기 단계에서 특이적인 독성을 예측합니다.

세포 분석은 2024년 시험관 내 독성 시험 시장 점유율의 36.28%를 차지했습니다. 형광 리포터 시스템과 자동 현미경은 세포 사멸, 산화 스트레스 및 DNA 손상에 대한 정량적 데이터를 제공하고 규제 당국에 신청을 지원합니다. 동시에, 인실리코 기술은 최소한의 추가 비용으로 가상 라이브러리를 스크리닝하는 클라우드 기반 머신러닝 플랫폼에 힘입어 가장 높은 수익 증가를 가져올 것으로 예측됩니다.

in-silico 도구의 시험관 내 독성 시험 시장 규모는 의약품 포트폴리오의 합리화와 데이터 풍부한 계산 증거 규제 당국의 수용을 통해 2025년부터 2030년까지 연평균 복합 성장률(CAGR) 13.88%로 성장할 것으로 예상됩니다. 생화학적 분석과 생체외 제제는 계속 경로에 특화된 의문을 해결하고 예측 모델의 검증이 불충분한 복잡한 엔드포인트의 교차 도구로서의 역할을 합니다.

지역 분석

북미는 2024년 매출액 47.75%로 체외 독성 시험 시장을 선도해 대체법에 대한 FDA의 자금 지원과 국민 1인당 연구개발비의 높이에 지지되고 있습니다. 미국의 체외 독성 시험 시장 규모는 AI 유도형 고처리량 플랫폼의 급속한 도입과 고도 진단제에 대한 유리한 상환 환경에 의해 견인되고 있습니다. 실험실이 개발한 검사에 관한 규제의 명확화는 엄격하지만, 유효한 시험관내 기술을 공식적으로 승인하고 있음을 나타냅니다.

아시아태평양이 가장 급성장하고 있으며, 2025년부터 2030년까지의 CAGR은 12.58%로 예측됩니다. 다국적 기업은 방대한 환자 기반과 비용 효율적인 인재 풀을 활용하기 위해 지역 혁신 허브를 설립하고 있습니다. 이러한 요인이 결합되어 세계 규제 기준을 충족하는 안전성 예측 솔루션에 대한 지역 수요가 높아지고 있습니다.

유럽은 엄격한 동물실험 금지와 진보적인 화학물질 안전 지령에 힘입어 2위를 견지하고 있습니다. 유럽 위원회가 2024년 11월에 발표한 동물 실험 폐지 로드맵은 장기 온칩 및 멀티오믹스 분석의 조기 채택을 뒷받침하고 있습니다. 지역 컨소시엄은 검증 경로를 표준화하고 기업에게 부드러운 신청 경로를 제공합니다. 한편, 남미와 중동, 아프리카의 신흥 시장은 의료 인프라와 파마 코비지란스의 틀이 성숙함에 따라 꾸준히 보급되고 있으며, 검사 키트 공급자와 서비스 제공업체에게 장기적인 성장 전망이 되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전임상 연구에서 동물 사용에 대한 반대

- 체외 독성 시험법의 대폭적인 진보

- 의약품의 안전성에 관한 의식의 고조

- 맞춤형 의료에 대한 수요 증가

- 고처리량 스크리닝 기술의 성장

- 동물을 사용하지 않는 시험에 대한 규제 강화

- 시장 성장 억제요인

- 자가면역성 및 면역자극성을 판정하기 위한 시험관내 모델의 무력성

- 체외 시험에 대한 엄격한 규제 틀

- 복잡한 전신 독성에 대한 예측 정밀도의 한계

- 데이터 관리와 통합의 과제

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 기술별

- 세포 배양

- 하이 스루풋

- 분자 이미징

- OMICS

- 3D 세포 배양 및 오가노이드

- 수법별

- 세포 분석

- 생화학 검정

- In-Silico

- Ex-Vivo

- 용도별

- 전신독성

- 경피독성

- 내분비 교란

- 안독성

- 기타 용도

- 최종 사용자별

- 제약산업

- 생명공학 및 CRO

- 진단

- 학술기관 및 연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Charles River Laboratories International Inc.

- Thermo Fisher Scientific Inc.

- Eurofins Scientific SE

- SGS SA

- Merck KGaA

- Agilent Technologies Inc.

- Abbott Laboratories

- Bio-Rad Laboratories Inc.

- Danaher Corporation

- GE HealthCare Technologies Inc.

- Intertek Group plc

- Quest Diagnostics Inc.

- Catalent Inc.

- Evotec SE

- WuXi AppTec Co. Ltd.

- Cyprotex Ltd.

- Promega Corporation

- MB Research Laboratories

- Gentronix Ltd.

- BioIVT LLC

제7장 시장 기회와 전망

SHW 25.11.03The In Vitro Toxicology Testing Market size is estimated at USD 13.06 billion in 2025, and is expected to reach USD 21.69 billion by 2030, at a CAGR of 10.67% during the forecast period (2025-2030).

This pace underscores the sector's central role in safeguarding human health across pharmaceuticals, cosmetics, and chemicals while meeting global regulations that discourage animal testing. Tighter safety mandates, the FDA's New Alternative Methods program, and Europe's roadmap to phase out animal models are spurring demand. Parallel advances in 3D cell culture, organ-on-chip systems, and AI-enabled analytics are raising predictive accuracy, trimming R&D costs, and opening new revenue streams for contract research organizations. Investor interest remains strong as the technology shift promises earlier toxicity detection, fewer late-stage failures, and faster time-to-market for innovative therapeutics.

Global In Vitro Toxicology Testing Market Trends and Insights

Opposition to the Usage of Animals in Pre-clinical Research

Ethical pressure and regulatory bans continue to displace animal studies. The Society of Toxicology notes that Europe's strict cosmetics directive and the FDA Modernization Act 2.0 have legitimized non-animal approaches. As companies align with these rules, demand for validated in vitro assays accelerates. Multinational firms now embed alternative methods into global submission dossiers, creating unified workflows across regions. The trend also catalyzes public-private partnerships that share reference data to speed assay validation. Rising social awareness further encourages investors to favor firms offering cruelty-free testing services.

Significant Advancements In-vitro Toxicology Assays

Breakthroughs in 3D organoids, microfluidics, and single-cell analytics deliver richer human-relevant data. Microfluidic lung-on-chip models now evaluate particulate toxicity with higher throughput than classical air-liquid interface tests. Combined with real-time imaging and AI, scientists can capture subtle phenotypic changes hours after exposure. These tools support regulatory decision-making for complex endpoints such as developmental neurotoxicity, where rodent models often fall short. As protocols mature, CROs integrate assay bundles to provide full mechanistic insights, boosting their revenue per project.

Incapability of In-vitro Models to Determine Autoimmunity and Immunostimulation

Even sophisticated 3D tissues lack full immune complexity. AZoLifeSciences underscores that organoids without vascular and lymphoid components struggle to predict cytokine storms. Biologics developers therefore still complement assays with in vivo studies. Emerging multi-organ-on-chip systems show promise, but reproducibility and regulatory validation remain ongoing challenges, delaying widespread adoption.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Awareness Regarding Drug Product Safety

- Rising Demand for Personalized Medicine

- Stringent Regulatory Framework for the In-vitro Tests

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cell culture retained the largest share at 43.91% of in vitro toxicology testing market in 2024, benefiting from mature protocols and broad user familiarity. The segment's strength lies in its versatility across exploratory screens, potency assays, and regulatory submissions. The in vitro toxicology testing market size for Cell Culture applications is projected to remain above USD 8 billion by 2030 as enhancements such as CRISPR-edited lines and AI-assisted imaging unlock new mechanistic insights. Emerging 3D constructs further emulate human organs, reducing false negatives often seen with two-dimensional monolayers.

OMICS approaches, spanning transcriptomics, proteomics, and metabolomics, recorded the fastest CAGR at 13.88% to 2030. Rapid declines in sequencing costs and advances in single-cell analytics broaden adoption among pharma, biotech, and academia. The integration of multi-omics layers offers systems-level toxicological signatures that complement phenotypic screens, positioning OMICS as a cornerstone of next-generation safety pipelines. As datasets grow, machine-learning models trained on OMICS fingerprints refine structure-activity relationships and predict idiosyncratic toxicities earlier in drug discovery.

Cellular assays commanded 36.28% of the in vitro toxicology testing market share in 2024. Fluorescent reporter systems and automated microscopy supply quantitative data on apoptosis, oxidative stress, and DNA damage, underpinning regulatory-grade submissions. Concurrently, in-silico techniques are projected to generate the highest revenue increment, propelled by cloud-based machine-learning platforms that screen virtual libraries at minimal incremental cost.

The in vitro toxicology testing market size for in-silico tools is growing with CAGR 13.88% between 2025 and 2030, driven by pharmaceutical portfolio rationalization and regulatory acceptance of data-rich computational evidence. Biochemical assays and ex-vivo preparations continue to address pathway-specific questions and serve as bridging tools for complex endpoints where predictive models lack validation.

The in Vitro Toxicology Testing Market Report is Segmented by Technology (Cell Culture, High Throughput, and More), Method (Cellular Assay, Biochemical Assay, and More), Application (Systemic Toxicology, and More), End User (Pharmaceutical Industry, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the in vitro toxicology testing market with 47.75% revenue in 2024, supported by FDA funding for alternative methods and high R&D spend per capita. The in vitro toxicology testing market size in the United States is driven by rapid adoption of AI-guided high-throughput platforms and a favorable reimbursement environment for advanced diagnostics. Regulatory clarity around laboratory-developed tests, although stringent, signals official endorsement of validated in vitro technologies.

Asia-Pacific is the fastest-growing region, forecast at 12.58% CAGR from 2025 to 2030. Multinational firms establish regional innovation hubs to tap the vast patient base and cost-effective talent pool. These factors collectively elevate local demand for predictive safety solutions that meet global regulatory criteria.

Europe holds a firm second place, bolstered by stringent animal-test bans and progressive chemical-safety directives. The European Commission's November 2024 roadmap to eliminate animal studies propels early adoption of organ-on-chip and multi-omics assays. Regional consortia standardize validation pathways, offering companies smoother submission routes. Meanwhile, emerging markets in South America and the Middle East & Africa witness steady uptake as healthcare infrastructure and pharmacovigilance frameworks mature, presenting long-term growth prospects for test kit suppliers and service providers.

- Charles River

- Thermo Fisher Scientific

- Eurofins

- SGS

- Merck

- Agilent Technologies

- Abbott Laboratories

- Bio-Rad Laboratories

- Danaher

- GE HealthCare Technologies Inc.

- Intertek Group

- Quest Diagnostics

- Catalent

- Evotec

- WuXi AppTec Co. Ltd.

- Cyprotex Ltd.

- Promega

- MB Research Laboratories

- Gentronix Ltd.

- BioIVT

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Opposition to the Usage of Animals in Pre-clinical Research

- 4.2.2 Significant Advancements In-vitro Toxicology Assays

- 4.2.3 Increasing Awareness Regarding Drug Product Safety

- 4.2.4 Rising Demand for Personalized Medicine

- 4.2.5 Growth in High-Throughput Screening Technologies

- 4.2.6 Regulatory Push for Animal-Free Testing

- 4.3 Market Restraints

- 4.3.1 Incapability of In-vitro Models to Determine Autoimmunity and Immunostimulation

- 4.3.2 Stringent Regulatory Framework for the In-vitro Tests

- 4.3.3 Limited Predictive Accuracy for Complex Systemic Toxicities

- 4.3.4 Data Management & Integration Challenges

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value in USD)

- 5.1 By Technology

- 5.1.1 Cell Culture

- 5.1.2 High Throughput

- 5.1.3 Molecular Imaging

- 5.1.4 OMICS

- 5.1.5 3D Cell Culture & Organoids

- 5.2 By Method

- 5.2.1 Cellular Assay

- 5.2.2 Biochemical Assay

- 5.2.3 In-Silico

- 5.2.4 Ex-Vivo

- 5.3 By Application

- 5.3.1 Systemic Toxicology

- 5.3.2 Dermal Toxicity

- 5.3.3 Endocrine Disruption

- 5.3.4 Ocular Toxicity

- 5.3.5 Other Applications

- 5.4 By End User

- 5.4.1 Pharmaceutical Industry

- 5.4.2 Biotechnology & CROs

- 5.4.3 Diagnostics

- 5.4.4 Academic & Research Institutes

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Charles River Laboratories International Inc.

- 6.3.2 Thermo Fisher Scientific Inc.

- 6.3.3 Eurofins Scientific SE

- 6.3.4 SGS SA

- 6.3.5 Merck KGaA

- 6.3.6 Agilent Technologies Inc.

- 6.3.7 Abbott Laboratories

- 6.3.8 Bio-Rad Laboratories Inc.

- 6.3.9 Danaher Corporation

- 6.3.10 GE HealthCare Technologies Inc.

- 6.3.11 Intertek Group plc

- 6.3.12 Quest Diagnostics Inc.

- 6.3.13 Catalent Inc.

- 6.3.14 Evotec SE

- 6.3.15 WuXi AppTec Co. Ltd.

- 6.3.16 Cyprotex Ltd.

- 6.3.17 Promega Corporation

- 6.3.18 MB Research Laboratories

- 6.3.19 Gentronix Ltd.

- 6.3.20 BioIVT LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment