|

시장보고서

상품코드

1844541

테크니컬 세라믹 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Technical Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

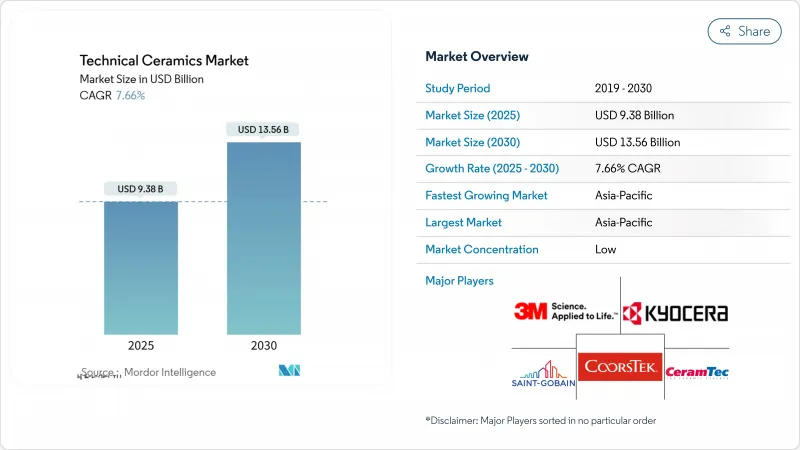

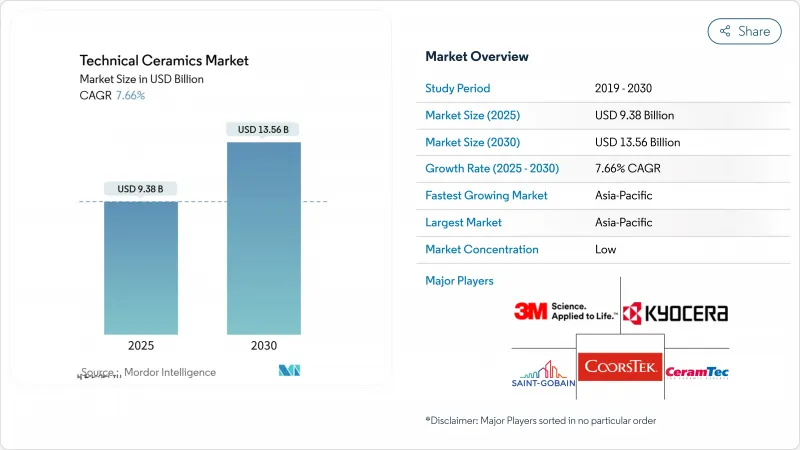

테크니컬 세라믹 시장 규모는 2025년에 93억 8,000만 달러로 평가되었고, 2030년에 135억 6,000만 달러에 이를 것으로 예측되며, 시장 추계 및 예측 기간(2025-2030년)의 CAGR은 7.66%를 나타낼 전망입니다.

수요는 반도체 기판, 전기차(EV) 열 제어 부품, 생체 적합성 임플란트 분야에 집중되고 있으며, 이 분야에서는 결함 허용도가 사실상 제로에 가깝고 재료 과학이 전략적 차별화 요소로 작용합니다. 중국, 일본, 한국에서 증가하는 팹 건설은 질화 알루미늄 및 실리콘 카바이드 패키지 소비를 증가시키고 있으며, 800V EV 구동계 아키텍처는 자동차 제조업체들이 전기 절연을 손상시키지 않으면서 200W/mK 이상을 방출할 수 있는 세라믹 방열판을 지정하도록 강제하고 있습니다. 공급망은 여전히 핵심 광물 집중화에 취약하지만, 주요 생산업체들은 위험도가 낮은 지역에서의 생산 능력 확대와 재활용 루프 강화로 신규 원자재 노출을 줄이는 대응책을 마련 중입니다. 단일체(모놀리식) 제형이 여전히 대량 시장을 주도하지만, 항공우주 및 방산 주요 업체들이 질량 감량과 연비 향상을 위한 경량·고온 내성 부품에 프리미엄을 지불함에 따라 세라믹 매트릭스 복합재의 성장 속도가 가장 빠르게 가속화되고 있습니다.

세계의 테크니컬 세라믹 시장 동향 및 인사이트

아시아태평양 지역의 반도체 및 소비자 가전 생산량 확대

대만, 중국 본토, 일본, 한국 전역에 걸친 팹 건설은 절연 무결성을 보장하면서 1,000°C를 초과하는 최고 접합 온도를 견딜 수 있는 질화 알루미늄 및 실리콘 카바이드 기판에 대한 수요 기준을 재설정하고 있습니다. 갈륨 나이트라이드 아키텍처를 추구하는 칩 설계사들은 기존 금속 리드 프레임이 감당할 수 있는 수준보다 빠르게 열 예산을 확대하고 있어 세라믹 패키지가 필수적인 처리량 확보 수단이 되고 있습니다. 교세라는 차세대 프로세서 노드와 세라믹 기판 공급을 동기화하기 위해 일본 전용 라인에 4억 7,000만 달러를 투자 중입니다. 기판 성장 주기와 리소그래피 양산 확대를 동기화하는 것은 여전히 어렵습니다. 가마는 반도체 클린룸보다 검증 주기가 더 길기 때문입니다. 그러나 1차 반도체 제조사들은 공급을 확보하기 위해 다년간의 구매 계약을 체결하고 있습니다. 동시에 지역 정부들은 해외 원자재 의존도를 낮추기 위해 첨단 재료 클러스터를 지원하고 있으며, 이는 리드 타임을 단축하고 가격 변동성을 완화할 수 있는 정책적 움직임입니다.

EV 파워트레인의 열 관리 요구

2024년 글로벌 전기차 출하량은 1,500만 대를 돌파했으며, 거의 모든 플랫폼 업등급는 소형 인버터를 통해 더 많은 전력을 공급하는 800V 전기 아키텍처를 목표로 하고 있습니다. 실리콘 카바이드 전력 모듈은 실리콘 장치보다 3배 빠른 속도로 열을 방출하지만, 허용 접합 온도 범위는 여전히 좁아 200W/mK 이상의 열전도도를 자랑하는 세라믹 방열판이 이상적인 설계 솔루션을 제공합니다. CeramTec의 칩-온-히트싱크 솔루션은 열저항을 낮추면서 절연 분리 기능을 유지해 고진동 자동차 환경에서 모듈 수명을 연장합니다. 자동차 제조사들은 가격에 민감하지만, 열 관련 고장으로 인한 보증 책임 부담으로 인해 단위 비용이 높더라도 고신뢰성 세라믹 재료 구매를 선택하게 됩니다. 중국, 유럽, 미국에서 차량 전기화가 가속화됨에 따라 세라믹 기판, 버스바, 겔 코팅 냉각판에 대한 수요도 동시에 증가하고 있습니다.

내재적 취성 및 가공 손실

내열성과 내마모성을 동시에 제공하는 경도는 소결 후 연삭 과정에서 파단 위험을 증가시킵니다. 20-30%의 수율 손실은 단가를 상승시키고 리드 타임을 연장시킵니다. 섬유 강화 세라믹 매트릭스 복합재는 균열 전파를 완화하지만, 공정 복잡성을 높여 내구성 향상 효과를 상쇄하는 적층 및 침투 공정을 추가합니다. 적층 제조는 근사 형상 대안을 제공하지만, 재료 선택지와 처리량은 여전히 기존 프레스 방식에 미치지 못해 시제품 제작 외 적용이 제한됩니다.

부문 분석

모놀리식 세라믹은 대규모 생산에서도 균일한 품질을 제공하는 성숙한 프레스 및 소결 라인을 바탕으로 2024년 기술 세라믹 시장의 46.68% 점유율을 유지했습니다. 산업용 OEM 업체들이 펌프, 노즐, 절연체를 강철 대비 내구성이 우수한 알루미나 본체로 개조함에 따라 해당 부문는 여전히 중간 단일자리 수 성장률을 기록할 것으로 예상됩니다. 그러나 복합 부문는 8.84%의 연평균 복합 성장률(CAGR)로 30% 이상의 경량화와 1,500°C 이상의 내열성을 추구하는 항공우주 및 방위 예산을 유치하며 전체 테크니컬 세라믹 시장을 견인할 것입니다. 2025년에는 엔진 고온부품 부문만으로도 테크니컬 세라믹 시장 규모에서 11억 달러를 차지할 전망입니다. 급속 강제공기 소결과 같은 공정 혁신으로 다결정화 단계가 수시간에서 수분으로 단축되며 에너지 비용 곡선이 낮아지고, 단일체와의 가격 격차도 좁혀지고 있습니다. 이러한 효율성이 확산됨에 따라 복합재가 단일체 점유율을 잠식할 것으로 예상되나, 자동차 및 산업 플랜트에서는 여전히 예측 가능한 수축률과 낮은 불량률을 중시하기 때문에 완전히 대체하지는 못할 전망입니다.

코팅 틈새 시장은 과도기적 경로 역할을 합니다: OEM 업체들은 기존 금속 부품에 지르코니아나 실리콘 카바이드를 분사하여 전체 조립체 재설계 없이도 열유속 향상을 달성할 수 있습니다. 이러한 개조 방식은 가동 중단 예산이 제한적인 석유화학 버너 및 디젤 미립자 필터 분야에서 널리 채택되고 있습니다. 세라믹 섬유는 생산량은 적지만 단열 시장에서 영향력이 크다. 1,100°C까지 견디는 에어로겔 충전 섬유 퀼트는 LNG 선박 화물창에 적용되며, 이는 특수 성능 인증이 소규모 하위 부문에서 프리미엄 가격을 유지하는 또 다른 지표다.

알루미나, 지르코니아, 멀라이트와 같은 산화물 계열은 풍부한 원자재 공급과 검증된 공정 제어 덕분에 2024년 매출의 63.37%를 차지했습니다. 이 등급들은 다양한 산업 분야의 커패시터 유전체 및 마모 방지판의 기준을 형성합니다. 그러나 실리콘 카바이드, 실리콘 나이트라이드, 신흥 비산화물인 붕소 카바이드 제품군은 낮은 밀도와 구리에 근접한 열전도도를 결합하여 더 빠른 주문 증가세를 보이고 있습니다. 비산화물 제품군은 2030년까지 7.86% 성장 궤도에 올라, 산화물 유리 상이 견딜 수 없는 첨단 장치 시장을 공략하며 테크니컬 세라믹 시장을 확장하고 있습니다. 비용 장벽은 여전히 존재하지만, 팹 라인 수율이 개선되고 불량률이 5% 미만으로 떨어짐에 따라 비산화물의 가격 프리미엄은 좁혀지고 있습니다. 규제된 연비 기준과 데이터센터의 열유량 증가는 모두 이러한 고성능 등급에 대한 장기적인 호재가 지속될 것임을 시사합니다.

복합 또는 하이브리드 재료군은 산화물 매트릭스와 비산화물 위스커 또는 섬유를 결합하여 시너지 효과를 내는 강도와 전도성을 제공합니다. 고전압에서 유전체 파괴를 견디는 란타늄 도핑 알루미나 혼합물에 대한 관심이 높아지고 있으며, 이는 그리드 규모 고체 변압기 프로젝트에서 가치 있는 특성입니다. 이러한 크로스오버 제형은 향후 시장 점유율 경쟁이 산화물 대 비산화물이 아닌 하이브리드 대 단일상 간에 벌어질 것이라는 주장을 입증하며, 복잡성을 더하지만 솔루션 영역을 넓히고 있습니다.

테크니컬 세라믹 시장 보고서는 제품 유형(단일체 세라믹, 세라믹 매트릭스 복합재 등), 재료 등급(산화물 세라믹, 비산화물 세라믹, 기타), 최종 사용자 산업(전기 및 전자, 자동차 등), 주요 응용 분야(절연체 및 기판, 열 관리 부품 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

지역 분석

아시아태평양 지역은 2024년 테크니컬 세라믹 시장의 43.87% 점유율로 우위를 점했으며, 2030년까지 연평균 7.91%의 성장률을 기록할 것으로 전망됩니다. 중국 본토는 알루미나 분말 소성 공정 대부분을 차지하며 노동 집약적 마무리 공정에서 비용 차익을 제공하지만, 전기 요금 인상과 환경 규제 준수 비용 증가로 인해 기존 비용 절감 효과가 점차 축소되고 있습니다. 일본은 국가 반도체 부흥 인센티브와 부합하는 초고순도 고부가가치 기판으로 재편 중이며, 교세라 나가사키 공장은 2026년 가동 시 국내 정밀 세라믹 생산량을 10% 증가시킬 전망입니다. 한국의 메모리 칩 중심지는 저결함 실리콘 나이트라이드 기판 수요를 견인하고 있으며, 인도는 구자라트와 타밀나두 주의 세금 감면 혜택으로 전기차 공급망 투자자를 유치 중입니다. 지역 정부들은 또한 폐기된 지르코니아와 이트리아를 확보하기 위한 재활용 회랑을 구축 중이며, 이는 장기적으로 원자재 수입 의존도를 낮출 수 있는 방안입니다.

북미는 성숙 단계에 있지만 혁신이 활발하여 세라믹 매트릭스 복합재 관련 글로벌 R&D 지출의 약 30%를 차지합니다. 미국은 항공우주 터빈 및 의료 임플란트 주문량의 대부분을 차지하며, 규제 수준이 낮은 지역이 생략하는 ISO 등급 가마와 USP Class VI 클린룸 규정을 정당화합니다. 생고뱅의 뉴욕 4천만 달러 규모 촉매 캐리어 공장은 100개의 일자리를 창출하고 동부 해안 석유 정제업체의 납기 주기를 단축할 전망입니다. 캐나다 광산 기업들은 보크사이트와 희토류 농축물을 공급하지만, 여전히 대부분의 원료를 아시아 정제소로 보낸다. 멕시코는 전기차 인버터 조립 허브로 부상하며, 기판 공급업체들이 USMCA 원산지 규정을 회피하는 근거리 조달 방안을 검토하게 하고 있습니다.

유럽은 전 세계 매출의 약 5분의 1을 차지하며 상업적 성공을 지속가능성 의무와 연계합니다. 독일 공작기계 제조사들은 윤활 수요를 60% 절감하는 내마모성 알루미나 가이드를 지정하며 EU 생태설계 기준과 부합합니다. 프랑스와 스페인은 수천 평방미터의 고체산화물 전해조 판이 곧 필요할 수소 허브 시범 운영 중입니다. 지역의 REACH 화학 안전 프레임워크는 엄격한 추적성을 요구하며, 이는 기존 업체를 지지하지만 신규 벤처 출범을 지연시키는 준수 비용입니다. 브렉시트 이후 영국 정책은 첨단 재료 촉진 장치에 중점을 두어 대학 연구실의 혁신을 3년 내 파일럿 라인으로 전환하는 것을 목표로 하지만, 국내 수요가 제한적이어서 상당한 규모 확대는 수출 시장에 달려 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 아시아태평양 지역의 반도체 및 소비자 가전 생산량 확대

- EV 파워트레인의 열 관리 요구

- 고부가가치 의료용 임플란트 및 기기에서의 사용 증가

- 수소 전기분해기 스택 구성 요소

- 우주 내 제조 및 위성 하드웨어

- 시장 성장 억제요인

- 높은 자본 및 가공 비용

- 본질적 취성 및 가공 손실

- 핵심 광물 공급망 노출

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 정도

- 특허 분석

- 가격 분석

제5장 시장 규모와 성장 예측

- 제품 유형별

- 모놀리식 세라믹

- 세라믹 매트릭스 복합재

- 세라믹 코팅

- 기타 제품

- 재료 등급별

- 산화물 세라믹

- 비산화물 세라믹

- 기타

- 최종 사용자 산업별

- 전기 및 전자

- 자동차

- 에너지 및 전력

- 의료

- 항공우주 및 방위

- 기타 최종 사용자 산업

- 주요 용도별

- 절연체 및 기판

- 열 관리 부품

- 내마모 부품과 베어링

- 바이오 임플란트와 치과

- 장갑 및 보호

- 지역별

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Dyson Technical Ceramics

- Kyocera Corporation

- Mantec Technical Ceramics Ltd

- McDanel Advanced Ceramic Technologies

- Morgan Advanced Materials

- NGK SPARK PLUG CO., LTD.

- Ortech, inc.

- Rauschert GmbH

- Saint-Gobain

- Schott AG

- STC Material Solutions

제7장 시장 기회와 전망

HBR 25.11.03The Technical Ceramics Market size is estimated at USD 9.38 billion in 2025, and is expected to reach USD 13.56 billion by 2030, at a CAGR of 7.66% during the forecast period (2025-2030).

Demand is clustering around semiconductor substrates, electric-vehicle (EV) thermal control parts, and biocompatible implants, where failure tolerance is virtually zero and material science is a strategic differentiator. Rising fab construction across China, Japan, and South Korea is lifting consumption of aluminum nitride and silicon carbide packages, while 800 V EV drive-train architectures force automakers to specify ceramic heat spreaders that can dissipate more than 200 W/mK without compromising electrical insulation. Supply chains remain vulnerable to critical-mineral concentration, yet leading producers are countering with capacity additions in lower-risk jurisdictions and tighter recycling loops that reduce virgin material exposure. Monolithic formulations still dominate volume, but ceramic-matrix composites are accelerating fastest as aerospace and defense primes pay premiums for lighter, hotter-capable components that cut mass and raise fuel efficiency.

Global Technical Ceramics Market Trends and Insights

Expanding Semiconductor & Consumer-Electronics Output in Asia Pacific

Fab build-outs across Taiwan, mainland China, Japan, and South Korea are resetting the demand baseline for aluminum nitride and silicon carbide substrates that can survive peak junction temperatures exceeding 1,000 °C while ensuring dielectric integrity. Chip designers pursuing gallium nitride architectures are widening thermal budgets faster than legacy metal lead-frames can handle, making ceramic packages an essential throughput enabler. Kyocera is funneling USD 470 million into a dedicated Japanese line to synchronize ceramic substrate availability with next-generation processor nodes. Synchronizing substrate growth cycles with lithography ramp-ups remains difficult because kilns require longer validation loops than semiconductor clean-rooms, but tier-one device makers are now signing multi-year offtake agreements to lock in supply. Regional governments are simultaneously underwriting advanced-materials clusters to reduce reliance on overseas feedstocks, a policy move that could compress lead times and moderate pricing volatility.

EV Power-Train Thermal-Management Needs

Global EV shipments surpassed 15 million units in 2024, and nearly every platform upgrade now targets 800 V electrical architectures that squeeze more power through smaller inverters. Silicon carbide power modules dissipate heat at triple the rate of silicon devices, yet the allowable junction temperature band remains tight, creating a design window ideally served by ceramic heat spreaders boasting greater than 200 W/mK conductivity. CeramTec's chip-on-heatsink solution lowers thermal resistance while maintaining dielectric separation, a combination that lengthens module life in high-vibration automotive environments. Automakers are price-sensitive, but warranty liabilities linked to thermal failures tip purchasing decisions toward high-reliability ceramics despite higher unit costs. As fleet electrification accelerates in China, Europe, and the United States, demand for ceramic substrates, busbars, and gel-coated cooling plates is scaling in parallel.

Intrinsic Brittleness & Machining Losses

Hardness that delivers heat and wear resistance simultaneously increases fracture risk during post-sinter grinding. Yield losses of 20-30% inflate unit costs and lengthen lead times. Fiber-reinforced ceramic-matrix composites mitigate crack propagation but add layer-up and infiltration steps that offset durability gains with higher process complexity. Additive manufacturing offers near-net-shape alternatives, yet material palettes and throughput still lag conventional presses, limiting adoption outside prototyping.

Other drivers and restraints analyzed in the detailed report include:

- Rising Use in High-Value Medical Implants & Devices

- Hydrogen-Electrolyzer Stack Components

- Critical-Minerals Supply-Chain Exposure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monolithic ceramics retained 46.68% technical ceramics market share in 2024 due to mature press-and-sinter lines that deliver uniform quality at scale. The segment should still post mid-single-digit gains as industrial OEMs retrofit pumps, nozzles, and insulators with alumina bodies that outlast steel equivalents. Composite grades, however, will lift the overall technical ceramics market as their 8.84% CAGR attracts aerospace and defense budgets chasing weight savings above 30% alongside thermal ceilings beyond 1,500 °C. In 2025, the engine hot-section segment alone accounts for a USD 1.1 billion slice of the technical ceramics market size. Processing breakthroughs such as rapid forced-air sintering are collapsing densification steps from hours to minutes, trimming energy cost curves, and narrowing price spreads with monolithics. As these efficiencies propagate, composites are expected to erode monolithic share, but not displace them outright, because automotive and industrial plants still prize predictable shrinkage and low scrap rates.

The coatings niche serves as a transitional pathway: OEMs can spray zirconia or silicon carbide onto legacy metal parts, achieving incremental heat-flux gains without redesigning the entire assembly. This retrofit approach is popular in petrochemical burners and diesel particulate filters where shutdown budgets are tight. Ceramic fibers remain small in tonnage yet influential in insulation markets; aerogel-filled fiber quilts rated to 1,100 °C are seeing uptake in LNG ship cargo holds, another indicator that specialized performance credentials sustain premium pricing in smaller sub-segments.

Oxide families such as alumina, zirconia, and mullite delivered 63.37% of 2024 revenue owing to abundant raw material availability and well-documented process controls. These grades form the baseline for capacitor dielectrics and wear plates across multiple industries. Yet silicon carbide, silicon nitride, and emerging boron carbide non-oxide formulations are booking faster order growth because they combine lower density with thermal conductivities approaching copper. The non-oxide cohort is on a 7.86% trajectory through 2030, expanding the technical ceramics market by servicing frontier devices where oxide glass phases cannot survive. Cost barriers persist, but as fab line yields improve and reject rates fall below 5%, non-oxide price premiums are narrowing. Regulatory fuel-economy mandates and data-center heat-flux escalation both point to sustained long-run tailwinds for these higher-performance grades.

Composite or hybrid material classes merge oxide matrices with non-oxide whiskers or fibers, delivering synergistic toughness and conductivity. Interest is building in lanthanum-doped alumina blends that resist dielectric breakdown at elevated voltages, a property valued by grid-scale solid-state transformer projects. These cross-over formulations validate the thesis that future share battles will not be oxide versus non-oxide but hybrid versus single-phase, adding complexity yet widening solution space.

The Technical Ceramics Market Report is Segmented by Product Type (Monolithic Ceramics, Ceramic Matrix Composites, and More), Material Class (Oxide Ceramics, Non-Oxide Ceramics, Others), End-User Industry (Electrical and Electronics, Automotive, and More), Key Application (Insulators & Substrates, Thermal Management Components, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa).

Geography Analysis

Asia Pacific dominated the technical ceramics market with 43.87% share in 2024 and is tracking a 7.91% CAGR to 2030. Mainland China hosts the majority of alumina powder calcination and offers cost arbitrage in labor-intensive finishing steps, yet rising electricity tariffs and environmental compliance fees are eroding the historic savings gap. Japan is repositioning toward ultra-clean, high-value substrates that align with national semiconductor revival incentives; Kyocera's Nagasaki site will lift domestic fine-ceramic output by 10% upon its 2026 start-up. South Korea's memory-chip epicenter drives demand for low-defect silicon nitride boards, while India is luring EV supply-chain investors with tax holidays in Gujarat and Tamil Nadu. Regional governments are also mapping recycling corridors to capture scrap zirconia and yttria, an initiative that may dilute raw-material import dependencies over the long term.

North America is mature yet innovation-heavy, claiming nearly 30% of global R&D outlays tied to ceramic matrix composites. The United States accounts for the bulk of aerospace turbine and medical implant orders, justifying ISO-class kilns and USP Class VI clean-room protocols that less regulated regions bypass. Saint-Gobain's USD 40 million catalyst-carrier plant in New York will add 100 jobs and shorten delivery cycles for East-Coast petro-refiners. Canadian mining houses supply bauxite and rare-earth concentrates, but still send most feedstock to Asian refineries. Mexico is emerging as an assembly hub for EV inverters, prompting substrate suppliers to weigh near-shoring steps that sidestep USMCA rules-of-origin tariffs.

Europe claims roughly one-fifth of global revenue and aligns commercial success with sustainability mandates. Germany's machine-tool builders specify wear-resistant alumina guides that cut lubrication demand by 60%, dovetailing with EU eco-design standards. France and Spain are piloting hydrogen hubs that will soon require thousands of square meters of solid-oxide electrolyzer plates. The region's REACH chemical-safety framework compels tight traceability, a compliance cost that props up incumbents but slows new venture launches. Post-Brexit United Kingdom policy leans toward advanced materials catapults, aiming to translate university lab breakthroughs into pilot lines within three years, yet significant scale will hinge on export markets, given limited domestic demand.

- 3M

- CeramTec GmbH

- CoorsTek Inc.

- Dyson Technical Ceramics

- Kyocera Corporation

- Mantec Technical Ceramics Ltd

- McDanel Advanced Ceramic Technologies

- Morgan Advanced Materials

- NGK SPARK PLUG CO., LTD.

- Ortech, inc.

- Rauschert GmbH

- Saint-Gobain

- Schott AG

- STC Material Solutions

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding semiconductor and consumer-electronics output in Asia Pacific

- 4.2.2 EV power-train thermal-management needs

- 4.2.3 Rising use in high-value medical implants and devices

- 4.2.4 Hydrogen-electrolyser stack components

- 4.2.5 In-space manufacturing and satellite hardware

- 4.3 Market Restraints

- 4.3.1 High capital and processing cost

- 4.3.2 Intrinsic brittleness and machining losses

- 4.3.3 Critical-minerals supply-chain exposure

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Rivalry

- 4.6 Patent Analysis

- 4.7 Price Analysis

5 Market Size and Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Monolithic Ceramics

- 5.1.2 Ceramic Matrix Composites

- 5.1.3 Ceramic Coatings

- 5.1.4 Other Products

- 5.2 By Material Class

- 5.2.1 Oxide Ceramics

- 5.2.2 Non-Oxide Ceramics

- 5.2.3 Others

- 5.3 By End-user Industry

- 5.3.1 Electrical and Electronics

- 5.3.2 Automotive

- 5.3.3 Energy and Power

- 5.3.4 Medical

- 5.3.5 Aerospace and Defense

- 5.3.6 Other End-user Industries

- 5.4 By Key Application

- 5.4.1 Insulators and Substrates

- 5.4.2 Thermal Management Components

- 5.4.3 Wear-resistant Parts and Bearings

- 5.4.4 Bio-implants and Dental

- 5.4.5 Armor and Protection

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/ Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 3M

- 6.4.2 CeramTec GmbH

- 6.4.3 CoorsTek Inc.

- 6.4.4 Dyson Technical Ceramics

- 6.4.5 Kyocera Corporation

- 6.4.6 Mantec Technical Ceramics Ltd

- 6.4.7 McDanel Advanced Ceramic Technologies

- 6.4.8 Morgan Advanced Materials

- 6.4.9 NGK SPARK PLUG CO., LTD.

- 6.4.10 Ortech, inc.

- 6.4.11 Rauschert GmbH

- 6.4.12 Saint-Gobain

- 6.4.13 Schott AG

- 6.4.14 STC Material Solutions

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Increasing Usage in Nano Technology