|

시장보고서

상품코드

1844558

자동차 열교환기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive Heat Exchanger - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

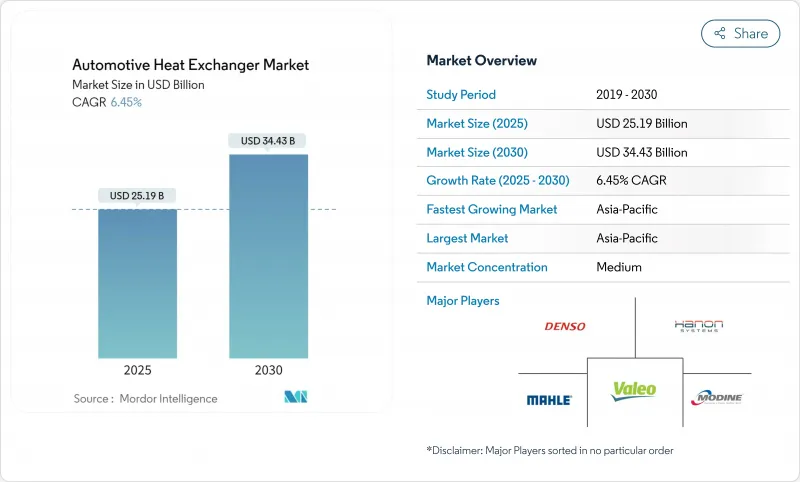

자동차 열교환기 시장은 2025년에 251억 9,000만 달러에 이르고, 2030년에는 344억 3,000만 달러로 확대되며, CAGR 6.45%를 나타낼 것으로 예측됩니다.

내연기관의 냉각 루프에서 배터리, 파워 일렉트로닉스, 차내 에어컨 제어를 위한 멀티 루프 아키텍처로의 전환이 자동차 열교환기 시장의 확대를 지원하고 있습니다. 전동화 플랫폼에서는 배터리의 열폭주를 방지하고, 800V의 충전 부하를 관리하고, 차량의 항속 거리를 절약하는 부품이 요구되고 있습니다. 아시아태평양의 전기자동차 보급, 유로 7 내구성 규칙, 히트 펌프의 통합은 자동차 열교환기 시장 제품의 복잡성과 가치를 높이고 있습니다. 공급업체는 마이크로채널 설계, 내식성 합금, 히트펌프 통합 모듈로 대응하고 있지만, 알루미늄과 구리의 재료 변동은 자동차 열교환기 시장 전체의 마진을 계속 압박하고 있습니다.

세계의 자동차 열교환기 시장 동향과 인사이트

EV 판매에 견인되는 고도 열 관리 수요

전기자동차는 내연 자동차보다 약 30% 더 알루미늄을 필요로 하기 때문에 라디에이터용 이외의 열교환기의 재설계를 강요하고 있습니다. 배터리 루프는 폭주를 피하기 위해 셀 온도를 2℃ 범위로 유지해야 하며, 실리콘 카바이드 인버터는 마이크로채널 코어에 의해 처리되는 국부적인 히트 스파이크를 야기합니다. 프레스톤의 GB29743-2 호환 쿨런트 모양 및 코팅 선택, 직접 침지 냉각과 같은 낮은 전도도 유체는 전도도 위험을 제거하는 유전체 장치의 틈새를 엽니다.

세계 엄격한 배기 가스 규제

2024년 5월에 발표된 Euro 7 규제에서는 테일 파이프 규제가 통일되고 브레이크 및 타이어 파티큘레이트 규제가 추가되므로 자동차 제조업체는 효율 향상을 추구하면서 간접적으로 열 부하가 증가했습니다. 배터리의 내구성이 요구되고 교환기의 수명 목표가 10년을 넘어 방청 브레이징 시트에 박차를 가하는 반면 온보드 진단은 예측 유량 제어를 가능하게 합니다. 2026년 11월까지의 프로그램 스케줄은 검증 창을 강화하고 사전 인증된 테스트 벤치가 있는 공급업체에게 유리하게 작용합니다.

알루미늄과 구리의 가격 변동

전기 모델에는 최대 80kg의 구리를 사용할 수 있으며, 이는 내연차의 4배에 해당합니다. 자동차 제조업체는 다년간 계약과 폐쇄 루프 재활용으로 헤지하고 있지만, 여전히 지역 프리미엄은 조달 전략을 왜곡하고 있습니다. 단위 중량당 전도성을 높이는 합금의 기술 혁신은 1차 금속 수요를 제한하고 환율이 급등했을 때 비용을 안정시키는 데 도움이 됩니다.

부문 분석

자동차 열교환기 시장 규모에서는 라디에이터가 가장 크고, 2024년에는 39.29%의 매출을 차지했습니다. 배터리와 파워 일렉트로닉스의 쿨러가 2030년까지 13.20%의 연평균 복합 성장률(CAGR)을 나타내 전동화의 우선 순위를 반영해 점유율이 저하됩니다. 리튬 이온 팩은 급속 충전을 위해 -2℃의 열 안정성이 요구되므로 자동차 열교환기 시장에서는 일체형 칠 플레이트와 유전체 침지 모듈이 요구됩니다. 차지 에어 시스템은 터보차징과 보조를 맞추고 오일 쿨러는 e-액슬 윤활에 축발을 옮깁니다. 캐빈용 증발기와 커패시터는 가역 히트펌프식 열교환기로 진화하고 수소연료전지용 가습기는 신흥의 틈새 분야로 부상하고 있습니다.

자동차 열교환기 시장은 라디에이터 부피를 계속 중시하고 있습니다. 그러나 연료전지 버스나 트럭용 스택식 가습 모듈에는 백스페이스가 있어, 에바슈파하의 배기 공기 유닛은 물 회수와 음향 댐핑을 융합시키고 있습니다. 하이브리드 폐열 회수는 여전히 Euro-7 호환 파워트레인과 관련이 있으며, 순수한 배터리 채택이 증가하는 동안 공급업체에게 브리지 제품을 제공합니다.

튜브 핀 코어는 성숙한 금형과 저비용으로 2024년 자동차 열교환기 시장 점유율의 47.28%를 차지했습니다. 플레이트 바 어셈블리는 CAGR 8.84%를 나타내는데, 이는 OEM이 스케이트 보드 섀시에서 충돌 패키징을 위해 두께를 트레이드 오프하기 때문입니다. 자동차 열교환기 시장 규모는 마이크로채널 플랫 튜브 유닛이 가장 빠르게 확대되고 있습니다. 히트 파이프와 베이퍼 챔버는 프리미엄 배터리 팩에 채택되었으며, 이러한 동향은 고체 셀이 열 부하를 낮추면서 온도 균일성 요구가 엄격해짐에 따라 연쇄적으로 확장될 가능성이 높습니다.

고압 루프에서는 쉘 앤 튜브식 열교환기가 비계를 굳히고 주로 수소 연료전지 및 폐열 회수 시스템에 사용되고 있습니다. 동시에, 플레이트 바형은 내부 오프셋 핀을 채용하여 유속과 소음을 억제하고, 상용차의 충전 공기 냉각의 지위를 강화하고 있습니다.

지역 분석

2024년 자동차 열교환기 시장은 아시아태평양이 47.23%의 점유율을 차지했고 CAGR 8.78%를 나타낼 것으로 예측됩니다. 중국은 2025년 자동차 생산 대수가 3,500만대를 넘어, EV의 판매 대수는 매년 50% 증가하고 있으며, 마이크로채널 튜브를 대규모 생산하는 수직 통합형 알루미늄 압출기가 혜택을 받습니다. 일본의 연료전지 로드맵과 한국의 복사난방의 약진은 자동차 열교환기 시장 전체의 기술 수요를 더욱 다양화시킵니다.

북미에서는 EV의 소매 수요 연화로 Ford가 F-150 Lightning의 생산 대수를 삭감하는 한편, 인플레이션 억제법에 의해 공급 체인의 지역화가 촉진되는 등 다양한 신호가 교차하고 있습니다. Gentherm은 2025년 1분기에 3억 5,400만 달러의 매출을 달성하는 반면, 4억 달러의 신규 주문을 계상했습니다. 국내 압출 및 납땜에 대한 투자는 외재 충격에 대한 쿠션이 될 수 있습니다.

유럽 점유율은 유로 7의 2026년 11월 적합 기한에 따라 형성됩니다. 자동차 제조업체는 76%의 회수율을 활용하여 재활용 알루미늄의 사용을 늘리고 있습니다. 체코의 온세미 20억 달러 SiC 시설은 접합 온도 상승으로 지역 히트싱크 수요를 증가시킵니다. 또한 국가 예산이 수소 트럭의 통로를 목표로 하고 있으며 자동차 열교환기 시장에서 연료전지용 가습기 라인을 존속시키고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- EV 판매에 견인되는 고도 열 관리 수요

- 세계의 엄격한 배기가스 규제

- 신흥 시장에서 HVAC 보급률 상승

- 전기자동차의 히트 펌프 시스템 통합

- 800V 고전압 XEV 아키텍처

- 연료전지식 가습기의 채용

- 시장 성장 억제요인

- 알루미늄과 구리의 가격 변동

- 엄격한 내구성과 부식 검증 비용

- 고체 전지 팩의 열부하 저하

- 마이크로채널 압출 공급의 병목

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모와 성장 예측

- 용도별

- 라디에이터

- 충전 공기 쿨러/인터쿨러

- 오일 쿨러

- EGR 및 배기 가스 열 회수

- 실내 HVAC(증발기 및 응축기)

- 배터리/파워 일렉트로닉스 쿨러

- 연료 전지 가습기

- 기타 용도

- 설계 유형별

- 튜브-핀

- 플레이트 바

- 마이크로채널 플랫 튜브

- 쉘 앤 튜브

- 기타

- 재료별

- 알루미늄

- 구리/황동

- 스테인리스강

- 복합재 및 폴리머

- 차량 유형별

- 승용차

- 소형 상용차

- 대형 상용차 및 오프 하이웨이차

- 파워트레인 유형별

- 내연 엔진(ICE)

- 하이브리드 전기자동차(HEV/PHEV)

- 배터리 전기자동차(BEV)

- 연료전지 전기자동차(FCEV)

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- DENSO Corporation

- MAHLE GmbH

- Valeo SA

- Hanon Systems

- Modine Manufacturing Company

- Dana Incorporated

- Marelli(Calsonic Kansei)

- Sanden Holdings

- GEA Group

- Kelvion Holdings

- T.RAD Co. Ltd.

- Behr Hella Service

- AKG Thermal Systems

- American Industrial Heat Transfer

- Banco Products(India) Ltd.

- Climetal SL

- Constellium SE

- GandM Radiator

- Nippon Light Metal Holdings

- Valeo SA(Thermal Systems)

제7장 시장 기회와 전망

KTH 25.11.05The automotive heat exchanger market reached USD 25.19 billion in 2025 and is projected to rise to USD 34.43 billion by 2030, advancing at a 6.45% CAGR.

The shift from internal-combustion cooling loops to multi-loop architectures for battery, power electronics, and cabin climate control underpins this expansion across the automotive heat exchanger market. Electrified platforms demand components that prevent battery thermal runaway, manage 800-V charging loads, and conserve vehicle range. Strong electric-vehicle adoption in Asia-Pacific, Euro 7 durability rules, and heat-pump integration also elevate product complexity and value content in the automotive heat exchanger market. Suppliers are responding with micro-channel designs, corrosion-resistant alloys, and integrated heat-pump modules, while materials volatility in aluminum and copper continues to pressure margins across the automotive heat exchanger market.

Global Automotive Heat Exchanger Market Trends and Insights

EV Sales-Driven Demand for Advanced Thermal Management

Electric vehicles require roughly 30% more aluminum than combustion cars, forcing the redesign of exchangers beyond radiator duty. Battery loops must keep cell temperatures within a 2 °C band to avoid runaway, while silicon-carbide inverters impose localized heat spikes handled by micro-channel cores. Low-conductivity fluids, such as Prestone's GB29743-2-compliant coolant shape alloy and coating choices, and direct-immersion cooling, open a niche for dielectric units that eliminate conductivity risk.

Stringent Global Emission Regulations

Euro 7 rules published in May 2024 unify tailpipe limits and add brake- and tire-particulate caps, indirectly raising thermal loads as automakers chase efficiency gains. Required battery durability pushes exchanger life targets beyond a decade, spurring corrosion-proof brazing sheets while onboard diagnostics enable predictive flow control. Program timelines to November 2026 tighten validation windows, favoring suppliers with pre-certified test benches.

Aluminum and Copper Price Volatility

Electric models can contain up to 80 kg copper-four times that of combustion cars-making exchanger cost highly sensitive to spot prices. Automakers hedge with multiyear contracts and closed-loop recycling, yet regional premiums still skew sourcing strategies. Alloy innovation that lifts conductivity per unit weight helps limit primary metal demand, stabilizing costs when exchange rates spike.

Other drivers and restraints analyzed in the detailed report include:

- Heat-pump System Integration in Electric Vehicles

- Rising HVAC Penetration in Emerging Markets

- Micro-channel Extrusion Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Radiators accounted for the largest slice of the automotive heat exchanger market size, holding 39.29% revenue in 2024. Their share slips as battery and power-electronics coolers record a 13.20% CAGR to 2030, reflecting electrification priorities. Lithium-ion packs demand +-2 °C thermal stability for fast charging, prompting integrated chill plates and dielectric immersion modules in the automotive heat exchanger market. Charge-air systems keep pace with turbocharging, while oil coolers pivot toward e-axle lubrication. Cabin evaporators and condensers evolve into reversible heat-pump exchangers, and hydrogen fuel-cell humidifiers surface as a nascent niche.

The automotive heat exchanger market continues to prize radiator volumes. Yet, white-space lies in stack humidification modules for fuel-cell buses and trucks, where Eberspacher's exhaust-air unit blends water recovery with acoustic damping. Hybrid exhaust-heat recovery remains relevant in Euro-7-compliant powertrains, giving suppliers a bridge product as pure battery adoption climbs.

Tube-fin cores represented 47.28% of automotive heat exchanger market share in 2024 owing to mature tooling and low cost. Plate-bar assemblies grow 8.84% CAGR as OEMs trade off thickness for crash packaging in skateboard chassis. The automotive heat exchanger market size for micro-channel flat tube units is scaling fastest because superior transfer coefficients enable slim modules around crowded battery trays. Heat pipes and vapor chambers appear in premium battery packs, a trend likely to cascade as solid-state cells lower heat loads but tighten temperature uniformity needs.

In high-pressure loops, shell-and-tube exchangers preserve a foothold, mainly in hydrogen fuel-cell and waste-heat recovery systems where robustness outweighs weight penalties. Concurrently, plate-bar variants adopt internal offset fins to temper flow velocity and noise, reinforcing their position in commercial-vehicle charge-air cooling.

The Automotive Heat Exchanger Market Report is Segmented by Application (Radiator, Charge-Air Coolers / Intercoolers, and More), Design Type (Tube-Fin, Plate-Bar, and More), Material (Aluminum, Copper / Brass, and More) Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Powertrain Type (Internal Combustion Engine Vehicles, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the automotive heat exchanger market with 47.23% share in 2024 and is forecast to expand 8.78% CAGR. China exceeded 35 million vehicle builds in 2025, with EV sales up 50% yearly, benefiting vertically integrated aluminum extruders that produce micro-channel tubes at scale. Japan's fuel-cell roadmap and South Korea's radiant heating breakthroughs further diversify technical demand across the automotive heat exchanger market.

North America confronts mixed signals: softer retail EV demand led Ford to trim F-150 Lightning volumes, yet the Inflation Reduction Act spurs localized supply chains. Gentherm booked USD 400 million in new awards while achieving USD 354 million Q1 2025 revenue, reflecting resilience in climate-comfort niches. Domestic extrusion and brazing investment could cushion against foreign material shocks.

Europe's share is shaped by Euro 7's November 2026 compliance deadline. Automakers are boosting recycled aluminum use, leveraging a 76% collection rate. Onsemi's USD 2 billion SiC facility in Czechia elevates regional heat-sink demand owing to higher junction temperatures. National funding also targets hydrogen truck corridors, keeping fuel-cell humidifier lines viable within the automotive heat exchanger market

- DENSO Corporation

- MAHLE GmbH

- Valeo SA

- Hanon Systems

- Modine Manufacturing Company

- Dana Incorporated

- Marelli (Calsonic Kansei)

- Sanden Holdings

- GEA Group

- Kelvion Holdings

- T.RAD Co. Ltd.

- Behr Hella Service

- AKG Thermal Systems

- American Industrial Heat Transfer

- Banco Products (India) Ltd.

- Climetal SL

- Constellium SE

- GandM Radiator

- Nippon Light Metal Holdings

- Valeo SA (Thermal Systems)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV Sales-Driven Demand For Advanced Thermal Management

- 4.2.2 Stringent Global Emission Regulations

- 4.2.3 Rising HVAC Penetration In Emerging Markets

- 4.2.4 Heat-Pump System Integration In Electric Vehicles

- 4.2.5 800-V High-Voltage XEV Architectures

- 4.2.6 Fuel-Cell Humidifier Exchanger Adoption

- 4.3 Market Restraints

- 4.3.1 Aluminum and Copper Price Volatility

- 4.3.2 Stringent Durability and Corrosion Validation Costs

- 4.3.3 Declining Heat-Load In Solid-State Battery Packs

- 4.3.4 Micro-Channel Extrusion Supply Bottlenecks

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value (USD))

- 5.1 By Application

- 5.1.1 Radiators

- 5.1.2 Charge-Air Coolers / Intercoolers

- 5.1.3 Oil Coolers

- 5.1.4 EGR and Exhaust Gas Heat Recovery

- 5.1.5 Cabin HVAC (Evaporator and Condenser)

- 5.1.6 Battery / Power-electronics Coolers

- 5.1.7 Fuel-cell Humidifiers

- 5.1.8 Other Applications

- 5.2 By Design Type

- 5.2.1 Tube-Fin

- 5.2.2 Plate-Bar

- 5.2.3 Micro-channel Flat Tube

- 5.2.4 Shell-and-Tube

- 5.2.5 Others

- 5.3 By Material

- 5.3.1 Aluminum

- 5.3.2 Copper / Brass

- 5.3.3 Stainless Steel

- 5.3.4 Composites and Polymers

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles

- 5.4.3 Heavy Commercial and Off-Highway Vehicles

- 5.5 By Powertrain Type

- 5.5.1 Internal Combustion Engine (ICE)

- 5.5.2 Hybrid Electric Vehicles (HEV/PHEV)

- 5.5.3 Battery Electric Vehicles (BEV)

- 5.5.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Russia

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DENSO Corporation

- 6.4.2 MAHLE GmbH

- 6.4.3 Valeo SA

- 6.4.4 Hanon Systems

- 6.4.5 Modine Manufacturing Company

- 6.4.6 Dana Incorporated

- 6.4.7 Marelli (Calsonic Kansei)

- 6.4.8 Sanden Holdings

- 6.4.9 GEA Group

- 6.4.10 Kelvion Holdings

- 6.4.11 T.RAD Co. Ltd.

- 6.4.12 Behr Hella Service

- 6.4.13 AKG Thermal Systems

- 6.4.14 American Industrial Heat Transfer

- 6.4.15 Banco Products (India) Ltd.

- 6.4.16 Climetal SL

- 6.4.17 Constellium SE

- 6.4.18 GandM Radiator

- 6.4.19 Nippon Light Metal Holdings

- 6.4.20 Valeo SA (Thermal Systems)