|

시장보고서

상품코드

1844586

나노 페인트 및 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Nano Paints And Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

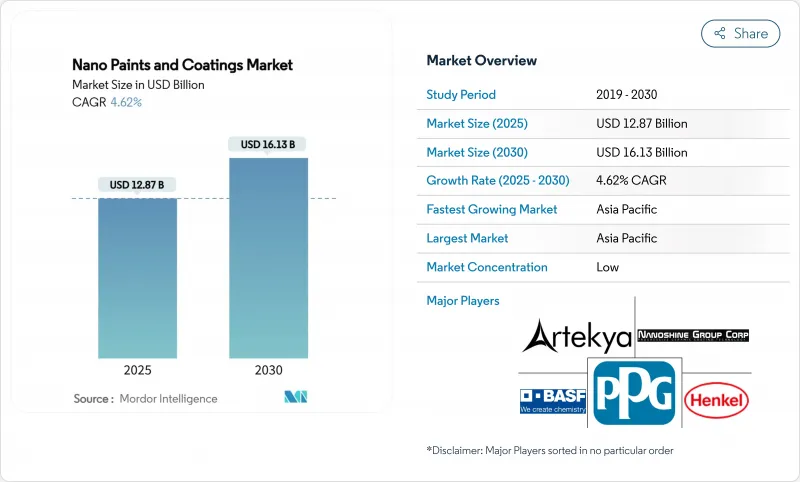

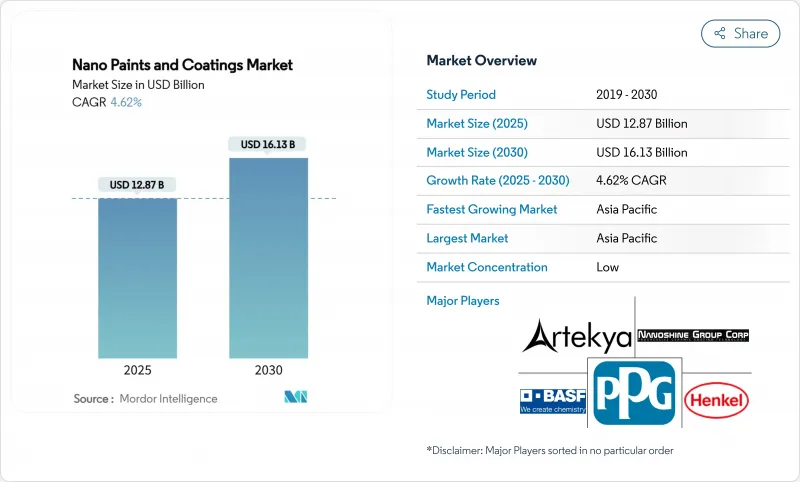

나노 페인트 및 코팅 시장 규모는 2025년에 128억 7,000만 달러로 추정되고 예측기간(2025-2030년)의 CAGR은 4.62%로, 2030년에는 161억 3,000만 달러에 달할 것으로 예상됩니다.

부식 경량 솔루션에 대한 항공우주 수요 증가, 전기자동차 화재 안전 요구 사항, 인프라의 내구성 요구에 따라 시장은 안정적인 상승 기조를 유지하고 있습니다. 나노 TiO2의 점유율은 39.17%로 압도적이며 그래핀의 CAGR 5.17%라는 급속한 성장과 함께 경쟁 우위를 유지하는데 있어서 첨단 나노 재료가 핵심적인 역할을 담당하고 있음을 보여줍니다. 지역적 기세는 아시아태평양이 여전히 강하고, 아시아태평양은 세계 매출의 거의 절반을 차지하며, 지역별로는 가장 빠른 성장을 이루고 있습니다. 화학기상성장(CVD)에 있어서공급의 진보와, 부식 방지, 열 관리, 항균 성능을 융합한 다기능 배합에의 변화가 새로운 비즈니스 기회를 형성하고 있는 한편, 높은 제조 비용과 진화하는 나노독성 규칙이 급속한 스케일 업을 억제하고 있습니다.

세계의 나노 페인트 및 코팅 시장 동향과 인사이트

항공우주 및 방위 부식 - 경량화 추진

미 국방부는 군용 장비의 부식에 매년 230억 달러의 비용이 소요될 것으로 추정하고 있으며 구조적 가벼움과 우수한 보호를 결합한 나노 코팅 채택을 강화하고 있습니다. 현장 데이터에서 나노 가공층은 해군 기체의 유지 보수 사이클을 단축하고 소빙 특성이 극단적인 기후에서 항공기의 반응성을 높입니다. 미국 해군의 SBIR 깃발 아래에 있는 프로그램은 벤치리서치에서 프리트라이얼로 전환하고 있으며, 엄격한 인증 장벽이 새로운 진입을 제한하는 동시에 유효한 공급업체에 대한 지속적인 수요를 보장하고 있음을 보여줍니다. 방위 조달 전략은 총 소유 비용을 줄인 플랫폼을 선호하므로 무게, 내구성 및 환경 노출 문제를 해결하는 단일 용도의 나노 제형이 점점 더 지정되고 있습니다.

EV용 열화재 안전 코팅 수요 증가

급속한 전기화로 인해 배터리 시스템은 더 높은 에너지 밀도와 더 엄격한 안전 기준으로 향하고 있습니다. 특수 나노층은 열을 빠르게 방출하고 난연성 장벽을 형성하여 셀과 인접한 부품을 보호합니다. 레조낙의 EV 팩용 단열 제품은 적극적인 상업 개발을 강조합니다. 탄소와 그래핀의 분산체는 유전 강도를 희생하지 않고 열전도성을 발휘하며 OEM의 안전 프로토콜에 적합합니다. 이와 병행하여 차내 온도를 10°C 낮추는 현대의 나노냉각 필름과 같은 승객 쾌적화 솔루션은 보조 용도로의 파급을 입증하고 있습니다. 열폭주 억제를 통합한 규제 프레임워크은 특히 배터리 생산 능력이 가장 높은 아시아태평양에서 대량 채용을 가속화합니다.

나노 재료의 높은 제조 비용

특수 CVD 반응기, 수율이 낮은 배치 공정, 엄격한 순도 요구 사항으로 인해 단가가 멈췄습니다. 자본 요건은 기술적 성능의 이점에도 불구하고 소비자용 가구 등 가격에 민감한 용도로의 채용을 지연시킵니다. 포지 나노가 4,000만 달러를 조달하는 등 벤처 캐피탈에 의한 자금 주입은 계속되고 있지만, 많은 스케일 업 프로그램은 파일럿 단계에 그치고 있어, 급격한 비용 저하보다는 서서히 비용이 저하해 나가는 것을 시사하고 있습니다. 생산자는 비용 절감을 위해 인라인 계측, 전구체 재활용, 하이브리드 습식 화학 단계를 추구하고 있지만, 손익 분기점의 경제성은 여전히 프리미엄 용도에 의존하고 있습니다.

부문 분석

나노 TiO2는 2024년 나노 페인트 및 코팅 시장에서 39.17%의 점유율을 유지했습니다. 안정적인 제조, 광촉매에 의한 셀프 클리닝 성능, 비용 효율이 외관, 자동차 트림, 실내 방담 패널에 채용을 뒷받침하고 있습니다. TiO2 나노입자를 사용한 초대형 투명 스크린을 OLED 유리의 10분의 1의 가격으로 제조하는 한국의 파일럿 라인이 이 소재의 확장성을 뒷받침하고 있습니다. 그래핀은 겸손한 베이스에 머물고 있지만, 배터리 히트 스프레더와 전자파 차폐 수요가 증가함에 따라 2030년까지 연평균 복합 성장률(CAGR)은 5.17%를 나타낼 전망입니다. 탄소나노튜브는 구조강성, 전도성, 경량화가 융합되는 항공우주나 하이엔드의 가전제품을 위한 틈새 옵션입니다. 나노SiO2는 인프라의 수명을 연장하는 시멘트 첨가제로 존재감을 늘리고, 나노ZnO는 의료기기나 스마트폰의 UV컷 코팅을 확보합니다. 향후 성장은 여러 나노입자를 조합하여 시너지 효과를 발휘하는 하이브리드 레시피에 기대됩니다.

산화티탄 수지 용도의 나노 페인트 및 코팅 시장 규모는 꾸준히 확대될 것으로 예상되는 반면, 그래핀의 점유율은 공급망의 해방과 반응로의 능력 증강에 의해 급속히 확대됩니다. 이 궤도를 보완하는 것으로, 이산화탄소 배출량을 삭감하기 위해 바이오 유래의 전구체나 무용매 분산액을 사용하는 그린 합성 루트가 병행하여 추진되고 있습니다.

지역 분석

아시아태평양은 2024년 세계 매출의 45.43%를 차지했으며 CAGR 4.91% 전망으로 리드를 유지합니다. 중국의 전자 공급 체인, 일본 재료 과학 클러스터, 한국 디스플레이 공장은 안정적인 기준선을 보장합니다. 중국의 메이드 인 차이나 2025 우선 순위와 일본의 문샷 R&D 목표 등의 정책 인센티브는 나노 생산 능력을 가속화하고 리드 타임을 단축합니다. 현지 CVD 반응기 공급업체는 선도적인 콩그로 매리트를 넘어 기술을 보급하여 중형 코팅 가게가 나노 제품을 인증할 수 있도록 합니다.

북미 수요의 중심은 항공우주, 방위, 의료기기입니다. 미국 공군의 유지 사령부와 우주 로켓의 프라임은 나노 코팅을 전략적 유지 보수 비용 절감으로 간주합니다. 멕시코에서는 EV 조립 에코시스템이 급성장하고 있으며 나노열 필름과 배터리 코팅 시스템을 수입하여 지역 공급과 원활하게 통합하고 있습니다. 유럽은 에코디자인과 근로자의 안전성을 중시하고 REACH나 그린빌딩 라벨을 충족하는 나노조합의 수성 코팅제의 채용을 추진하고 있습니다. 독일 자동차 Tier-1 공급업체와 프랑스 항공우주 OEM은 나노 코팅 전문가와 다년간의 프레임 워크 계약을 맺습니다.

남미에서는 브라질 운송 회랑과 아르헨티나 셰일 플레이 서비스에서 인프라 수리 노력이 기세를 늘리고 있습니다. 염수 분무, 고습도, 자외선 강도에 노출되기 때문에 고성능 코팅이 중시되어 현지의 페인트 제조업체는 일본이나 독일의 나노 재료 제조업체와 제휴해, 블렌드의 현지화를 진행시키고 있습니다. 중동의 에너지 부문은 산성 부식에 대항하기 위해 갱내 펌프와 수출 파이프라인에 나노 층을 시험적으로 사용합니다. 한편, 아프리카의 성장 스토리는 내부에 도포된 나노실런트가 고열 환경 하에서의 누출률을 줄이는 수도 네트워크에 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 항공우주 및 방위의 부식 - 경량화 추진

- EV용 내열·내화 코팅 수요 증가

- 고성능 코팅에 대한 요구 증가

- 인프라 분야에서의 수요 증가

- 일렉트로닉스와 소비재의 이용 증가

- 시장 성장 억제요인

- 나노 재료의 높은 제조 비용

- 나노독성규제의 불확실성

- 그래핀 CVD 반응기 공급의 병목

- 밸류체인 분석

- Porter's Five Forces

- 공급기업의 협상력

- 소비자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모·성장 예측

- 수지 유형별

- 그래핀

- 탄소나노튜브

- 나노 TiO2(이산화티타늄)

- 나노SiO2(이산화규소)

- 나노ZnO

- 나노 실버

- 방법별

- 전기분무 및 전기방사

- 화학 기상 증착(CVD)

- 물리적 기상 증착(PVD)

- 원자층 증착(ALD)

- 에어로졸 코팅

- 자가조립

- 졸-겔

- 최종 사용자 산업별

- 항공우주 및 방위

- 자동차

- 전자 및 광학

- 바이오메디컬

- 식품 및 포장

- 해양

- 석유 및 가스

- 기타 최종 사용자 산업(에너지 및 전력, 건설 및 인프라 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ASEAN 국가

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- Aculon

- Artekya Teknoloji

- BASF

- Europlasma NV

- Graphene NanoChem

- GVD Corporation

- Henkel AG and Co. KGaA

- I-CanNano

- Nanofilm

- Nanoshine Group Corp

- Pearl Global Ltd.

- Pellucere

- PPG Industries, Inc.

- SIA Naco Technologies

- Starshield Technologies Pvt Ltd

- Tesla NanoCoatings Inc.

제7장 시장 기회와 전망

KTH 25.11.05The Nano Paints & Coatings Market size is estimated at USD 12.87 billion in 2025, and is expected to reach USD 16.13 billion by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

Growing aerospace demand for corrosion-lightweight solutions, electric vehicle fire-safety requirements, and infrastructure durability needs keep the market on a steady upward course. A dominant 39.17% nano-TiO2 share combined with graphene's rapid 5.17% CAGR underlines the core role of advanced nanomaterials in sustaining competitive advantage. Regional momentum remains firmly with Asia-Pacific, which controls almost half of global revenues and commands the fastest regional growth. Supply advances in chemical vapor deposition (CVD) and a shift toward multifunctional formulations that merge corrosion protection, thermal management, and antimicrobial performance are shaping new business opportunities, while high production costs and evolving nano-toxicity rules restrain rapid scale-up.

Global Nano Paints And Coatings Market Trends and Insights

Aerospace and defense corrosion-light-weight push

Pentagon estimates that corrosion costs USD 23 billion each year across military equipment, intensifying the adoption of nano coatings that combine structural lightness with superior protection. Field data show nano-engineered layers lowering maintenance cycles on naval airframes, while icephobic properties enhance aircraft readiness in extreme climates. Programs under the U.S. Navy SBIR banner are moving from bench research to fleet trials, illustrating that rigorous certification barriers simultaneously limit new entrants and guarantee durable demand for validated suppliers. As defense procurement strategies favor platforms with reduced total ownership cost, single-application nano formulations that solve weight, durability, and environmental exposure challenges are increasingly specified.

Increase in demand for EV thermal-fire-safety coating

Rapid electrification pushes battery systems toward higher energy density and stricter safety standards. Specialized nano layers dissipate heat swiftly and form fire-retardant barriers, protecting cells and adjacent components. Resonac's thermal insulation product for EV packs highlights active commercial development. Carbon and graphene dispersions deliver thermal conductivity without sacrificing dielectric strength, matching OEM safety protocols. In parallel, passenger-comfort solutions such as Hyundai's nano cooling film that cuts cabin temperature by 10 °C demonstrate spill-over into ancillary applications. Regulatory frameworks that incorporate thermal runaway containment accelerate volume adoption, especially in Asia-Pacific, where battery production capacity is highest.

High production cost of nanomaterials

Specialized CVD reactors, low-yield batch processes, and stringent purity requirements keep unit costs elevated. Capital requirements delay adoption in price-sensitive uses such as consumer furniture, despite technical performance benefits. Venture capital continues to inject funds-Forge Nano's USD 40 million raise underscored private backing-but many scale-up programs remain in pilot phase, pointing to gradual cost attrition rather than abrupt drops. Producers pursue inline metrology, precursor recycling, and hybrid wet-chemistry steps to cut expenses, yet breakeven economics still hinge on premium applications.

Other drivers and restraints analyzed in the detailed report include:

- Growing requirement for high performance coatings

- Increasing demand from infrastructure sector

- Nano-toxicity regulatory uncertainty

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Nano-TiO2 kept its 39.17% hold on the nano paints & coatings market in 2024. Stable manufacturing, photocatalytic self-cleaning performance, and cost efficiency drive its acceptance on facades, automotive trims, and indoor anti-smog panels. Korean pilot lines producing ultra-large transparent screens using TiO2 nanoparticles at one-tenth the price of OLED glass underscore this material's scalability. Graphene, although capped at a modest base, posts a 5.17% CAGR through 2030 as demand from battery heat spreaders and electromagnetic shielding intensifies. Carbon nanotubes remain a niche choice for aerospace and high-end consumer electronics where structural stiffness, conductivity, and weight savings converge. Nano-SiO2 extends its presence in cement additions that lengthen infrastructure life, and nano-ZnO secures UV-blocking coatings for medical devices and smartphones. Future growth leans on hybrid recipes pairing multiple nanoparticles to secure synergistic properties.

The nano paints & coatings market size for titanium dioxide resin applications is projected to widen steadily, while graphene's share expands faster under supply chain releases and reactor capacity additions. Complementing that trajectory is a parallel push for green synthesis routes that use bio-derived precursors or solvent-free dispersion to cut carbon footprint.

The Nano Paints & Coatings Market Report is Segmented by Resin Type (Graphene, Carbon Nanotubes, Nano-TiO2, and More), Method (Electrospray and Electrospinning, Chemical Vapor Deposition, and More), End-User Industry (Aerospace and Defense, Automotive, Biomedical, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific anchored 45.43% of global revenue in 2024, keeping the lead with a 4.91% CAGR outlook. China's electronics supply chains, Japan's materials science clusters, and South Korea's display fabs guarantee a stable baseline. Policy incentives, such as China's Made-in-China 2025 priorities and Japan's Moonshot R&D goals, accelerate nano production capability, shortening lead times. Local CVD reactor suppliers help diffuse technology beyond top-tier conglomerates, enabling mid-size coating shops to certify nano offerings.

North America's demand profile centers on aerospace, defense, and medical devices. U.S. Air Force sustainment commands and space launch primes view nano-layering as strategic maintenance cost reducers. Mexico's ascending EV assembly ecosystem imports nano thermal films and battery coating systems, integrating seamlessly with regional supply. Europe champions eco-design and worker safety, thus driving the adoption of nano-formulated water-borne coatings that satisfy REACH and green building labels. Germany's automotive Tier-1 suppliers and France's aerospace OEMs lock up multi-year framework agreements with nano-coating specialists.

South America injects momentum from infrastructure rehabilitation commitments in Brazil's transport corridors and Argentina's shale play servicing. Exposure to salt spray, high humidity, and UV intensity places a premium on high-performance coatings, and local paint majors partner with Japanese and German nanomaterial producers to localize blends. The Middle East's energy sector trials nano layers on downhole pumps and export pipelines to combat sour corrosion, while Africa's growth story lies in water networks, where internally applied nano sealants cut leak rates under high ambient heat.

- Aculon

- Artekya Teknoloji

- BASF

- Europlasma NV

- Graphene NanoChem

- GVD Corporation

- Henkel AG and Co. KGaA

- I-CanNano

- Nanofilm

- Nanoshine Group Corp

- Pearl Global Ltd.

- Pellucere

- PPG Industries, Inc.

- SIA Naco Technologies

- Starshield Technologies Pvt Ltd

- Tesla NanoCoatings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aerospace and defense corrosion-light-weight push

- 4.2.2 Increase in demand for EV thermal-fire-safety coating

- 4.2.3 Growing requirement for high performance coatings

- 4.2.4 Inceasing demand from infrastructure sector

- 4.2.5 Rise in utilization from electronics and consumer goods

- 4.3 Market Restraints

- 4.3.1 High production cost of nanomaterials

- 4.3.2 Nano-toxicity regulatory uncertainty

- 4.3.3 Graphene CVD reactor supply bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitute Products and Services

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Graphene

- 5.1.2 Carbon Nanotubes

- 5.1.3 Nano-TiO2 (Titanium Dioxide)

- 5.1.4 Nano-SiO2 (Silicon Dioxide)

- 5.1.5 Nano-ZnO

- 5.1.6 Nano Silver

- 5.2 By Method

- 5.2.1 Electrospray and Electrospinning

- 5.2.2 Chemical Vapor Deposition (CVD)

- 5.2.3 Physical Vapor Deposition (PVD)

- 5.2.4 Atomic Layer Deposition (ALD)

- 5.2.5 Aerosol Coating

- 5.2.6 Self-Assembly

- 5.2.7 Sol-Gel

- 5.3 By End-User Industry

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Electronics and Optics

- 5.3.4 Biomedical

- 5.3.5 Food and Packaging

- 5.3.6 Marine

- 5.3.7 Oil and Gas

- 5.3.8 Other End-user Industries (Energy and Power, Construction and Infrastructure, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Aculon

- 6.4.2 Artekya Teknoloji

- 6.4.3 BASF

- 6.4.4 Europlasma NV

- 6.4.5 Graphene NanoChem

- 6.4.6 GVD Corporation

- 6.4.7 Henkel AG and Co. KGaA

- 6.4.8 I-CanNano

- 6.4.9 Nanofilm

- 6.4.10 Nanoshine Group Corp

- 6.4.11 Pearl Global Ltd.

- 6.4.12 Pellucere

- 6.4.13 PPG Industries, Inc.

- 6.4.14 SIA Naco Technologies

- 6.4.15 Starshield Technologies Pvt Ltd

- 6.4.16 Tesla NanoCoatings Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment