|

시장보고서

상품코드

1844641

내열 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Heat-Resistant Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

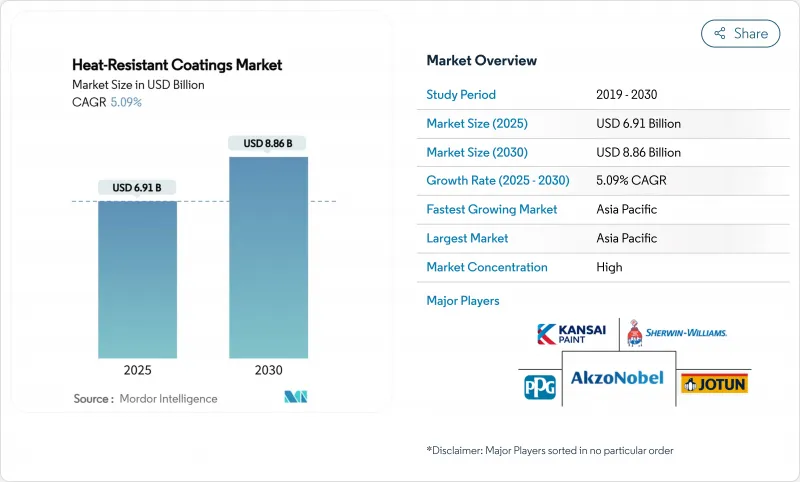

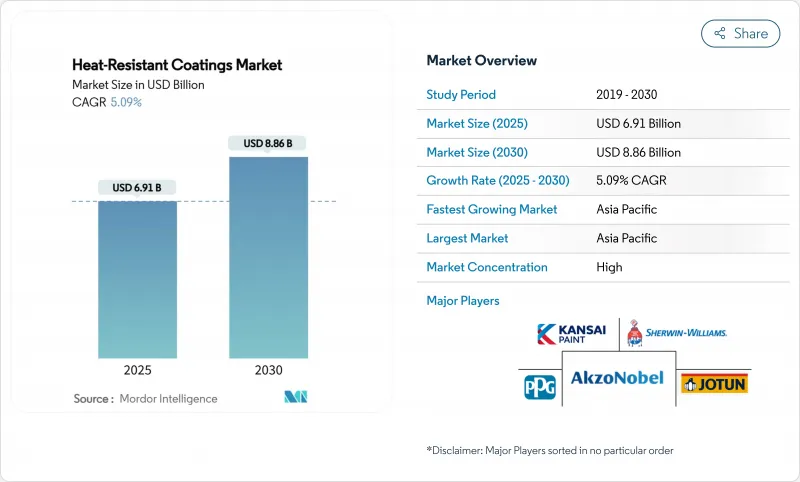

내열 코팅 시장 규모는 2025년에 69억 1,000만 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 5.09%를 나타낼 것으로 예측되며, 2030년에는 88억 6,000만 달러에 달할 전망입니다.

세계의 인프라 투자 증가, 강화된 화재 안전 규정, 항공우주 분야의 재사용 우주선 추진 등이 수요 확대를 지속하고 있습니다. 아시아태평양 지역은 정부 주도 건설 프로그램과 제조업 확장을 통해 규모 우위를 유지하는 반면, 북미와 유럽은 더 엄격한 환경 규정을 충족하는 고성능 솔루션을 중시합니다. 기술 채택은 두 가지 뚜렷한 경로를 보인다: 수성 시스템은 낮은 VOC 배출량으로 양적 우위를 점하고 있으며, UV/EB 경화형 화학물질은 빠른 경화 속도와 최소한의 환경 영향을 결합해 가장 빠른 성장을 기록 중입니다. 실리콘 기반 수지는 600°C 이상의 탁월한 안정성으로 규모와 성장 모두에서 우위를 점하고 있으며, 신흥 발전 프로젝트는 열 관리가 중요한 에너지 인프라로 수요를 전환시키고 있습니다. 원자재 가격 변동과 인증된 도포업체 부족은 여전히 걸림돌이지만, 지속 가능한 제형과 자동화 스프레이 시스템에 대한 지속적인 혁신으로 장기 전망은 긍정적입니다.

세계의 내열 코팅 시장 동향 및 인사이트

세계의 인프라 지출 급증

정부들은 기후 회복력과 도시 성장을 목표로 사상 최대 규모의 인프라 투자를 진행 중입니다. 미국의 인프라 투자 및 일자리 법안은 코팅 사양에 영향을 미치는 에너지 규격 업데이트를 위해 2억 2,500만 달러를 배정했습니다. 신흥 아시아태평양 경제권도 동력을 더하고 있습니다. 인도네시아, 인도, 중국이 고온 차단 필름을 요구하는 공항, 교량, 스마트 시티 프로젝트를 가속화하고 있기 때문입니다. 교통 터널 및 지역 난방 라인에 대한 공공-민간 파트너십은 장주기 내열 코팅 수요를 더욱 확대합니다.

세계의 화재안전규제 강화

화재 규정 개정으로 점화 저항성, 연기 독성, 최종 사용 표면 온도에 대한 최소 성능 기준이 상향 조정되었습니다. 2024년 국제 화재 규정(IFC)은 코팅 제형에 즉각적인 영향을 미치는 업데이트된 화염 확산 기준을 도입했습니다. 캘리포니아 화재 규정 제24장은 내열성 제품을 취급하는 코팅 부스에 자동 소화 시스템과 특수 환기 장치를 의무화합니다. EU 지침은 허용 용매 함량을 지속적으로 축소하여 건설사들이 저휘발성 유기화합물(VOC) 실리콘-아크릴 하이브리드 제품으로 전환하도록 유도하고 있습니다. 고층 건물 외벽 및 교통 허브의 개조 수요가 급증하며 소유주들이 자산을 규정 준수 상태로 전환하고 있습니다. 신규 기준을 상회하는 제품 인증을 획득한 제조사는 우선적인 사양 선정 기회를 얻고 비용이 많이 드는 재작업 필요성을 줄일 수 있습니다.

불안정한 실리콘과 에폭시 가격

미국 국제무역위원회(ITC) 판결에 따라 특정 에폭시 수입품이 공정 가치 이하로 판매된 것으로 확인되어 국내 공급이 위축되고 비용이 상승했습니다. 주요 아시아 실리콘 공장의 동시 가동 중단은 가격 변동성을 더욱 가중시켰습니다. 장기 계약이 없는 중소 규모 제형업체들은 두 자릿수 비용 급등으로 마진이 훼손되고 제품 재가격이 촉발되었습니다. 생산자들은 전구체 이중 조달과 내부 단량체 생산 능력 확대로 헤지하지만, 자본 지출로 인해 즉각적인 완화는 지연됩니다. 원자재 변동은 주기적이지만, 단기적으로 현금 흐름을 압박하고 연구 개발 지출을 저해합니다.

부문 분석

실리콘 수지는 2024년 내열 코팅 시장 점유율의 38.16%를 차지했으며, 이는 600°C 이상의 온도에서도 접착력을 유지하는 화학적 특성을 반영합니다. 이러한 선도적 지위는 2030년까지 8.90%라는 가장 빠른 세그먼트 연평균 복합 성장률(CAGR)과 맞물려 실리콘을 내열 코팅 시장의 핵심 성장 동력으로 자리매김하게 합니다. 수요는 고장이 용납될 수 없는 배기 스택, 플레어 스택, 베이킹 오븐 및 항공우주 부품에 걸쳐 있습니다. 에폭시는 중간 온도 영역에서 여전히 관련성을 유지하지만, 비스페놀-A 유도체에 대한 비용 부담과 규제 심사를 직면하고 있습니다. 아크릴 수지는 표면 온도 피크가 낮은 소비재의 가격 민감형 응용 분야를 채운다.

본 내열 코팅 보고서는 수지(실리콘, 에폭시, 아크릴, 기타 수지), 기술(용매형, 수성형, 분체형, UV/EB 경화형), 최종 사용자 산업(건축 및 건설, 석유 및 가스, 전력 부문, 운송, 목공 및 가구, 소비재, 기타 최종 사용자 산업), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류됩니다.

지역별 분석

아시아태평양 지역은 2024년 매출의 47.81%를 차지하며 선두를 달리고 있으며, 교통, 주택 및 에너지 분야의 메가 프로젝트에 힘입어 연평균 7.50%의 성장률을 보이고 있습니다. 중국의 일대일로(Belt and Road) 회랑은 산불 및 화학물질 유출 위험에 노출된 교량과 터널에 내열성 프라이머를 필요로 합니다. 인도는 ‘메이크 인 인디아’ 비전 하에 열안정성 필름이 필수인 조리기구, 보일러, 산업용 오븐의 국내 생산을 확대하고 있습니다.

북미는 여전히 혁신의 중심지입니다. 미국과 캐나다의 항공우주 주요 업체들은 MIL 표준을 충족하는 금속 및 세라믹 차단 코팅을 요구합니다. 노후 교량 교체 및 전력망 개선을 위한 연방 인프라 지출은 각 프로젝트마다 저휘발성 유기화합물(VOC) 고온 마감재를 의무화합니다.

유럽은 지속가능성을 강조합니다. EU의 VOC 상한선은 매년 강화되어 건설사들이 수성 실리콘 및 분체 도료 옵션으로 전환하도록 유도합니다. 독일, 프랑스, 이탈리아의 자동차 플랫폼은 열 조절을 위해 나노 구조 세라믹 필름으로 코팅된 경량 금속 부품을 통합합니다. 남미, 중동 및 아프리카 시장은 기반이 작지만 기술 이전과 국제 안전 규격 채택으로 혜택을 보며, 전체 내열성 코팅 시장 규모를 확대하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 인프라 지출의 급증

- 세계의 화재 안전 규제 강화

- 항공우주산업에서의 수요 증가

- 화재 방지 장비에 대한 인식 제고

- 재사용 가능 우주선 및 우주 관광선

- 시장 성장 억제요인

- 실리콘 및 에폭시 가격 변동성

- 용매 기반 시스템의 VOC 제한

- 다층 시스템 적용 기술 인력 부족

- 밸류체인 분석

- Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁도

제5장 시장 규모 및 성장 예측

- 수지별

- 실리콘

- 에폭시

- 아크릴

- 기타 수지(폴리우레탄, 알키드 등)

- 기술별

- 용매계

- 수성

- 분말

- UV/EB 경화형

- 최종 사용자 산업별

- 건축 및 건설

- 석유 및 가스

- 전력 섹터

- 운송

- 목공 및 가구

- 소비재

- 기타 최종 사용자 산업(산업 가공 기기 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- 3M

- Advanced Industrial Coatings

- AkzoNobel NV

- Aremco

- Arkema

- Axalta Coating Systems LLC

- BASF

- Belzona International Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- KCC Corporation

- Momentive

- PPG Industries Inc.

- Teknos Group

- The Sherwin-Williams Company

- Wacker Chemie AG

제7장 시장 기회와 전망

HBR 25.11.07The Heat-Resistant Coatings Market size is estimated at USD 6.91 billion in 2025, and is expected to reach USD 8.86 billion by 2030, at a CAGR of 5.09% during the forecast period (2025-2030).

Rising global infrastructure investments, tighter fire-safety rules and the aerospace sector's push for reusable spacecraft continue to widen demand. Asia-Pacific retains scale advantages through government-led building programs and manufacturing expansion, while North America and Europe emphasize high-performance solutions that meet stricter environmental rules. Technology adoption shows two clear tracks: water-borne systems hold volume leadership owing to lower VOC emissions, and UV/EB-curable chemistries post the fastest gains by combining rapid cure with minimal environmental impact. Silicone-based resins dominate both scale and growth because of unmatched stability above 600 °C, and emerging power-generation projects are shifting volume toward energy infrastructure where thermal management is critical. Raw-material price swings and a shortage of certified applicators remain counterweights, yet sustained innovation in sustainable formulations and automated spray systems keeps the long-term outlook positive.

Global Heat-Resistant Coatings Market Trends and Insights

Surge in Global Infrastructure Spending

Governments are funding record levels of infrastructure aimed at climate resilience and urban growth. The United States Infrastructure Investment and Jobs Act earmarked USD 225 million for updated energy codes that influence coating specifications. Emerging Asia-Pacific economies add momentum as Indonesia, India, and China accelerate airport, bridge, and smart-city projects that specify high-temperature barrier films. Public-private partnerships in transport tunnels and district-heating lines further widen demand for long-cycle thermal coatings.

Stricter Global Fire-Safety Regulations

Fire-code revisions raise minimum performance thresholds for ignition resistance, smoke toxicity, and end-use surface temperature. The International Fire Code 2024 introduces updated flame-spread benchmarks that immediately affect coating formulations. California's Fire Code Chapter 24 mandates automatic extinguishing systems and specialized ventilation for coating booths handling heat-resistant products. EU directives continue to shrink allowed solvent content, pushing builders toward low-VOC silicone-acrylic hybrids. Retrofits of high-rise facades and transportation hubs create demand spikes as owners bring assets into compliance. Manufacturers that certify products above the new baseline win specification priority and reduce the need for costly rework.

Volatile Silicone and Epoxy Prices

A United States International Trade Commission ruling found certain epoxy imports were sold below fair value, tightening domestic supply and raising costs. Simultaneous outages in key Asian silicone plants amplified volatility. Smaller formulators lacking long-term contracts faced double-digit cost spikes that eroded margins and triggered product repricing. Producers hedge by dual-sourcing precursors and expanding in-house monomer capacity, but capital outlays delay immediate relief. Although raw-material swings are cyclical, they compress cash flow and hinder research and development spending in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Growing Demand from the Aerospace Industry

- Rising Awareness Toward Fire Protection Equipment

- VOC Limits on Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone resins accounted for 38.16% of the 2024 heat-resistant coatings market share, reflecting the chemistry's ability to tolerate temperatures above 600 °C without losing adhesion. That leadership is matched by the fastest segment CAGR of 8.90% through 2030, making silicone the pivotal growth engine of the heat-resistant coatings market. Demand spans exhaust stacks, flare stacks, bake ovens, and aerospace parts where failure is unacceptable. Epoxies retain relevance in mid-temperature zones but face cost headwinds and regulatory scrutiny on bisphenol-A derivatives. Acrylics fill price-sensitive applications in consumer goods where surface temperature peaks are lower.

The Heat-Resistant Coatings Report is Segmented by Resin (Silicone, Epoxy, Acrylic, Other Resins), Technology (Solvent-Borne, Water-Borne, Powder, UV/EB-curable), End-User Industry (Building and Construction, Oil and Gas, Power Sector, Transportation, Woodworking and Furniture, Consumer Goods, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific led with 47.81% of 2024 revenue and advances at 7.50% CAGR, powered by megaprojects in transport, housing, and energy. China's Belt and Road corridors require heat-resistant primers for bridges and tunnels exposed to wildfire and chemical spill risks. India, under its Make in India vision, expands domestic manufacturing of cookstoves, boilers, and industrial ovens that all specify heat-stable films.

North America remains an innovation center. Aerospace primes in the United States and Canada specify metallic and ceramic barrier coats qualified to MIL standards. Federal infrastructure outlays replace aging bridges and improve energy grids, each project mandating low-VOC, high-temperature finishes.

Europe emphasizes sustainability. EU VOC ceilings tighten yearly, pushing builders to waterborne silicones and powder options. Automotive platforms in Germany, France, and Italy integrate lightweight metal components coated with nano-structured ceramic films for thermal regulation. Markets in South America, the Middle East and Africa grow from a smaller base yet benefit from technology transfer and the adoption of international safety codes, widening the total addressable heat-resistant coatings market.

- 3M

- Advanced Industrial Coatings

- AkzoNobel N.V.

- Aremco

- Arkema

- Axalta Coating Systems LLC

- BASF

- Belzona International Ltd.

- Hempel A/S

- Jotun

- Kansai Paint Co. Ltd.

- KCC Corporation

- Momentive

- PPG Industries Inc.

- Teknos Group

- The Sherwin-Williams Company

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in Global Infrastructure Spending

- 4.2.2 Stricter Global Fire-safety Regulations

- 4.2.3 Growing Demand from the Aerospace Industry

- 4.2.4 Rising Awareness Toward Fire Protection Equipment

- 4.2.5 Re-usable Spacecraft and Space-tourism Vehicles

- 4.3 Market Restraints

- 4.3.1 Volatile Silicone and Epoxy Prices

- 4.3.2 VOC Limits on Solvent-borne Systems

- 4.3.3 Applicator Skill Shortage for Multi-layer Systems

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Silicone

- 5.1.2 Epoxy

- 5.1.3 Acrylic

- 5.1.4 Other Resins (Polyurethane, Alkyd, etc.)

- 5.2 By Technology

- 5.2.1 Solvent-borne

- 5.2.2 Water-borne

- 5.2.3 Powder

- 5.2.4 UV/EB-curable

- 5.3 By End-user Industry

- 5.3.1 Building and Construction

- 5.3.2 Oil and Gas

- 5.3.3 Power Sector

- 5.3.4 Transportation

- 5.3.5 Woodworking and Furniture

- 5.3.6 Consumer Goods

- 5.3.7 Other End-user Industries (Industrial Processing Equipment, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Advanced Industrial Coatings

- 6.4.3 AkzoNobel N.V.

- 6.4.4 Aremco

- 6.4.5 Arkema

- 6.4.6 Axalta Coating Systems LLC

- 6.4.7 BASF

- 6.4.8 Belzona International Ltd.

- 6.4.9 Hempel A/S

- 6.4.10 Jotun

- 6.4.11 Kansai Paint Co. Ltd.

- 6.4.12 KCC Corporation

- 6.4.13 Momentive

- 6.4.14 PPG Industries Inc.

- 6.4.15 Teknos Group

- 6.4.16 The Sherwin-Williams Company

- 6.4.17 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment