|

시장보고서

상품코드

1844649

유럽의 치과용 장비 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Europe Dental Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

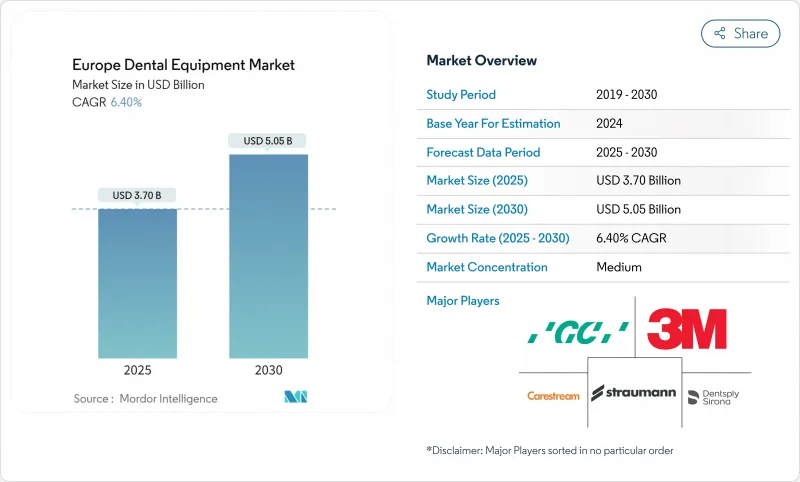

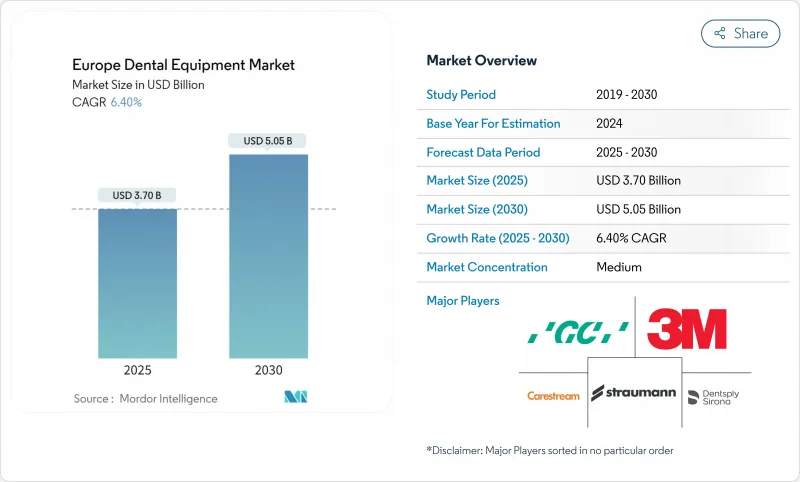

유럽의 치과용 장비 시장 규모는 2025년에 37억 달러로 평가되었고, 예측 기간(2025-2030년)의 CAGR은 6.4%를 나타낼 것으로 예측되며, 2030년에는 50억 5,000만 달러에 달할 전망입니다.

체어사이드 디지털 워크플로우와 인공지능 기반 진단의 융합이 치료 주기를 단축하고 임상 정확도를 향상시키며 수요를 견인하고 있습니다. 맞춤형 보철물을 위한 3D 프린팅의 활발한 도입과 생체모방 및 지르코니아 소재에 대한 선호도 증가는 수복 시술 방식을 재편하고 있습니다. 국가별 동향도 중요합니다. 독일의 공학 기반은 장비 제조를 주도하는 반면, 영국의 개인 진료소 붐은 프리미엄 장비 투자를 가속화하고 있습니다. 한편, 새로운 의료장비 규정(MDR)은 품질 기준을 강화하고 승인 기간을 연장하여, 신뢰할 수 있는 다국적 공급업체와 잘 문서화된 장비로 의료기관을 유도하고 있습니다.

유럽의 치과용 장비 시장 동향 및 인사이트

치과 질환 발생률 증가

유럽의 치과용 장비 시장은 현재 지역 성인의 절반 이상에게 영향을 미치는 증가하는 질병 부담의 영향을 크게 받고 있습니다. 충치만으로도 주민의 33.6%가 고통받고 있으며, 25.2%는 상당한 치아 상실을 경험하여 보철 장치 및 영상 시스템에 대한 꾸준한 수요를 창출하고 있습니다. 심각한 치주염 사례는 2050년까지 증가할 것으로 예상되어, 진료소들이 첨단 치주 프로브와 휴대용 진단 장비를 도입하도록 촉진하고 있습니다. 난민 집단은 충족되지 않은 수요를 증폭시킵니다. 이탈리아에서 검사받은 우크라이나 어린이의 84%가 우식을 보였으며, 이는 이동식 X선 및 예방 기술의 필요성을 강조합니다. 종합적으로, 이러한 역학적 압박은 소모품, 스케일러, CAD/CAM 기반 보철물 전반에 걸쳐 단위 출하량을 증가시킬 것으로 예상됩니다.

치과 제품 혁신

생체모방 유리 이오머 시멘트와 나노 충전 복합 레진은 수복물의 내구성을 향상시키고 재치료율을 낮추며 진료 시간을 단축시키고 있습니다(materials-journal.com). 키토산과 콜라겐 같은 천연 폴리머는 현재 유도 조직 재생 막의 기반이 되어 호환 가능한 전달 장비의 임상적 채택을 촉진하고 있습니다(materials-journal.com). 장비 공급업체들은 이러한 새로운 화학 물질에 최적화된 전용 디스펜서와 경화등을 통합하고 있습니다. 이산화 지르코늄 임플란트는 광역학 생물막 불활성화가 가능한 광도파관 역할을 하여 세균 수를 최대 85%까지 감소시키고 레이저 적용 임플란트 핸드피스 개발 기회를 열어줍니다(microorganisms-journal.com). 연구개발 파이프라인이 확대됨에 따라 소모품과 적용 장치를 묶어 제공하는 공급업체들은 유럽 치과용 장비 시장에서 반복적 수익 흐름을 확보할 수 있을 전망입니다.

치과 치료에 대한 적절한 보험 적용 부족

국가별 보험 적용 모델의 분절화는 기술의 균일한 보급을 방해합니다. 프랑스는 기본 진료비의 60%만 보험 적용하여 소규모 진료소의 고급 영상 장비 업그레이드 의욕을 저해합니다. 덴마크는 성인에게 진료비의 60%를 부담하도록 요구하는 반면, 스웨덴의 단계별 보조금 제도는 공동부담금 불확실성을 초래하여 고비용 레이저의 조기 도입을 저해하고 있습니다(nhwstat.org). 영국 클리닉들은 제한된 NHS 예산으로 인해 자본 준비금이 감소하는 상황에 직면해 있으며, 셰필드 지역 진료소들이 최근 확장 대출 상환에 어려움을 겪는 사례가 이를 입증합니다. 그 결과, 유럽의 치과용 장비 시장에서 리스 및 사용량 기반 요금제 모델이 점차 확산되고 있습니다.

부문 분석

유럽의 치과용 장비 시장 규모 데이터에 따르면, 반복 구매 주기와 시술 필수성 덕분에 2024년 치과 소모품이 매출 점유율 58.50%를 차지했습니다. 알지네이트, 셀룰로오스, 하이드록시아파타이트와 같은 천연 생체재료는 생체적합성으로 인해 임상의들의 선호를 얻고 있으며, 이는 공급업체들이 진료실 내 재료 취급을 간소화하는 사전 용량 조절 카트리지 도입을 촉진하고 있습니다. 동시에 유럽의 치과용 장비 산업에서는 사용량을 추적하고 재주문을 자동화하여 재고 부족을 줄이는 스마트 디스펜서의 급속한 확산을 목격하고 있습니다.

일반 및 진단 장비는 매출 규모는 작지만, AI 지원 구강 스캐너와 CBCT 장비가 치료 계획 수립에 일상적으로 활용되면서 2030년까지 8.07%의 가장 빠른 연평균 성장률(CAGR)을 기록할 전망입니다. 레이저 분야는 가장 역동적인 하위 카테고리로, Er:YAG 시스템이 절개 없는 발치술을 가능하게 하고, 다이오드 레이저 치주 보조 장비가 측정 가능한 탐침 깊이 감소를 제공하기 때문입니다. 이미징 센서와 함께 포장된 감염 관리 키트와 같이 소모품을 진단 장비와 번들로 제공하는 공급업체들은 유의럽 치과용 장비 시장에서 지갑 점유율을 확대할 수 있을 것으로 보인다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 치과 질환 증가

- 치과 제품의 혁신

- 미용 치과 수요 증가

- 치과 솔루션 기술 발전

- 북유럽 지역 정부 지원 구강 건강 검진 프로그램 확대 및 영상 장비 증설

- 스페인 및 헝가리로의 교정 관광 유입 증가로 인한 디지털 구강 내 스캐너 수요 증대

- 시장 성장 억제요인

- 치과 치료에 대한 적절한 보험 적용 부족

- 수술비용 상승

- 중부 및 동유럽(CEE) 지역의 숙련된 CAD/CAM 기술자 부족으로 인한 실험실 자동화 도입 지연

- 아시아 OEM 업체 유입으로 인한 보급형 핸드피스 가격 압박

- 공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 구매자의 협상력

- 공급기업의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 일반 및 진단장비

- 치과용 레이저

- 연조직 레이저

- 경조직 레이저

- 방사선 장비

- 구강외 방사선 장비

- 구강내 방사선 장비

- 치과용 체어 및 장비

- 기타 일반 및 진단 장비

- 치과용 소모품

- 치과 생체 재료

- 치과 임플란트

- 크라운 브릿지

- 기타 치과용 소모품

- 기타 치과용 장비

- 일반 및 진단장비

- 치료별

- 치열 교정

- 치내 요법

- 치주 치료

- 보철

- 최종 사용자별

- 치과 병원

- 치과 진료소

- 학술연구기관

- 국가별

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Dentsply Sirona

- Envista Holdings(KaVo Kerr)

- Planmeca Oy

- Straumann Group

- Align Technology, Inc.

- 3M Oral Care

- Ivoclar Vivadent

- GC Corporation

- Vatech Co., Ltd.

- Acteon Group

- Carestream Dental LLC

- A-dec Inc.

- Midmark Corporation

- Coltene Holding AG

- Ultradent Products Inc.

- DentalEZ Group

- Nobel Biocare Services AG

- Anthogyr SAS

- VOCO GmbH

- Osstem Implant Co.

- Eurodent Srl

제7장 시장 기회와 전망

HBR 25.11.07The Europe Dental Equipment Market size is estimated at USD 3.70 billion in 2025, and is expected to reach USD 5.05 billion by 2030, at a CAGR of 6.4% during the forecast period (2025-2030).

Demand is propelled by the convergence of chairside digital workflows with AI-powered diagnostics, which shortens treatment cycles and improves clinical accuracy. Strong uptake of3D printing for customized prosthetics, coupled with growing preference for biomimetic and zirconia materials, is reshaping restorative procedures. Country-level dynamics also matter: Germany's engineering base anchors equipment manufacturing, while the UnitedKingdom's private-practice boom is accelerating premium device investment. Meanwhile, the new Medical Devices Regulation (MDR) is tightening quality standards and lengthening approval timelines, nudging clinics toward trusted multinational suppliers and well-documented devices health.

Europe Dental Equipment Market Trends and Insights

Increasing Incidence of Dental Diseases

The Europe dental equipment market is heavily influenced by a rising disease burden that now affects more than half of the region's adults who.int. Dental caries alone afflict 33.6% of residents, while 25.2% experience significant tooth loss, generating steady demand for restorative devices and imaging systems. Severe periodontitis cases are projected to escalate through 2050, prompting practices to adopt advanced periodontal probes and portable diagnostic units. Refugee cohorts amplify unmet need: 84% of Ukrainian children examined in Italy showed caries, underscoring the requirement for mobile X-ray and preventive technologies . Collectively, these epidemiological pressures are set to lift unit shipments across consumables, scalers, and CAD/CAM-enabled prosthetics.

Innovation in Dental Products

Biomimetic glass ionomer cements and nanofilled composite resins are improving longevity of restorations, lowering retreatment rates, and reducing chair time materials-journal.com. Natural polymers such as chitosan and collagen now underpin guided tissue regeneration membranes, boosting clinical adoption of compatible delivery equipment materials-journal.com. Equipment vendors are integrating dedicated dispensers and curing lights optimized for these new chemistries. Zirconium dioxide implants act as optical waveguides that allow photodynamic biofilm inactivation, cutting bacterial counts by as much as 85% and opening opportunities for laser-ready implant handpieces microorganisms-journal.com. As R&D pipelines widen, suppliers that bundle consumables with application devices stand to capture recurring revenue streams across the Europe dental equipment market.

Lack of Proper Reimbursement of Dental Care

Fragmented national coverage models hinder uniform technology rollouts. France reimburses only 60% of basic consultations, dampening appetite for premium imaging upgrades among smaller practices. Denmark requires adults to pay 60% of fees, while Sweden's tiered subsidy introduces copay uncertainty, blunting early adoption of high-cost lasers nhwstat.org. UK clinics, grappling with constrained NHS budgets, face reduced capital reserves, as evidenced by practices in Sheffield struggling to service recent expansion loans. As a result, leasing and pay-per-use models are gaining ground within the Europe dental equipment market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Demand for Cosmetic Dentistry

- Technological Advancements in Dental Solutions

- High Cost of Surgeries

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Europe dental equipment market size data show dental consumables captured 58.50% revenue share in 2024 on the back of recurring purchase cycles and procedural indispensability. Natural biomaterials such as alginate, cellulose, and hydroxyapatite are winning clinician favor for their biocompatibility, pushing suppliers to introduce pre-dosed cartridges that simplify chairside handling materials. The Europe dental equipment industry is simultaneously witnessing a leap in smart dispensers that track usage and automate reordering, reducing stockouts.

General and diagnostics equipment, although smaller by revenue, is posting the fastest 8.07% CAGR through 2030 as AI-ready intraoral scanners and CBCT units become routine for treatment planning. Lasers represent the most dynamic subcategory because Er:YAG systems now enable flapless extractions, while diode-laser periodontal adjuncts deliver measurable reductions in probing depth. Suppliers focused on bundling consumables with diagnostics-such as infection-control kits packaged with imaging sensors-stand to deepen wallet share in the Europe dental equipment market.

The Europe Dental Equipment Market Report Segments the Industry Into by Product (General and Diagnostics Equipment, Dental Consumables and More), by Treatment (Orthodontic, Endodontic, Peridontic, Prosthodontic), by End User (Dental Hospitals, Dental Clinics, and More), and Geography (Germany, United Kingdom, France, Italy, Spain, Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Dentsply Sirona

- Envista Holdings (KaVo Kerr)

- Planmeca

- Straumann Group

- Align Technology

- 3M Oral Care

- Ivoclar Vivadent

- GC Corporation

- Vatech Co., Ltd.

- Acteon Group

- Carestream Dental

- A-dec

- Midmark

- Coltene Holding

- Ultradent Products

- DentalEZ Group

- Nobel Biocare Services

- Anthogyr

- VOCO

- Osstem Implant Co.

- Eurodent Srl

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Incidence of Dental Diseases

- 4.2.2 Innovation in Dental Products

- 4.2.3 Increasing Demand for Cosmetic Dentistry

- 4.2.4 Technological Advancements in Dental Solutions

- 4.2.5 Government-sponsored oral-health screening programs expanding imaging fleet in Nordics

- 4.2.6 Orthodontic tourism inflow to Spain & Hungary boosting demand for digital intra-oral scanners

- 4.3 Market Restraints

- 4.3.1 Lack of Proper Reimbursement of Dental Care

- 4.3.2 High Cost of Surgeries

- 4.3.3 Shortage of trained CAD/CAM technicians in CEE slows lab automation uptake

- 4.3.4 Price compression in entry-level handpieces due to Asian OEM influx

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 General and Diagnostics Equipment

- 5.1.1.1 Dental Laser

- 5.1.1.1.1 Soft Tissue Lasers

- 5.1.1.1.2 Hard Tissue Lasers

- 5.1.1.2 Radiology Equipment

- 5.1.1.2.1 Extra Oral Radiology Equipment

- 5.1.1.2.2 Intra-oral Radiology Equipment

- 5.1.1.3 Dental Chair and Equipment

- 5.1.1.4 Other General and Diagnostic equipment

- 5.1.2 Dental Consumables

- 5.1.2.1 Dental Biomaterial

- 5.1.2.2 Dental Implants

- 5.1.2.3 Crowns and Bridges

- 5.1.2.4 Other Dental Consumables

- 5.1.3 Other Dental Devices

- 5.1.1 General and Diagnostics Equipment

- 5.2 By Treatment

- 5.2.1 Orthodontic

- 5.2.2 Endodontic

- 5.2.3 Peridontic

- 5.2.4 Prosthodontic

- 5.3 By End User

- 5.3.1 Dental Hospitals

- 5.3.2 Dental Clinics

- 5.3.3 Academic & Research Institutes

- 5.4 By Country

- 5.4.1 Germany

- 5.4.2 United Kingdom

- 5.4.3 France

- 5.4.4 Italy

- 5.4.5 Spain

- 5.4.6 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Dentsply Sirona

- 6.3.2 Envista Holdings (KaVo Kerr)

- 6.3.3 Planmeca Oy

- 6.3.4 Straumann Group

- 6.3.5 Align Technology, Inc.

- 6.3.6 3M Oral Care

- 6.3.7 Ivoclar Vivadent

- 6.3.8 GC Corporation

- 6.3.9 Vatech Co., Ltd.

- 6.3.10 Acteon Group

- 6.3.11 Carestream Dental LLC

- 6.3.12 A-dec Inc.

- 6.3.13 Midmark Corporation

- 6.3.14 Coltene Holding AG

- 6.3.15 Ultradent Products Inc.

- 6.3.16 DentalEZ Group

- 6.3.17 Nobel Biocare Services AG

- 6.3.18 Anthogyr SAS

- 6.3.19 VOCO GmbH

- 6.3.20 Osstem Implant Co.

- 6.3.21 Eurodent Srl

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment