|

시장보고서

상품코드

1844675

영국의 심혈관 의료기기 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)United Kingdom Cardiovascular Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

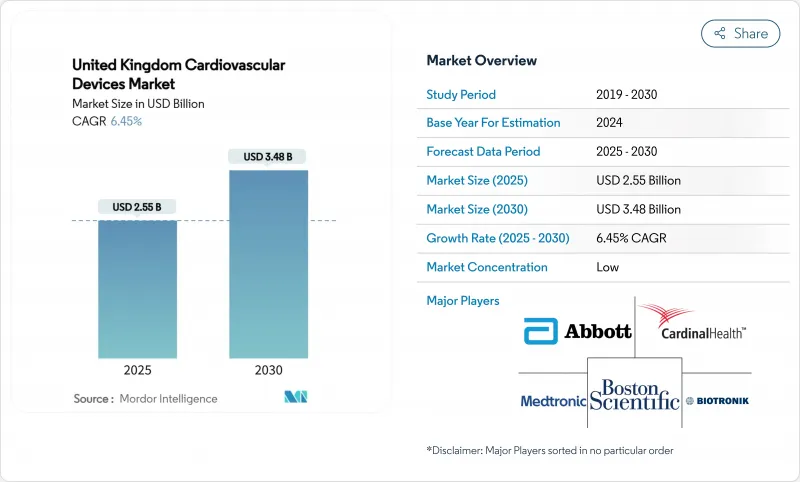

영국의 심혈관 의료기기 시장 규모는 2025년에 25억 5,000만 달러로 평가되었고, 2030년에는 34억 8,000만 달러에 이를 것으로 예측되며, 예측 기간 동안 CAGR 6.45%로 성장할 전망입니다.

탄탄한 NHS 자본 자금 지원, 가상 병동 확대 및 AI 기반 진단 기술의 신속한 도입이 브렉시트 이후 규제 중복으로 인한 비용과 복잡성 증가에도 불구하고 성장 동력을 유지하고 있습니다. 수요는 입원 기간을 단축하는 최소 침습적 시스템에 집중되고 있으며, 경피적 판막 및 펄스필드 절제술 플랫폼이 주류 치료법으로 자리 잡고 있습니다. 공급망 압박은 국내 제조 이니셔티브를 촉진한 반면, 지속가능성 요구사항은 재활용 가능한 일회용 카테터 투자 증가를 이끌고 있습니다. 전략적 인수합병과 AI 중심 제품 출시가 기술 리더십을 재편하면서 경쟁 구도는 여전히 치열합니다.

영국의 심혈관 의료기기 시장 동향 및 인사이트

NHS 장기 계획 자금 지원으로 심장 네트워크 확대, 기기 도입 가속화

2024-2025년 NHS 증액분 257억 파운드를 통해 집중 투자된 자금은 심장 네트워크 현대화와 기술 교체 주기 단축을 가능케 합니다. 수술 허브에 15억 파운드, 첨단 방사선 치료실에 7천만 파운드를 배정함으로써 의료기관들은 시술 대기열을 해소하는 동시에 신형 기기를 통합할 역량을 확보했습니다. NHS 10년 계획은 구매를 측정 가능한 성과와 연계하여 강력한 임상 증거 자료를 보유한 공급업체를 우대합니다. 통합 의료 시스템은 병원 간 공동 구매를 장려하여 주문량을 증가시키고 도입 주기를 최대 2년까지 단축시킵니다. 이러한 자금 흐름은 입증된 가치 제안을 가진 혁신 기업들의 선점자 우위를 강화합니다.

NHS “가상 병동” 프로그램 하 원격 심장 모니터링의 신속한 도입

NHS 잉글랜드는 2025년까지 50,000개의 가상 병동 병상을 제공하여 심장 치료 경로를 근본적으로 재설계할 계획입니다. 노던 케어 얼라이언스의 500병상 모델과 같은 초기 시범 사업은 급성 입원률을 30% 감소시켜 대규모 서비스 설계의 타당성을 입증했습니다. 심부전 입원률을 최대 72%까지 감소시키는 HeartLogic 및 TriageHF 기술을 승인한 NICE 지침은 빠른 확산을 더욱 뒷받침합니다. 임페리얼 칼리지 헬스케어의 학술 연구에 따르면 표준 치료에 원격 모니터링을 병행할 경우 재입원률이 76% 감소했습니다. 환자당 1,958파운드의 비용 절감 효과는 사업 타당성을 강화하며, NHS 디지털 아키텍처와 연계된 기기 제조사에 새로운 수익 채널을 열어줍니다.

특정 스텐트 모델의 높은 불량 리콜률로 의료진 신뢰도 하락

보스턴 사이언티픽의 아콜레이드(Accolade) 심박조율기와 애보트의 어슈어리티(Assurity) 시리즈에 대한 Class I 리콜은 신뢰를 흔들며 신기술에 대한 철저한 검증을 촉발했습니다. 2025년 6월 시행되는 MHRA(영국 의약품규제청) 개혁안은 능동적 감시와 신속한 사고 보고를 요구하여 규정 준수 비용을 증가시키고 출시를 지연시키고 있습니다. 부정적 여론은 리콜된 SKU를 넘어 인접 제품군 전반의 도입을 위축시키고 있습니다. 의료진은 플랫폼 전환 전 광범위한 시판 후 데이터를 요구하며, 이는 판매 주기를 연장하고 중소기업의 진입 장벽을 높입니다.

부문 분석

치료 및 수술 플랫폼은 고가치 시술을 수행하는 자원이 풍부한 심장 센터에 힘입어 2024년 매출의 58.20%를 차지했습니다. 초박형 약물 방출 스텐트와 TAVR 시스템의 채택은 시술 효율성이 구매 결정에 어떻게 영향을 미치는지 보여줍니다. 애보트의 AVEIR 리드리스 맥박조율기는 현재 혁신 의료기기 지정을 획득하며 선도 기업이 요구할 수 있는 혁신 프리미엄을 보여줍니다.

진단 및 모니터링 솔루션은 현재 규모는 작지만, 예방 및 원격 의료가 중심 무대에 오르면서 2030년까지 연평균 6.98% 성장할 것으로 전망됩니다. 12-리드 병원 기기에 필적하는 AI 기반 ECG 기기가 이러한 성장세를 뒷받침합니다. 가상 병동 확장은 표준 치료 경로에 원격 텔레메트리 기능을 통합하여 클라우드 분석을 통한 반복 수익을 증대시킵니다. 결과적으로 영국의 심혈관 의료기기 시장의 진단 부문 규모는 치료 부문보다 빠른 성장세를 보이며 향후 10년간 수익 구조를 재편할 전망입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사의 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

- 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- NHS 장기 계획의 심장 네트워크 자금 지원 확대로 기기 도입 가속화

- NHS “가상 병동” 프로그램 하에서 원격 심장 모니터링의 급속한 확산

- 선택적 심장 시술의 누적 대기 환자 증가로 최소 침습 기기로의 전환 촉진

- 고령화 영국 인구에서 증가하는 심방세동 유병률, 리듬 관리 기기 수요 증가

- 환경적으로 지속 가능한 일회용 카테터를 선호하는 정부 조달 체계

- 브렉시트 이후 규제 중복으로 중소기업의 승인 비용 증가

- 시장 성장 억제요인

- 특정 스텐트 모델의 높은 실패-리콜률로 인한 의료진 신뢰도 하락

- NHS 인력 부족으로 인한 기기 교체 주기 제약

- 브렉시트 이후 수입 주도 인플레이션으로 인한 첨단 기기 평균판매가격(ASP) 상승

- UKCA 인증 불확실성으로 인한 중소기업 제품 출시 위축

- 가치 및 공급망 분석

- 규제 상황

- 기술적 전망

- Five Forces 분석

- 신규 참가업체의 위협

- 공급기업의 협상력

- 구매자의 협상력

- 대체품의 위협

- 경쟁 기업간 경쟁 관계

제4장 시장 규모 및 성장 예측

- 제품 유형별

- 진단 및 모니터링 기기

- 심전도(ECG) 시스템

- 원격 심장 모니터

- 심장 MRI

- 심장 CT

- 심초음파/초음파

- 분획 유량 예비력(FFR) 시스템

- 치료 및 수술용 기기

- 관상동맥 스텐트

- 약제 용출 스텐트

- 베어 메탈 스텐트

- 생체 흡수성 스텐트

- 카테터

- PTCA 풍선 카테터

- IVUS/OCT 카테터

- 심장 리듬 관리

- 심박조율기

- 이식형 제세동기

- 심장 재동기 치료 기기

- 심장 벨브

- TAVR/TAVI

- 기계식 밸브

- 조직/생체 인공 밸브

- 보조 인공 심장

- 인공 심장

- 그래프트 & 패치

- 기타 심혈관 수술용 기기

- 진단 및 모니터링 기기

- 용도별

- 관상동맥 질환

- 부정맥 및 전도 장애

- 심부전 및 심근증

- 구조적 및 선천성 심장 결함

- 말초 혈관 질환

- 최종 사용자별

- 병원 및 심장 센터

- 외래 수술 센터

- 심장병/EP클리닉

- 재택치료 및 원격 모니터링 프로그램

제5장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Medtronic plc

- Abbott Laboratories

- Boston Scientific Corporation

- Edwards Lifesciences Corporation

- Koninklijke Philips NV(Philips Healthcare)

- Siemens Healthineers AG

- Johnson & Johnson(Biosense Webster & Cordis)

- GE Healthcare Technologies Inc.

- Terumo Corporation

- B. Braun Melsungen AG

- Biotronik SE & Co. KG

- LivaNova PLC

- MicroPort Scientific Corporation

- Cook Medical LLC

- WL Gore & Associates Inc.

- Getinge AB(Maquet)

- Merit Medical Systems Inc.

- Shockwave Medical Inc.

- Penumbra Inc.

- SynCardia Systems LLC

- Nipro Corporation

- Corin Group PLC

제6장 시장 기회와 전망

- 화이트 스페이스와 미충족 요구 평가

The UK cardiovascular devices market size is USD 2.55 billion in 2025 and is projected to reach USD 3.48 billion by 2030, expanding at a 6.45% CAGR during the forecast period.

Robust NHS capital funding, virtual ward roll-outs and rapid uptake of AI-enabled diagnostics are sustaining momentum even as post-Brexit regulatory duplication adds cost and complexity. Demand is concentrating around minimally invasive systems that shorten hospital stays, with transcatheter valve and pulsed-field ablation platforms becoming mainstay therapies. Supply-chain pressures have encouraged domestic manufacturing initiatives, while sustainability mandates are spurring investment in recyclable single-use catheters. Competitive dynamics remain intense, with strategic acquisitions and AI-centric product launches reshaping technology leadership.

United Kingdom Cardiovascular Devices Market Trends and Insights

NHS Long-Term Plan Funding Boost for Cardiac Networks Accelerating Device Adoption

Targeted investments channelled through the GBP 25.7 billion NHS uplift for 2024-2025 are modernising cardiac networks and enabling faster technology rotation . Allocating GBP 1.5 billion to surgical hubs and GBP 70 million to advanced radiotherapy suites gives trusts the capacity to clear procedure backlogs while integrating novel devices. The NHS 10-Year Plan ties procurement to measurable outcomes, favouring vendors with strong clinical-evidence files. Integrated care systems encourage cross-trust purchasing, increasing order volumes and shortening adoption cycles by up to two years. These funding streams thus reinforce first-mover advantages for innovators with proven value propositions.

Rapid Uptake of Remote Cardiac Monitoring under NHS "Virtual Wards" Programme

NHS England aims to deliver 50,000 virtual-ward beds by 2025, fundamentally redesigning cardiac care pathways. Early pilots such as the Northern Care Alliance's 500-bed model cut acute admissions by 30%, validating the service design at scale. NICE guidance endorsing HeartLogic and TriageHF technologies, which reduce heart-failure hospitalisations by up to 72%, further underpins rapid diffusion. Academic studies at Imperial College Healthcare show 76% fewer readmissions when tele-monitoring complements standard therapy. Savings of GBP 1,958 per patient strengthen the business case, opening new revenue channels for device makers aligned with NHS digital architecture.

High Failure-Recall Rates of Certain Stent Models Eroding Clinician Confidence

Class I recalls involving Boston Scientific's Accolade pacemakers and Abbott's Assurity series have shaken trust, prompting closer scrutiny of new technologies. MHRA reforms effective June 2025 demand active surveillance and faster incident reporting, raising compliance costs and delaying launches. Adverse publicity extends beyond recalled SKUs, dampening uptake across adjacent product categories. Clinicians now seek extensive post-market data before switching platforms, lengthening sales cycles and elevating barriers for SMEs.

Other drivers and restraints analyzed in the detailed report include:

- Growing Backlog of Elective Cardiac Procedures Driving Shift to Minimally Invasive Devices

- Increasing Prevalence of Atrial Fibrillation in Ageing UK Population Raising Demand for Rhythm-Management Devices

- NHS Workforce Shortage Constraining Equipment Replacement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Therapeutic and surgical platforms generated 58.20% of 2024 revenues, sustained by well-resourced cardiac centres performing high-value interventions. Uptake of ultrathin drug-eluting stents and TAVR systems illustrates how procedural efficiency steers purchasing decisions. Abbott's AVEIR leadless pacemaker, now under breakthrough-device designation, shows the innovation premium vendors can command .

Diagnostic and monitoring solutions, though smaller today, are projected to grow at a 6.98% CAGR through 2030 as prevention and remote care take centre stage. AI-enabled ECG devices that rival 12-lead hospital units underscore this momentum. Virtual-ward expansion embeds remote telemetry in standard care pathways, lifting recurring revenue from cloud analytics. Consequently, the UK cardiovascular devices market size for diagnostics is on path to outstrip therapeutics in growth pace, reshaping revenue mixes over the decade.

The UK Cardiovascular Devices Market Report is Segmented by Product Type (Diagnostic & Monitoring Devices, Therapeutic & Surgical Devices), Application (Coronary Artery Disease, Arrhythmia & Conduction Disorders, Heart Failure & Cardiomyopathy, Structural & Congenital Heart Defects, and More), End User (Hospitals & Cardiac Centres, Ambulatory Surgical Centres, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Medtronic

- Abbott Laboratories

- Boston Scientific

- Edward Lifesciences

- Koninklijke Philips

- Siemens Healthineers

- Johnson & Johnson (Biosense Webster & Cordis)

- GE Healthcare Technologies Inc.

- Terumo

- B. Braun

- BIOTRONIK

- LivaNova

- MicroPort

- Cook Group

- W. L. Gore & Associates

- Getinge AB (Maquet)

- Merit Medical Systems

- Shockwave Medical Inc.

- Penumbra

- SynCardia Systems

- Nipro

- Corin Group PLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

- 3.1 Market Landscape

- 3.2 Market Overview

- 3.3 Market Drivers

- 3.3.1 NHS Long-Term Plan Funding Boost for Cardiac Networks Accelerating Device Adoption

- 3.3.2 Rapid Uptake of Remote Cardiac Monitoring under NHS "Virtual Wards" Programme

- 3.3.3 Growing Backlog of Elective Cardiac Procedures Driving Shift to Minimally Invasive Devices

- 3.3.4 Increasing Prevalence of Atrial Fibrillation in Ageing UK Population Raising Demand for Rhythm Management Devices

- 3.3.5 Government Procurement Frameworks Favouring Environmentally Sustainable Single-Use Catheters

- 3.3.6 Post-Brexit Regulatory Duplication Increasing Approval Costs for SMEs

- 3.4 Market Restraints

- 3.4.1 High Failure-Recall Rates of Certain Stent Models Eroding Clinician Confidence

- 3.4.2 NHS Workforce Shortage Constraining Equipment Replacement Cycles

- 3.4.3 Import-led Inflation Raising ASPs of High-tech Devices Post-Brexit

- 3.4.4 UKCA Certification Uncertainty Deterring SME Product Launches

- 3.5 Value/ Supply-Chain Analysis

- 3.6 Regulatory Landscape

- 3.7 Technological Outlook

- 3.8 Porter's Five Forces

- 3.8.1 Threat of New Entrants

- 3.8.2 Bargaining Power of Suppliers

- 3.8.3 Bargaining Power of Buyers

- 3.8.4 Threat of Substitutes

- 3.8.5 Competitive Rivalry

4 Market Size & Growth Forecasts (Value)

- 4.1 By Product Type

- 4.1.1 Diagnostic & Monitoring Devices

- 4.1.1.1 ECG Systems

- 4.1.1.2 Remote Cardiac Monitor

- 4.1.1.3 Cardiac MRI

- 4.1.1.4 Cardiac CT

- 4.1.1.5 Echocardiography / Ultrasound

- 4.1.1.6 Fractional Flow Reserve (FFR) Systems

- 4.1.2 Therapeutic & Surgical Devices

- 4.1.2.1 Coronary Stents

- 4.1.2.1.1 Drug-Eluting Stents

- 4.1.2.1.2 Bare-Metal Stents

- 4.1.2.1.3 Bioresorbable Stents

- 4.1.2.2 Catheters

- 4.1.2.2.1 PTCA Balloon Catheters

- 4.1.2.2.2 IVUS/OCT Catheters

- 4.1.2.3 Cardiac Rhythm Management

- 4.1.2.3.1 Pacemakers

- 4.1.2.3.2 Implantable Cardioverter Defibrillators

- 4.1.2.3.3 Cardiac Resynchronization Therapy Devices

- 4.1.2.4 Heart Valves

- 4.1.2.4.1 TAVR/TAVI

- 4.1.2.4.2 Mechanical Valves

- 4.1.2.4.3 Tissue/Bioprosthetic Valves

- 4.1.2.5 Ventricular Assist Devices

- 4.1.2.6 Artificial Hearts

- 4.1.2.7 Grafts & Patches

- 4.1.2.8 Other Cardiovascular Surgical Devices

- 4.1.1 Diagnostic & Monitoring Devices

- 4.2 By Application

- 4.2.1 Coronary Artery Disease

- 4.2.2 Arrhythmia & Conduction Disorders

- 4.2.3 Heart Failure & Cardiomyopathy

- 4.2.4 Structural & Congenital Heart Defects

- 4.2.5 Peripheral Vascular Disease

- 4.3 By End User

- 4.3.1 Hospitals & Cardiac Centres

- 4.3.2 Ambulatory Surgical Centres

- 4.3.3 Cardiology/EP Clinics

- 4.3.4 Home-care & Remote Monitoring Programs

5 Competitive Landscape

- 5.1 Market Concentration

- 5.2 Market Share Analysis

- 5.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 5.3.1 Medtronic plc

- 5.3.2 Abbott Laboratories

- 5.3.3 Boston Scientific Corporation

- 5.3.4 Edwards Lifesciences Corporation

- 5.3.5 Koninklijke Philips N.V. (Philips Healthcare)

- 5.3.6 Siemens Healthineers AG

- 5.3.7 Johnson & Johnson (Biosense Webster & Cordis)

- 5.3.8 GE Healthcare Technologies Inc.

- 5.3.9 Terumo Corporation

- 5.3.10 B. Braun Melsungen AG

- 5.3.11 Biotronik SE & Co. KG

- 5.3.12 LivaNova PLC

- 5.3.13 MicroPort Scientific Corporation

- 5.3.14 Cook Medical LLC

- 5.3.15 W. L. Gore & Associates Inc.

- 5.3.16 Getinge AB (Maquet)

- 5.3.17 Merit Medical Systems Inc.

- 5.3.18 Shockwave Medical Inc.

- 5.3.19 Penumbra Inc.

- 5.3.20 SynCardia Systems LLC

- 5.3.21 Nipro Corporation

- 5.3.22 Corin Group PLC

6 Market Opportunities & Future Outlook

- 6.1 White-Space & Unmet-Need Assessment