|

시장보고서

상품코드

1846143

그린 코팅 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Green Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

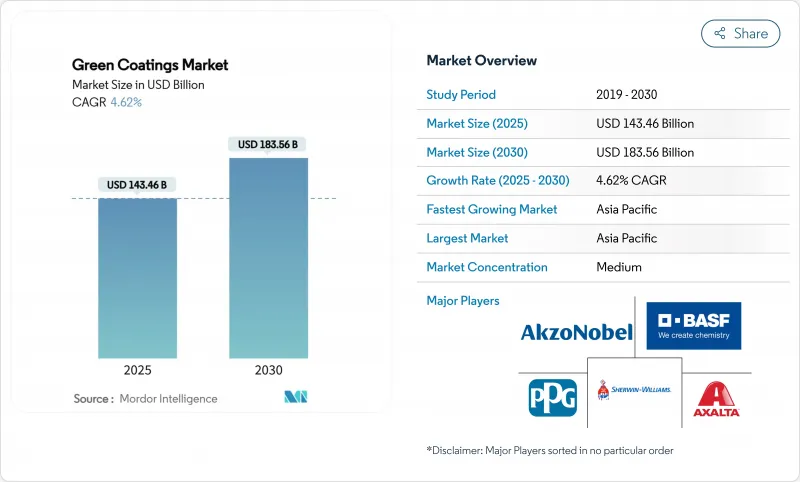

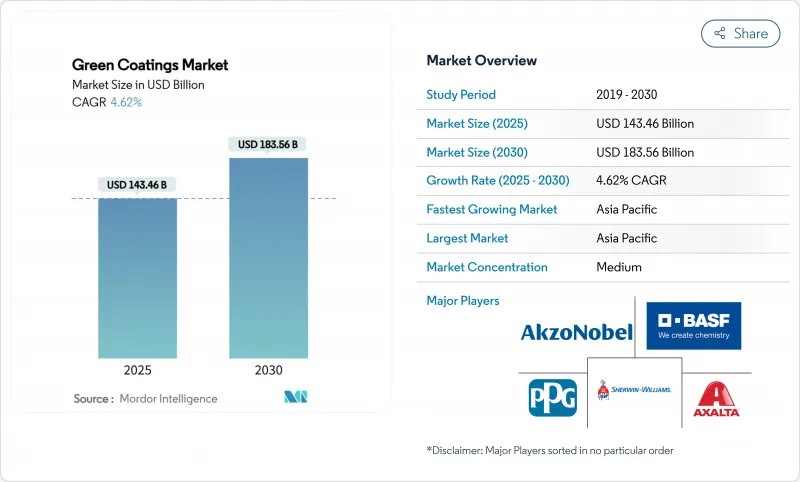

2025년 그린 코팅 시장 규모는 1,464억 6,000만 달러로, 2030년에는 1,835억 6,000만 달러에 이를 것으로 예상되며, CAGR은 4.62%를 나타낼 전망입니다.

휘발성 유기화합물(VOC)의 규제를 강화하는 규제압력, 수성화학물질과 분체기술의 급속한 진보, 자동차 및 건축용도로의 침투가 그린 코팅 시장의 중심적인 성장 엔진임에 변함이 없습니다. 캘리포니아주 사우스코스트 대기질관리지구는 개정규칙 1151에 따라 자동차용 재도장제품의 허용 VOC 함량을 삭감하고 있으며, 2033년까지 더욱 엄격한 수준을 실시할 예정입니다. 이와 병행하여 유럽연합(EU)은 2026년 8월부터 식품과 접촉하는 포장에 포함된 과불소 및 폴리불소알킬물질(PFAS)을 금지하고 포장의 처방자를 바이오의 장벽으로 방향전환시킵니다. 또한, 수성 수지의 내구성을 향상시키는 기술은 이제 용제계에 필적하는 것이 되고 있습니다.

세계의 그린 코팅 시장 동향과 인사이트

VOC 배출에 대한 엄격한 환경 규제

새로운 VOC 규제는 그린 코팅 시장에 허용되는 배합 프레임을 재정의하고 있습니다. 사우스코스트 AQMD 규정 1151은 2025년 5월부터 자동차 재도장 제품의 VOC 상한을 단계적으로 낮추고 2033년까지 가장 엄격한 임계값에 도달하여 바디샵을 수성 시스템으로 밀어 올렸습니다. 또한 EU의 포장·포장 폐기물 규칙에서는 PFAS의 상한을 개별 물질당 25ppb, 합계로 250ppb로 하고 있으며, 포장 공급업체는 불소계 화학물질을 피하는 바이오의 코팅제에 방향타를 자르고 있습니다. 이미 적합 제품 포트폴리오를 보유한 기업은 선행자 이익을 얻는 반면, 기존의 솔벤트 기반 제품에 묶여 있는 제조업체는 적합 비용 증가 및 시장 제거 가능성에 직면하게 됩니다.

낮은 VOC 건축용 페인트에 대한 수요 증가

주택 수리, 상업시설 리노베이션 및 그린 빌딩 기준에 따라 건축 밸류체인은 낮은 VOC 대체품으로 계속 끌려가고 있습니다. Sherwin-Williams에 따르면 주택 재도장 주문은 재활용이 용이하고 부피 탄소량이 적은 설계의 페인트로 현저하게 이동하고 있습니다. 수성 코팅는 현재 용제 코팅와 동등한 광택 유지성과 내마모성을 실현하고 있습니다. 악조노벨의 RUBBOL WF 3350은 실내 및 실외 목재 마감재에서 20%의 바이오 함량과 보증을 뒷받침하는 내구성을 결합한 이 전환을 보여줍니다.

가혹한 환경에서 용매 시스템과의 성능 차이

해양선체, 해상 플랫폼, 화학약품 저장 탱크 등에서는 용제를 많이 포함하는 고고형분 에폭시 수지의 장기적인 내오염성과 배리어 강도가 여전히 요구되고 있습니다. 자기수복성 실록산 하이브리드나 크롬 프리 방청제가 등장하고 있지만, 인증 사이클이 길고 선주가 미시험의 화학물질에 저항하기 때문에 상업적인 채용은 완만합니다.

부문 분석

2024년 그린 코팅 시장에서는 수성 시스템이 55.16%의 점유율을 차지해 주도권을 유지했습니다. 이점은 유리한 컴플라이언스 풋 프린트와 솔벤트 유형과 동등한 기계적 강도를 제공하는 수지의 지속적인 업그레이드에 뿌리를 두고 있습니다. 마쓰다는 공장 전체를 첨단 수성 탑코트로 전환한 것만으로 쇼룸급 광택을 유지하면서 VOC 배출량을 57% 줄였습니다. 그러나 파우더 페인트는 가장 빠른 궤도를 묘사하며 2030년까지 연평균 복합 성장률(CAGR)은 6.51%를 나타낼 전망입니다. 촉매 보조 적외선 오븐은 현재 후막을 약 225 ° C에서 불과 2 - 3 분 안에 경화시켜 생산 처리량을 높이고 광열비를 줄입니다. 샤윈 윌리엄스의 Powdura ECO는 1파운드 파우더에 반 리터 병 16개 분량의 재생 PET를 포함한 순환 디자인을 보여줍니다. 파우더 라인의 그린 코팅 시장 규모는 150℃에서 경화되는 저온 처방과 연동하여 확대될 것으로 예측되며 열에 민감한 플라스틱과 MDF 가구에 문을 엽니다. 한편, UV 경화형 액제는 순간에 가까운 경화가 요구되는 일렉트로닉스 분야에서 특수한 틈새를 차지하고 있습니다.

그린 코팅 산업은 고 솔리드 알키드와 아크릴 하이브리드에서도 이익을 얻고 있습니다. 이 시스템은 습식 가장자리와 금속 기판에 대한 접착력을 희생하지 않고 솔벤트 분율을 250g/L 이하로 줄일 수 있습니다. 이들을 종합하면, 지속가능한 화학물질이 기존 벤치마크에 부합하거나 그것을 초과할 수 있다는 인식이 강화됩니다.

지역 분석

아시아태평양은 2024년 매출액의 44.05%를 차지했으며, 2030년까지 연평균 복합 성장률(CAGR)이 가장 빠른 5.56%를 나타내는 등 우위성을 확인했습니다. 인도네시아의 생산량은 2024년에 100만톤을 돌파해 수성 장식 코팅가 현지 생산량의 67%를 차지한다는 현저한 결과가 되었습니다. 이 지역의 그린 코팅 시장은 전자상거래 창고에 적합 페인트로 전환을 강제하는 중국의 특급 포장법 GB 43352-2023에 의해 더욱 자극됩니다. 인도의 식품안전기준국(FSSAI)에 의한 식품용기 규제 강화의 움직임도 수요를 뒷받침하고 있습니다. 지속적인 도시화, 자동차 생산량 증가, OEM 페인트 공장에 대한 외국 직접 투자는 장기적인 기세를 나타냅니다.

북미는 캘리포니아의 VOC 기준과 견조한 주택 재도장 사이클에 의해 지원되며 회복 기조에 있습니다. General Motors의 3 습식 기술은 저에너지 라인의 경쟁력을 강조하고 여러 Tier 1 공급업체는 색상 전환을 단순화하는 수성 프라이머에 축 다리를 놓습니다. 캐나다는 가전제조업체가 분체 도장 부스에 투자함으로써 이러한 발전을 반영하며, 멕시코의 코일 도장 능력은 360만 달러의 업그레이드를 수행하고 이 지역에 비용 효율적인 공급 기지를 제공합니다.

유럽은 PFAS의 전반적인 규제와 탄소 경계에 대한 배려로 신속한 재제조의 동기 부여가 되는 중진하고 있습니다. 회원국은 고용제 이산화티탄의 수입에 반덤핑 관세를 부과하고 있으며, 간접적으로 처방 담당자를 적은 안료를 필요로 하는 저용제 또는 수용성 루트로 유도하고 있습니다. 독일과 프랑스는 바이오베이스 수지 신흥 기업의 인큐베이션을 계속하고 기존 콩그로 매리트와의 기술 협력을 촉진하고 있습니다.

남미, 중동, 아프리카의 신흥 지역은 완만하지만 보급이 가속하고 있습니다. 브라질의 산업 생산 높이와 사우디아라비아의 '비전 2030' 메가 프로젝트는 보호 철공 및 장식 라인에서 지속 가능한 코팅의 관련성을 높입니다. 그러나 규제 시행이 단편적이며 재생 가능 원료에 대한 접근이 제한되어 있기 때문에 일부 지역 시장에서는 페이스가 둔화되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사 전제조건

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- VOC 배출에 관한 엄격한 환경 규제

- 낮은 VOC 건축용 페인트에 대한 수요 증가

- 에너지 효율이 높은 도장 공장으로의 자동차 OEM 변화

- 내구성을 높이는 수성 수지 화학의 진보

- 농업 폐기물로부터의 바이오 베이스 수지의 채용

- 시장 성장 억제요인

- 가혹한 환경에 있어서의 용제형과의 성능 격차

- 최종 사용자에게 총 도장 비용 상승

- 바이오 베이스 원료공급 제약

- 밸류체인 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 유형별

- 수성

- 분체

- 고고형분

- UV 경화형 코팅

- 용도별

- 건축용 코팅

- 산업용 코팅

- 자동차용 코팅

- 목재용 코팅

- 포장용 코팅

- 기타 용도(전자 및 전기 코팅 등)

- 지역별

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 기타 아시아태평양

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 기타 유럽

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 기타 중동 및 아프리카

- 아시아태평양

제6장 경쟁 구도

- 시장 집중도

- 전략적인 동향

- 시장 점유율(%)/랭킹 분석

- 기업 프로파일

- AkzoNobel NV

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India Ltd.

- DAW SE

- Eastman Chemical Company

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

제7장 시장 기회와 전망

KTH 25.10.31The green coatings market size stands at USD 146.46 billion in 2025 and is forecast to reach USD 183.56 billion by 2030, translating into a 4.62% CAGR.

Regulatory pressure that tightens limits on volatile organic compounds (VOC), rapid progress in water-borne chemistries and powder technologies, and higher penetration in automotive and architectural uses remain the central growth engines of the green coating market. California's South Coast Air Quality Management District has already cut allowable VOC content in automotive refinish products under amended Rule 1151 and will enforce even stricter levels by 2033. In parallel, the European Union will prohibit per- and polyfluoroalkyl substances (PFAS) in food-contact packaging from August 2026, redirecting packaging formulators toward bio-based barriers. OEMs seeking lower energy paint shops and builders pursuing green certifications are expanding the addressable pool for sustainable solutions, while technology that lifts the durability of water-based resins now rivals solvent-borne systems.

Global Green Coatings Market Trends and Insights

Stringent Environmental Regulations on VOC Emissions

New VOC limits are redefining acceptable formulation windows for the green coating market. South Coast AQMD's Rule 1151 phases in lower VOC ceilings for automotive refinish products beginning May 2025 and culminates in the strictest thresholds by 2033, pushing body shops toward water-borne systems. On another front, the EU Packaging and Packaging Waste Regulation caps PFAS at 25 ppb per individual substance and 250 ppb total, steering packaging suppliers to bio-based coatings that avoid fluorinated chemistries. Businesses already holding portfolios of compliant products gain a first-mover advantage, whereas producers tied to legacy solvent-borne lines face incremental compliance cost and potential market exclusion.

Growing Demand for Low-VOC Architectural Coatings

Home repairs, commercial retrofits, and green-building standards continue to draw the construction value chain toward low-VOC alternatives. Sherwin-Williams reports a noticeable shift in residential repaint orders toward paints designed for easy recycling and lower embodied carbon. Water-borne formulations now deliver the same gloss retention and scrub resistance as solvent-borne equivalents. AkzoNobel's RUBBOL WF 3350 exemplifies this transition, pairing 20% bio-based content with warranty-backed durability in indoor and outdoor wood finishes.

Performance Gaps Versus Solvent-Borne in Harsh Environments

Marine hulls, offshore platforms, and chemical storage tanks still demand the long-term fouling resistance and barrier strength of high-solids epoxies rich in solvents. Although self-healing siloxane hybrids and chrome-free inhibitors are emerging, their commercial adoption is gradual because certification cycles are lengthy and shipowners resist untested chemistries.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift Toward Energy-Efficient Paint Shops

- Advances in Water-Based Resin Chemistry Enhancing Durability

- Higher Total Applied Cost for End-Users

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Water-borne systems preserved leadership in 2024 with a 55.16% share of the green coating market. Their dominance is rooted in favorable compliance footprints and constant resin upgrades that yield mechanical strength on par with solvent-borne counterparts. Mazda's plant-wide switch to advanced water-based topcoats alone lowered VOC output by 57% while retaining showroom-grade gloss. Powder coatings, however, offer the most rapid trajectory, advancing at 6.51% CAGR to 2030. Catalyst-assisted infrared ovens now cure thick films in just 2-3 minutes at roughly 225 °C, elevating production throughput and slashing utility bills. Sherwin-Williams' Powdura ECO illustrates circular design, embedding every pound of powder with recycled PET equal to sixteen half-liter bottles. The green coating market size for powder lines is projected to expand in tandem with low-temperature formulations that harden at 150 °C, opening doors to heat-sensitive plastics and MDF furniture. Meanwhile, UV-curable liquids occupy specialized niches in electronics where near-instant cure is mandatory.

The green coating industry also benefits from higher-solids alkyd and acrylic hybrids. These systems cut the solvent fraction below 250 g/L without sacrificing wet edge or adhesion to metallic substrates. Collectively, such variants reinforce the perception that sustainable chemistries can meet or exceed conventional benchmarks.

The Green Coatings Market Report is Segmented by Type (Water-Borne, Powder, and More), Application (Architectural Coatings, Industrial Coatings, and More), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific confirmed its dominance with 44.05% of 2024 revenue while charting the fastest 5.56% CAGR through 2030. Indonesian output surpassed 1 million tons in 2024, with waterborne decorative paints taking a striking 67% share of local production. The region's green coating market is further stimulated by China's express-packaging law GB 43352-2023 that forces e-commerce warehouses to switch to compliant coatings. India's move to tighten food-container rules under the Food Safety and Standards Authority (FSSAI) also underpins demand. Continued urbanization, automotive build-outs, and foreign direct investment into OEM paint shops present long-run momentum.

North America enjoys a resilient path powered by California's VOC benchmarks and robust residential repaint cycles. General Motors' three-wet technique underscores the competitive edge of low-energy lines, and multiple Tier 1 suppliers pivot to water-borne primers that simplify color changeover. Canada mirrors this progress through appliance manufacturers investing in powder booths, whereas Mexico's coil-coating capacity staking USD 3.6 million in upgrades provides the region a cost-efficient supply hub.

Europe remains a heavyweight courtesy of sweeping PFAS restrictions and carbon-border considerations that motivate rapid reformulation. Member states impose antidumping duties on high-solvent titanium dioxide imports, indirectly steering formulators toward lower-solids or water-borne routes that require less pigment. Germany and France continue to incubate bio-based resin start-ups, fostering technical collaborations with existing conglomerates.

Emerging geographies in South America, the Middle East, and Africa post moderate yet accelerating uptake. Brazil's industrial output and Saudi Arabia's Vision 2030 mega-projects heighten the relevance of sustainable coatings in protective steelwork and decorative lines. However, fragmented regulatory enforcement and limited access to renewable feedstocks temper pace in several local markets.

- AkzoNobel N.V.

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Beckers Group

- Berger Paints India Ltd.

- DAW SE

- Eastman Chemical Company

- Evonik Industries AG

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- RPM International Inc.

- Sika AG

- The Sherwin-Williams Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent environmental regulations on VOC emissions

- 4.2.2 Growing demand for low-VOC architectural coatings

- 4.2.3 Automotive OEM shift toward energy-efficient paint shops

- 4.2.4 Advances in water-based resin chemistry enhancing durability

- 4.2.5 Adoption of bio-based resins from agricultural waste

- 4.3 Market Restraints

- 4.3.1 Performance gaps versus solvent-borne in harsh environments

- 4.3.2 Higher total applied cost for end-users

- 4.3.3 Supply constraints of bio-based feedstocks

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Water-borne

- 5.1.2 Powder

- 5.1.3 High-solids

- 5.1.4 UV-cured coatings

- 5.2 By Application

- 5.2.1 Architectural Coatings

- 5.2.2 Industrial Coatings

- 5.2.3 Automotive Coatings

- 5.2.4 Wood Coatings

- 5.2.5 Packaging Coatings

- 5.2.6 Other Applications (Electronics and Electrical Coatings, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 AkzoNobel N.V.

- 6.4.2 Arkema

- 6.4.3 Asian Paints Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Beckers Group

- 6.4.7 Berger Paints India Ltd.

- 6.4.8 DAW SE

- 6.4.9 Eastman Chemical Company

- 6.4.10 Evonik Industries AG

- 6.4.11 Hempel A/S

- 6.4.12 Jotun

- 6.4.13 Kansai Paint Co., Ltd.

- 6.4.14 Nippon Paint Holdings Co., Ltd.

- 6.4.15 PPG Industries Inc.

- 6.4.16 RPM International Inc.

- 6.4.17 Sika AG

- 6.4.18 The Sherwin-Williams Company

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment