|

시장보고서

상품코드

1846214

자동차 및 운송용 커넥터 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Automotive And Transportation Connector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

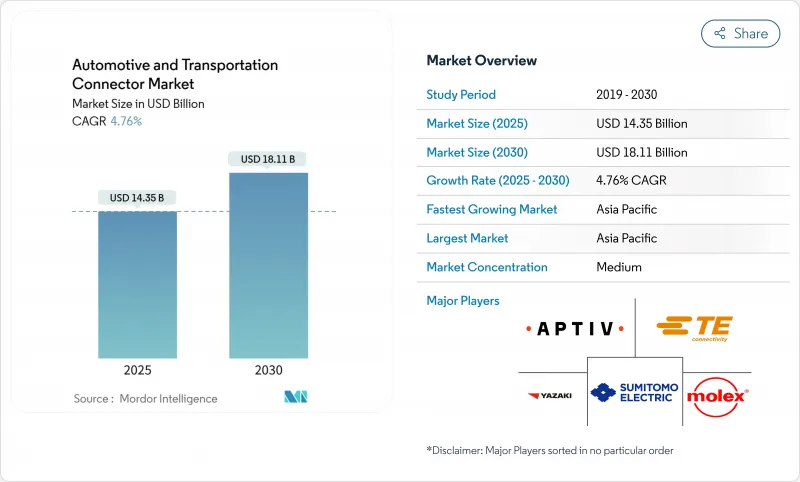

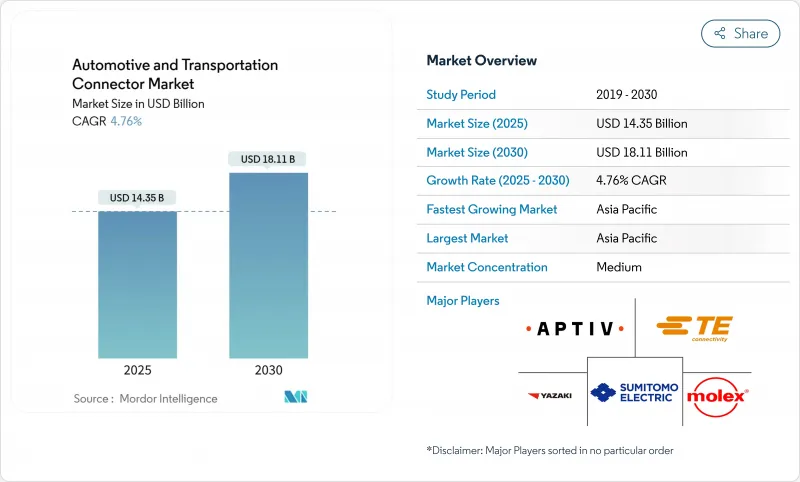

자동차 및 운송용 커넥터 시장 규모는 2025년에 143억 5,000만 달러에 이르고, CAGR은 4.76%를 나타내, 2030년에는 181억 1,000만 달러에 이를 전망입니다.

현재 성장은 수량보다 고전압 전동 파워트레인, 자율주행을 위한 멀티기가비트 데이터 교환, 빠르게 진화하는 세계 규정 준수를 지원하는 설계의 복잡성에 달려 있습니다. 수요는 성숙한 차체 배선 직기를 지원하는 레거시 Wire-to-Board 형식과 존형 차량 아키텍처에 필요한 고급 고밀도 인터페이스 사이에서 이분됩니다. 자동차 제조업체의 소프트웨어 정의 플랫폼으로의 전환은 데이터 속도 성능을 주목하는 반면, 지정 학적 우려로 형성된 조달 정책을 통해 설계 엔지니어는 여러 지역공급 기지를 인증해야 합니다. 이러한 역류는 높은 신뢰성 씰, 전자기 실드, 열 관리에 대한 개발 비용을 증가시키고 이러한 분야에 익숙한 공급업체는 자동차 1 대당 가치를 크게 높일 수 있습니다.

세계의 자동차 및 운송용 커넥터 시장 동향 및 인사이트

전동화 파가 고전압 커넥터 수요에 박차를 가한다.

전기자동차는 동등한 연소 모델보다 3배 가까이 많은 구리를 필요로 하고, 커넥터의 암페어 수와 연면 설계의 규율을 병렬로 급상승시킵니다. TE 커넥티비티의 AMP 시리즈는 이미 800V 아키텍처를 지원하며 350A 이상의 충전 전류를 견딜 수 있는 터치 안전 하우징과 최적화된 절연 경로를 사용합니다. 전류가 증가함에 따라 초고속 충전 세션 동안 열 한계를 보장하는 무전해 냉각 커넥터 어셈블리가 나타납니다. 유전 강도, 내진동성 및 자동 제조성의 균형을 맞출 수 있는 공급업체는 세계적인 EV 프로그램 중에서 우선 소스의 지위를 획득하고 있습니다.

ADAS와 인포테인먼트의 통합으로 고속 데이터 커넥터 견인

자율 주행 프로토타입은 하루에 4TB를 초과하는 데이터를 생성하므로 1dB 미만의 삽입 손실로 20GHz 신호를 전송하면서 높은 진동을 견디는 커넥터 시스템이 필요합니다. Aptiv의 H-MTD 소형 동축 제품군은 밀폐된 차량 탑재 하우징 내에서 56Gbps의 요구 사항을 충족하며 기존 FAKRA 설계에 비해 설치 면적을 줄였습니다. 1000BASE-T1과 같은 이더넷 변화는 와이어 하네스를 단일 트위스트 페어로 단순화하고 고급 차량의 경량화 목표를 지원합니다. 신뢰할 수 있는 커넥터 EMI 성능은 레벨 3 자율성을 지원하는 카메라 기반 센서 퓨전 정확도를 직접 형성합니다.

구리 가격 변동이 부품 비용을 밀어 올립니다.

미국 지질조사소에 따르면 구리 공급은 전기 수요에 뒤처지고 광석의 품위가 저하되어 채굴 비용이 상승하고 2024년에는 톤당 평균 8,490달러까지 가격이 변동하는 요인이 되었다고 합니다. 따라서 커넥터의 부품 비용은 더 자주 지수화되고 엔지니어링 팀은 전도도가 낮더라도 알루미늄 합금을 비중요한 파워 핀에 대해 테스트합니다. 재활용은 현재 세계의 구리 소비량의 32%를 차지하고 있지만, 자동차 등급의 청정도 제한으로 인해 여전히 습관이 남아 있습니다.

부문 분석

전선 대 기판 설계는 2024년 매출의 39.66%를 차지하고 계기 패널에서 영원한 역할을 뒷받침했지만, 자동차 및 운송용 커넥터 시장은 현재 주요 연구개발을 고전압 어셈블리로 향하고 있으며, 2030년까지의 CAGR 성장률은 9.45%를 나타낼 것으로 예측됩니다. 고전류 카테고리는 800V에서 작동하는 실리콘 카바이드 인버터로부터 혜택을 누리며 연면 갭 강화 및 액체 냉각 핀이 요구됩니다. RF & 동축 커넥터도 레이더와 카메라의 수가 증가함에 따라 다시 중요성이 커지고 있습니다. JAE와 같은 공급업체는 200A CHAdeMO 플러그에 전자기 잠금 장치와 긴급 정합 해제를 통합하여 세계 안전 표준을 충족합니다.

표준 ECU 패키지는 여전히 기판 대 기판의 메자닌 데크에 기울어져 있지만, 존 하드웨어는인치당 120핀 이상의 밀도를 제공합니다. 하나의 헤더에 신호 블레이드와 50A 블레이드를 혼합하는 하이브리드 하우징은 SKU 수를 줄이고 자동 픽앤플레이스를 간소화합니다. 그 결과, 모듈 통합자는 커넥터를 범용 패스닝 포인트가 아닌 기능적 서브시스템으로 취급하게 되어 자동차 및 운송용 커넥터 시장에서 프리미엄 가격을 유지하고 있습니다.

차체 배선과 배전은 2024년 지출액의 38.25%를 차지했지만, 카메라, 레이더, 라이더 센서의 보급이 진행됨에 따라 ADAS와 자율주행 일렉트로닉스는 12.23%의 연평균 복합 성장률(CAGR)을 나타낼 것으로 보입니다. 이러한 상승 동향으로 ADAS Connectivity는 전문 공급업체에게 마진 확대에 대한 최단 경로가 됩니다. 콕핏 엔터테인먼트 플랫폼은 몰입형 디스플레이와 무선 업그레이드가 멀티기가비트 백본을 필요로 하기 때문입니다.

파워트레인 및 배터리 시스템용 자동차 및 운송용 커넥터 시장 규모는 EV의 대수 증가에 연동하여 상승할 것으로 예측되며, 차폐된 고전압 인터페이스의 스케일 이코노미의 여지가 넓어지고 있습니다. 반면에 안전 보안 모듈은 중복 전원 핀을 단일 하우징에 통합하여 ISO 26262 진단 요구 사항을 충족하면서 공간 오버헤드를 제한합니다.

지역 분석

아시아태평양은 2024년 매출의 45.31%를 차지하며 세계 최대의 자동차 조립 거점인 동시에 가장 급성장하고 있는 전동 이동성 클러스터로서의 지위를 반영했습니다. 중국의 OEM은 고전압 커넥터와 배터리 관리 커넥터에 집중적인 수요를 낳고 일본과 한국은 세계의 고급 자동차 제조업체에 정밀한 기판 대 기판 커넥터와 동축 커넥터를 공급하고 있습니다. 인도네시아의 승용차 생산 대수는 2024년에 140만대에 달했지만, 이는 동남아시아가 2차 생산 거점으로 부상하고 미국 조달 규칙이 중국제 부품의 인정 패스를 엄격히 해도 현지의 커넥터 금형 제작을 자극하는 것을 강조했습니다.

북미는 IP68 이상의 밀폐형 원형 파워 커넥터를 선호하는 프리미엄 트럭 수요를 유지하고 있습니다. 인플레이션 삭감법이 국내 배터리 공장에 인센티브를 주고 고전압 단자의 현지 공급에 박차를 가합니다. 2024년 캐나다의 구리 생산량은 50만 8,250톤으로 가격 변동을 헤지하는 지역의 프레스 가공 공장에 원료공급력을 확보했습니다. 커넥터 제조업체는 2027년에 예정된 미국 내 함량 규제로 중국제 텔레매틱스 모듈의 사용이 금지되어 듀얼 소스화가 가속화됩니다.

유럽에서는 첨단 EV 생산과 수입차 급증으로 인한 비용 압력이 결합되어 있습니다. 독일에서는 2024년에 135만대의 전기차가 생산되었지만 EU 제조업체는 같은 해 5만 3,669명의 고용을 잃었습니다. 유럽위원회의 전략적 대화(Strategic Dialogue)는 상호 운용가능한 10BASE-T1S 네트워크에 호라이즌(Horizon) 자금을 투입하여 하네스의 무게를 줄이는 한편, 중동 및 아프리카 프로젝트는 걸프의 스마트 시티 투자와 남아프리카 수출 계약을 활용합니다. 영국은 2027년부터 산업용 전력요금의 25% 인하를 공약하고 커넥터 스탬핑의 경쟁력 회복을 목표로 하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

- 조사 전제조건과 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 전기화 급증으로 고전압 커넥터 수요를 촉진

- ADAS와 인포테인먼트 통합이 고속 데이터 커넥터를 견인

- 존 E/E 아키텍처로의 이행이 고밀도 보드 엣지 커넥터를 뒷받침

- 세이프티 크리티컬한 컴플라이언스(ISO 26262, UN R155)가 신뢰성 요구 증진

- 기가비트 이더넷 및 FAKRA-Mini 동축 인터페이스로의 전환

- 내연 기관차의 48V 서브 시스템의 상승

- 시장 성장 억제요인

- 구리 가격 변동으로 인한 부품 비용 상승

- 저비용 조달을 제한하는 현지 조달의 의무화

- 커넥터의 씰이나 압착 불량에 의한 리콜

- 차량 탑재 무선 센서 노드 증가에 의한 하드 와이어 포트의 감소

- 가치/공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모·성장 예측

- 제품 유형별

- 전선 대 기판 커넥터

- 기판 대 기판 커넥터

- 전선 대 전선 커넥터

- 고전압/EV 커넥터

- RF 및 동축 커넥터

- 모듈러/하이브리드 커넥터

- 용도별

- 안전 및 보안

- 차체 배선 및 전력 분배

- 운전석, 연결성 및 엔터테인먼트(CCE)

- 파워트레인 및 배터리 시스템

- 첨단 운전자 보조/자율주행

- 차량 유형별

- 승용차

- 소형 상용차

- 중대형 상용차

- 이륜차

- 추진별

- 내연기관 자동차

- 하이브리드 전기자동차

- 플러그인 하이브리드 자동차

- 배터리 전기자동차

- 판매 채널별

- OEM

- 애프터마켓

- 지역별

- 북미

- 미국

- 캐나다

- 기타 북미

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 기타 아시아태평양

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이집트

- 튀르키예

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장의 집중도

- 전략적인 동향

- 시장 점유율 분석

- 기업 프로파일

- TE Connectivity

- Yazaki Corporation

- Aptiv PLC

- Amphenol Corporation

- Molex(Koch Industries)

- Sumitomo Electric Industries

- Lear Corporation

- Leoni AG

- Korea Electric Terminal(KET)

- Rosenberger Hochfrequenztechnik

- Luxshare Precision Industry

- JST Mfg.

- HARTING Technology Group

- Furukawa Electric

- ITT Cannon

- Hirose Electric

- Japan Aviation Electronics(JAE)

제7장 시장 기회와 전망

KTH 25.11.07The automotive and transportation connector market size stands at USD 14.35 billion in 2025 and is tracking a 4.76% CAGR that will lift revenue to USD 18.11 billion by 2030.

Growth now hinges less on sheer unit volume and more on the design complexity that supports high-voltage electrified powertrains, multi-gigabit data exchange for automated driving, and fast-evolving global compliance regimes. Demand bifurcates between legacy wire-to-board formats that anchor mature body-wiring looms and advanced high-density interfaces required for zonal vehicle architectures. Automakers' shift to software-defined platforms keeps data-rate performance in focus, while sourcing policies shaped by geopolitical concerns push design engineers to qualify multiple regional supply bases. These crosscurrents elevate development spending on high-reliability seals, electromagnetic shielding, and thermal management, allowing suppliers that master these disciplines to capture outsized value per vehicle.

Global Automotive And Transportation Connector Market Trends and Insights

Electrification Surge Spurring High-Voltage Connector Demand

Electric vehicles require nearly three times more copper than comparable combustion models, driving a parallel jump in connector amperage and creepage design discipline. TE Connectivity's AMP+ range already supports 800 V architectures, using touch-safe housings and optimized insulation paths that withstand charging currents above 350 A . Immersion-cooled connector assemblies are emerging as currents climb, ensuring thermal limits during ultra-fast charging sessions. Suppliers capable of balancing dielectric strength, vibration resistance, and automated manufacturability gain preferred-source status among global EV programs.

ADAS and Infotainment Integration Driving High-Speed Data Connectors

Autonomous prototypes generate over 4 TB of data per day, dictating connector systems that endure high vibration while transmitting 20 GHz signals at under-1 dB insertion loss. Aptiv's H-MTD miniature coax family meets 56 Gbps requirements within a sealed automotive housing, shrinking footprint versus legacy FAKRA designs. Ethernet shifts such as 1000BASE-T1 simplify wiring harnesses to a single twisted pair, supporting weight reduction targets on premium vehicles. Reliable connector EMI performance directly shapes camera-based sensor fusion accuracy that underpins level-3 autonomy.

Copper-Price Volatility Inflating BOM Costs

Global copper supply lags electrification demand, and the US Geological Survey notes declining ore grades lift extraction costs, contributing to price swings that averaged USD 8,490 per tonne in 2024. Connector bills of material are therefore indexed more frequently, and engineering teams test aluminum alloys for non-critical power pins even though conductivity remains lower. Recycling now covers 32% of worldwide copper consumption, but automotive-grade cleanliness limits still confine the practice .

Other drivers and restraints analyzed in the detailed report include:

- Shift to Zonal Architectures Boosting High-Density Board-Edge Connectors

- Safety-Critical Compliance Heightening Reliability Needs

- Local-Sourcing Mandates Limiting Procurement Flexibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wire-to-board designs kept 39.66% of 2024 revenue, confirming their evergreen role in instrumentation panels, yet the automotive and transportation connector market now directs major R&D toward high-voltage assemblies that will grow 9.45% CAGR to 2030. The high-current category benefits from silicon-carbide inverters operating at 800 V, which demand reinforced creepage gaps and liquid-cooled pins. RF & coax connectors also gain renewed relevance as radar and camera counts increase. Suppliers such as JAE incorporate electromagnetic locks and emergency unmating in 200 A CHAdeMO plugs to satisfy global safety codes.

Standard ECU packaging still leans on board-to-board mezzanine decks, but zonal hardware elevates density beyond 120 pins per inch. Hybrid housings that mix signal and 50 A blades inside one header reduce SKU count and simplify automated pick-and-place. As a result, module integrators now treat the connector as a functional sub-system rather than a commodity fastening point, sustaining premium pricing inside the automotive and transportation connector market.

Body wiring and power distribution commanded 38.25% of 2024 spend, yet ADAS and autonomous electronics will log a 12.23% CAGR as camera, radar, and lidar sensor proliferation intensifies. That uptrend positions ADAS connectivity as the fastest pathway to margin expansion for specialized suppliers. Cockpit entertainment platforms follow closely because immersive displays and over-the-air upgrades need multi-gigabit backbones.

The automotive and transportation connector market size for powertrain and battery systems is projected to climb in tandem with EV unit growth, opening space for scale economies on shielded high-voltage interfaces. Meanwhile, safety-security modules integrate redundant power pins within a single housing, limiting space overhead while meeting ISO 26262 diagnostics requirements.

The Automotive and Transportation Connector Market Report is Segmented by Product Type (Wire-To-Board Connectors, Board-To-Board Connectors, and More), Application (Safety and Security, Body Wiring and Power Distribution, and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and More), Propulsion, Sales Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific contributed 45.31% of 2024 revenue, reflecting its position as both the world's largest vehicle assembly hub and the fastest-growing electric-mobility cluster. Chinese OEMs generate concentrated demand for high-voltage and battery-management connectors, while Japan and Korea supply precision board-to-board and coaxial formats for global premium nameplates. Indonesia's passenger-car output of 1.4 million units in 2024 underscored Southeast Asia's rise as a secondary production base that stimulates local connector tooling even as US sourcing rules tighten qualification paths for Chinese-made parts.

North America maintains premium-truck demand that favors sealed circular power connectors rated beyond IP68. The Inflation Reduction Act channels incentives into domestic battery plants, spurring localized high-voltage terminal supply. Canadian copper output of 508,250 tonnes in 2024 shores up raw-material availability for regional stamping operations that hedge price shocks. Connector makers also confront upcoming U.S. content rules slated for 2027 that bar Chinese telematics modules, accelerating dual-source qualifications.

Europe combines advanced EV production with cost pressure from surging imports. Germany built 1.35 million electric cars in 2024, yet EU manufacturers lost 53,669 jobs in the same year. The European Commission's Strategic Dialogue is funneling Horizon funds into interoperable 10BASE-T1S networking to cut harness weight, while Middle East and African projects tap Gulf smart-city investments and South-African export contracts. The UK's pledge to lower industrial power tariffs by 25% from 2027 aims to restore connector stamping competitiveness.

- TE Connectivity

- Yazaki Corporation

- Aptiv PLC

- Amphenol Corporation

- Molex (Koch Industries)

- Sumitomo Electric Industries

- Lear Corporation

- Leoni AG

- Korea Electric Terminal (KET)

- Rosenberger Hochfrequenztechnik

- Luxshare Precision Industry

- JST Mfg.

- HARTING Technology Group

- Furukawa Electric

- ITT Cannon

- Hirose Electric

- Japan Aviation Electronics (JAE)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrification Surge Spurring High-Voltage Connector Demand

- 4.2.2 ADAS and Infotainment Integration Driving High-Speed Data Connectors

- 4.2.3 Shift to Zonal E/E Architectures Boosting High-Density Board-Edge Connectors

- 4.2.4 Safety-Critical Compliance (ISO 26262, UN R155) Heightening Reliability Needs

- 4.2.5 Migration to Gigabit Ethernet and FAKRA-Mini Coax Interfaces

- 4.2.6 Emerging 48 V Sub-Systems in ICE Vehicles

- 4.3 Market Restraints

- 4.3.1 Copper-Price Volatility Inflating BOM Costs

- 4.3.2 Local-Sourcing Mandates Limiting Low-Cost Procurement

- 4.3.3 Recalls from Connector Seal or Crimp Failures

- 4.3.4 Rising In-Vehicle Wireless Sensor Nodes Reducing Hard-Wired Ports

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product Type

- 5.1.1 Wire-to-Board Connectors

- 5.1.2 Board-to-Board Connectors

- 5.1.3 Wire-to-Wire Connectors

- 5.1.4 High-Voltage/EV Connectors

- 5.1.5 RF & Coax Connectors

- 5.1.6 Modular/Hybrid Connectors

- 5.2 By Application

- 5.2.1 Safety and Security

- 5.2.2 Body Wiring and Power Distribution

- 5.2.3 Cockpit, Connectivity and Entertainment (CCE)

- 5.2.4 Powertrain and Battery Systems

- 5.2.5 Advanced Driver-Assistance/Autonomous

- 5.3 By Vehicle Type

- 5.3.1 Passenger Cars

- 5.3.2 Light Commercial Vehicles

- 5.3.3 Medium and Heavy Commercial Vehicles

- 5.3.4 Two-Wheelers

- 5.4 By Propulsion

- 5.4.1 Internal-Combustion Engine Vehicles

- 5.4.2 Hybrid Electric Vehicles

- 5.4.3 Plug-in Hybrid Electric Vehicles

- 5.4.4 Battery Electric Vehicles

- 5.5 By Sales Channel

- 5.5.1 OEM

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Egypt

- 5.6.5.4 Turkey

- 5.6.5.5 South Africa

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 TE Connectivity

- 6.4.2 Yazaki Corporation

- 6.4.3 Aptiv PLC

- 6.4.4 Amphenol Corporation

- 6.4.5 Molex (Koch Industries)

- 6.4.6 Sumitomo Electric Industries

- 6.4.7 Lear Corporation

- 6.4.8 Leoni AG

- 6.4.9 Korea Electric Terminal (KET)

- 6.4.10 Rosenberger Hochfrequenztechnik

- 6.4.11 Luxshare Precision Industry

- 6.4.12 JST Mfg.

- 6.4.13 HARTING Technology Group

- 6.4.14 Furukawa Electric

- 6.4.15 ITT Cannon

- 6.4.16 Hirose Electric

- 6.4.17 Japan Aviation Electronics (JAE)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment