|

시장보고서

상품코드

1846261

망막 임플란트 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Retinal Implants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

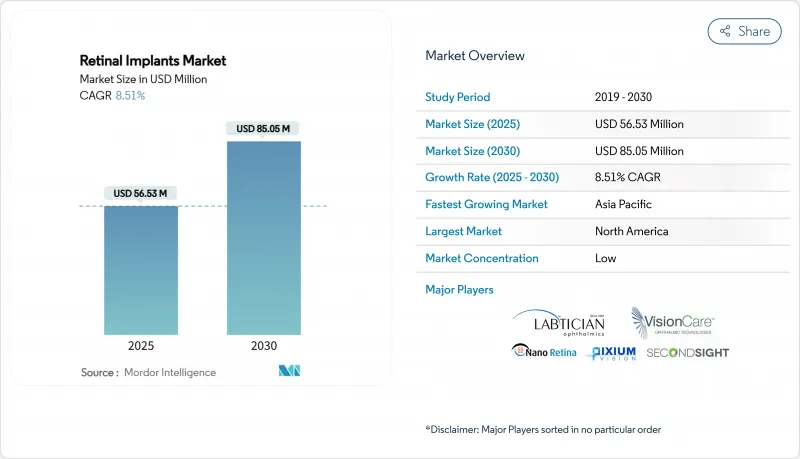

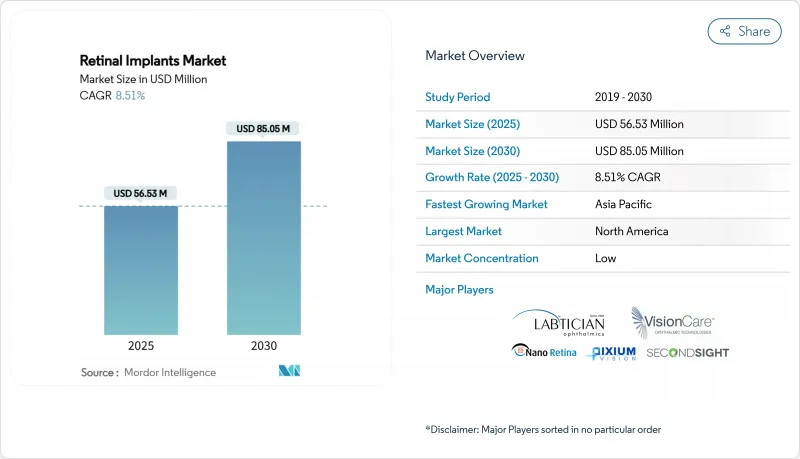

망막 임플란트 시장 규모는 2025년에 5,653만 달러로 평가되고, 2030년에는 8,505만 달러에 이르며, CAGR 8.51%를 나타낼 것으로 예측됩니다.

외과 수술의 채용이 증가하고, 무선 신경 보철 공학이 급속히 진보하고, 미국의 획기적인 장치의 길이 보다 부드러워진 것이 총체로서 지속적인 수요를 키우고 있습니다. 임상시험은 현재 측정 가능한 기능적 시력 회복을 입증하고 있으며, 외과의사는 변성 시계열의 초기 단계에서 임플란트를 배치할 수 있습니다. 동시에, 유전자 치료의 기세는 보다 고해상도의 전극 어레이나 AI를 구사한 화상 처리에 의한 차별화를 제조업체에 촉구하고 있습니다. Science Corporation의 픽슘 비전 자산 인수와 같은 전략적인수는 차세대 시스템에 대한 자본 형성의 가속을 시사합니다.

세계의 망막 임플란트 시장 동향과 인사이트

세계 시력 상실 부담 증가

세계에서는 5억 9,600만 명이 중등도에서 중증의 시력장애를 겪었고, 4,300만 명이 실명하고 있습니다. 기존의 약물 요법은 시세포 상실을 지연시킬 수는 있지만 회복시킬 가능성은 거의 없기 때문에 기능적 시력이 네비게이션 임계값 아래로 떨어지면 의지 장비에 대한 수요가 높아집니다. 당뇨병 망막증과 황반변성의 스크리닝 프로그램에서는 특히 고령화가 급속히 진행되는 아시아태평양에서 더 많은 후보자가 조기에 발견되고 있습니다. 질병 비용 분석에 따르면 유전성 망막 질환은 북미에서 매년 135억-320억 달러를 유출하고 있어 시력 회복 기구를 사용하는 경제적 근거가 강해지고 있습니다. 이러한 역학적 압력이 증가함에 따라 망막 임플란트 시장은 원래 망막 색소 변성 틈새 시장을 넘어 계속 확대되고 있습니다.

신경 보철 기술 혁신

소형화된 무선 모듈은 현재 4.6mm×3.7mm×0.9mm의 256 전극 다이아몬드 어레이를 통합하여 부피가 큰 송신기 팩을 제거하고 각막을 통해 레이저 전력을 끌어냅니다. PRIMA와 같은 광기전력 임플란트는 배터리를 내장하지 않고 근적외선을 망막 자극으로 자율적으로 변환하여 장기 장비의 고장 위험을 줄입니다. 머신러닝 알고리즘은 시선 방향을 자극 패턴에 매핑하여 낮은 콘트라스트 환경에서 얼굴과 물체의 인식을 향상시킵니다. 후두엽에 내장된 400개의 무선 자극기로 테스트된 피질 인공 시각장치는 온전한 시신경이 부족한 환자를 대상으로 하고 잠재력의 폭을 넓히고 있습니다. 이러한 혁신은 환자의 이동성, 수술의 간편성, 화질의 향상으로 이어져 망막 임플란트 시장의 꾸준한 성장을 지원합니다.

장비 및 수술의 높은 비용

정가는 3-4시간의 수술, 입원에 의한 회복, 최장 2년간의 로비전 재활을 제외하면 임플란트 1개당 10만 달러 가까이에 머물고 있습니다. 1인당 지출이 비교적 적은 라틴아메리카와 아프리카의 의료 제도에서는 이러한 경제성이 가중되고 있습니다. 생산량이 적기 때문에 밀폐형 전극 어레이나 사파이어 광학계의 부품 비용이 상승하고 있습니다. 미국에서도 메디케어는 여전히 좁은 지역 적용 결정에 의존하고 있으며, 지불을 승인하기 전에 철저한 문서화를 요구하기 때문에 환자의 대기 시간이 길어지고 있습니다. 스케일 메리트나 모듈 제조가 가격을 인하할 때까지 저소득 지역에서의 보급은 스티커 쇼크에 머물러 있다고 생각됩니다.

부문 분석

에피레티날 어레이는 Argus II의 레거시와 외과 의사의 수술에 대한 숙련도를 배경으로 2024년 망막 임플란트 시장 점유율의 42.54%를 차지했습니다. 망막하 어레이는 포토다이오드 매트릭스를 생존하는 쌍극세포 가까이에 집적하여 콘트라스트를 향상시키지만 수술 위험을 높입니다. Phoenix 99로 대표되는 맥락막 상형은 망막 관통을 회피하여 박리율을 낮추고 CAGR 예측 10.45%를 나타낼 전망입니다.

또한 공막과 맥락막 사이에 하드웨어를 설치하기 때문에 적출 재치환이 보다 간편해진다는 이점도 있습니다. PRIMA와 같은 광기전력 망막하 칩은 유럽에서 보급되고 있지만, 피질 임플란트는 아직 조사 중입니다. 해상도가 높아짐에 따라 제조업체는 다초점 전극 클러스터로 증례 구성을 이동시키고 망막 임플란트 시장이 임플란트의 모양에 관계없이 다양화를 계속할 것으로 기대합니다.

망막 색소 변성증은 2024년 망막 임플란트 시장 규모의 47.54%를 차지했는데, 이는 잘 이해된 자연사와 명확한 적격 임계값을 반영하고 있습니다. 스타가르트병은 유전체 스크리닝에 의해 조기에 보인자가 확인되어 적극적인 임플란트 치료가 받아들여지기 때문에 CAGR 10.55%를 나타낼 전망입니다.

건조한 노화 황반 변성증은 또 다른 성장 영역입니다. PRIMA의 지리적 위축증 코호트에서는 12개월 후의 편지 점수의 일관된 향상이 보였습니다. 맥락막혈증과 같은 희귀한 이영양증에서는 산발적인 동정적 이식이 이루어지고 있지만, 유전자 치료는 이들 환자에게 다른 길을 제공합니다. 그럼에도 불구하고 후기 유전성 망막 질환은 여전히 망막 임플란트 산업의 핵심을 담당하고 있습니다.

지역 분석

북미는 2024년 세계 매출의 40.12%를 차지했지만, 이는 미국의 특정 지역에서 메디케어 상환과 매우 중요한 IDE 시험을 실시하는 견고한 임상 책임 의사 네트워크에 의해 지원되고 있습니다. 캘리포니아, 일리노이, 텍사스의 아카데믹 센터에서는 연간 사례 수가 가장 많습니다. 캐나다는 국민 모두 보험제도를 활용하여 액세스를 확대하고 있지만, 수술의 상한과 대기시간은 여전히 남아 있습니다. 보험 회사와의 협상은 장기적인 비용 상쇄와 로비전 케어에 달려 있으며, 병원 구매주기를 형성하고 있습니다.

아시아태평양은 2030년까지 연평균 복합 성장률(CAGR)이 9.65%로 가장 빠르게 성장하고 있으며, 중국과 인도에서 인구의 고령화와 당뇨병 망막증 유병률의 상승이 그 원동력이 되고 있습니다. 일본의 국민 모두 보험제도는 이미 고액 의료비 조성 제도 하에서 망막하 임플란트를 커버하고 있어, 안정된 파이프라인량을 낳고 있습니다. 한국의 의료기술평가기관은 최근 맥락막상 프로토타입의 일부 상환을 승인하고 국내 생산에 대한 조성을 촉진했습니다. 도시와 지방 간의 격차는 여전히 심각하기 때문에 원격 의료에 의한 후속 조치가 대부분의 새로운 전개 계획에 통합되었습니다.

유럽에서는 정책에 의해 지원되는 완만한 성장을 볼 수 있습니다. 독일의 DRG 코드에서는 이식과 프로그래밍 세션이 모두 환불되고 프랑스에서는 지역 의료 예산에 수술 후 재활이 포함됩니다. 영국 NICE는 첨단 무선 시스템의 비용 효과적인 지표를 재검토하고 있습니다. 초기의 실사회에 있어서의 근거가, 기존 유선 모델보다 질 조정 생존 연수가 높다는 것을 시사했기 때문입니다. EMA의 Advanced Therapy Fast Track은 각국의 장비 신청과 중복되므로 시장 진입이 길어질 수 있지만 엄격한 안전 모니터링이 보장됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 도입

- 조사 전제조건과 시장 정의

- 연구 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 세계의 시력 상실의 부담 증가

- 신경보장구의 기술 혁신

- 유리한 규제와 상환환경

- 노년 인구 증가

- 안과 연구 개발에 대한 투자 증가

- 신흥 시장의 헬스케어 인프라 확대

- 시장 성장 억제요인

- 고액의 의료기기와 처치 비용

- 제한된 임상 효과와 환자의 결과

- 복잡한 규제와 제조의 과제

- 대체 시력 회복 요법의 이용 가능성

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자·소비자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계의 강도

제5장 시장 규모·성장 예측

- 임플란트 유형별

- 망막상 임플란트(예 : Argus II)

- 망막하 임플란트(알파 AMS 등)

- 초황반상 임플란트

- 이식형 소형 망원경(IMT)

- 기타 임플란트

- 적응 질환별

- 색소성 망막염

- 연령 관련 황반변성

- 스타가르트병

- 기타 질환

- 최종 사용자별

- 병원

- 안과 전문 클리닉

- 학술 및 연구 센터

- 기술별

- 무선 전원 공급 시스템

- 유선/공막 관통 케이블 시스템

- 적응형 영상 처리 및 AI 통합

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Second Sight Medical Products, Inc.

- Pixium Vision SA

- VisionCare, Inc.

- Nano Retina

- Retina Implant AG

- Bionic Vision Technologies(BVT)

- iBIONICS

- Intelligent Implants Ltd.

- LambdaVision, Inc.

- Optobionics Corp.

- iSight Technologies

- NIDEK Co., Ltd.

- Boston Retinal Implant Project

- i-Med Technology Inc.

- GenSight Biologics

- Korey Implant Technologies

- Biomedical Innovations Pty Ltd.

- Shanghai NIDEK Ophthalmic Products

- Vivani Medical

- Advanced Bionics AG

제7장 시장 기회와 전망

KTH 25.10.31The retinal implants market size is valued at USD 56.53 million in 2025 and is forecast to reach USD 85.05 million by 2030, advancing at an 8.51% CAGR.

Increasing surgical adoption, rapid gains in wireless neuro-prosthetic engineering, and a smoother United States breakthrough-device pathway collectively nurture sustained demand. Clinical trials now document measurable functional vision restoration, allowing surgeons to position implants earlier in the degenerative timeline. At the same time, gene-therapy momentum is nudging manufacturers to differentiate through higher-resolution electrode arrays and AI-powered image processing. Strategic acquisitions-such as Science Corporation's purchase of Pixium Vision assets-signal accelerating capital formation around next-generation systems.

Global Retinal Implants Market Trends and Insights

Rising Global Burden of Vision Loss

Globally, 596 million people live with moderate-to-severe vision impairment and 43 million are blind, creating a substantial pool of late-stage patients suitable for implantation. Conventional pharmacotherapy slows but rarely reverses photoreceptor loss, so demand gravitates to prosthetics once functional vision falls below navigation thresholds. Screening programs for diabetic retinopathy and macular degeneration are flagging more candidates earlier, particularly in Asia-Pacific where population aging is rapid. Cost-of-illness analyses indicate inherited retinal diseases drain USD 13.5 billion-32 billion each year in North America, strengthening the economic case for device-based vision restoration. As these epidemiologic pressures mount, the retinal implants market continues to scale beyond its original retinitis-pigmentosa niche.

Technological Innovations in Neuroprosthetics

Miniaturized wireless modules now integrate 256-electrode diamond arrays measuring 4.6 mm X 3.7 mm X 0.9 mm and draw laser power through the cornea, eliminating bulky transmitter packs. Photovoltaic implants such as PRIMA autonomously convert near-infrared illumination into retinal stimulation without implanted batteries, reducing long-term device failure risk. Machine-learning algorithms map gaze direction to stimulation patterns, improving recognition of faces and objects in low-contrast environments. Cortical visual prostheses-tested with 400 wireless stimulators embedded in the occipital lobe-target patients lacking an intact optic nerve, broadening the potential pool. These breakthroughs collectively lift patient mobility, surgical simplicity, and image quality, underpinning steady unit growth for the retinal implants market.

High Cost of Devices and Procedures

List prices remain near USD 100,000 per implant, excluding a 3- to 4-hour operative session, inpatient recovery, and up to two years of low-vision rehabilitation. Such economics deter health systems in Latin America and Africa where per-capita expenditure is comparatively low. Production volumes remain small, inflating component costs for hermetically sealed electrode arrays and sapphire optics. Even in the United States, Medicare still relies on narrow Local Coverage Determinations, demanding exhaustive documentation before authorizing payment, extending patient wait times. Until economies of scale or modular manufacturing trim prices, sticker shock will cap penetration in lower-income regions.

Other drivers and restraints analyzed in the detailed report include:

- Favorable Regulatory and Reimbursement Climate

- Growing Geriatric Population

- Limited Clinical Efficacy and Patient Outcomes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epiretinal arrays delivered 42.54% of the retinal implants market share in 2024 on the strength of the Argus II legacy and surgeons' procedural familiarity. Subretinal alternatives integrate photodiode matrices closer to surviving bipolar cells, improving contrast but adding surgical risk. Suprachoroidal designs, exemplified by the Phoenix 99, avoid retinal penetration, lowering detachment rates and driving a 10.45% CAGR forecast.

Suprachoroidal platforms also benefit from simpler explant revision because hardware rests between sclera and choroid layers. Photovoltaic subretinal chips like PRIMA are gaining European traction, whereas cortical implants remain investigational. As resolution rises, manufacturers anticipate shifting case mix toward multi-focal electrode clusters, ensuring the retinal implants market continues diversifying across implant geometries.

Retinitis pigmentosa captured 47.54% of the retinal implants market size in 2024, reflecting well-understood natural history and clear eligibility thresholds. Stargardt disease is expanding at 10.55% CAGR as genomic screening identifies carriers earlier, making them receptive to proactive implantation.

Dry age-related macular degeneration is another growth locus; PRIMA's geographic-atrophy cohort showed consistent letter-score gains at 12 months. Rare dystrophies such as choroideremia see sporadic compassionate-use implants, but gene therapy is giving these patients alternative avenues. Even so, late-stage inherited retinal disease remains the core driver for the retinal implants industry.

The Retinal Implants Market Report is Segmented by Implant Type (Epiretinal, and More), Disease Indication (Retinitis Pigmentosa, AMD, Stargardt, and Other Disease Indications), End User (Hospitals, Clinics, and Research Centers), Technology (Wireless, Wired, and AI Integration), and Geography (North America, Europe, Asia-Pacific, MEA, South America). Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America delivered 40.12% of global revenue in 2024, sustained by Medicare reimbursement in select U.S. jurisdictions and a robust investigator network running pivotal IDE trials. Academic centers in California, Illinois, and Texas collectively implanted the largest annual case numbers. Canada leverages universal coverage to widen access, though procedure caps and queue times persist. Insurer negotiations hinge on long-term cost offset versus low-vision care, shaping hospital purchasing cycles.

Asia-Pacific is the fastest mover with a 9.65% CAGR through 2030, driven by population aging and rising diabetic retinopathy prevalence in China and India. Japan's single-payer system already covers subretinal implants under high-cost medical-expense subsidies, creating steady pipeline volume. South Korea's Health Technology Assessment body recently green-lit partial reimbursement for suprachoroidal prototypes, catalyzing domestic production grants. Urban-rural disparities remain acute; telemedicine follow-up is therefore integrated into most new rollout plans.

Europe shows gradual, policy-anchored growth. Germany's DRG codes reimburse both implantation and programming sessions, while France bundles post-operative rehabilitation in its regional health budgets. The United Kingdom's NICE is reevaluating cost-utility metrics for advanced wireless systems after early real-world evidence suggested higher quality-adjusted life-year gains than legacy wired models. EMA's Advanced Therapy fast track overlaps with national device dossiers, occasionally prolonging market entry but ensuring rigorous safety oversight.

- Second Sight Medical Products

- Pixium Vision SA

- VisionCare

- Nano Retina

- Retina Implant AG

- Bionic Vision Technologies (BVT)

- iBIONICS

- Intelligent Implants Ltd.

- LambdaVision, Inc.

- Optobionics Corp.

- iSight Technologies

- Nidek

- Boston Retinal Implant Project

- i-Med Technology Inc.

- GenSight Biologics

- Korey Implant Technologies

- Biomedical Innovations Pty Ltd.

- Shanghai NIDEK Ophthalmic Products

- Vivani Medical

- Advanced Bionics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Burden Of Vision Loss

- 4.2.2 Technological Innovations In Neuroprosthetics

- 4.2.3 Favorable Regulatory And Reimbursement Climate

- 4.2.4 Growing Geriatric Population

- 4.2.5 Increasing Investments In Ophthalmic R&D

- 4.2.6 Expanding Healthcare Infrastructure In Emerging Markets

- 4.3 Market Restraints

- 4.3.1 High Cost Of Devices And Procedures

- 4.3.2 Limited Clinical Efficacy And Patient Outcomes

- 4.3.3 Complex Regulatory And Manufacturing Challenges

- 4.3.4 Availability Of Alternative Vision Restoration Therapies

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers/Consumers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Implant Type

- 5.1.1 Epiretinal Implants (e.g., Argus II)

- 5.1.2 Subretinal Implants (e.g., Alpha AMS)

- 5.1.3 Suprachoroidal Implants

- 5.1.4 Implantable Miniature Telescope (IMT)

- 5.1.5 Other Implant Types

- 5.2 By Disease Indication

- 5.2.1 Retinitis Pigmentosa

- 5.2.2 Age-related Macular Degeneration

- 5.2.3 Stargardt Disease

- 5.2.4 Other Disease Indications

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialty Ophthalmic Clinics

- 5.3.3 Academic & Research Centers

- 5.4 By Technology

- 5.4.1 Wireless Powered Systems

- 5.4.2 Wired / Trans-scleral Cable Systems

- 5.4.3 Adaptive Image Processing & AI Integration

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Second Sight Medical Products, Inc.

- 6.3.2 Pixium Vision SA

- 6.3.3 VisionCare, Inc.

- 6.3.4 Nano Retina

- 6.3.5 Retina Implant AG

- 6.3.6 Bionic Vision Technologies (BVT)

- 6.3.7 iBIONICS

- 6.3.8 Intelligent Implants Ltd.

- 6.3.9 LambdaVision, Inc.

- 6.3.10 Optobionics Corp.

- 6.3.11 iSight Technologies

- 6.3.12 NIDEK Co., Ltd.

- 6.3.13 Boston Retinal Implant Project

- 6.3.14 i-Med Technology Inc.

- 6.3.15 GenSight Biologics

- 6.3.16 Korey Implant Technologies

- 6.3.17 Biomedical Innovations Pty Ltd.

- 6.3.18 Shanghai NIDEK Ophthalmic Products

- 6.3.19 Vivani Medical

- 6.3.20 Advanced Bionics AG

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment