|

시장보고서

상품코드

1846289

miRNA 시퀀싱 및 어세이 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)MiRNA Sequencing And Assay - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

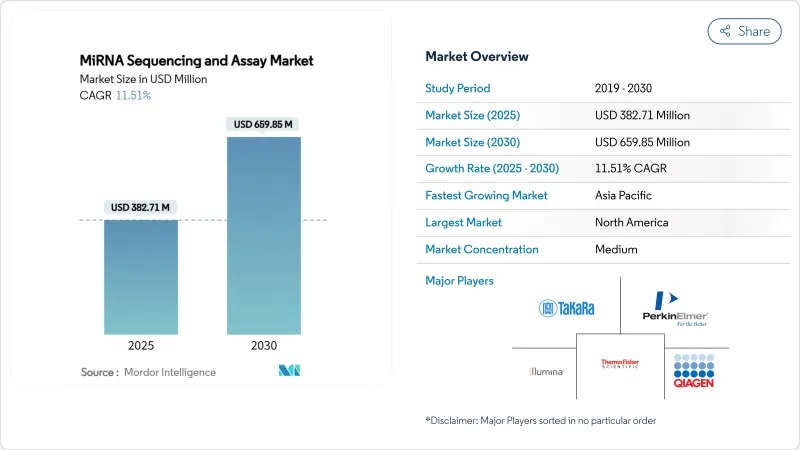

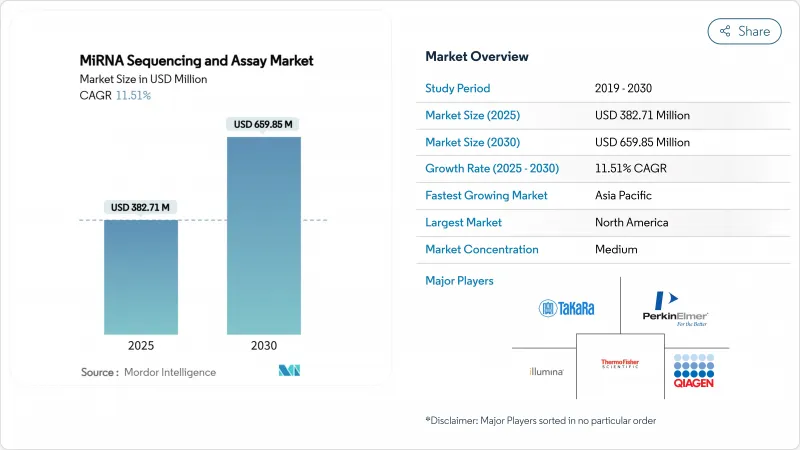

miRNA 시퀀싱 및 어세이 시장 규모는 2025년에 3억 8,271만 달러로 추정되고, 2030년에는 6억 5,985만 달러에 이를 전망이며, CAGR 11.51%로 상승할 것으로 예측됩니다.

시퀀싱 비용의 감소, 실험실 개발 검사에서 규제의 명확화, 액체 생검 진단의 급속한 보급이 이 확대를 뒷받침합니다. 북미가 지역별로 최대 규모를 유지하는 한편, 아시아태평양은 중국의 유전체학 인프라의 규모 확대에 따라 가장 빠르게 성장하고 있습니다. 옥스포드 나노포어의 직접 RNA 단편의 정밀도 중앙값 98.8%와 같은 정밀도의 향상은 임상 검증 사이클을 단축하고 병원의 검사실을 끌어들입니다. 제약 회사는 miRNA 패널을 의약품 워크플로우에 통합하고 인공지능 바이오인포매틱스 도구는 데이터 분석 시간을 며칠에서 몇 시간으로 단축합니다. 기업 인수는 기존 기업과 신규 진출 기업이 샘플 단가의 인하와 멀티오믹스 제품의 확충을 경쟁하는 경쟁 환경의 격화를 부각하고 있습니다.

세계의 miRNA 시퀀싱 및 어세이 시장 동향 및 인사이트

분자 진단에서 차세대 시퀀서의 이점

차세대 시퀀서는 현재 miRNA 분석에서 임상 수준의 정확성을 실현하고 있습니다. 옥스포드 나노포어의 직접 RNA 워크플로우는 50개 염기 단편의 중앙값 98.8%의 정확도를 보고하고, 증폭 바이어스를 제거하며, 병원의 품질 임계값을 충족합니다. 2024년 FDA에 의한 일루미나의 TruSight Oncology Comprehensive 검사 승인은 NGS 동반진단의 선례를 수립했습니다. 검증 연구에 따르면, 다중암 miRNA 패널은 99% 이상의 특이성을 유지하면서 9개의 종양 유형으로 90% 이상의 감도를 나타냅니다. 자동화된 샘플 전처리 및 실시간 분석을 통해 결과 제공은 몇 주에서 몇 시간으로 단축되고 암 클리닉에서 일상적인 채용을 장려합니다.

유전체학 연구를 위한 공적 및 민간 자금 확대

NIH-NSF 이니셔티브가 나노포어 강화를 포함한 RNA 기술 프로젝트에 1,540만 달러를 기여했습니다. 노발티스는 레글루스 세라퓨틱스를 인수하여 치료 포트폴리오를 강화하고 miRNA 기반 의약품에 대한 업계의 헌신을 명확히 했습니다. 산학 컨소시엄은 조직의 전문 지식과 상업적 능력을 결합하여 지속적인 연구 프로그램을 촉진합니다. 비슷한 자금 흐름은 유럽의 Horizon 구상과 유럽과 미국의 의존을 줄이기 위해 정부가 국내 플랫폼을 지원하는 아시아태평양에서도 볼 수 있습니다.

시퀀싱 플랫폼 및 부속 장비에 대한 고액 설비 투자

최상급 장비는 수십만 달러, 서비스 계약 및 소모품도 소요되므로 자원에 제한이 있는 환경에서의 전개가 제한됩니다. FDA 품질 시스템 규칙은 컴플라이언스 오버헤드를 추가합니다. 시퀀싱 아즈 어 서비스 모델은 완화 조치를 제공하지만 데이터 지연과 보안에 대한 우려가 있기 때문에 일부 병원에서는 도입이 연기되고 있습니다.

부문 분석

시퀀싱 소모품은 2024년 miRNA 시퀀싱 및 어세이 시장의 46.43%를 차지하였고, 시약 판매의 경상적인 성질을 뒷받침하고 있습니다. miRNA 시퀀싱 및 어세이 시장 규모에 대한 소모품의 기여는 제조업체가 키트를 장비에 번들로 하여 로열티를 확보하기 때문에 2030년까지 높은 수준으로 추이할 것으로 예측됩니다. 바이오인포매틱스 서비스는 CAGR 13.54%로 가장 빠르게 성장하지만, 이는 많은 실험실이 복잡한 분석을 전문 공급업체에 아웃소싱하는 것을 선호하기 때문입니다. 이 아웃소싱 동향은 확장 가능한 스토리지와 표준화된 파이프라인을 보장하는 클라우드 네이티브 공급자에게 이익을 제공합니다. 자동화 가능 시약 제제는 또한 기술자의 시간을 줄이고 재현성을 향상시킵니다.

소모품의 이점은 시퀀싱 실행마다 소비되는 플로우 셀 및 라이브러리 키트에 대한 일정한 수요에 달려 있습니다. 동시에 서비스 제공업체는 턴어라운드 및 컴플라이언스 문서화를 통해 차별화를 도모하고 있으며 장비 가격이 하락하더라도 수익성이 높은 틈새 시장을 열고 있습니다. 소프트웨어 구독으로의 이동은 물리적 시약 판매를 보완하고 공급업체가 하드웨어 교체 주기에 관련된 수익 변동을 원활하게 하는 데 도움이 됩니다.

시퀀싱 바이 신세시스는 성숙한 케미스트리와 광범위한 인포매틱스 지원으로 2024년 miRNA 시퀀싱 및 어세이 시장 점유율의 62.54%를 차지했습니다. 이 방법은 충분히 검증된 워크플로우를 중시하는 임상 실험실에서 계속 정착하고 있습니다. 나노포어 플랫폼은 역전사를 우회하는 직접 RNA 리드를 가능하게 하고, 기능 연구에 중요한 네이티브 수식을 유지하는 것으로, CAGR 13.89%로 확대될 전망입니다.

나노포어 유닛은 특히 분산된 환경에서 신속한 결과와 낮은 자본 임계값을 요구하는 사용자에게 호소합니다. 실시간 스트리밍은 긴급 질환 감시에도 적합합니다. SBS 벤더는 시장에서의 지위를 지키기 위해 더 높은 처리량 모델과 번들된 인포매틱스로 대응하고 있습니다. 하이브리드 시설은 비용, 속도 및 읽기 시간의 균형을 맞추기 위해 두 가지 양식을 모두 도입했습니다.

지역 분석

북미는 2024년 miRNA 시퀀싱 및 어세이 시장 매출의 42.43%를 차지하며 NIH-NSF의 1,540만 달러의 RNA 이니셔티브와 진단 승인을 단축하는 FDA의 로드맵에 지원되고 있습니다. 분자 분석의 상환 경로와 강력한 벤처 캐피탈의 흐름은 병원에서의 채용을 뒷받침하고 있습니다. 노발티스-레글루스와 같은 대규모 인수는 이 지역의 전문지식과 자본을 더욱 집중시킵니다.

아시아태평양은 2030년까지 CAGR 12.54%로 성장이 전망되며, 중국의 생산 능력 확대와 MGI의 DNBSEQ와 같은 국내 플랫폼에 대한 조성 정책에 힘쓰고 있습니다. 지역 농업 및 수의학 유전체학 프로젝트가 추가 수요를 제공하는 반면, 지역 신생 기업은 소규모 클리닉을 위해 저비용 시퀀싱 서비스를 제공합니다. 인도와 일본은 개인화된 의료시험에 많은 투자를 하고 있으며 소모품과 바이오인포매틱스의 지속적인 성장을 강화하고 있습니다.

유럽에서는 임상 전개 전에 새로운 증거 요건을 부과하는 IVDR이 진행되는 동안 꾸준한 성장을 보여줍니다. 관민협동의 컨소시엄이 중소이노베이터의 컴플라이언스 비용을 평준화합니다. 각국 정부는 정밀 의료에 대한 조성을 확대하고, miRNA에 기초한 층별화를 이용한 국경을 넘은 임상시험을 지원하고 있습니다. 규제 상의 장애물에도 불구하고 아메리카 대륙에는 강력한 제약 회사가 존재하며 바이오 마커에 대한 새로운 노력이 끊임없이 태어났습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 분자진단에서 차세대 시퀀서의 우위성

- 유전체 연구에 대한 공적 및 민간 자금의 확대

- 시퀀싱 비용 및 소요 시간의 급속한 저하

- 암 이환율의 상승이 리퀴드 바이옵시 바이오 마커 수요 견인

- 새로운 농업 및 수의사 유전체 용도

- miRNA 데이터의 자동 해석에 있어서 인공지능의 채용

- 시장 성장 억제요인

- 시퀀싱 플랫폼 및 부속 기기에 대한 고액의 설비 투자

- 숙련된 바이오인포매틱스 인재 부족

- miRNA 검사의 규제 및 상환 상황의 단편화

- 엄격한 데이터 프라이버시 및 국경을 넘은 유전체 데이터 규제

- 규제 상황

- Porter's Five Forces 분석

- 신규 참가업체의 위협

- 구매자의 협상력

- 공급기업의 협상력

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 시장 규모 및 성장 예측

- 제품별

- 시퀀싱 소모품

- 라이브러리 준비 키트

- 시퀀싱 플랫폼 및 기기

- 바이오인포매틱스 파이프라인 및 서비스

- 기술별

- 합성에 의한 시퀀싱(SBS)

- 이온 반도체

- SOLiD

- 나노포어 시퀀싱

- 단일 분자 실시간(SMRT)

- 용도별

- 종양 진단 및 리퀴드 바이옵시

- 창약 및 트랜스 크림 연구

- 기타 용도

- 최종 사용자별

- 임상연구소

- 학술기관 및 연구기관

- 바이오테크놀러지 및 제약회사

- 수탁연구기관

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 기타 아시아태평양

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Illumina Inc.

- Thermo Fisher Scientific

- QIAGEN NV

- PerkinElmer Inc.

- Takara Bio Inc.

- New England Biolabs

- Norgen Biotek

- TriLink Biotechnologies

- Lexogen GmbH

- Oxford Nanopore Technologies

- Agilent Technologies

- BGI/MGI Tech

- Pacific Biosciences

- NanoString Technologies

- MedGenome

- SomaGenics

- CD Genomics

- Illumina(BlueBee Bioinformatics)

- Guardant Health

- Eurofins Genomics

제7장 시장 기회 및 전망

AJY 25.11.10The miRNA sequencing and assay market size stands at USD 382.71 million in 2025 and is forecast to reach USD 659.85 million by 2030, rising at an 11.51% CAGR.

Declining sequencing costs, regulatory clarity in laboratory-developed tests, and rapid uptake of liquid biopsy diagnostics steer this expansion. North America retains the largest regional footprint, while Asia-Pacific posts the quickest gains as Chinese genomics infrastructure scales. Accuracy gains such as Oxford Nanopore's 98.8% median precision for direct RNA fragments shorten clinical validation cycles and attract hospital laboratories. Pharmaceutical companies integrate miRNA panels into drug discovery workflows, and artificial-intelligence bioinformatics tools cut data-analysis time from days to hours. Corporate acquisitions underline an intensifying competitive climate as incumbents and new entrants race to lower per-sample prices and broaden multiomics offerings.

Global MiRNA Sequencing And Assay Market Trends and Insights

Dominance of Next-Generation Sequencing in Molecular Diagnostics

Next-generation sequencing now delivers clinical-grade precision in miRNA analysis. Oxford Nanopore's direct RNA workflow reports 98.8% median accuracy for 50-nucleotide fragments, removing amplification biases and meeting hospital quality thresholds. The FDA's 2024 clearance of Illumina's TruSight Oncology Comprehensive test established a precedent for NGS companion diagnostics. Validation studies show multi-cancer miRNA panels surpass 90% sensitivity across nine tumor types while keeping specificity above 99%. Automated sample prep and real-time analytics shrink result delivery from weeks to hours, encouraging routine adoption in oncology clinics.

Expanding Public and Private Funding for Genomics Research

An NIH-NSF initiative dedicates USD 15.4 million to RNA technology projects, including nanopore enhancements. Novartis strengthened its therapeutic portfolio by acquiring Regulus Therapeutics, underscoring industry commitment to miRNA-based drugs. Academic-industry consortia combine institutional expertise with commercial capacity, fostering sustained research programs. Similar capital flows appear in Europe's Horizon initiatives and in Asia-Pacific where governments back domestic platforms to lessen Western dependence.

High Capital Expenditure for Sequencing Platforms and Ancillary Equipment

Top-tier instruments cost hundreds of thousands of dollars, plus service contracts and consumables, limiting uptake in resource-constrained settings. FDA quality-system rules add compliance overhead. Sequencing-as-a-service models offer relief yet introduce concerns over data latency and security, causing some hospitals to defer adoption.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Decline in Sequencing Costs and Turnaround Time

- Rising Cancer Incidence Driving Demand for Liquid-Biopsy Biomarkers

- Shortage of Skilled Bioinformatics Workforce

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sequencing consumables generated 46.43% of the miRNA sequencing and assay market in 2024, underlining the recurring nature of reagents sales. The consumable contribution to miRNA sequencing and assay market size is expected to stay high through 2030 as manufacturers bundle kits with instruments to lock in loyalty. Bioinformatics services grow the fastest at a 13.54% CAGR because many laboratories prefer outsourcing complex analytics to specialized vendors. This outsourcing trend benefits cloud-native providers that guarantee scalable storage and standardized pipelines. Automation-ready reagent formulations also cut technician time and bolster reproducibility.

Consumables' dominance rests on constant demand for flow cells and library kits each sequencing run consumes. At the same time, service providers differentiate on turnaround and compliance documentation, carving out profitable niches even as instrument prices fall. The movement toward software subscriptions complements physical reagent sales and helps vendors smooth revenue swings tied to hardware replacement cycles.

Sequencing-by-synthesis delivered 62.54% of miRNA sequencing and assay market share in 2024 thanks to mature chemistries and broad informatics support. The method remains entrenched in clinical laboratories that value well-validated workflows. Nanopore platforms expand at a 13.89% CAGR by enabling direct RNA reads that bypass reverse transcription, preserving native modifications important for functional studies.

Nanopore units appeal to users seeking rapid results and lower capital thresholds, especially in decentralized settings. Their real-time streaming also fits emergency disease surveillance. SBS vendors respond with higher throughput models and bundled informatics to defend market position. Hybrid facilities now deploy both modalities to balance cost, speed, and read-length requirements across research and diagnostic tasks.

The MiRNA Sequencing and Assay Market Report is Segmented by Product (Sequencing Consumables, and More), Technology (Sequencing by Synthesis, and More), Application (Oncology Diagnostics/Liquid Biopsy, and More), End User (Clinical Laboratories, and More), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America contributed 42.43% of 2024 revenue to the miRNA sequencing and assay market, anchored by the NIH-NSF USD 15.4 million RNA initiative and an FDA roadmap that shortens diagnostic approvals. Reimbursement pathways for molecular assays and strong venture capital flows encourage hospital adoption. Major acquisitions such as Novartis-Regulus further concentrate expertise and capital in the region.

Asia-Pacific advances at a 12.54% CAGR to 2030, propelled by Chinese capacity expansion and policies that subsidize domestic platforms like MGI's DNBSEQ, which targets a USD 10 genome. Regional agricultural and veterinary genomics projects provide additional demand, while local start-ups offer lower-cost sequencing services for small clinics. India and Japan invest heavily in personalized-medicine trials, reinforcing sustained consumable and bioinformatics growth.

Europe shows steady gains amid IVDR implementation, which imposes new evidence requirements before clinical rollout. Collaborative public-private consortia smooth compliance costs for smaller innovators. Governments widen precision-medicine funding and support cross-border clinical trials using miRNA-based stratification. Despite regulatory hurdles, the continent retains a strong pharmaceutical footprint that continually seeds new biomarker initiatives.

- Illumina

- Thermo Fisher Scientific

- QIAGEN

- PerkinElmer

- Takara Bio

- New England Biolabs

- Norgen Biotek

- TriLink Biotechnologies

- Lexogen GmbH

- Oxford Nanopore Technologies

- Agilent Technologies

- BGI / MGI Tech

- Pacific Biosciences

- NanoString Technologies

- MedGenome

- SomaGenics

- CD Genomics

- Illumina (BlueBee Bioinformatics)

- Guardant Health

- Eurofins

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Dominance of Next-Generation Sequencing in Molecular Diagnostics

- 4.2.2 Expanding Public and Private Funding for Genomics Research

- 4.2.3 Rapid Decline in Sequencing Costs and Turnaround Time

- 4.2.4 Rising Cancer Incidence Driving Demand for Liquid Biopsy Biomarkers

- 4.2.5 Emerging Agricultural and Veterinary Genomic Applications

- 4.2.6 Adoption of Artificial Intelligence for Automated MiRNA Data Interpretation

- 4.3 Market Restraints

- 4.3.1 High Capital Expenditure for Sequencing Platforms and Ancillary Equipment

- 4.3.2 Shortage of Skilled Bioinformatics Workforce

- 4.3.3 Fragmented Regulatory and Reimbursement Landscape for MiRNA Tests

- 4.3.4 Stringent Data-Privacy and Cross-Border Genomic Data Restrictions

- 4.4 Regulatory Landscape

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Product

- 5.1.1 Sequencing Consumables

- 5.1.2 Library Preparation Kits

- 5.1.3 Sequencing Platforms / Instruments

- 5.1.4 Bioinformatics Pipelines & Services

- 5.2 By Technology

- 5.2.1 Sequencing by Synthesis (SBS)

- 5.2.2 Ion Semiconductor

- 5.2.3 SOLiD

- 5.2.4 Nanopore Sequencing

- 5.2.5 Single-Molecule Real-Time (SMRT)

- 5.3 By Application

- 5.3.1 Oncology Diagnostics / Liquid Biopsy

- 5.3.2 Drug Discovery & Transcriptome Research

- 5.3.3 Other Applications

- 5.4 By End User

- 5.4.1 Clinical Laboratories

- 5.4.2 Academic & Research Institutes

- 5.4.3 Biotech / Pharma Companies

- 5.4.4 Contract Research Organizations

- 5.5 Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Business Segments, Financials, Headcount, Key Information, Market Rank, Market Share, Products and Services, and analysis of Recent Developments)

- 6.3.1 Illumina Inc.

- 6.3.2 Thermo Fisher Scientific

- 6.3.3 QIAGEN N.V.

- 6.3.4 PerkinElmer Inc.

- 6.3.5 Takara Bio Inc.

- 6.3.6 New England Biolabs

- 6.3.7 Norgen Biotek

- 6.3.8 TriLink Biotechnologies

- 6.3.9 Lexogen GmbH

- 6.3.10 Oxford Nanopore Technologies

- 6.3.11 Agilent Technologies

- 6.3.12 BGI / MGI Tech

- 6.3.13 Pacific Biosciences

- 6.3.14 NanoString Technologies

- 6.3.15 MedGenome

- 6.3.16 SomaGenics

- 6.3.17 CD Genomics

- 6.3.18 Illumina (BlueBee Bioinformatics)

- 6.3.19 Guardant Health

- 6.3.20 Eurofins Genomics

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment