|

시장보고서

상품코드

1846306

인공 성대 시장 : 시장 점유율 분석, 산업 동향, 통계, 성장 예측(2025-2030년)Global Voice Prosthesis Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030) |

||||||

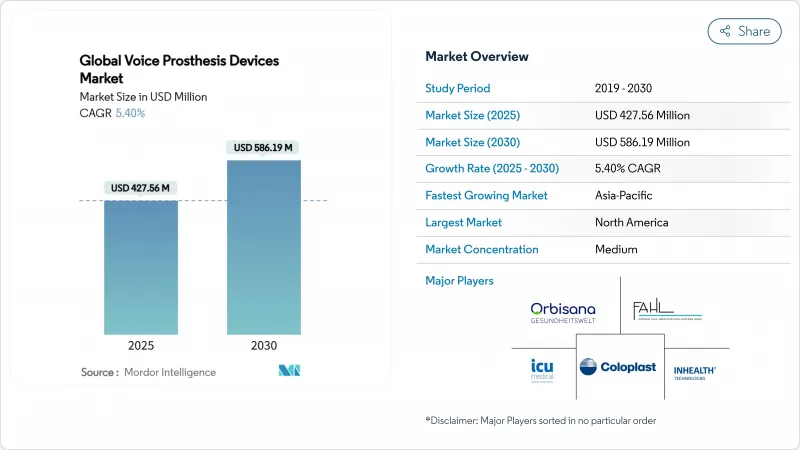

인공 성대 시장 규모는 2025년에 4억 2,756만 달러로 추정되고, 2030년에는 5억 8,619만 달러에 이를 것으로 예측되며, 예측 기간 동안 CAGR 5.40%로 확대될 전망입니다.

바이오필름 내성 밸브 재료의 꾸준한 진보, 고소득 지역의 광범위한 상환, 후두 절제술의 생존자 증가가 인공 성대 시장의 이 궤도를 유지하고 있습니다. 북미가 가장 큰 수익 기반을 유지하고 있지만 국내 업체들이 지역 예산에 맞는 저가 제품을 출시하기 때문에 아시아태평양이 가장 빠르게 성장하고 있습니다. 규제 수렴, 특히 FDA의 품질 시스템 규칙이 2026년 ISO 13485와 일치함에 따라 규정 준수 비용이 상승하지만 여러 지역의 등록 주기가 단축되고 더 빠른 출시가 가능합니다. 이와 병행하여, 이비인후과 수술의 외래 환자로의 전환은 연간 교환 대수를 증가시키는 한편 가격 감응도를 높입니다.

세계의 인공 성대 시장 동향 및 인사이트

후두암 및 후두 총 절제술의 발생률 증가

인구 기반 데이터에 따르면 미국에서는 2000-2020년 10만 4,991명의 환자가 발생했으며, 이 수치는 인구 고령화에 따라 증가할 것으로 예측됩니다. 유럽과 아시아에서도 비슷한 증가 경향이 있으며, 2040년까지 하인두암이 50% 증가할 것으로 예측되고 있습니다. 후두 적출술을 받은 사람의 70-75%가 인공 성대 후보자가 되기 때문에 이환 동향은 직접 수요로 변환되어 인공 성대 시장의 성장 곡선을 강화합니다.

보철물의 수명을 연장하는 기술의 진보

차세대 실리콘 블렌드, 소수성 코팅, 자석 어시스트 클로저는 초기 연구에서 기능 수명을 6개월에서 12개월로 두 배로 늘렸습니다 (ATOSMEDICAL.COM). 맞춤형 3D 프린팅 플랜지는 장착과 관련된 누출을 줄이고 항균 표면은 곰팡이 정착을 지연시킵니다. 이러한 개선은 교환 빈도와 총 소유 비용을 낮추고 선진국 시장의 임상의가 유치형을 보다 쉽게 추천하게 되어 인공 성대 시장 전체의 수익 기세가 지속됩니다.

외래 이비인후과 수술의 성장

외래센터는 2022년 330만 명의 메디케어 유료 서비스 수혜자들에게 서비스를 제공하였고, 지출은 61억 달러에 이르렀습니다. 이비인후과 팀에서는 당일 퇴원을 가능하게 하는 개선된 역행성 삽입술의 사용이 증가하고 있습니다. 시설 비용의 감소는 지불자에게 호소하고, 편리성은 환자를 유치하며, 더 많은 교환을, 나아가서 시장의 수익을, 인공 성대 시장의 높은 스루풋 외래 채널에 밀어 올리고 있습니다.

부문 분석

유치 밸브는 2024년 인공 성대 시장 점유율의 73.75%를 차지했습니다. 이 부문와 관련된 인공 성대 시장 규모는 재료 개선에 의해 관리되는 코호트에서의 체류 시간이 1년이 되기 때문에 CAGR 5.1%를 보일 것으로 예측됩니다. 유치형 시스템은 전문가 교환이 필요하며 병원 및 전문 클리닉 워크플로우에 원활하게 적합합니다. 비침투형 장치는 CAGR 6.05%를 기록하며 특히 원격 재활이 활발한 시장에서 자율성을 중시하는 자기 관리 환자에게 어필합니다. 전기 후두 장치와 신흥 3D 프린터 밸브는 표준 플랜지에서 사용할 수 없는 해부학적 구조의 임상적 격차를 메우지만 그 점유율은 여전히 5% 미만입니다.

외과의사가 보고한 1차 천자의 성공률은 76.2%로, 2차 천자의 성공률은 81.8%로 상승했지만 합병증은 더 높습니다(IJORL.COM). 미국 보험사는 3-6개월 간격으로 유치형 인공 혈관 교환을 환불하고 예측 가능한 주문 주기를 유지하고 있습니다. 자원에 제한이 있는 지역에서는 혁신자가 100달러 이하의 저렴한 밸브를 판매하고, 접근을 확대하며, 판매량의 변동을 완화하고 있습니다. 이러한 동향은 틈새 성장 벡터를 키우면서 유치형 리더십을 확보하고 인공 성대 시장의 다양성 및 안정성을 유지하고 있습니다.

인공 성대 시장 보고서는 기관 유형별(유치형, 비유치형, 전기 후두, 맞춤형 3D 인쇄), 밸브 유형별(Provox, Blom-Singer, Activalve, Groningen, Aum, Specialty Custom), 최종 사용자별(병원, 전문 클리닉, Ascs, 홈 케어), 지역별(북미, 유럽, 아시아태평양, 남미, MEA)로 구분합니다. 시장 예측은 금액(달러)으로 제공됩니다.

지역별 분석

북미의 선진적인 상환 환경이 예측 가능한 수요를 지원하고 있습니다. 메디케어의 내구 소비재 규칙에서는 누출이나 열화가 증명된 경우 연간 2회의 유치 교환이 인정되고 있습니다. 미국에는 13개의 후두 적출술 전문센터가 있으며 세계적으로 영향력 있는 결과 데이터를 공표하고 있습니다. 캐나다에서는 주가 자금을 제공하는 시스템이 동등한 접근을 제공하고 있으며, 카리브해 지역의 환자들은 플로리다 센터까지 발길을 옮기고 서비스를 제공하는 인구를 조금씩 늘리고 있습니다.

아시아태평양의 가속은 정책과 생산에 기인합니다. 인도의 의료 제도, 중국의 신속한 승인, 일본의 초고령화 사회는 모두 후보자 수를 확대하고 있습니다. 국내 제조는 랜드메이드 비용을 40-60% 삭감하여 연간 교환 어드히어런스의 향상으로 이어집니다. 'Healthy China 2030'의 조기 발견 프로그램은 수술 가능한 종양 수를 증가시키고 인공 성대 시장의 사용자 풀을 추가로 보충합니다.

유럽의 유니버설 시스템은 접근을 보장하면서 가격 협상을 적극적으로 수행하고 있습니다. 독일의 진단 관련 그룹의 개선은 내시경으로 대체술에 점수를 더하고 병원의 경제성을 향상시킵니다. 프랑스의 'assurance maladie'는 소매 가격으로 의료기기에 환불을 실시하지만, 긴축 재정에 의해 의사는 비용에 신경 쓰고 있습니다. NHS는 밸브를 고비용 탈리프 제외 목록에 포함하고 진료 보상에 상한을 설정하는 한편, 수량은 유지하고 있습니다. Brexit과 관련된 물류 혼란은 완화되고 재고 버퍼는 현재 영국 환자를 공급 부족 위험으로부터 보호하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 후두암 및 후두 전적술의 이환율 증가

- 기술의 진보에 의한 인공 후두의 수명 연장

- 고소득 국가의 상환 범위 확대

- 외래에서 이비인후과에 특화한 수술 건수 증가

- 가격에 민감한 아시아에서 저가격의 국산 인공 밸브 채용

- 부가 제조에 의한 커스텀 밸브의 피트감 및 쾌적성 향상

- 시장 성장 억제요인

- 신흥 시장에서 고액의 교환 비용 및 한정된 보험

- 디바이스 관련 합병증(누설, 바이오필름, 오연)

- 엄격한 멸균 및 공급망 규제에 의한 비용 증가

- 저자원 지역에서 훈련된 TEP 외과의의 부족

- 밸류체인 및 공급망 분석

- 규제 상황

- 기술적 전망

- Porter's Five Forces 분석

- 협상력-공급 기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

제5장 세분화

- 디바이스 유형별

- 기관식도 유치형 인공 성대

- 비유치형 기관식도 인공 성대

- 전기 후두 및 인공 성대

- 커스텀 3D 프린팅 음성 밸브

- 밸브 유형

- Provox 시리즈 밸브

- Blom-Singer 시리즈 밸브

- ActiValve 자기 밸브

- 플로닝겐 밸브

- 옴 보이스 보철

- 특수 커스텀 밸브(Kapitex, Hood 등)

- 최종 사용자별

- 병원

- 이비인후과 전문 클리닉

- 외래수술센터(ASC)

- 재택 치료 및 환자 직접 판매 채널

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 기타 남미

- 중동 및 아프리카

- GCC

- 남아프리카

- 기타 중동 및 아프리카

- 북미

제6장 경쟁 구도

- 시장 집중도

- 시장 점유율 분석

- 기업 프로파일

- Atos Medical(Coloplast A/S)

- InHealth Technologies(Freudenberg Medical)

- Hood Laboratories

- Kapitex Healthcare Ltd.

- Teleflex Incorporated

- TRACOE medical GmbH

- Servona GmbH

- Andreas Fahl Medizintechnik-Vertrieb GmbH

- Smiths Medical(ICU Medical)

- Boston Medical Products Inc.

- Griffin Laboratories

- Soluvos Medical BV

- Beijing Tellyes Scientific Inc.

- Innaumation Medical Devices Pvt Ltd.

- Medtronic plc

- Johnson & Johnson(Acclarent)

- Nu-Vois Inc.

- La Maison Medicale

- Amplivox Ltd.

- Bruce Medical Supply Corp.

제7장 시장 기회 및 전망

AJY 25.11.10The voice prosthesis devices market size is valued at USD 427.56 million in 2025 and is projected to reach USD 586.19 million by 2030, expanding at a 5.40% CAGR during the forecast period .

Steady progress in biofilm-resistant valve materials, broader reimbursement in high-income regions and a rising pool of laryngectomy survivors sustain this trajectory for the voice prosthesis devices market. North America keeps the largest revenue base, yet Asia-Pacific posts the quickest gains as domestic manufacturers introduce lower-priced products adapted to regional budgets. Regulatory convergence-most notably the 2026 alignment of the FDA's quality-system rule with ISO 13485-raises compliance costs but shortens multi-region registration cycles, enabling quicker launches. In parallel, the migration of ENT procedures to outpatient settings multiplies yearly replacement volumes while intensifying price sensitivity.

Global Voice Prosthesis Devices Market Trends and Insights

Rising Incidence of Laryngeal Cancer and Total Laryngectomies

Population-based data show 104 991 U.S. cases between 2000-2020, a figure expected to escalate as the population ages. Europe and Asia present similar upward trends, and forecasts point to a 50% rise in hypopharyngeal cancer by 2040. Because 70-75% of laryngectomy survivors become candidates for a prosthetic voice, incidence trends convert directly into demand, reinforcing the growth curve of the voice prosthesis devices market.

Technological Advances Extending Prosthesis Lifetime

Next-generation silicone blends, hydrophobic coatings and magnet-assisted closures double functional life from six to twelve months in early studies [ATOSMEDICAL.COM]. Custom 3-D-printed flanges reduce fit-related leakage, while antimicrobial surfaces slow fungal colonisation. These improvements lower replacement frequency and total cost of ownership, encouraging clinicians in developed regions to recommend indwelling models more readily and sustaining revenue momentum across the voice prosthesis devices market.

Outpatient ENT Surgery Growth

Ambulatory centres served 3.3 million Medicare fee-for-service beneficiaries in 2022, with USD 6.1 billion in spending.. ENT teams increasingly use modified retrograde insertion techniques that allow same-day discharge. Lower facility costs appeal to payers, while convenience attracts patients, pushing more replacements-and thus market revenue-into high-throughput outpatient channels of the voice prosthesis devices market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Reimbursement Coverage in High-Income Countries

- High Replacement Cost and Limited Insurance in Emerging Markets

- Device-Related Complications (Leakage, Biofilm, Aspiration)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Indwelling valves represented 73.75% of voice prosthesis devices market share in 2024. The voice prosthesis devices market size tied to this segment is forecast to grow at 5.1% CAGR as upgraded materials push dwell time to a year in controlled cohorts. Indwelling systems demand professional replacement, fitting seamlessly into hospital and specialty-clinic workflows. Non-indwelling devices-posting a 6.05% CAGR-appeal to self-managing patients who value autonomy, especially in markets with robust tele-rehabilitation. Electrolarynx units and emerging 3-D-printed valves fill clinical gaps for anatomies unsuited to standard flanges, but their collective share remains below 5%.

Surgeon-reported primary-puncture success rates hover at 76.2%, climbing to 81.8% for secondary puncture though with higher complications [IJORL.COM]. U.S. insurers reimburse indwelling replacements at three- to six-month intervals, sustaining predictable order cycles. In resource-constrained regions, innovators market budget valves under USD 100, broadening access and buffering volume volatility. These trends collectively ensure indwelling leadership while fostering niche growth vectors, keeping the voice prosthesis devices market diversified yet stable.

The Voice Prosthesis Device Market Report is Segmented by Device Type (Indwelling, Non-Indwelling, Electrolarynx, Custom 3D-Printed), Valve Types (Provox, Blom-Singer, Activalve, Groningen, Aum, Specialty Custom), End User (Hospitals, Specialty Clinics, Ascs, Homecare), and Geography (North America, Europe, Asia-Pacific, South America, MEA). Market Forecasts are Provided in Value (USD).

Geography Analysis

North America's advanced reimbursement environment underpins predictable demand. Medicare's durable equipment rules authorise two indwelling replacements yearly when leakage or degradation is documented . The United States houses 13 dedicated laryngectomy centres that publish outcome data influential worldwide. Canada's provincially funded system provides comparable access, and Caribbean patients travel to Florida centres, incrementally enlarging the served population.

Asia-Pacific's acceleration stems from policy and production. India's Health Scheme, China's fast-track approvals and Japan's super-aged society all expand candidate numbers. Domestic manufacturing cuts landed cost by 40-60%, translating into higher annual replacement adherence. Early detection programs under Healthy China 2030 are set to lift operable tumour counts, further replenishing the user pool for the voice prosthesis devices market.

Europe's universal systems guarantee access yet negotiate aggressively on price. Germany's diagnosis-related group refinements add points for endoscopic replacements, improving hospital economics. France's assurance maladie reimburses devices at retail price, but austerity keeps physicians mindful of cost. The NHS includes valves on its High Cost Tariff Excluded list, sustaining volume while capping reimbursement. Logistics disruptions tied to Brexit have eased, and stock buffers now shield UK patients from shortage risk.

- Atos Medical (Coloplast A/S)

- InHealth Technologies (Freudenberg Medical)

- Hood Laboratories

- Kapitex Healthcare Ltd.

- Teleflex

- TRACOE medical

- Servona GmbH

- Andreas Fahl Medical Technology Sales

- Smiths Group

- Boston Medical Center

- Griffin Laboratories

- Soluvos Medical BV

- Beijing Tellyes Scientific Inc.

- Innaumation Medical Devices Pvt Ltd.

- Medtronic

- Johnson & Johnson (Acclarent)

- Nu-Vois Inc.

- La Maison Medicale

- Amplivox Ltd.

- Bruce Medical Supply Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of laryngeal cancer and total laryngectomies

- 4.2.2 Technological advances extending prosthesis lifetime

- 4.2.3 Expanding reimbursement coverage in high-income countries

- 4.2.4 Growing ENT-focused surgical volumes in outpatient settings

- 4.2.5 Adoption of low-cost indigenous prostheses in price-sensitive Asia

- 4.2.6 Additive-manufactured custom valves improving fit & comfort

- 4.3 Market Restraints

- 4.3.1 High replacement costs and limited insurance in emerging markets

- 4.3.2 Device-related complications (leakage, biofilm, aspiration)

- 4.3.3 Stringent sterilization/supply-chain regulations raising COGS

- 4.3.4 Shortage of trained TEP surgeons in low-resource regions

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power - Suppliers

- 4.7.2 Bargaining Power - Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Segmentation

- 5.1 Device Type

- 5.1.1 Indwelling Tracheoesophageal Voice Prosthesis

- 5.1.2 Non-Indwelling Tracheoesophageal Voice Prosthesis

- 5.1.3 Electrolarynx / Artificial Larynx Devices

- 5.1.4 Custom 3-D Printed Voice Valves

- 5.2 Valve Types

- 5.2.1 Provox Series Valves

- 5.2.2 Blom-Singer Series Valves

- 5.2.3 ActiValve Magnetic Valves

- 5.2.4 Groningen Valve

- 5.2.5 Aum Voice Prosthesis

- 5.2.6 Specialty Custom Valves (Kapitex, Hood etc.)

- 5.3 End User

- 5.3.1 Hospitals

- 5.3.2 Specialty ENT Clinics

- 5.3.3 Ambulatory Surgery Centers

- 5.3.4 Homecare & Direct-to-Patient Channels

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.3.1 Atos Medical (Coloplast A/S)

- 6.3.2 InHealth Technologies (Freudenberg Medical)

- 6.3.3 Hood Laboratories

- 6.3.4 Kapitex Healthcare Ltd.

- 6.3.5 Teleflex Incorporated

- 6.3.6 TRACOE medical GmbH

- 6.3.7 Servona GmbH

- 6.3.8 Andreas Fahl Medizintechnik-Vertrieb GmbH

- 6.3.9 Smiths Medical (ICU Medical)

- 6.3.10 Boston Medical Products Inc.

- 6.3.11 Griffin Laboratories

- 6.3.12 Soluvos Medical BV

- 6.3.13 Beijing Tellyes Scientific Inc.

- 6.3.14 Innaumation Medical Devices Pvt Ltd.

- 6.3.15 Medtronic plc

- 6.3.16 Johnson & Johnson (Acclarent)

- 6.3.17 Nu-Vois Inc.

- 6.3.18 La Maison Medicale

- 6.3.19 Amplivox Ltd.

- 6.3.20 Bruce Medical Supply Corp.